Alpha Index Options Explained. These can be used to efficiently convert concentrated employee stock or options positions to a diversified portfolio

•

1 recomendación•669 vistas

Alpha Index Options Explained. These can be used to efficiently convert concentrated employee stock or options positions to a diversified portfolio by Jacob Sagi and Robert Whaley John Olagues www.truthinoptions.net olagues@gmail.com 504-875-4825 http://www.wiley.com/WileyCDA/WileyTitle/productCd-0470471921.html

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (7)

Similar a Alpha Index Options Explained. These can be used to efficiently convert concentrated employee stock or options positions to a diversified portfolio

Similar a Alpha Index Options Explained. These can be used to efficiently convert concentrated employee stock or options positions to a diversified portfolio (20)

Más de Truth in Options

Más de Truth in Options (19)

Último

Último (20)

Alpha Index Options Explained. These can be used to efficiently convert concentrated employee stock or options positions to a diversified portfolio

- 1. JACOB S. SAGI ROBERT E. WHALEY* Trading Relative Performance with Alpha Indexes Abstract Relative performance is at the heart of investment management. Stock-picking refers to the practice of attempting to profit from buying stocks that are under- or over-priced relative to the market. Market-timing refers to the practice of attempting to profit from the performance of one asset category versus another. While relative performance is central to investment management, however, complex trading strategies must be devised to capture potential gains because relative performance cannot be traded directly. The purpose of this paper is to introduce a platform for trading the relative performance of various securities. Specifically, we describe a class of relative performance indexes that offer an attractive payoff structures. We then provide a valuation framework for futures and option contracts written on such indexes, and illustrate a variety of ways in which relative performance index products can be a more efficient and cost-effective means of realizing investment objectives than are traditional futures and options markets. Current draft: February 7, 2011 *Corresponding author. The Owen Graduate School of Management, Vanderbilt University, 401 21st Avenue South, Nashville, TN 37203, Telephone: 615-343-7747, Email: whaley@vanderbilt.edu. The authors are grateful for the financial support from NASDAQ OMX and for comments by Dan Carrigan, Paul Jiganti, Eric Noll, Mark Rubinstein, and Walt Smith. Electronic copy available at: http://ssrn.com/abstract=1692738

- 2. Trading Relative Performance with Alpha Indexes Relative performance is at the heart of investment management. Many stock portfolio managers, for example, focus on identifying under- and over-priced stocks with the hope of “beating the market.” Commonly referred to as “stock-pickers,” these individuals take long and short positions in stocks based on their firm-specific analyses and price predictions. Other stock portfolio managers operate globally and focus on identifying under- and over-priced stock markets. These managers are also stock pickers, but of country-specific rather than firm-specific performance. Large institutional investors, such as pension fund managers and university endowments, spread fund wealth across many asset categories like stocks, bonds, and real estate. They constantly monitor the relative performance of the different asset categories in the ongoing decision-making regarding the allocation of fund wealth. As these examples illustrate, investment management pits the performance of individual securities and security portfolios both domestically and internationally against one another or some benchmark. Relative performance is the overarching theme. Consequently, it is surprising that relative performance has yet to be actively traded directly. If a stock-picker believes that a particular stock will outperform the market, he/she will buy the stock and sell the market using index products such as exchange- traded funds or index futures. But, long stock/short market is only one payoff structure and such a position can entail unlimited downside. Suppose, for instance, that the stock- picker prefers a call-like payoff structure on the relative performance or otherwise wishes to limit the downside. In this case, the investor could buy a call on the stock and a put on the market, however, this entails paying unnecessarily for the market volatility embedded in the call and put option premiums. To avoid this, the investor would have to take dynamically shifting positions in the stock and a market ETF (or in their respective derivative products). For the typical institutional or retail investor, constantly migrating funds from one asset category to another in response to a change in expected performance is cumbersome and costly. Exchange-traded products on relative performance would seem to provide a simple and cost-effective means not only of handling existing 1 Electronic copy available at: http://ssrn.com/abstract=1692738

- 3. return/risk management strategies but also of introducing new return/risk management strategies to the investment management arsenal. Currently, the NASDAQ OMX computes and disseminates on a real-time basis nineteen indexes that measure the relative total return of a single stock (“Target Component”) against the SPDR ETF (“Benchmark Component”).1 Pending Securities and Exchange Commission approval, options on these nineteen alpha indexes will be listed on the NASDAQ OMX PHLXSM within the next few months. The purpose of this paper is to provide an academic analysis of a complex of relative performance indexes and associated derivatives (futures and options) which includes the new NASDAQ OMX Alpha Indexes™. The paper has four main sections. In the first, we supply the mechanics for calculating the underlying “relative performance index” of a target security versus a benchmark security. In the second, we describe how futures and option contracts written on relative performance indexes might be structured and how these contracts can be valued. The third section provides a set of scenarios in which relative performance index derivatives are shown to be a more cost effective means for trading relative performance than are traditional futures and options markets. The fourth section summarizes the key results of the paper. I. Relative Performance Indexes A relative performance index is defined as an index that measures the total return performance of a target security relative to the adjusted total return performance of a benchmark like the S&P 500. The total daily security return includes both price St +1 − St + DS ,t +1 appreciation and dividends and is defined as RS ,t +1 ≡ , where St is the St target security price at the end of day t, and DS ,t is the dividend (or other distribution) paid by the security during day t. The total daily benchmark return is defined in a similar 1 See http://www.nasdaqtrader.com/TraderNews.aspx?id=fpnews2010-044 and http://www.nasdaqtrader.com/Micro.aspx?id=Alpha. 2

