Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (11)

Similar a 11 May Daily market report

Similar a 11 May Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

11 May Daily market report

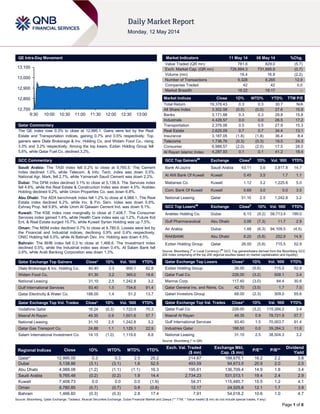

- 1. Page 1 of 6 QE Intra-Day Movement Qatar Commentary The QE index rose 0.3% to close at 12,995.1. Gains were led by the Real Estate and Transportation indices, gaining 0.7% and 0.5% respectively. Top gainers were Dlala Brokerage & Inv. Holding Co. and Widam Food Co., rising 3.3% and 3.2% respectively. Among the top losers, Ezdan Holding Group fell 5.6%, while Qatar Fuel Co. declined 3.2%. GCC Commentary Saudi Arabia: The TASI index fell 0.2% to close at 9,765.5. The Cement Index declined 1.0%, while Telecom. & Info. Tech. index was down 0.5%. National Agr. Mark. fell 2.7%, while Yamamah Saudi Cement was down 2.2%. Dubai: The DFM index declined 3.1% to close at 5,138.9. The Services index fell 4.6%, while the Real Estate & Construction Index was down 4.5%. Arabtec Holding declined 9.2%, while Union Properties Co. was down 6.8%. Abu Dhabi: The ADX benchmark index fell 1.2% to close at 4,988.1. The Real Estate index declined 6.2%, while Inv. & Fin. Serv. index was down 5.9%. Eshraq Prop. fell 9.8%, while Umm Al Qaiwain Cement Ind. was down 9.1%. Kuwait: The KSE index rose marginally to close at 7,408.7. The Consumer Services index gained 1.4%, while Health Care index was up 1.2%. Future Kid Ent. & Real Estate surged 15.7%, while Kuwait Syrian Holding was up 7.5%. Oman: The MSM index declined 0.7% to close at 6,780.9. Losses were led by the Financial and Industrial indices, declining 0.9% and 0.4% respectively. ONIC Holding fell 5.0%, while Al Batinah Dev. Inv. Holding was down 4.5%. Bahrain: The BHB index fell 0.3 to close at 1,466.6. The Investment index declined 0.5%, while the Industrial index was down 0.4%. Al Salam Bank fell 2.6%, while Arab Banking Corporation was down 1.3%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Dlala Brokerage & Inv. Holding Co. 40.40 3.3 900.1 82.8 Widam Food Co. 61.30 3.2 365.0 18.6 National Leasing 31.10 2.5 1,242.8 3.2 Gulf International Services 93.40 1.5 754.6 91.4 Qatar Electricity & Water Co. 188.00 1.4 51.2 13.7 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 18.24 (0.3) 1,723.9 70.3 Masraf Al Rayan 49.35 0.9 1,601.6 57.7 National Leasing 31.10 2.5 1,242.8 3.2 Qatar Gas Transport Co. 24.88 1.1 1,129.1 22.9 Salam International Investment Co. 14.15 (1.0) 1,119.6 8.8 Market Indicators 11 May 14 08 May 14 %Chg. Value Traded (QR mn) 781.6 829.0 (5.7) Exch. Market Cap. (QR mn) 726,884.3 731,895.9 (0.7) Volume (mn) 16.4 16.8 (2.2) Number of Transactions 9,328 8,265 12.9 Companies Traded 42 42 0.0 Market Breadth 16:22 16:17 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 19,378.43 0.3 0.3 30.7 N/A All Share Index 3,302.58 (0.0) (0.0) 27.6 15.9 Banks 3,171.88 0.3 0.3 29.8 15.8 Industrials 4,428.57 0.0 0.0 26.5 17.2 Transportation 2,376.06 0.5 0.5 27.9 15.3 Real Estate 2,625.09 0.7 0.7 34.4 13.1 Insurance 3,187.05 (1.8) (1.8) 36.4 8.4 Telecoms 1,736.76 (0.3) (0.3) 19.5 24.3 Consumer 6,988.57 (2.0) (2.0) 17.5 28.0 Al Rayan Islamic Index 4,287.93 0.1 0.1 41.2 18.4 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Bank Al-Jazira Saudi Arabia 43.11 3.6 3,817.8 14.7 Al Ahli Bank Of Kuwait Kuwait 0.45 3.5 1.7 1.1 Mabanee Co. Kuwait 1.12 3.2 1,225.6 5.0 Com. Bank Of Kuwait Kuwait 0.69 3.0 0.0 3.5 National Leasing Qatar 31.10 2.5 1,242.8 3.2 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Arabtec Holding Co. Dubai 6.13 (9.2) 58,713.4 199.0 Gulf Pharmaceutical Abu Dhabi 3.06 (7.3) 11.7 2.9 Air Arabia Dubai 1.48 (6.3) 94,109.5 (4.5) RAKBANK Abu Dhabi 8.20 (5.8) 252.9 14.9 Ezdan Holding Group Qatar 26.00 (5.6) 715.5 52.9 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 26.00 (5.6) 715.5 52.9 Qatar Fuel Co. 226.00 (3.2) 508.1 3.4 Mannai Corp. 117.40 (3.0) 84.4 30.6 Qatar General Ins. and Reins. Co. 42.70 (3.0) 1.7 7.0 Qatari Investors Group 68.00 (2.3) 309.0 55.6 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Qatar Fuel Co. 226.00 (3.2) 115,266.2 3.4 Masraf Al Rayan 49.35 0.9 