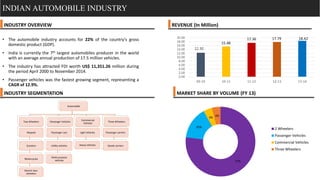

1. • The automobile industry accounts for 22% of the country's gross

domestic product (GDP).

• India is currently the 7th largest automobiles producer in the world

with an average annual production of 17.5 million vehicles.

• The industry has attracted FDI worth US$ 11,351.26 million during

the period April 2000 to November 2014.

• Passenger vehicles was the fastest growing segment, representing a

CAGR of 12.9%.

INDUSTRY OVERVIEW

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

09-10 10-11 11-12 12-13 13-14

15.48

17.36 17.79 18.42

12.30

Figures in Mn

INDIAN AUTOMOBILE INDUSTRY

INDUSTRY SEGMENTATION

Automobile

Two Wheelers

Mopeds

Scooters

Motorcycles

Electric two-

wheelers

Passenger Vehicles

Passenger cars

Utility vehicles

Multi-purpose

vehicles

Commercial

Vehicles

Light Vehicles

Heavy Vehicles

Three Wheelers

Passenger carriers

Goods carriers

REVENUE (In Million)

MARKET SHARE BY VOLUME (FY 13)

77%

15%

4% 4%

2 Wheelers

Passenger Vehicles

Commercial Vehicles

Three Wheelers

2. MARUTI SUZUKI – AN OVERVIEW

INTRODUCTION & OVERVIEW

• Maruti Udyog Limited (MUL) : established in February 1981, though the actual

production commenced in 1983 with the Maruti 800, based on Suzuki alto.

• Maruti Udyog Limited was renamed as Maruti Suzuki India Limited (17th

September 2007).

• The Company was awarded the highest financial credit rating of AAA/ stable

(long term) and A1+ (short term) on its bank facilities by CRISIL.

• Originally, 74% of the company was owned by the Indian Govt, and 26% by Suzuki of

Japan. As of May 2007, the government of India sold its complete share to Indian

financial institutions and no longer has any stake in Maruti Udyog.

• As of 31 March 2014 Maruti Suzuki has 933 dealerships across 666 towns and cities in

all states and union territories of India.

1,155,041 Vehicles Sold in

2013-14.

16% Growth in Rural

Sales.

1000+ Vehicles operating

& providing door to door

service.

4 out of 5 top selling

models in India are from

Maruti Suzuki.

ACHIEVEMENTS IN PRESTECTIVE (2013-14)

MARUTI SUZUKI – MAJOR CAR PORTFOLIO

1984

1999

2005 2008

Omni

WagonR

Swift

Swift DZire

3. Competitive

Rivalry

(High)

Threat of New

Entrants

(Low)

Substitute

Products

(Moderate)

Bargaining

Power of

Suppliers

(Low)

Bargaining

Power of

Customers

(High)

PORTER’S FIVE FORCE ANALYSIS – MARUTI SUZUKI

Competitive Rivalry

• The competition has become very intense with the entry of foreign players like

Volkswagen, Renault in low-priced hatchback segment.

• Foreign players have increased the competition by catering to Indian needs.

Threat Of New Entrants

• The threat of new entrants is low

because of the capital intensity of

business is very high.

• Brand equity.

Substitute Products

• The threat of substitute product is

moderate because the public

transportation is still

underdeveloped in major cities.

• Two wheelers are the major

substitute products available in the

market.

Bargaining Power of Suppliers

• The bargaining power of the seller

is low as most car manufacturers

are specialized in a particular

segment.

• Other players provide various

other features.

Bargaining Power of Customers

• In a market like India the

bargaining power of the buyer is

very high, as there are different

options available with the buyer

for variety of products available

in the same price range.

4. INDIAN AUTOMOBILE INDUSTRY– PASSENGER SEGMENT

• India’s passenger car market shrank for the first time in 11 years during 2013-14.

KEY HIGHLIGHTS

• The auto industry is oligopolistic in nature. HHI of 0.22 is not a true reflection of the

intense rivalry in the sector.

Exports

Domestic Sales

Production

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

3.4

4.5

4.4

5.1

5.6

5.9

16 20

25

26 27

25

18

24

30 31

32

31

Passenger Vehicle

Volumes

• The auto industry is capital intensive with high amount of raw material, depreciation

expenses and as well high selling and distribution expenses due to intense rivalry in the

industry.