- 4. M t +1 − M t + DM ,t +1 fashion, RM ,t +1 ≡ , where M t is the benchmark price level at the end of Mt day t, and DM ,t is the dividend paid by the benchmark during day t. A family of relative performance indexes is defined by the updating rule: I b ,t +1 = I b ,t × (1 + R ) S ,t +1 (1) (1 + R ) b M ,t +1 where b is a relative risk-adjustment coefficient and can be set equal to any value to reflect the security’s systematic variation with the benchmark.2 Where b = 0 , the relative performance index is a total return index. Where b = 1 , the right hand side of (1) corresponds to the ratio of the target and benchmark returns, and the relative performance index is an outperformance index.3 The family of relative performance indexes (1) has several noteworthy features. First, the performance measure is based on dividends as well as price appreciation in order to put all stocks on an equal footing. AAPL, for example, does not pay dividends. Comparing its price appreciation to that of, say, IBM (which often distributes a dividend yield of 2% or more) unfairly handicaps IBM in a performance comparison. Second, the index, like the value of an actual portfolio, is always positive. Technically, the index represents the value of a portfolio that is continuously rebalanced such that, for every dollar long in security S, the portfolio is short b dollars in security M. Such a portfolio cannot be synthesized by a buy-and-hold strategy and most of the investment community would avoid mimicking the index due to excessive trading costs and/or tracking error. Futures and option contracts on relative performance indexes would create buy-and-hold 2 The value of b can be set to the security’s price elasticity or beta with respect to the benchmark. The daily updating rule is used for illustration purposes only. In practice the index will be updated continually throughout the trading day. 3 Note that this measure of outperformance is relative performance. The more usual definition of outperformance is the degree to which the price on the target exceeds the price of the benchmark, or absolute performance (see, for example, Margrabe (1978) or Fischer (1978)). Rubinstein (1991) also focuses on the valuation of absolute performance options. More closely related is the work Reiner (1992) who values foreign equity options struck in a domestic currency. This is a special case of (1) where the risk adjustment coefficient is set equal to one (i.e., the exchange rate is acting like 1/benchmark) and only price appreciation is considered. 3

- 5. strategy opportunities, and these may be appealing to some segment of the investment community. We explore these first two issues more deeply in Section III. Third, the ratio of the levels of the index at two different points in time is easily interpreted, particularly in the case where b = 1 . If the current level of the index is 150 and its level three months ago was 120, the target security outperformed the benchmark by 25%. Finally, relative performance indexes can readily be extended to multi-asset benchmarks. An asset pricing purist, for example, may want to benchmark target security performance to a benchmark that includes a number of asset classes such as stocks, bonds, real estate, and commodities. In this case, the returns of asset categories would be included in the denominator of (1), effectively assigning each category its own relative risk adjustment coefficient. Appendix A provides the multi-factor version of (1). II. Futures and Options on Relative Performance Indexes Valuation equations for futures and option contracts on relative performance indexes can be derived analytically under the Black-Scholes (1973)/Merton (1973) (hereafter, “BSM”) valuation assumptions. Specifically, we assume that markets are frictionless (e.g., no trading costs or different tax rates on different forms of income) and that market participants can borrow or lend risklessly at a constant annualized interest rate r. We also assume now that the total return on the target security and the benchmark security evolve as multivariate geometric Brownian motion with constant drifts, μS and μM , volatilities, σ S and σ M , and instantaneous return correlation, ρSM . Under these assumptions, a relative performance index with constant relative risk-adjustment coefficient b will evolve as ⎛⎛ bσ 2 − σ s2 ⎞ ⎞ I b ,t = I b ,0 exp ⎜ ⎜ μ S − bμ M + m ⎟ t + σ S BS ,t − bσ M BM ,t ⎟ , (2) ⎝⎝ 2 ⎠ ⎠ where BS,t and BS,t are the Brownian motion variables associated with securities S and M, respectively. Calculating the present value of payoff derivatives on I b,t requires discounting for risk. To do so and avoid arbitrage in the BSM framework, we replace the 4

- 6. drift terms in (2) by the risk-free interest rate. This results in the following “risk- adjusted” evolution of the relative performance index: ⎛⎛ bσ m − σ s2 ⎞ 2 ⎞ I b ,t = I b ,0 exp ⎜ ⎜ (1 − b ) r + ⎟ t + σ S BS ,t − bσ M BM ,t ⎟ . (3) ⎝⎝ 2 ⎠ ⎠ With the relative performance index dynamics in hand, we now turn to the valuation of futures and option contracts. We assume that futures and options on the index expire at the same point in time and are settled in cash. To avoid the complications of early exercise, we consider only European-style index options. A. The relative performance index as a dynamically rebalanced portfolio Earlier we mentioned that the relative performance index represents the value of a portfolio that is continuously rebalanced such that, for every dollar long in security S, the portfolio is short b dollars in security M. While most of the investment community would avoid mimicking the index because of excessive trading costs and tracking error, it is useful to see the mechanics of such a trading strategy in order to develop a better intuition for how relative performance indexes help to complete the market. Table 1 contains a simple example of the dynamic rebalancing rule in the case b = 1. In the illustration, the total return indexes for the security and the benchmark as well as the relative performance index start at a level of 100 on day 0. The subsequent levels for the security and the benchmark are set arbitrarily. Note that, at any point in time, the relative performance index equals 100 times the total return index of the security divided by the total return index of the benchmark. Over the first day, both the security and the benchmark advanced—the security by 4.17% and the benchmark by 7.16%. Because the benchmark return was larger, the relative performance index fell. The objective of the mimicking portfolio is to match the dollar gain of the relative performance index. On day 1, the dollar gain on the index is –2.79. The mimicking portfolio has three constituent securities. On day 0, the portfolio is long 100 dollars of the security, short 100 dollars of the benchmark, and long 100 dollars in risk-free bonds. Because the sales proceeds from the benchmark exactly offset the 5

- 7. purchase price of the security, the value of the mimicking portfolio equals the value of the risk-free bonds or 100. Over the first day, the bond position produces 0.070 in interest income,4 the security position produces a gain (i.e., price appreciation and dividends) of 4.170, and the benchmark position produces a loss of 7.160. The net gain across the three positions is –2.920. To bring the mimicking portfolio value to the level of the relative performance index, an additional investment of 0.130 is made in risk-free bonds (i.e., the mimicking portfolio has a negative payout or dividend). The mimicking portfolio is then rebalanced. The long position in the security is reduced from 104.17 to 97.21, generating a gain of 6.96. The short position in the benchmark is, likewise, reduced to the same dollar value, producing a loss of 9.95. Subtracting the difference, 2.99, from the available risk-free funds, 100.20, the value of the risk-free bonds in the mimicking portfolio becomes 97.21, exactly the level of the relative performance index. On day 2, the interest income from the investment of 97.21 in risk-free bonds is 0.068, bringing the balance to 97.278. The long position in the security rises in value from 97.21 to 97.21(108.61/104.17 ) = 101.353 for a gain of 4.143, and the short position in the benchmark rises in value from 97.21 to 97.21(111.53 /107.16 ) = 101.174 for a loss of 3.964. To bring the value of the mimicking portfolio into line with the relative performance index level, 0.075 is paid out, bringing the risk-free bond balance to 97.203. The mimicking portfolio is then rebalanced. The long position in the security goes from 101.353 to the new index level 97.38, and the short position in the benchmark goes from 101.174 to 97.38. Adding the difference, 0.179, to the value of the risk-free bonds, 97.203, the new risk-free bond balance settles, and not coincidently, at the level of the relative performance index, 97.38. Under the BSM assumptions and continuous (instead of daily) rebalancing, it can be shown that the payout is a constant proportion of the index level, δ = r − (σ M − ρ SM σ Sσ M ) . In other words, the relative performance index is the value of a 2 4 For illustrative purposes only, the interest income is based on a simple rate of 7 basis points per day. 6