78,721.9 57.7 Gulf International Services 93.40 1.5 70,003.7 91.4 Industries Qatar 188.50 0.0 39,284.3 11.6 National Leasing 31.10 2.5 38,504.3 3.2 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,995.05 0.3 0.3 2.5 25.2 214.67 199,675.1 16.2 2.2 3.8 Dubai 5,138.86 (3.1) (3.1) 1.6 52.5 493.59 94,673.5 20.9 2.0 2.0 Abu Dhabi 4,988.08 (1.2) (1.1) (1.1) 16.3 195.61 136,709.4 14.9 1.8 3.4 Saudi Arabia 9,765.48 (0.2) (0.2) 1.9 14.4 2,734.23 531,013.1 19.4 2.4 2.9 Kuwait 7,408.73 0.0 0.0 0.0 (1.9) 54.31 115,485.7 15.5 1.2 4.1 Oman 6,780.85 (0.7) (0.7) 0.8 (0.8) 12.17 24,525.8 12.1 1.7 3.9 Bahrain 1,466.60 (0.3) (0.3) 2.8 17.4 7.91 54,018.2 10.6 1.0 4.7 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,700 12,800 12,900 13,000 13,100 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QE index rose 0.3% to close at 12,995.1. The Real Estate and Transportation indices led the gains. The index rose on the back of buying support from Qatari shareholders despite selling pressure from non-Qatari shareholders. Dlala Brokerage & Inv. Holding Co. and Widam Food Co. were the top gainers, rising 3.3% and 3.2% respectively. Among the top losers, Ezdan Holding Group fell 5.6%, while Qatar Fuel Co. declined 3.2%. Volume of shares traded on Sunday fell by 2.2% to 16.4mn from 16.8mn on Thursday. Further, as compared to the 30-day moving average of 30.4mn, volume for the day was 46.1% lower. Vodafone Qatar and Masraf Al Rayan were the most active stocks, contributing 10.5% and 9.8% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Earnings Earnings Releases Company Market Currency Revenue (mn)1Q2014 % Change YoY Operating Profit (mn) 1Q2014 % Change YoY Net Profit (mn) 1Q2014 % Change YoY Fawaz Abdulaziz Alhokair & Co. Saudi SR 5,482.0 17.7% 720.2 23.3% 771.4 24.5% Shuaa Capital Dubai AED 64.2 77.5% – – 8.2 NA Arabian Scandinavian Insurance Co. (Ascana) Dubai AED 13.0 13.4% 0.3 -27.2% 2.3 -65.9% Orient Insurance Co. Dubai AED 170.2 11.3% 46.6 6.1% 108.5 1.5% Al Dhafra Insurance Co. Abu Dhabi AED 78.0 -7.0% 34.5 0.5% 37.5 13.4% Gulf Livestock (GLS) Abu Dhabi AED – – -1.3 NA 5.1 127.4% Agility Public Warehousing Co. Dubai KD 1.0 NA – – 11.2 10.9% Kuwait Food Co. (Americana Group) Kuwait KD – – – – 18.1 10.4% Dhofar Cattle Feed Co. (DCF) Oman OMR 7,186.0 4.4% – – 1.0 NA The Financial Corporation Co. (Fincorp) Oman OMR 2.2 93.6% 1.2 528.7% 1.4 5773.4% Source: Company data, DFM, ADX, MSM News Qatar QE, QNBFS conclude week-long international roadshow – The Qatar Exchange (QE), in collaboration with QNB Financial Services, Deutsche Bank and Merrill Lynch concluded a week- long roadshow that was held in London and New York to enhance investor relations between international investment institutions and Qatari listed companies. The forum was designed to complement the companies' ongoing investor relations activities by providing an opportunity for the senior management of listed companies to meet key decision makers from a number of the world's largest international fund managers. The forthcoming inclusion of Qatar in the MSCI Emerging Market Index provided a unique opportunity for Qatar to showcase its market-leading listed companies at a time when the profile of Qatar was set to be raised further. During the two days of meetings in London, the QE-listed companies met with over 64 fund managers representing 40 major institutions, which represented the most important funds allocating money to Qatar, the GCC and the broader emerging markets. In aggregate the event hosted 140 meetings. (QE) QCB auctions T-bills worth QR4bn – The Qatar Central Bank (QCB) auctioned treasury bills worth QR4bn on May 6, 2014, for which it received bids totaling QR10.1bn. T-bills worth QR2bn with a maturity period of 3 months were auctioned at a yield of 0.72%. T-bills valued at QR1bn with a maturity period of 6 months were sold at 0.89% yield, while T-bills with a maturity period of 9 months were auctioned at 0.95% yield. (QCB) Century 21 Qatar: Real estate market remains stable – Qatar’s real estate market remained firm in April 2014 with rents and transactions maintaining their upward trend. According to