• Indian share in the global passenger vehicle market to double to 8 per cent from 4 per

cent over 2010–11.; Passenger vehicle sales to increase from 3.2 million in FY2013 to 8.6

million in FY2021E as per SIAM.

• Word-of-mouth is the most influential source of information for the Indian buyer.

• The industry is not very profitable. Margins are low. Reducing fixed cost per unit by

boosting sales is the key to profitability as it leads to Economies of Scale.

• The Indian Passenger Vehicle (PV) industry recorded volumes of 2.3 million units in 11m

2013-14, a decline of 6.0% Y-o-Y. Sluggishness in PV demand over the last 3 years are

due to high inflation, elevated interest rates and rising fuel prices that have exerted

pressure on disposable income of consumers

• The prevailing weakness in domestic PV demand has meant a relatively prolonged

period of heavy discounts offered by Original Equipment Manufacturers (OEMs) on PV

models across segments.

• Overall though, the industry trend in favour of ‘push-sales’ through discounting rather

than ‘pull-sales’ through advertisements and brand building seems to have got further

entrenched during the current period of slowdown. .

• The PV industry is expected to revert to a volume CAGR of 10-11% (domestic +exports) over the medium

term. The profitability metrics of industry participants too are unlikely to have any meaningful respite over

the near term in view of

• (a) Increase in expenses related to launch of new models, (b) Increase in employee costs as several OEMs

have announced substantial wage hikes, (c) Likely sustenance of discounts-led sales push, (d) Restricted

pricing power in the wake of intense competition and (e) Currency headwinds.

• Market share in the domestic PV industry still remains concentrated in the hands of few players, reflected

in the fact that top four players account for 75% of industry volumes. This implies that profitability

pressures on the relatively low volume players may be even higher resulting in sustained external

financing dependence to fund losses and CAPEX requirements.

5. INDIAN AUTOMOBILE INDUSTRY– PASSENGER SEGMENT – PEER COMPARISON

MARKET SHARE – 14 COMPANIES – FY 2014

Maruti Suzuki,

42.0%

Hyundai, 15.5%

M&M, 9.5%

Tata Motors,

5.7%

Honda, 5.5%

Toyota

Kirloskar, 5.3%

Volkswagen,

2.5%

Ford, 3.3%

Fiat, 0.75%

Nissan,

3.5%

General

Motors, 3.2%

Ranault, 1.0%

Skoda, 2.0%

Mitsubishi,

0.3%

Market Leader – Maruti Suzuki

PROFIT / LOSS – FY 13 AND FY 14

269

-420

76

-1142 -1109

1025

311

2392

216

-597

420

-3812

-479

1108

410

2783

-4000

-3000

-2000

-1000

0

1000

2000

3000

FY 13 FY 14

FFiat

FFord

FGM

FHyundai

FNissan

FMaruti

Suzuki

FVolkswagen FHonda

Figures in crores

KEY HIGHLIGHTS

• Maruti Suzuki further strengthened its dominant position. Market share increased by 2% in

FY14

• Exporting is a significant chunk of production to other markets from India and stepping up

domestic production of spare parts is key to run a profitable business in India for foreign MNC’s

• General Motors struggled with corporate fraud and product recalls (Cheverlot Tavera -1.26 L

units recalled).

• Volkswagen sales dropped to 52K units in FY14 from 75K in FY13; Yet their net profits nearly

sextupled. Every 2nd car was exported in FY14 compared to only 1 in 5 in FY13. Domestically

made spare parts increased to 70% from 40%; Shared resourcing with its sister firm Skoda

increased Economies of Scale.

• Nissan’s exports grew 17% in FY14 and overtook Maruti as the 2nd largest exporter. 60% of its

products are exported. Micra constitutes 70% of its exports. A whopping 80% of its products are

manufactured in India. Increase in the number of dealerships to 300 from 128 would help it to

utilize its full capacity of 4.8L units by FY16. This could boost its market share to 10% by FY18.

Despite its entry in the late 2000’s it has broken even quickly and is a profitable business unlike

some its peers.