- 8. portfolio that has a constant proportional payout rate or “dividend yield.”5 Note that, in some cases such as when the risk-free interest rate is low or the correlation is low, the dividend yield can be negative. In most cases, however, it will be positive. Suppose, for example, that the total return volatilities of AAPL and SPY are 26.7% and 17.9% respectively, and that the correlation between the two is 71.1%.6 If the risk-free interest rate is 2% the portfolio that mimics the b = 1 AAPL vs. SPY index would pay a constant continuous dividend yield of 2.19%. B. Valuation of relative performance index futures The value of a futures contract written on a relative performance index can be derived from calculating the risk-adjusted expected value of the index at the futures expiration, that is, Fb = Ib e( r −δ )T , (4) where T is the time remaining to expiration of the futures and bσ M δ = br − 2 ( (1 + b ) σ M − 2 ρ SM σ S ) . The term δ can be viewed as the generalization of the payout rate in the previous subsection to the case where b can be different from 1. Note that (4) is the usual cost of carry relation for a stock with a payout yield of δ .7 The payout rate δ depends on the correlation between the stock and the benchmark. This feature of the underlying relative performance index would allow one to infer from index futures prices information about the correlation between the target and benchmark returns. C. Valuation of relative performance index options Under the valuation assumptions listed at the beginning of this section, the simplest way to value European-style options on relative performance indexes is to first apply Black’s (1976) futures option formula. Because the futures price and relative performance index level are the same at futures/option expiration, the value of a 5 Merton (1973) was the first to value securities using the constant proportional dividend yield assumption. 6 The figures correspond to daily returns for the calendar year 2010 used in generating Table 2. 7 For a development of the cost of carry relation, see Whaley (2006, pp. 125-127). 7

- 9. European-style option on the relative performance index equals the value of a European- style option on the futures.8 The value of a European-style call option on a relative performance index futures is Cb = e − rT ⎡ Fb N ( d1 ) − XN ( d 2 ) ⎤ ⎣ ⎦ (5) where X is the exercise price of the option, N ( d ) is the cumulative normal density function with upper integral limit d, and the upper integral limits are ln ( Fb / X ) + .5σ 2T d1 = and d 2 = d1 − σ T . σ T Because the underlying source of uncertainty is the ratio of two lognormally distributed prices, the volatility rate in the expressions for d1 and d2 is σ = σ S + b2σ M − 2bρSM σ Sσ M . 2 2 (6) Then, to value a European-style call option on a relative performance index, substitute (4) into (5) as well as into the expressions for the upper integral limits d1 and d2 that accompany (5) to get Cb = Ibe−δ T N ( d1 ) − Xe− rT N ( d2 ) , (7) where ln ( Ib / X ) + (r − δ + .5σ 2 )T d1 = , and d 2 = d1 − σ T . σ T The value of a European-style put option on a relative performance index follows straightforwardly from put-call parity. More specifically, the payoff resulting from purchasing a call option and selling a put option (with the same exercise price and time remaining to expiration) equals the value of the index at expiration less the exercise price. The present value of these payoffs yields the put-call parity relation for European-style options: 8 For a proof, see Whaley (2006, p. 198). 8

- 10. Cb − Pb = Ib e−δ T − Xe− rT . (8) Substituting (7) into (8) and isolating the put value, we get Pb = e− rT XN ( −d2 ) − Ibe−δ T N ( −d1 ) . (9) D. Hedging relative performance index futures and options The valuation equations for the futures on relative performance indexes (4) and for the options on relative performance indexes (7) and (9) allow us to develop analytical expressions for the metrics used in risk management (i.e., delta, gamma and vega). Appendix B contains these expressions. Several results are noteworthy. First, because the underlying payoffs depend on changes in two distinct securities, delta-risk management will necessarily require a simultaneous position in both the security S and its corresponding benchmark M. As one might suspect from the links between portfolio formation and relative performance indexes, for every dollar of security S used to hedge a relative performance index derivative, one must take a position of –b dollars in the benchmark security M. Thus, although a relative performance index derivative might at first blush seem twice as complicated to hedge as a derivative product on a single underlying, in practice the hedging position in M is completely determined by the hedging position in S. A second noteworthy result is that, because the futures price depends on the volatilities of S and M (as well as on the correlation between them), the futures vega is not zero. Indeed, we must consider a new type of vega here, corresponding to price- sensitivity to changes in the correlation between S and M. This is apparent from the expression for the futures price (4). Finally the gamma with respect to the benchmark and the cross-gamma (i.e., the sensitivity of the benchmark delta with respect to the benchmark and its sensitivity with respect to the stock) of the futures price are not zero. The intuition for this is as follows. The current value of the index is inversely proportional to the cumulative performance of the benchmark. Such inverse dependence is necessarily a convex function, which implies that the gamma of the index with respect 9

- 11. to the benchmark will not be zero. Among other things, this means that extra care should be taken when delta-hedging index derivatives against large benchmark movements. III. Using Relative Performance Index Products With the relative performance index product valuation mechanics in hand, we now turn to providing a series of illustrations that show the potential benefits of these products. To keep matters simple and realistic, we focus again on the case where the risk- adjustment coefficient equals one, that is, b = 1 . This case is germane because such indexes are computed on a real-time basis and are disseminated as NASDAQ OMX Alpha Indexes™.9 Pending Securities and Exchange Commission approval, options on nineteen alpha indexes pitting the total return of an individual stock against the total return performance of the SPDR ETF will listed on the NASDAQ OMX PHLXSM within the next few months. A list of the individual companies, together with the ticker symbols of the stock and the alpha index, are shown in Table 2. Option products on relative performance indexes where b ≠ 1 are planned, as are futures contracts on alpha indexes. To begin, it is worthwhile to note that, under the assumption that b = 1, the dividend yield term in the various valuation equations is δ = r − σ M (σ M − ρ SM σ S ) . The futures price, therefore, can be rewritten as σ M (σ M − ρSM σ S )T F = Ie , (10) which implies that, depending upon whether σ M is greater than or less than ρ SM σ S , the futures may trade at a premium or a discount relative to the underlying relative performance index. It is also worthwhile to note that, if a relative performance index futures is actively traded, its price implies the level of correlation between the stock and the benchmark returns via 9 Most of the discussion in this section also applies qualitatively to other cases in which b > 0 . 10