the Century 21 Qatar’s monthly report, upmarket West Bay witnessed the highest rentals with the average monthly rental price for villas ranging between QR20,000 and QR35,000. The Qatari real estate market recorded QR4.7bn worth of real estate deals in 935 transactions during April. Al Waab area remained the most popular area for the medium to high-income bracket with villa rentals ranging between QR14,000 and QR26,000. The lowest villa rental could be found in Al Dhakhira and Al Khor where rentals ranged between QR6,000 and QR12,000. (Peninsula Qatar) Five more airlines set to move to HIA – According to sources, five more airlines will move their entire operations to Hamad International Airport (HIA) on May 14 and 15, 2014. An airport spokesperson said United Airways Bangladesh will begin its operation from HIA on May 15, while four other airlines – Etihad Airways, Kuwait Airways, Sri Lankan and Royal Jordanian will also move their operations to HIA from May 14. Earlier, the national carrier Qatar Airways (QA) had said it would officially move to its new home at HIA on May 27. Qatar has plans to build a second terminal at HIA for the use of foreign airlines. Overall Activity Buy %* Sell %* Net (QR) Qatari 69.82% 68.52% 10,131,032.08 Non-Qatari 30.18% 31.49% (10,131,032.08)

- 3. Page 3 of 6 This is expected to be ready by 2022, when Qatar hosts the FIFA World Cup in Doha. (Gulf-Times.com) International BoE faces guidance challenge as recovery picks up – The Bank of England’s (BoE) Governor Mark Carney faces a growing challenge of explaining why the central bank is signaling that it is in no rush to raise record low interest rates, even as Britain's recovery picks up speed. The BoE is due to give new inflation and growth forecasts and hold a news conference this week against a backdrop of soaring house prices and a faster growth rate than any other big rich nation. The BoE has struggled to give a clear direction about its interest rate outlook since adopting the so-called ‘forward guidance’ as a policy last year, shortly after Carney took over. The central bank has said it thinks the recovery can carry on without inflation taking off, allowing it to keep interest rates at 0.5% for possibly another year to nurse Britain's economy back to full health. Central to the argument is the BoE's belief that companies can squeeze more out of their workers and machines as demand grows, avoiding a surge in wages that could fuel inflation. (Reuters) Japan current-account surplus narrows more than forecast – Japan’s current-account surplus narrowed more than forecast in March as a surge in imports before last month’s sales-tax increase trimmed gains from overseas investments. The excess of 116.4bn Yen reported by the Ministry of Finance in Tokyo compared with a median forecast of 347.7bn yen in a Bloomberg News survey of 25 economists. A 782.9bn yen deficit on a seasonally adjusted basis was the largest in comparable data back to at least 1996. Consumers splurged on items such as refrigerators and computers in March before the 3 percentage point tax rise, boosting imports already climbing due to a weaker yen and nuclear plant closures pushing up energy costs. According to economist Takeshi Minami, as the higher levy takes grip, the current account surplus may grow as shipments from overseas slow down. The yield on 10-year government bonds is about 0.6%, the lowest of any nation. The Yen has fallen about 15% against the dollar since the start of 2013, and was 0.2% down at 102.02 recently. (Bloomberg) China needs to adapt to ‘new normal’ of slower growth – Chinese President Xi Jinping said the nation needs to adapt to a “new normal” in the pace of its economic growth and remain “cool-minded” amid a slowdown that analysts forecast will lead to the weakest expansion since 1990. Jinping said China’s growth fundamentals have not changed and the country is still in a significant period of strategic opportunity. At the same time, the government must prevent risks and take timely countermeasures to reduce potential negative effects. China’s policy makers are trying to keep economic expansion