6. • Fiat wrote off accumulated loss of 406cr. Despite making quality cars Fiat has struggled to

increased its market share, owing to poor quality after sales service. Fiat sells its 1.3 Multijet

small diesel engines to number of car makers in India. The diesel variants of Maruti Swift, Ritz,

Desire, Tata Manza, Indica Vista, Cheverlot Beat, etc run on the Multijet.. Reduction in engine

purchases by Maruti to about 45% of FY13 in FY14 resulted in the decline in revenues and profits

to Fiat.

• After 5 years of recurring losses, Honda pulled itself together by the bootstraps in FY14. Losses

dipped by a substantial 57%. The introduction of diesel variants and many Indian centric cars

such as Brio, Mobilio, Amaze etc have increased volumes (Economies of Scale) and boosted

revenues by 83% and 43% in FY13 and FY14 respectively. With the launch of new models in the

MUV and the compact SUV segment in the near future Honda would be catering to 50% of the

overall passenger car market as against 10% in FY14. Investment of 3800cr (Rajasthan plant) to

localise body panels and engine components to reduce costs in the years to come.

0

50

100

150

200

250

Alto Swift

Dzire

Swift

Wagonr

Grand

i10

Bolero Eon City Omni Celerio

242

194 185

147

96 92

74 71 68 63

Top 10 SELLING CARS [JANUARY 2014 – NOVEMBER 2014]

6 out of 10 are Maruti Suzuki cars. Maruti Omni is at the end of its life cycle.

The budget hatchback segment is the largest contributor in the

overall car sales forming more than 25% of the total sales.

• Hyundai is the only completely foreign-owned carmaker to consistently report profits in India.

With 60 variants across nine car models, HMIL’s strong performance has come on the back of a

string of successful product launches like the Grand i10, Xcent and most recently, the new i20.

With plans to enter the compact SUV and MPV segments in the next two years, HMIL aims to

gain a market share percentage every year. The India unit was the first successful venture for

Hyundai overseas, and soon turned into an export hub for small cars going to 120 countries.40

new rural outlets by 2014, to take the tally to 320.Rural sales constituted 20% of the total sales

as against 8% in 2012.

Figures in thousands

• Mahindra & Mahindra gets 65% of its total passenger car revenues from its 2 most popular

models Scorpio and Bolero. It is yet to venture into compact SUV segment. Its market share in

the SUV segment declined to 48% in FY2013 from 56% in FY14 owing to intense completion and

lack of new products from M&M. It entered the compact segment with the launch of Verito Vibe.

The sale of passenger vehiles declined by 6% in FY14 as against FY13.

• Tata’s passenger vehicle division recorded sales of 13,767 units, up 21.56 percent compared to

11,325 units sold in February 2014. The trend of growth in passenger vehicles continued with

strong sales of the Zest sedan and a good market response to the Bolt hatchback. However

below industry standard after sales service is key deterrent for its progress

• Renault has a joint manufacturing unit with Nissan in Chennai. The Renault DeSign Studio in

Mumbai is one of the 5 satellite global design studios for monitoring customer trends and

helping customize global products for India. Despite its relatively new entry in the Indian market

it posted a net profits of 15cr in FY13.

• Toyota Kirloskar incurred a loss of Rs.180cr in FY14 marking a dubious first in the

Japanese auto maker’s 15-year history in India. The loss was largely on account of a

recent focus on the small-car Liva and the entry-level sedan Etios for a company that

has always made money in India on the back of a focus on workhorse-like utility

vehicles—the iconic Qualis first, and then the Innova—and up-market sedans such as

the popular Corolla. Sales of the Liva declined 20% during last fiscal and 13.27% in the

five months to August this fiscal year. Sales of the Etios sedan declined 19.44% and

15.5% during the same periods, respectively.

• Ford first started selling cars in India during 1996. Since then, six CEOs have led Ford

India, which has sunk in $2 billion in investments and launched nine models. 18 years

later, all that Ford has to show is a market share of less than 3 per cent, a plant that

was working at half its capacity (2012-13) and 2360cr in accumulated losses.

• Skoda is one of the fringe players, with all its key products in premium sedan

segment. It offers 4 variants in the above segment. Production of the Škoda Fabia

ended in 2013 due to low sales and high assembly cost

7. Internal

External

Strengths

1. Strong business network - Established

distribution and after sales network.

2. Cost effectiveness – due to economies of

scale

3. Loyal customer base – strong brand image

4. Broad product portfolio

5. Good Infrastructure and labour base

6. Largest market share in the PV segment –

42%

7. USP - fuel efficient cars – first to launch

cars with ethanol(mixed fuel) as per govt

regulations.