- 12. ln ( F / I ) σM − Tσ M ρ SM = . (11) σS Because the level of the relative performance index and the time remaining to the expiration of the futures are known, and σ S and σ M can be estimated using stock option and index option prices, the correlation is uniquely determined and, by definition, is forward-looking. Likewise, the implied beta of a security can also be inferred from alpha index derivative prices because its definition is σS β SM ≡ ρ SM . (12) σM Such an estimation approach may be particularly useful given that current approaches to estimating beta involve using a long time-series of past return data and assuming the beta is constant over the entire time-series history. In other words, typical beta estimates are inherently backward-looking and stable through time. At the same time, finance theory has long recognized that the beta of a stock changes with the nature of a firm’s business, financial and operating leverage, the macro-economy, and other factors—an obvious conundrum. To demonstrate the potential value of alpha index options as a source of information about correlations, consider the example of CSCO (Cisco Systems, Inc.) vs. SPY. The realized correlation between the daily returns of these assets was 66% in 2010Q3 and 34% in 2010Q4. This suggests that realized correlation in one quarter may be a poor forecast correlation in the subsequent quarter and underscores the need for forward-looking estimates of correlations. One obvious concern is whether the Alpha- option bid-ask spreads will be too large to allow for useful inference of option-implied correlations. To examine this, assume it is October 1, 2010 and that the true correlation between CSCO and SPY over the next quarter is 34%. Suppose further that the volatilities of CSCO and SPY are well-estimated from standard options to be 11% and 11

- 13. 39% over 2010Q4.10 With the index level at 100 and absent a bid/ask spread, an at-the- money alpha-option should sell for $7.25. If bid/ask spreads provided a price range of $7.14 to $7.36 (a 3% difference), then the corresponding range in implied correlation would be 30% to 38%.11 This is significantly more accurate than the 66% correlation estimate from the previous quarter’s realized correlation. Moreover, even if the previous quarter’s realized correlation happened to be 34%, estimation error would lead to a 90%- confidence interval of 15% to 52% for the historical correlation forecast, which is nearly four times larger than the interval implied by the alpha-option price.12 In summary, under reasonable assumptions for option bid/ask spreads, we expect that option-implied correlations will be both forward-looking and more accurate than estimates based on historical time-series.13 A. Efficiency gains to trading relative performance using index derivatives Absent a specific view on individual stock performance, an equities investor should hold a well-diversified stock portfolio. With a strong view that a particular stock will outperform the market, on the other hand, an investor may want to devote a large portion of portfolio wealth to the individual stock rather than the market. Buying the stock directly, however, is not a “clean” way to implement the view that the stock will outperform the market. To illustrate, consider an investor who, on April 21, 2010, believed that AAPL’s shares would outperform the market over the remaining part of the second quarter of the year. Buying AAPL’s shares on April 21 and holding until June 30 would have produced a disappointing return of –3.0%. Does that mean the investor was wrong? The answer is no. The price of SPY ETF shares (a proxy for the stock market) fell by 14.0% over the same period. While AAPL outperformed the market as the investor expected, it also declined with the rest of the market. Over the same period, 10 We are using the actual realized volatilities in 2010Q4. 11 Standard options on CSCO and SPY feature a bid/ask spread of roughly 1.5%, half of the spread we assume in the example. 12 To arrive at this confidence interval we employ a Fisher transformation and the fact that there were 64 days in 2010Q3. 13 Implied correlations and betas, by definition, apply to the life of the alpha option. Thus one can deduce a term structure of implied correlations/betas from alpha index options of varying maturities, corresponding to the market’s forecast of how a firm’s systematic risk is forecasted to change over time. 12

- 14. AVSPY (i.e., the NASDAQ OMX Alpha Indexes™ that pits the performance of AAPL against SPY) rose by 12.9%.14 By construction, the relative performance index is less exposed to events that move the entire market. We now turn to comparing how alpha index futures and option values change in reaction to changes in relative performance with those of alternative buy-and-hold strategies that use existing exchange-traded products. Our aim is to highlight the differences, thereby helping to point out how these new instruments help to “complete the market” for investors interested in relative performance. Long stock/short benchmark: Consider an investor who has 100 dollars to invest and wants to speculate that the price of a particular stock will rise relative to a benchmark. One possible trading strategy that uses currently traded securities is to buy $100-worth of stock, financing its purchase by selling an equal dollar amount of the benchmark ETF.15 Assuming the 100 dollars is invested in risk-free bonds, the overall value of this three-security, passive position is 100. If alpha index futures (hereafter, “alpha-futures”) were also traded, the investor could also form a similarly-purposed, passive strategy by buying 100 dollars of risk-free bonds and buying an equal dollar amount of alpha-futures.16 Over a very short horizon, the benefits of both of these strategies are the same. Over longer periods of time, however, the passive long stock/short ETF position can become unbalanced, exposing the investor to more downside risk. Suppose, for example, that the stock, the benchmark ETF, and the alpha index are priced at 100 at the beginning of the investment horizon. The long stock/short benchmark-ETF position has a value of 100 (i.e., the risk-free bonds), as does the fully collateralized alpha-futures position. Now, suppose that, over the investment horizon, the stock falls to 50, and the benchmark rises to 200. The gain on the long stock/short benchmark-ETF position is –150, while the gain on the alpha-futures is –75. The total value of the long/short strategy is negative because the loss exceeds the value of the risk- 14 Neither AAPL nor SPY paid dividends during the period. 15 This assumes, of course, that the investor can short the benchmark ETF at low cost and largely maintain full use of the cash proceeds. 16 This type of position involving an exact dollar futures overlaid on risk-free bonds is called a fully- collateralized futures position. 13