from slipping below the 2014 target of about 7.5%, while reining in a credit boom that threatens to undermine the financial system. The government has so far limited its support to tax breaks, and speeding up infrastructure and social housing investment, with the focus remaining on the quality of growth and on changing the structure of the economy. (Bloomberg) Regional Al-Khodari Sons appoints Chairman – Abdullah A. M. Al- Khodari Sons Company (Al-Khodari Sons) has appointed Ali Abdullah Abdul Mohsen Al Khodari as the Chairman of the company. (Tadawul) BSA submits license cancellation request to CMA – Barclays Saudi Arabia (BSA) has submitted a request to the Saudi Capital Market Authority (CMA) to cancel its licenses for securities business in the Kingdom. BSA will continue working with the CMA until the process is concluded. (Tadawul) Listed Saudi transport firms grow 32% YoY – According to sources, net profits of the listed transport companies in Saudi Arabia grew by 32% to SR257.4mn in 1Q2014 when compared to SR194.7mn in 1Q2013. However, 1Q2014 profits dropped by 40% as compared to SR429.3mn in 4Q2013. The sector is consists of four listed companies whose market capitalization is worth SR19.6bn, or 1% of the total market value. Their total capital stood at SR4.97bn. (GulfBase.com) NWC, Panda to promote water conservation – The National Water Company (NWC) and Al-Azizia Panda of Savola Group have entered into a strategic partnership to strengthen their joint efforts to promote environmental awareness and highlight the importance of water conservation. This agreement will enhance the sustainability of water and the conservation of natural resources. (GulfBase.com) Schneider, NGSA sign 3-year agreement – Schneider Electric has signed a MoU with National Grid Saudi Arabia (NGSA) to cooperate in developing and advancing electricity infrastructure in the Kingdom. The three-year agreement will facilitate the exchange of knowledge, best practices and technology between the two organizations through periodic technical forums. Additionally, Schneider Electric will provide the Saudi Electricity Company and NGSA with training on mutually agreed focus areas, particularly environmental issues and regulations affecting the industry. (Bloomberg) CDSI: Kingdom’s non-oil exports up 12.5%, Imports down 9.1% in March – According to the Central Department of Statistics & Information (CDSI), the total value of non-oil commodity exports from Saudi Arabia grew by 12.5% to SR19,249mn in March 2014 as compared to March 2013. However, the value of imports fell by 9.1% to SR51,198mn as compared to March 2013. Non-oil exports amounted to 37.6% of the total value of imports during this period of previous year. CDSI said that the exports of chemical industry and related products came first with SR6,277mn, representing 32.61% of the total value of non-petroleum accommodates exports. Plastics and rubber products exports ranked second with a value of SR5,890mn, representing 30.6%, while transport equipment and parts exports occupied third place with a value of SR2,098mn, representing 10.9%. (Bloomberg) IIF: UAE’s banking sector returns to a strong growth trajectory – The Institute of International Finance’s (IIF) Deputy Director, Garbis Iradian said that the 1Q2014 figures from leading UAE banks indicate that the country’s banking system has turned around with strong rebound in profitability, steady decline in non-performing loans (NPLs) and faster asset growth. The largest eight banks, which account for 80% of the total banking assets, have recorded impressive growth in 1Q2014 with their profits increasing by 21% YoY on average. The outlook for the UAE banks in 2014 remains favorable supported by robust non-hydrocarbon growth, low interest rates and a steady increase in real estate prices. The IIF has forecast 11% growth in loans and deposits each, with provisions remaining stable and NPLs declining further to 7.4%. (GulfBase.com) GCAA signs MoU with Airbus Middle East – The UAE General Civil Aviation Authority (GCAA) has signed a MoU with Airbus Middle East to support the future of aviation through a series of workshops. The two parties will work together to develop engagement and training initiatives for youth at a grass- roots level in the UAE, to support the growing needs for talent and to encourage young UAE nationals to pursue a career in the aviation industry. (Bloomberg)