Weaknesses

1. Contemporary technology

2. Low quality interiors

3. Lack of products in mid size car –sedan

and utility vehicle segment

4. Image stuck on small cars

5. Inferior diesel engines – noisy

6. Manufacturing defects – resulted in a high

product recall of 30,000 altos to fix door

assembly.

7. Low geographic concentration

8. Poor safety features – Poor build quality,

failed crash test

Opportunities

1. Growing potential in emerging markets –

UVs and electric cars. Maruti did launch

an LPG version of wagon R

1. Increasing demand for fuel efficient cars -

- re-launch of Dzire in February 2015,

pegged as India’s most fuel efficient car.

SO strategy

Using their infrastructure and technical

know how, Maruti should reach out to

wider segments in the market by

investing more into R&D for electric cars.

M&M has already ventured into this

segment.

WO strategy

With the recent strategic move to re-

launch Dzire, Maruti can rebuild its

image from inferior engines,

manufacturing defects and from small

car image to mid-sized fuel efficient

cars.

Threats

1. Ever changing customer’s tastes and

purchasing power

2. Global players – Price wars

3. Intense competition

4. Brand loyalists switching to different

brands - Youth favoring foreign

brands/make

5. Global economic slowdown

ST strategy

Leveraging on maruti’s brand image and

reliability, maruti should invest in R&D in

order to develop better and new technology

and market its products well in order to beat

competition from global players.

WT strategy

Maruti should overcome some weaknesses

such as manufacturing defects, inferior

quality of engines and interiors by

implementing better quality check practices

so that the threat of brand loyalists

switching is minimized and maruti can

retain its customer base.

MARUTI SUZUKI INDIA LIMITED – COMPANY ANALYSIS

Swift

Swift Dezire

Zen Estillo

SX4

Grand Vitara

Ritz

A-Star

Alto

WagonR

Omni

Versa

BCG Matrix

Market share

Marketgrowth

High

High

Low

Low

8. GE

MATRIX INDUSTRY ATTRACTIVENESS

BUSINESSSTRENGTH

HIGH MEDIUM LOW

HIGH Investment

and growth -

SWIFT

Investment

and growth –

ALTO

Selectivity/e

arnings – A-

STAR

MEDIUM Investment

and growth –

SWIFT Dzire

Selectivity/ea

rnings – SX4

Harvest –

ECO

LOW Selectivity/ea

rnings –

WAGON R

Harvest –

VERSA

Harvest –

OMNI

COMPANY ANALYSIS AND CORE COMPETENCIES

CORE COMPETENCIESGE MATRIX

• Alliances with

suppliers

• Alliances with

dealers

FORWARD AND BACKWARD

INTEGRATION

• Most extensive

network in India

• Greater customer

satisfaction

STRONG DISTRIBUTOR

NETWORK

• Lean manufacturing

• PMS

• Quality control

MANUFACTURING

EXCELLENCE

• True value

• Anytime Maruti

• Authorized service

centres

• Insurance

OTHER CRM INITIATIVES

CAPABILITIES OF MARUTI

• Manufacturing and production technology

• Understanding customer needs

• Developing new designs and models of car which are fuel efficient

• Quality focus

• Prompt service and customer satisfaction

9. INDUSTRY CSF MARUTI

SUZUKI

HYUNDAI TATA MOTORS

Brand Equity High Low Medium

Productivity High Low Medium

Quality Low High Medium

Strong Dealer Network High Low Medium

Range Of Models High Low Medium

Product Mix Width Medium Low High

Advertising and Brand Recall High Low Medium

Price competitiveness High Low Medium

Efficient Manufacturing Low High Medium

After Sales Service High Medium Low

Engine technology Low High Medium

Styling and Features Low High Medium

R&D spending Low High Medium

Innovation Low Medium High

COMPARATIVE ANALYSIS USING CRITICAL SUCCESS FACTORS – COMPETITIVE ADVANTAGE

The above study shows that Maruti Suzuki has an advantage over its competitors in the Indian Market.

• The Brand Recall coupled with the Strong Dealer network makes it a household name.

• Their high price competitiveness and the after sales service gives them a cost advantage.

• Maruti caters to the needs of the Indian Market. Even though its products mix width is medium, they have managed to maintain and continually increase their market share.