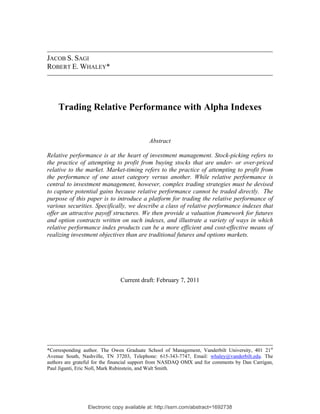

- 15. free bonds, illustrating that there is no limit to the loss that can be incurred from the short benchmark-ETF position. On the other hand, the value of the fully collateralized alpha- futures position is 25, well above its minimum level of 0. Long stock-call, short benchmark-call: Oftentimes investors prefer to use option-like structures in their trading strategies. To capture relative performance, an investor could buy an at-the-money call option on the stock and sell an at-the-money call option on the benchmark. Using the illustration above, the long stock-call would expire worthless at the end of the investment horizon since the stock price, 50, sank below the exercise price, 100. On other hand, the benchmark call is 100 dollars in the money at expiration. Since the investor is short the call, he loses 100. As an alternative strategy, the investor could choose to buy an at-the-money call on the alpha index (hereafter, “alpha- call”). In the example, at the end of the call option’s life the index is at 25 and the call expires worthless. Obviously, the alpha-call has less potential downside exposure. To examine the potential upside of the alpha-call, we reverse the price movements by letting the stock price go from 100 to 200 and the benchmark to go from 100 to 33.33. The long stock-call/short benchmark-call strategy would have a payoff of 100 at expiration because the stock-call is 100 in the money and the benchmark call is worthless. On the other hand, the alpha index rises to a level of 600 leaving the alpha-call 500 in the money. Obviously, the alpha-call has greater upside potential. Naturally, the decision about which strategy to use must be based on investor preferences and other portfolio considerations. Our purpose is to illustrate how a static position in an alpha-call differs from a position in existing instruments. To this end, Figure 1 shows the value of the alpha-call as a function of the stock price and the benchmark price at expiration. The call option has an exercise price of 100 and three months remaining to expiration. The volatility rates of the stock (AAPL) and the benchmark (SPY) are 26.7% and 17.9%, respectively. The correlation between the returns is 0.711. The risk-free interest rate is 2%. Note that, as the stock price falls and the benchmark price rises, the call goes to its lowest possible value of 0. On the other hand, as the stock price rises, the call value rises, however, as the benchmark price falls, 14

- 16. the call value rises at an increasing rate. This is because the benchmark price is in the denominator of the alpha index. Figure 2 shows the value surface of the long stock-call/short benchmark-call portfolio. The value of this portfolio position is scaled to match the value of the at-the- money alpha-call option to ensure equal dollar investment. In general, the scale factor is greater than one because the proceeds from the sale of the benchmark-call are used to offset the purchase price of the stock-call. Like the alpha-call, the value of the long stock- call/short benchmark-call portfolio falls in value as the stock price falls and/or the benchmark price rises. Unlike the alpha-call, however, the portfolio value may become negative. Moreover, as the stock price rises and the benchmark price falls, the portfolio value rises, albeit not to the same levels as the alpha-call. Long stock-call/long benchmark-put: Another option strategy that is designed to capture relative performance is to buy an at-the-money stock-call and buy an at-the- money benchmark-put. Returning to our illustration, suppose the stock price falls from 100 to 50 and the index level rises from 100 to 200. The long stock-call expires out of the money, as does the long benchmark put. Hence, the “straddle” expires worthless, similar to the alpha-call. If the reverse happens and the stock price rises to 200 and the benchmark falls to 50, the stock-call is 100 in the money, the put is 50 in the money, and the straddle value is 150. The alpha-call, on the other hand, has a value of 300. Again, the decision about which strategy to use is based on investor preferences. Figure 3 shows the value surface of the long stock-call/long benchmark-put portfolio at expiration which can be compared with the corresponding alpha-call surface in Figure 1. Here too the call-put position is scaled so that its initial value matches that of the alpha- call. In general, the scale factor is less than one because two options are being purchased, and the stock-call alone has a higher premium than the alpha-call. Like the alpha-call, the value of the long stock-call/long benchmark-put portfolio falls in value as the stock price falls and/or the benchmark price rises. And, also like the alpha-call, the call-put position never falls below 0. On the other hand, as the stock price rises and the benchmark price falls, the call-put position value does not rise to the same levels as the alpha-call. 15

- 17. To illustrate yet another important difference between the call-put strategy above and the alpha-call, consider an unexpected change to market volatility. Roughly, the call- put position value will be highly affected because both the call and the put are exposed to market risk and move in the same direction in reaction to news about market volatility. By contrast, the alpha-call value will be less affected for most stocks.17 The three strategy comparisons provided above illustrate the distinctive features of alpha index derivatives. These products can simultaneously provide downside protection while reducing exposure to market volatility. While existing exchange-traded products can be combined to create a passive, directional bet on relative performance, they cannot be combined to create a passive, directional bet on the alpha index or its derivatives products. To do so would require dynamic trading strategies, and dynamic strategies are prohibitively expensive, at least for retail investors. To get a rough sense for the trading costs in replicating alpha-products, we perform a set of simulations. In the simulations, the investor is assumed to pay a proportional cost of $0.01 per share, a fixed cost of $1.00 for trading any quantity of the stock, benchmark, or bond, and an additional 0.20% net fee for a short sale.18 The trading strategy aims to replicate a $1,000 investment in a three-month, at-the-money alpha-call option on the b = 1 AAPL vs. SPY index using standard delta-hedging techniques.19 The volatility and correlation parameters are drawn from Table 2. The simulation results are quite striking. In order to achieve a tracking standard error no larger than about 5%, the average trading costs are around 110% of the value of the position! The reason is that hedging an at-the-money call requires frequent rebalancing (about 300 times during the three months to achieve the 5% standard tracking error). Each time the portfolio is rebalanced the investor must pay $1 per trade, or $3 in total to trade in risk-free bonds, AAPL, and SPY, amounting to about $900 over the life of the option. The remaining $200 in average costs is generated by the proportional 17 In particular, if the stock’s beta is fixed at one then the alpha-call value only depends on the stock’s idiosyncratic volatility. 18 We assume that the proportional costs for trading the short-term bond are negligible. Our cost assumptions are conservative and understate the true trading costs currently faced by retail investors. 19 Specific details regarding the delta-hedge simulation are available from the authors upon request. 16