- 4. Page 4 of 6 DFM changes trading session structure ahead of MSCI upgrade – The Dubai Financial Market (DFM) said that it will introduce a pre-closing period to its trading sessions from May 14, 2014, to ensure that closing prices are more predictable and eliminate large last-minute swings. DFM said the move was timed to come ahead of the UAE’s inclusion in the list of emerging markets by MSCI at the end of May, which is expected to bring more foreign investors to the market. Under the new rule, orders for equity and debt securities submitted within the last 10 minutes of trading will accumulate for completion at closing. The auction aims to match as many orders as possible, but leaves out those made at extremely low or high prices. (Reuters) DED: Dubai’s business confidence surges – According to a survey by the Department of Economic Development (DED), Dubai’s business community has been significantly more optimistic during 1Q2014 as compared to 1Q2013. Optimism is especially high among manufacturing and services firms out of the total of 502 companies covered in the 1Q2014 survey. The composite Business Confidence Index for Dubai stood at 135.5 points in 1Q2014, indicating an increase of 22.4 points from 1Q2013. Large companies are more optimistic than SMEs, as indicated by their corresponding index scores of 141.6 and 126.4 respectively. (GulfBase.com) Dubai agrees $1.7bn sale of Mauser to CD&R – According to sources, private equity firm Clayton Dubilier & Rice (CD&R) has agreed a deal to buy Germany-based packaging group Mauser from Dubai International Capital (DIC) for around $1.72bn. The deal is one of the largest asset disposals by a state-owned investment fund in the Emirate since its debt crisis, which forced a number of these vehicles to reschedule debt worth billions of dollars. (Gulf-Times.com) Jafza signs MoU with Arab Brazilian Chamber – Jebel Ali Free Zone (Jafza), the Free Zone operation of Economic Zones World (EZW), has signed a MoU with the Arab Brazilian Chamber of Commerce to further strengthen bilateral commercial relations between the two sides. (GulfBase.com) Empower inks AED750mn deal with Tecom Investments – Empower is set to provide 120,000 refrigeration tons (RT) of district cooling services for Tecom Investments’ Dubai Design District (D3) project. The project total value is estimated at AED750mn, which will be financed through Empower’s revenues. D3’s district cooling network will be implemented in several phases, the first of which is expected to begin in 4Q2014, with a capacity of 10,000 RT. (Bloomberg) Nakheel partners with Premier Inn for Ibn Battuta Hotel – Nakheel has signed a management agreement with UK-based Premier Inn for its new 372-room hotel at Ibn Battuta Mall. The hotel is part of Nakheel’s 28,000 sqm expansion of the Ibn Battuta complex, which is scheduled to open in 2016. The mall is spread across 521,000 sqm and currently has 270 shops, 50 restaurants and a 21-screen cinema. The expansion will add another 150 shops to the existing complex. (Bloomberg) UAB enters into retail banking partnership – The United Arab Bank (UAB) has entered into a three year partnership agreement with The Club. Under the agreement, UAB will be the exclusive retail banking partner, and will install and operate ATMs at The Club. The Bank is sponsoring the leisure club’s newly inaugurated Al Nadi Tower, erected to mark its 50th anniversary in 2012. (GulfBase.com) SIB joins Nasdaq Dubai Murabaha platform for Islamic financing – Sharjah Islamic Bank (SIB) has joined Nasdaq Dubai’s growing Islamic financing Murabaha platform, which offers unique advantages to bank customers seeking Shari’ah solutions. SIB is the first bank to join the facility since the official launch of the Nasdaq Dubai Murabaha platform in April 2014, which was set up by Nasdaq