Protect Your House With These Estate Planning Strategies

•

0 recomendaciones•623 vistas

This document summarizes different options for protecting a house, including doing nothing, giving the house to children, selling the house to children, contributing the house to a family limited partnership, using a Qualified Personal Residence Trust, Grantor Retained Annuity Trust, or Private Retirement Trust. It outlines the setup requirements, tax implications, ability of creditors to access the house, rental options, ability to deduct debt, and ability to access equity for each option.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (20)

Similar a Protect Your House With These Estate Planning Strategies

Similar a Protect Your House With These Estate Planning Strategies (20)

Protect Your House With These Estate Planning Strategies

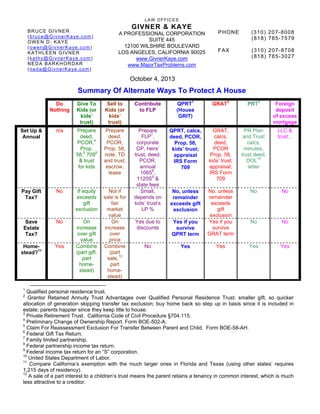

- 1. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION SUITE 445 12100 WILSHIRE BOULEVARD LOS ANGELES, CALIFORNIA 90025 www.GivnerKaye.com www.MajorTaxProblems.com BRUCE GIVNER (bruce@GivnerKaye.com) OWEN D. KAYE (owen@GivnerKaye.com) KATHLEEN GIVNER (kathy@GivnerKaye.com) NEDA BARKHORDAR (neda@GivnerKaye.com) PHONE (310) 207-8008 (818) 785-7579 FAX (310) 207-8708 (818) 785-3027 October 4, 2013 Summary Of Alternate Ways To Protect A House Do Nothing Give To Kids (or kids’ trust) Sell to Kids (or kids’ trust) Contribute to FLP QPRT1 (House GRIT) GRAT2 PRT3 Foreign deposit of excess mortgage Set Up & Annual n/a Prepare deed, PCOR,4 Prop. 58,5 7096 & trust for kids Prepare deed, PCOR, Prop. 58, note, TD and trust; escrow, lease Prepare FLP7 , corporate GP, heirs’ trust, deed, PCOR, annual 10658 , 1120S9 & state fees QPRT, calcs, deed, PCOR, Prop. 58, kids’ trust; appraisal IRS Form 709 GRAT, calcs, deed, PCOR Prop. 58, kids’ trust; appraisal; IRS Form 709 PR Plan and Trust calcs, minutes, trust deed, DOL10 letter LLC & trust; . Pay Gift Tax? No If equity exceeds gift exclusion Not if sale is for fair market value Small, depends on kids’ trust’s LP % No, unless remainder exceeds gift exclusion No, unless remainder exceeds gift exclusion No No Save Estate Tax? No On increase over gift value On increase over price Yes due to discounts Yes if you survive QPRT term Yes if you survive GRAT term No No Home- stead?11 Yes Combine (part gift, part home- stead) Combine (part sale,12 part home- stead) No Yes Yes Yes Yes 1 Qualified personal residence trust. 2 Grantor Retained Annuity Trust Advantages over Qualified Personal Residence Trust: smaller gift, so quicker allocation of generation skipping transfer tax exclusion; buy home back so step up in basis since it is included in estate; parents happier since they keep title to house. 3 Private Retirement Trust. California Code of Civil Procedure §704.115. 4 Preliminary Change of Ownership Report. Form BOE-502-A. 5 Claim For Reassessment Exclusion For Transfer Between Parent and Child. Form BOE-58-AH. 6 Federal Gift Tax Return. 7 Family limited partnership. 8 Federal partnership income tax return. 9 Federal income tax return for an “S” corporation. 10 United States Department of Labor. 11 Compare California’s exemption with the much larger ones in Florida and Texas (using other states’ requires 1,215 days of residency). 12 A sale of a part interest to a children’s trust means the parent retains a tenancy in common interest, which is much less attractive to a creditor.

- 2. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Summary of Alternate Ways To Protect A House Page 2 of 2 October 4, 2013 Do Nothing Give To Kids (or kids’ trust) Sell to Kids (or kids’ trust) Contribute to FLP QPRT13 (House GRIT) GRAT14 PRT15 Foreign deposit of excess mortgage Can Creditor Get House? Yes No No, but can seize the note No, but can get charging order on your LP units BK Code §548(e)(1) (A): 10 years to challenge BK Code §548(e)(1) (A): 10 years to challenge BK Code §548(e)(1)( A): 10 years to challenge Discourag es those who do asset search You Rent? No not while kids are minors Yes Yes Not until term ends Yes No No You Deduct Debt? Yes Yes if grantor trust16 Yes if grantor trust Your % flows thru Yes Yes Yes Yes You Use Equity? Yes No No Indirectly, through FLP No, unless it is sold Yes Yes Yes 13 Qualified personal residence trust. 14 Grantor Retained Annuity Trust Advantages over Qualified Personal Residence Trust: smaller gift, so quicker allocation of generation skipping transfer tax exclusion; buy home back so step up in basis since it is included in estate; parents happier since they keep title to house. 15 Private Retirement Trust. California Code of Civil Procedure §704.115. 16 A “grantor trust” is an irrevocable trust which is disregarded for income tax purposes. In other words, the parents – as grantors – are taxed on all of the trust’s income. However, the trust is still not included in the parents’ taxable estates. So it is recognized for estate and gift taxes as a separate legal person but disregarded for income tax purposes.