- 18. transaction costs and is still staggeringly large. In other words, even a $1M position in at- the-money calls would require an expenditure of roughly 20% of the portfolio value in trading costs if the standard tracking error is to be kept below 5%. Table 3 documents simulation results of tracking errors and trading costs for various three-month AAPL vs. SPY alpha-call options. The initial investment is assumed to be $10,000, and the replicating portfolio is assumed to be rebalanced daily (90 trading periods after the initial portfolio setup) over the life of the option. Note that the at-the- money alpha-call now has a tracking error of 9% as opposed to the 5% in the earlier illustration. This is because the replicating portfolio is rebalanced only 90 times as opposed to 300. Out-of-the-money calls are the most difficult and costly to replicate. The reason is that the high leverage implicit in such options requires large positions in the stock and benchmark relative to the option value. Even small fluctuations in the underlying prices can greatly unbalance the portfolio. In addition, the large trades required for rebalancing entail higher costs. The 10% out-of-the-money alpha-call has an average tracking error of 34% and an average total trading cost of 36% of the option’s value. Overall, the lesson from this exercise is that, while forward/futures positions on an alpha index might be relatively inexpensive to implement through dynamic trading, replicating alpha-options is not. B. Relative performance index options are generally less expensive The fact that relative performance index products are less exposed to market risk means that relative performance index options are less expensive than standard options. The reason is simple. Stock options are based on the total risk of the stock (i.e., the sum of market risk and idiosyncratic risk), while relative performance index options are essentially based on the difference in risk between the stock and the benchmark. Because option value varies directly with volatility, relative performance index options are cheaper. To illustrate, return once more to the AAPL vs. SPY example. Suppose an investor decides to buy an at-the-money call option with an exercise price of 100 and three months remaining to expiration. The investor estimates that the expected future 17

- 19. return volatility of AAPL is 26.7% and SPY is 17.9%, and that the expected correlation between AAPL and SPY returns is 0.711. The risk-free interest is 2%. Under the BSM assumptions, the value of an at-the-money call option on AAPL is $11.53. At the same time, the value of an at-the-money call option on AVSPY is $7.24, corresponding to a discount of 37%. The volatility used in the valuation of the relative performance index option, given by equation (6), is 18.8%. As long as the correlation between the assets is positive and σ S > σ M , the volatility of the index (i.e., σ ) is guaranteed to be smaller than the volatility of the stock (i.e., σ S ), and the price an alpha-call will likewise be guaranteed to be cheaper than the price on a target-call. C. Relative performance index products are based on total return Earlier, we argued that in order to make a fair comparison between the performances of two securities, one should consider their total return, which includes income distribution as well as price appreciation. There are other advantages to using total returns in measuring performance. Standard exchange-traded stock futures and option contracts are based only on the price appreciation of the underlying stock. Because a relative performance index futures incorporates dividends into the performance calculation, its payoffs implicitly include the automatic reinvestment of security income without incurring transaction costs. It also means that relative performance index options are not susceptible to the trading games played in the stock option market when deep in- the-money options remain unexercised.20 D. Trading correlation According to the valuation equations derived in Section II, the values of relative performance index futures and options depend on the correlation between the security S and the benchmark M. A higher correlation implies lower index futures and call options prices. A trader who believes correlations will increase (decrease) can sell (buy) index futures or sell (buy) index call options to benefit from his or her insights. With the earlier 20 Pool, Stoll, and Whaley (2008), for example, show that many long call option holders unwittingly fail to exercise outstanding call option positions on stocks when it is optimal to do so (just prior to the ex-dividend day) and, as a result, forfeit the ex-dividend call option price drop to market makers and proprietary firms. 18

- 20. example of AAPL vs. SPY, an increase in the correlation from 0.711 to 0.8 corresponds to a decline in the value of a one-year at-the-money call option from $7.24 to $6.08. The trader could sell the option and hope that the new information would be reflected in prices soon after (at which point he or she would close out the position for a profit). The risk here is that the index will simultaneously move higher, cancelling the decline in the option value. To make a cleaner investment, the trader can hedge the written option using the deltas calculated in Appendix B and using a correlation value of 0.711 to calculate the hedging positions. The net position will be insensitive to changes in the index itself, but once the new correlation value of 0.8 is absorbed by the market, the option value will sink below that of the hedging portfolio and the trader can close out the portfolio at a profit.21 The opposite strategy can be employed if the trader believes correlations will decline. This illustrates how investors can trade on their views concerning correlations between the index components. In general, the construction of a portfolio that moves only with the correlation between two assets requires model-calculated positions in relative performance index derivatives and the index constituents (and potentially their derivatives). What is important to emphasize is that such trades could not be contemplated without traded index derivatives (just as one could not trade volatility without traded stock derivatives). Thus, just as stock options have enabled markets to trade stock volatility, relative performance index products have the potential of opening up an entirely new market for trading correlations. IV. Summary The purpose of this paper is to introduce a new complex of relative performance indexes, tracking the performance of a target security versus that of a benchmark security. In particular, we assess how derivatives (options and futures) on these indexes might provide investors with new opportunities to trade relative performance. We provide 21 This assumes that volatilities are constant. If this is not the case, then the trader would have to account for changing volatility in constructing the hedging portfolio. 19

- 21. valuation formulae for futures and option contracts on the family of relative performance indexes. In addition, we illustrate a variety of ways in which the new index products could be a more efficient and cost-effective means of realizing certain investment objectives than are traditional futures and options markets. The new indexes essentially track a portfolio that is long on a target stock and short on a benchmark asset, such that the ratio of the two dollar positions is constant. As the target asset outperforms its benchmark, the equivalent long-short position increases. Likewise, if the target asset underperforms its benchmark over a period, then the equivalent portfolio long-short position is decreased. This behavior ensures downside protection which could only otherwise be implemented through dynamic trading – an exercise typically beyond the reach of most investors. The introduction of options on the new indexes poses several additional benefits. We show that such options are generally cheaper than options on the target security. We also show that they offer a different payoff structure than related positions using standard calls and puts on the underlying target and benchmark securities. In particular, the new index call options simultaneously have downside protection and an accelerated upside relative to static positions in existing instruments. At the same time, such options would be creating investment opportunities otherwise only available to typical investors at great costs. Finally, an exciting aspect of the new index options is that they present investors with the ability to trade the correlation between the target and benchmark securities. Indeed, we show that option implied correlations (which could be used to calculate option implied target CAPM betas if the benchmark is a market index) are both forward-looking and potentially more informative about future correlations than historical estimates. 20

- 22. References Black, Fischer. 1976. The pricing of commodity contracts, Journal of Financial Economics 3, 167-179. Black, Fischer and Myron Scholes. 1973. The pricing of options and corporate liabilities, Journal of Political Economy 81, 637-659. Fischer, Stanley. 1978. Call option pricing when the exercise price is uncertain and the valuation of index bonds, Journal of Finance 33, 169-176. Margrabe, William. 1978. The value of an option to exchange one asset for another, Journal of Finance 33, 177-186. Merton, Robert C. 1973. Theory of rational option pricing, Bell Journal of Economics and Management Science 1, 141-183. Pool, Veronika, Hans R. Stoll, and Robert E. Whaley. 2008. Failure to exercise call options: An anomaly and a trading game, Journal of Financial Markets 11, 1-35. Reiner, Eric. 1992. Quanto mechanics, RISK 5, 59-63. Rubinstein, Mark. 1991. One for another, RISK 4, 30-32. Whaley, Robert E. 2006. Derivatives: Markets, Valuation, and Risk Management, John Wiley & Sons, Inc.: Hoboken, New Jersey. 21