Dubai jointly with Emirates Islamic. The platform is the ideal alternative to many traditional Islamic financing solutions, which can carry a risk of losses through price movements, spreads and poor liquidity as well as delays. Since the pilot phase began in September 2013, around AED3bn of financing has been processed on the platform for thousands of clients, involving transactions of more than AED12bn. (GulfBase.com) Aldar to launch off-plan sales for new Abu Dhabi project – Aldar Properties has announced it will start off-plan sales of apartments and townhouses at its new Al Hadeel at Al Bandar development. The sales event on May 17, 2014 for units at Al Hadeel will be conducted on a strictly first come, first serve basis. Al Hadeel was unveiled at the Cityscape Abu Dhabi property exhibition in April 2014 and the development has received strong interest ahead of the sales launch. Construction of the project is due to commence in early 2015. Al Hadeel offers studios, bedroom apartments, as well as townhouses, with the majority of the properties enjoying panoramic views. (Bloomberg) Kuwait signs $12bn LNG supply deal with Shell – Kuwait’s state oil group said it signed a six-year LNG supply deal worth an estimated $12bn with Royal Dutch Shell, as the major oil exporter seeks to meet energy demands for the hot summer months. The deal between Kuwait Petroleum Corp. (KPC) and Shell was finalized in April 2014. KPC’s Head of International Marketing Division Nasser Al-Mudaf said that the company also plans to sign a $3bn deal LNG supply deal with BP. (Bloomberg) KIB posts KD5mn profits for 1Q2014 – Kuwait International Bank (KIB) has reported a net profit of KD5mn in 1Q2014 as compared to KD4.24mn in 1Q2013. EPS amounted to 5.39 fils at the end of March 2014 as against 4.55 fils a year earlier. The bank’s total assets stood at KD1.5bn at the end of 1Q2014. (Bloomberg) SCPD: Kuwait plans to launch 82 mega projects – According to the Secretary-General of the Supreme Council for Planning & Development (SCPD), Adel Al-Wugayan, Kuwait’s development plan for 2014 involves 82 major projects, five public shareholding businesses and 10 BOT-based enterprises. Governmental allocations for these development projects for 2013-14 and 2014-15 have touched KD10.2bn. (Bloomberg) Burgan Bank reports KD17.1mn profit in 1Q2014 – Burgan Bank has reported a net profit of KD17.1mn in 1Q2014 as compared to KD15.6mn in 1Q2013, reflecting a growth of 10%. Operating income surged to KD61.7mn registering 10% growth, while operating profits before provisions soared to register KD34mn, reflecting a growth of 14%. Net interest income grew by 19% as compared to 1Q2013. EPS amounted to 11.2 fils at the end of March 2014 as against 10.1 fils a year earlier. (Bloomberg) CBO: Private deposits in Omani banks up by 14.4% – According to the statistics by the Central Bank of Oman (CBO), the total value of private deposits at the commercial banks in the Sultanate rose by 14.4% to OMR10,396.4mn at the end of February 2014 as compared to OMR9,089.0mn in February 2013. The gross value for these deposits included OMR3,340.3mn time deposits, OMR3,557.3mn saving deposits and OMR3,383.8mn on demand deposits. The broad money and clearance to the deposits was 13.9%. The combined money and clearance to the gross deposits was 12.3%, while the total percentage of loans to liabilities was 93.4%. (GulfBase.com)

- 5. Page 5 of 6 Oman launches OMR100mn SME Development Fund – Oman has launched a new SME Development Fund (Al Namaa Fund) with a capital of OMR100mn to help Omani entrepreneurs obtain debt finance ranging from OMR50,000 to OMR300,000 for their small and medium-scale enterprises. The fund was announced in March 2014 with its total capital to be raised in five tranches of OMR20mn each. (GulfBase.com) Omani power firms set to double profits after share offer – According to sources, Oman-based Al Batinah Power Company and Al Suwadi Power Company, which recently launched twin initial public offers, will double their profits from 2014 to 2018 as they pay off their start-up costs. The firms are owned by the same