• They have only improvised on existing products and have not really ventured into new emerging segments and this is why they lose out on having a differentiation advantage.

• Based on these and other CSFs we can say that Maruti Suzuki has a Cost Advantage and not a differentiation advantage.

COMPETITIVE ADVANTAGE

Cost Leadership

Maruti

Tata Motors

Differentiation

Audi

Volkswagon

Focus Cost Leadership

Hyundai

Focus Differentiation

Honda

Toyota

Integrated Cost

Leadership/

Differentiation

COMPETITIVE ADVANTAGE

Cost Uniqueness

COMPETITIVESCOPE

NarrowTargetBroadTarget

10. P

O

L

I

T

I

C

A

L

Automatic approval for foreign

equity investment up to 100%, no

minimum investment criteria.

Encourage R&D by offering rebates

on R&D expenditure.

Dept of Heavy Industries & Public

Enterprises have worked towards

reduction of excise duty on small cars

& increase budgetary allocation for

R&D.

Relaxation of excise duty on small

cars from 12 to 18 % bound to help

the sector in the long run.

Maruti Suzuki’s R&D Centre & test

course at Rohtak , Haryana, is a state-

of-the-art facility, comparable to the

best in the world. It is SMC’s first

global R&D Centre outside Japan.

Political

Economical

Socio Culture

Technological

11. E

C

O

N

O

M

I

C

A

L

GDP Per capita has grown from USD

1,432.25 IN 2010 To USD 1,500.76 in 2012,

and is expected to reach USD 1,869.34 by

2018.

Apart from the impact of rising incomes,

widening of the consumer base will also be

aided by expansion of the middle class,

increasing urbanization and changing

lifestyle.

A young population is boosting demand

for cars.

Greater access to credit eases the

purchase of passenger and commercial

vehicles.

7.7

9.3

13.2 12.9

11.7

0

2

4

6

8

10

12

14

FY 09 FY 10 FY 11 FY 12 FY 13

Car industry sales volume (mn)

Car Finance industry (USD bn)

Indian car finance market size

1 3 7

12

25

2935

40

32

50

26

15

0

20

40

60

80

100

120

2008 2020 2030

Seekers(3682.5 - 9206.4)

Deprived (<1657)

Aspirers (1657 - 3682.5)

Strivers(9206.4 - 18412.8)

Globals (>18412.8)

Changing Income Dynamics of India’s population

12. S

O

C

I

O

C

U

L

T

U

R

E

Maruti Mobile support (MMS) vehicles

operating and providing door-step

service to customers.

Maruti Suzuki has set up driving

schools for training people in safe

driving.

Good exchange options, encourages

customers to buy new car in exchange of

old car for good exchange value.

Expanded network, besides urban

outlets, they have developed emerging

market outlets and recruited and

groomed nearly 8000 local youth as

resident dealer sales executive to offer

comfort and assurance to first time

buyers in small town and rural areas.

T

E

C

H

N

O

L

O

G

Y

The Company has introduced India’s first

passenger car with shift technology in Celerio.

Projector Headlamp has been introduced in

Stingray. Projector headlamp provides focused

beam output which helps in better visibility on

the road.

Introduction of Kimekomi ( Fabric & leather

insertion technology) in door trims to provide

superior fit and finish.

The company achieved 3 to 15 per cent

increase in fuel efficiency during the year 13-14

across all the models among various fuel options

by working on different technologies and areas

like optimisation of crank and intake system, new

low viscosity oil, use of new technologies for

rolling resistance reduction on tyres,etc.

13. • The Indian passenger car segment is expected to grow by over four-

fold to 93 lakh units in 2020 to become the world’s third largest car

market.

• The presence of global players, introduction of global

platforms/technologies and stricter emission norms indicate that the

market is gradually attaining maturity.

• A buoyant economic growth, growing middle class population, rising

disposable income levels, relatively low penetration of cars and

adequate availability of financing are likely to provide an ideal

backdrop for a sustained long term demand growth for the sector.

• Increasing interest from foreign players, competitive intensity is likely

to become a key challenge for manufacturers in this segment..

• With most major markets facing excess capacity and demand

saturation, the Indian market is likely to remain a key destination for

global majors over the medium term.

• With most of the international players eyeing the small car market,

we expect the competitive intensity to increase in this segment

resulting in greater fragmentation of market share over the next 5

years.