- 23. Appendix A: Multi-asset relative performance indexes The benchmark used in the definition of the complex of relative performance indexes in (1) can be extended to include multiple-asset benchmarks. Suppose, for example, the desired benchmark has n different asset classes (i.e., stocks, bonds, real estate, and commodities) and each asset class constitutes w% of the overall benchmark n portfolio, where, of course, ∑ w = 1 . Under these assumptions, the updating rule for the i =1 i multi-asset relative performance index is I b , w,t +1 = I b , w,t × (1 + R ) S ,t +1 . n ∏ (1 + R ) wi b i ,t +1 i =1 where b is as before and w is a vector of benchmark asset allocation weights (i.e., wi , i = 1,..., n ) . With a relative performance so defined, a change in the log-index corresponds to the difference between the instantaneous performance of security S versus the weighted and scaled instantaneous performances of the benchmark assets, that is, n ln I b , w ,t +1 − ln I b , w ,t = ln (1 + RS ,t +1 ) − b ∑ wi ln (1 + Ri ,t +1 ) i =1 The futures and option valuation equations on these multi-factor benchmarks are also analytically tractable and available from the authors upon request. 22

- 24. Appendix B: Risk metrics for derivatives on relative performance indexes Under the BSM option valuation assumptions, we showed that the value of a futures contract written on a relative performance index with a constant relative risk- adjustment coefficient of b is Fb = Ib e( r −δ )T , (B-1) where Fb and Ib are the futures price and the relative performance index level, r is the annualized risk-free interest rate, T is the futures time remaining to expiration in years, bσ M δ = br − 2 ( (1 + b ) σ M − 2 ρ SM σ S ) , σ S and σ M are the volatility rates of the security and the benchmark, and ρSM is the correlation between the returns of the security and the benchmark. We also showed that the values of the European-style call and put options on the relative performance index are Cb = Ibe−δ T N ( d1 ) − Xe− rT N ( d2 ) , (B-2) and Pb = e− rT XN ( −d2 ) − Ibe−δ T N ( −d1 ) . (B-3) where X is the exercise price of the option, T is the time remaining to option expiration (i.e., same time as futures), N ( d ) is the cumulative normal density function with upper integral limit d, σ = σ S + b2σ M − 2bρSM σ Sσ M , and the upper integral limits are 2 2 ln ( Ib / X ) + (r − δ + .5σ 2 )T d1 = , and d 2 = d1 − σ T . σ T The put-call parity relation for European-style options is Cb − Pb = Ib e−δ T − Xe− rT . (B-4) Based on these equations, the risk metrics (i.e., delta, gamma and vega) of the futures and options are as follows. 23

- 25. Delta: Based on the futures pricing relation (B-1), the delta of the futures with respect to the underlying relative performance index is Δ F , I = e( r −δ )T . The deltas with respect to the prices of the security and the benchmark are I b ( r −δ )T I r −δ T Δ F ,S = e and Δ F , M = − b e( ) . S M Based upon the valuation equations (B-2) and (B-3), the deltas of the European- style call and put options with respect to a change in the underlying relative performance index are Δc, I = e−δ T N ( d1 ) and Δ p, I = −e−δ T N ( −d1 ) . Since the alpha options may be hedged using shares of the security or the benchmark, the deltas with respect to the per share security price, S, are Ib I Δc,S = Δ c , I and Δ p , S = − b Δ p , I S S and the deltas with respect to the per share benchmark price, M, are Ib I Δc,M = − Δ c , I and Δ p , M = b Δ p , I . M M Gamma: (B-5) shows that the delta is not a function of the relative performance index level, so the gamma of a futures with respect to the index is 0. This is also true of the gamma with respect to the security, S. The gamma with respect to the benchmark price is not zero, however, and is given by I b ( r −δ )T Γ F , MM = 2 e . M2 The cross gammas are 24

- 26. Ib Γ F , SM = Γ F , MS = − Δ F ,I . SM The gamma of a call option with respect to the underlying index is the same as that for the put option: n ( d1 ) Γ I = Γ c , I = Γ p , I = e −δ T , I bσ T 1 − d12 / 2 where n ( d1 ) = e is the normal density function evaluated at d1 . The gammas of 2π the call option with respect to the underlying security and benchmark prices are given by I b2 I ( I Γ + 2Δ I ) I ( I Γ + ΔI ) Γ c,S = 2 Γ I , Γc,M = b b I 2 and Γ c , SM = Γ c , MS = − b b I . S M SM By virtue of the put-call parity relation (B-4), the gammas of the European-style put options are related through the gamma of the futures price: Γ p ,S = Γc ,S , Γ p,M = Γc,M − e− rT ΓF ,M and Γ p ,SM = Γ p,MS = Γc,MS − e− rT Γ F ,MS . Vega: Unlike the usual cost of carry model, the futures pricing equation for a relative performance index is a function of volatility. The vegas with respect to σ S , σ M , and ρSM are: VegaF ,σ S = −b ρ SM σ M TFb , VegaF ,σ M = b ⎡(1 + b ) σ M − ρ SM σ S ⎤ TFb , ⎣ ⎦ and VegaF , ρSM = −bσ Sσ M TFb . The vegas of the European-style call option with respect to σ S , σ M , and ρSM are 25

- 27. ⎛ σ − bρ SM σ M ⎞ − rT Vegac ,σ S = I b e−δ T n ( d1 ) T ⎜ S ⎟ + e N ( d1 ) VegaF ,σ S ⎝ σ T ⎠ ⎛ b ( bσ M − ρ SM σ S ) ⎞ − rT Vegac ,σ M = I b e −δ T n ( d1 ) T ⎜ ⎟ + e N ( d1 ) VegaF ,σ M ⎝ σ T ⎠ and ⎛ bσ σ ⎞ − rT Vegac , ρSM = − Ib e−δ T n ( d1 ) T ⎜ S M ⎟ + e N ( d1 ) VegaF , ρSM . ⎝ σ T ⎠ Note that, by the put-call parity relation (B-4), the vegas of the call, put and futures are related by Vegac,i − Vega p,i = e− VegaF ,i , where i = σ S , σ M , ρSM . Hence, the vegas of the rT European-style put option with respect to σ S , σ M , and ρSM are Vega p ,σ S = Vegac,σ S − e− rTVegaF ,σ S , Vega p ,σ M = Vegac,σ M − e− rTVegaF ,σ M , and Vega p, ρSM = Vegac, ρSM − e− rTVegaF , ρSM . 26