consortium, whose owners aim to raise OMR62.7mn through the sale of 35% stake in each company, who together provide a quarter of the electricity for Oman’s main power grid. Launching their operations in April 2013, the two companies were required to go public and list on the Sultanate’s bourse under the terms of their licenses. (Bloomberg) BHEL commissions second gas turbine in Oman – India- based Bharat Heavy Electricals Ltd (BHEL) has commissioned another 126MW gas turbine generator at Qarn Alam-3 power project of Petroleum Development Oman (PDO). This is the second successive project after the commissioning of the 2x126 MW PDO Amal gas turbine generating project in 2012. (GulfBase.com) Oman's April oil output dips marginally – The Sultanate's crude oil and condensates production in April stood at 27.7mn barrels, at an average of 924,270 bpd, a 1.73% decline as compared to March 2014. The monthly report released by the Ministry of Oil & Gas pointed out that the total exported crude oil in April 2014 amounted to 22.7mn barrels, at an average of 755,656 bpd, indicating a 6.03% MoM decline. (Bloomberg) EDB: Non-oil sector growth set to drive economy – The Economic Development Board (EDB) said that Bahrain's non-oil sector is well positioned for growth in 2014, powered by the launch of infrastructure projects worth $4.43bn. In the first Bahrain Economic Quarterly (BEQ) for 2014, the EDB said it expects non-oil growth to accelerate to more than 4% in 2014 and even as the oil sector is likely to remain more or less flat, headline GDP growth should come in at 3.5-4%. The EDB said a number of infrastructure projects that were approved by the Gulf Development Fund are due to be launched in the coming months. Government expenditure for 2014 is expected to be more robust compared to last year. Due to delay in incremental government spending, the annual growth rate of the government services sector in the national accounts slowed down sharply last year. (Bloomberg) ABC Islamic Bank posts $3.5mn net profit – Bahrain-based ABC Islamic Bank reported 9% increase in its net profit for the 1Q2014 at $3.5mn as compared to $3.2mn in 1Q2013. ABC Islamic Bank's total assets stood at $1.13bn at the end of the 1Q2014 compared with $1.002bn at the end of last year. ABC Islamic Bank is a wholly owned subsidiary of Arab Banking Corporation. (GulfBase.com) ABG reports $67mn net profit for 1Q2014 – Bahrain’s leading Islamic bank, Al Baraka Banking Group (ABG) reported a net profit of $67mn for 1Q2014, reflecting a marginal increase of 1% YoY. While the bank’s total assets increased by 1%, total financing & investments went up by 2% and customer accounts rose by 1% in 1Q2014 as compared to the December 2013. These results reflect the group’s ability to continue investing in lucrative opportunities arising from the current situation, despite the current fluctuations in the international and regional economies and the financial markets. (AmeInfo.com)

- 6. Contacts Saugata Sarkar Keith Whitney Sahbi Kasraoui Head of Research Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC (0.2%) 0.3% 0.0% (0.3%) (0.7%) (1.2%) (3.1%) (4.0%) (3.2%) (2.4%) (1.6%) (0.8%) 0.0% 0.8% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,288.79 0.0 0.0 6.9 DJ Industrial 16,583.34 0.0 0.0 0.0 Silver/Ounce 19.16 0.0 0.0 (1.6) S&P 500 1,878.48 0.0 0.0 1.6 Crude Oil (Brent)/Barrel (FM Future) 107.89 0.0 0.0 (2.6) NASDAQ 100 4,071.87 0.0 0.0 (2.5) Natural Gas (Henry Hub)/MMBtu 4.57 0.0 0.0 5.3 STOXX 600 338.54 0.0 0.0 3.1 LPG Propane (Arab Gulf)/Ton 103.75 0.0 0.0 (17.8) DAX 9,581.45 0.0 0.0 0.3 LPG Butane (Arab Gulf)/Ton 116.50 0.0 0.0 (14.7) FTSE 100 6,814.57 0.0 0.0 1.0 Euro 1.38 0.0 0.0 0.1 CAC 40 4,477.28 0.0 0.0 4.2 Yen 101.86 0.0 0.0 (3.3) Nikkei 14,199.59 0.0 0.0 (12.8) GBP 1.69 0.0 0.0 1.8 MSCI EM 1,006.95 0.0 0.0 0.4 CHF 1.13 0.0 0.0 0.8 SHANGHAI SE Composite 2,011.14 0.0 0.0 (5.0) AUD 0.94 0.0 0.0 5.0 HANG SENG 21,862.99 0.0 0.0 (6.2) USD Index 79.90 0.0 0.0 (0.2) BSE SENSEX 22,994.23 0.0 0.0 8.6 RUB 35.23 0.0 0.0 7.2 Bovespa 53,100.34 0.0 0.0 3.1 BRL 0.45 0.0 0.0 6.8 RTS 1,232.78 0.0 0.0 (14.6) 186.7 154.0 140.1