Recomendados

Más contenido relacionado

La actualidad más candente

Destacado

Destacado (20)

Similar a Ias 16 case study 3

Similar a Ias 16 case study 3 (20)

Más de Hyderabad Chapter of ICWAI

Más de Hyderabad Chapter of ICWAI (18)

Último

Último (20)

Ias 16 case study 3

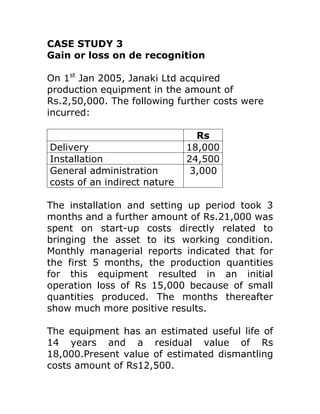

- 1. CASE STUDY 3 Gain or loss on de recognition On 1st Jan 2005, Janaki Ltd acquired production equipment in the amount of Rs.2,50,000. The following further costs were incurred: Rs Delivery 18,000 Installation 24,500 General administration 3,000 costs of an indirect nature The installation and setting up period took 3 months and a further amount of Rs.21,000 was spent on start-up costs directly related to bringing the asset to its working condition. Monthly managerial reports indicated that for the first 5 months, the production quantities for this equipment resulted in an initial operation loss of Rs 15,000 because of small quantities produced. The months thereafter show much more positive results. The equipment has an estimated useful life of 14 years and a residual value of Rs 18,000.Present value of estimated dismantling costs amount of Rs12,500.

- 2. The company adopted straight line depreciation. The asset was sold on 30.6.09 for Rs.3,00,000. The company follows calendar year as its accounting period. Incremental borrowing rate of the company is 10% p.a. What value is originally recorded as the historical cost of the asset and what are the annual charges in the income statement related to the consumption of the economic benefits embodied in the assets? Find out gain/loss of derecognition. How should the company recognize gain and reverse the decommissioning liability?