- 28. Table 1: Simulation of replicating portfolio for the b = 1 relative performance index. At the beginning of each day, the portfolio is rebalanced so that the position in cash and the target security is set equal to the level of the index, while the portfolio position in the benchmark is short an amount equal to the level of the index. The table documents the daily income from these positions, as well as the payout that results from rebalancing. Relative Hedge portfolio Mimicking Total return indexes performance index Interest Dollar income Net portfolio Day Security Benchmark Level Gain income Security Benchmark gain Payout value 0 100 100 100 100 1 104.17 107.16 97.21 -2.79 0.070 4.170 7.160 -2.920 -0.130 97.21 2 108.61 111.53 97.38 0.17 0.068 4.143 3.964 0.247 0.075 97.38 3 110.68 110.36 100.29 2.91 0.068 1.856 -1.022 2.946 0.038 100.29 4 111.01 113.83 97.52 -2.77 0.070 0.299 3.153 -2.784 -0.017 97.52 5 112.62 110.70 101.73 4.21 0.068 1.414 -2.682 4.164 -0.048 101.73 27

- 29. Table 2: List of NASDAQ OMX Alpha Indexes™ with option contracts pending approval of the SEC. All of the indexes listed are outperformance indexes with the benchmark being the SPDR ETF (ticker symbol SPY). The annualized volatility of each stock and correlation with SPY are calculated using daily return data for the calendar year 2010. The data were collected from Datastream. Over the sample period, SPY daily returns had a realized annualized volatility of 17.9%. Alpha Stock return Stock index Correlation Stock name ticker ticker Volatility with SPY return Amazon.com, Inc. AMZN ZVSPY 32.6% 60.4% Apple Inc. AAPL AVSPY 26.7% 71.1% Cisco Systems, Inc. CSCO CVSPY 31.9% 61.7% Ford Motor Company F FVSPY 38.1% 70.6% General Electric Company GE LVSPY 27.4% 82.3% Google Inc. GOOG UVSPY 27.8% 65.1% Hewlett Packard Company HPQ HVSPY 24.9% 68.0% International Business Machines IBM IVSPY 17.8% 78.3% Intel Corporation INTC JVSPY 25.3% 77.3% Coca-Cola Company KO KVSPY 15.5% 63.7% Merck & Company, Inc. MRK NVSPY 20.6% 65.7% Microsoft Corporation MSFT MVSPY 22.0% 73.0% Oracle Corporation ORCL OVSPY 24.4% 67.5% Pfizer Inc. PFE PVSPY 21.3% 66.2% Research in Motion Limited RIMM RVSPY 38.5% 44.9% AT&T Inc. T YVSPY 15.1% 70.7% Target Corporation TGT XVSPY 20.2% 66.0% Verizon Communications Inc. VZ VVSPY 16.0% 60.3% Wal-Mart Stores, Inc. WMT WVSPY 14.0% 50.3% 28

- 30. Table 3: Transaction costs and tracking error for delta-hedging portfolios of positions in three-month futures and options positions written on the AVSPY alpha index. Following the initial setup, the hedging portfolio is rebalanced 90 times in equal intervals (“days”) subsequent to the initial investment of $10,000. Fixed costs are set at $1 per asset per trade. Proportional costs are set to $0.01 per share, with initial share values for AAPL and SPY taken to be $340 and $130, respectively. Short selling costs are assumed to be 0.20% of the amount borrowed. The AAPL volatility rate is assumed to be 26.7%, the SPY volatility rate is 17.9%, and the correlation between the two returns is 71.1%. The index is set to 100 when the derivative positions are initiated. The table reports the standard deviation of the tracking error, defined as the difference between the option value and the value of the tracking portfolio at expiry in the absence of transaction costs. The table also reports a breakdown of the accrued trading costs at the option’s expiration. The fixed costs can accrue to more than $273 because costs are capitalized. They can also be below that value for deep out-of-the-money options because certain price paths lead to essentially zero option value well before the option’s expiration. Tracking Average fixed Average proportional Average total Derivative standard error (%) costs ($) costs ($) costs (%) Futures 0.1% $274 $30 3% Call option X=80 0.5% $274 $160 4% X=90 2% $274 $400 7% X=100 9% $272 $1,300 16% X=110 34% $268 $3,300 36% 29

- 31. F Figure 1: Simul lated expiration value of call op ption on AVSPY index. The ca option has an exercise price o 100 and three months Y all of r remaining to exppiration. The vol latility rates of th security (AAPL) and the ben he nchmark (SPY) a 26.7% and 1 are 17.9%, respective The ely. c correlation betwe the returns is 0.711. The risk-fr interest rate is 2%. een 0 free s 200 150 100 Option value 50 0 -50 -100 50 50 70 60 70 90 80 90 100 110 110 120 130 130 140 Benchmark price B 150 Security price 30

- 32. F Figure 2: Simulaated expiration value of portfolio consisting of lo call option o AAPL and sho call option on SPY. Both call options v o ong on ort l h have an exercise price of 100 and three months rem maining to expiraation. The volatili rates of the se ity ecurity (AAPL) a the benchmar (SPY) and rk a 26.7% and 17 are 7.9%, respectivel The correlatio between the re ly. on eturns is 0.711. T risk-free inte The erest rate is 2%. P Portfolio value o at-the- of m money options at origination is sca to match the value of the at-th aled he-money alpha c option. call 200 150 100 Option value 50 0 -50 -100 50 50 70 60 70 -150 90 80 90 100 110 110 120 130 130 140 150 Be enchmark price Security price 31

- 33. F Figure 3: Simulaated expiration value of portfolio consisting of lo call option o AAPL and lo put option on SPY. Both call and put v ong on ong n l o onths remaining to expiration. The volatility rates o the security (AA options have an exercise price of 100 and three mo e 1 o of APL) and the ben nchmark ( (SPY) are 26.7% and 17.9%, respectively. The cor rrelation between the returns is 0.7 711. The risk-free interest rate is 2 Portfolio valu of at- e 2%. ue t the-money option at origination is scaled to match the value of the at-the-money alp call option. ns h pha 200 150 100 Option value 50 0 -50 -100 50 50 70 60 70 90 80 90 100 110 110 120 130 130 140 150 Be enchmark price Security price 32