• Competition, the rising quality expectations and tightening

regulatory norms on emission and safety are likely to push up cost

pressures.

0

1000

2000

3000

4000

5000

6000

FY14 FY20E

in'000s

Vans

UV

premium

executive

midsize

super compact

compact

mini

micro

2.5 2.7

3

3.3

3.7

4.2

4.9

0

1

2

3

4

5

6

2014 2015E 2016E 2017E 2018E 2019E 2020E

inmn

PASSENGER VEHICLE SEGMENT OUTLOOK

PASSENGER VEHICLE SEGMENT FORECAST (CAGR 11.87%)

SEGMENT WISE DISTRIBUTION

14. • Hybrid vehicles are those that use two or more distinct power sources

to move the vehicle.

• The term most commonly refers to hybrid electric vehicles (HEV) or

Electric/hybrid cars (XeV), which combine an internal combustion

engine and one or more electric motors.

• Could become attractive option for Maruti Suzuki with the Centre

planning to offer fairly large subsidies with a view to push demand for

the nascent segment.

• This will result in India becoming a manufacturing and research base

for vehicles running on alternative/eco-friendly fuels.

• The global penetration of hybrid cars is expected to increase

exponentially in the near term.

• Imperative for Maruti Suzuki to concentrate on this sector in order to

continue its dominant position in the passenger vehicles segment.

• SUVs have been preferred choices for most of the car lovers across the

country. Many prefer their off-road capability as well as masculine

looks .

• The SUV segment in India is expected to triple in volume by 2020.

• It accounted for 21% of the overall passenger vehicle sales in 2014

and is expected to account for 29% of the sales by 2020.

45

61

70

2

5

10

0

2

4

6

8

10

12

0

10

20

30

40

50

60

70

80

2010 2015E 2020E

Penetrationin(%)oftotalsales

inmnunits

• Ford EcoSport and Renault Duster created a whole new category

of compact SUVs in 2013.

• People want a car that looks like a Sports Utility Vehicle and

carries a low price tag and all these wishes get settled down to a

compact SUV.

• Its one of the fastest growing and promising segments where

Maruti Suzuki needs to enter and make its presence felt in order

to maintain or increase its market share.

STRATEGIC OUTLOOK

XeV SALES IN THE WORLD

15. • Fiat Chrysler automobiles is the seventh largest automaker in

the world.

• But in India, its subsidiary has a market share of meagre 0.5 %

in the passenger vehicle segment.

• The engine-making unit of Fiat, Fiat Powertrain Technologies

SpA, has so far supplied close to 200,000 diesel powerplants to

Maruti. which powers various models of Maruti Suzuki

including the Swift and Dzire.

• The company expects demand for diesel cars to remain robust

and believes it might not be able to fulfil need on its own.

• Maruti produces 300,000 engines in Manesar. It has also set up

a diesel engine plant in Gurgaon, which will make additional

150,000 units of Maruti’s indigenously developed 800cc diesel

engine, which is likely to power the company’s latest Celerio

model and a mini-truck to be introduced in early 2015.

• Demand for diesel cars has fallen, but if you look at the

demand for Maruti’s diesel cars, it does not have its own

capacity to meet that requirement.

• Maruti sold as many 340,000 diesel cars, 33% of total sales,

during year ended 31 March.

• The production at the Gurgaon plant is for a different set of

engines, which are yet to hit the market.

• Even if one takes a very conservative growth for the industry,

Maruti will require lot more diesel engines..

• The sourcing from Fiat is based on the assumption that Maruti

will be selling more diesel cars in future as it moves closer to the

industry’s ratio of the diesel and petrol engines—48:52.

• Diesel cars will continue to be in favour, given the price gap with

petrol and better fuel efficiency.

• Moreover, given the demand swings, it makes better sense for

Maruti to source the engines rather than invest in creating its

own capacity.

• It would be much more beneficial for Maruti Suzuki to work on

a joint venture with Fiat India with respect to the production of

Diesel cars.

• Maruti will have the benefit of getting the diesel engines at a

cheaper rate which will boost its profit margin.

• Also there would be a lot of savings on the capital expenditure

front.

• Also, Fiat India is not its fiercest competitor in the segment due

to its meagre market share.

• Also since Maruti has recently entered into the SUV segment,

the requirement of Diesel engines for Maruti will increase as it

will try to increase its presence in this fast growing segment.

STRATEGIC OUTLOOK