logistics industry development power point ppt.pdf

2 February Daily market report

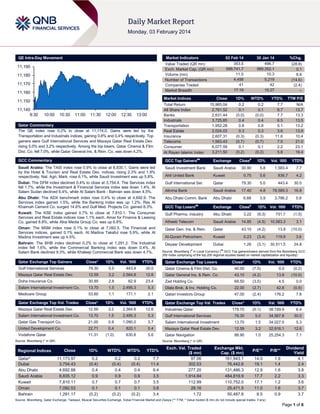

1. QE Intra-Day Movement

Market Indicators

11,190

11,180

11,170

11,160

Market Indices

11,150

11,140

9:30

02 Feb 14

353.5

589,741.7

11.0

4,458

41

17:19

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.2% to close at 11,174.0. Gains were led by the

Transportation and Industrials indices, gaining 0.8% and 0.4% respectively. Top

gainers were Gulf International Services and Mazaya Qatar Real Estate Dev.

rising 5.0% and 3.2% respectively. Among the top losers, Qatar Cinema & Film

Dist. Co. fell 7.0%, while Qatar General Ins. & Rein. Co. was down 4.2%.

%Chg.

(28.8)

0.1

6.6

(14.6)

(2.4)

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

15,965.04

2,761.52

2,631.44

3,725.85

1,952.28

2,024.03

2,607.31

1,563.43

6,077.59

3,211.50

0.2

0.1

(0.0)

0.4

0.8

0.3

(0.3)

(0.7)

0.1

(0.2)

0.2

0.1

(0.0)

0.4

0.8

0.3

(0.3)

(0.7)

0.1

(0.2)

7.7

6.7

7.7

6.5

5.1

3.6

11.6

7.5

2.2

5.8

N/A

13.7

13.3

13.5

13.2

13.9

10.4

21.0

23.1

16.4

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index rose 0.9% to close at 8,835.1. Gains were led

by the Hotel & Tourism and Real Estate Dev. indices, rising 2.3% and 1.9%

respectively. Nat. Agri. Mark. rose 6.1%, while Saudi Investment was up 5.8%.

Saudi Investment Bank

Saudi Arabia

Ahli United Bank

Dubai: The DFM index declined 0.4% to close at 3,754.4. The Services index

fell 1.7%, while the Investment & Financial Services index was down 1.4%. Al

Salam Sudan declined 6.4%, while Al Salam Bank - Bahrain was down 4.5%.

Abu Dhabi: The ADX benchmark index rose 0.4% to close at 4,692.9. The

Services index gained 1.5%, while the Banking index was up 1.2%. Ras Al

Khaimah Cement Co. surged 14.6% and Gulf Med. Projects Co. gained 8.3%.

Abu Dhabi Comm. Bank

Kuwait: The KSE index gained 0.7% to close at 7,810.1. The Consumer

Services and Real Estate indices rose 1.1% each. Amar for Finance & Leasing

Co. gained 8.8%, while Alrai Media Group Co. was up 6.8%.

Oman: The MSM index rose 0.1% to close at 7,092.5. The Financial and

Services indices, gained 0.1% each. Al Madina Takaful rose 5.9%, while Al

Madina Investment was up 4.5%.

Bahrain: The BHB index declined 0.2% to close at 1,291.2. The Industrial

index fell 1.6%, while the Commercial Banking index was down 0.4%. Al

Salam Bank declined 9.3%, while Khaleeji Commercial Bank was down 4.7%.

30 Jan 14

496.7

589,352.1

10.3

5,219

42

10:27

Close#

1D%

30.90

5.8

1,583.4

7.7

Kuwait

0.75

5.6

836.7

4.2

Gulf International Ser.

Qatar

79.30

5.0

443.4

30.0

Alinma Bank

Saudi Arabia

17.40

4.8

78,589.3

16.8

Abu Dhabi

6.88

3.9

3,786.2

5.8

GCC Top Losers

Exchange

#

Gulf Pharma. Industry

Abu Dhabi

3.22

(9.3)

731.7

(1.5)

Atheeb Telecom

Saudi Arabia

14.85

(4.5)

10,583.3

3.1

Qatar Gen. Ins. & Rein.

Qatar

43.10

(4.2)

13.8

(10.0)

Al-Qurain Petrochem.

Kuwait

0.23

(3.4)

119.9

3.6

Deyaar Development

Dubai

1.26

(3.1)

30,511.5

24.8

##

Close

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Gulf International Services

79.30

5.0

443.4

30.0

Qatar Cinema & Film Dist. Co.

40.00

(7.0)

0.5

(0.2)

Mazaya Qatar Real Estate Dev.

12.59

3.2

2,564.8

12.6

Qatar General Ins. & Rein. Co.

43.10

(4.2)

13.8

(10.0)

Doha Insurance Co.

30.85

2.8

62.9

23.4

Zad Holding Co.

69.50

(3.5)

4.5

0.0

Salam International Investment Co.

13.70

1.5

2,495.3

5.3

Dlala Brok. & Inv. Holding Co.

22.00

(2.7)

42.8

(0.5)

Medicare Group

53.60

1.1

171.1

2.1

Qatari Investors Group

47.00

(2.4)

176.2

7.6

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Industries Qatar

179.70

(0.1)

38,749.9

6.4

30.0

Qatar Exchange Top Gainers

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

Mazaya Qatar Real Estate Dev.

12.59

3.2

2,564.8

12.6

Salam International Investment Co.

13.70

1.5

2,495.3

5.3

Gulf International Services

79.30

5.0

34,567.8

Qatar Gas Transport Co.

21.00

0.9

1,090.0

3.7

Salam International Investment

13.70

1.5

34,027.0

5.3

United Development Co.

22.71

0.4

820.1

0.4

Mazaya Qatar Real Estate Dev.

12.59

3.2

32,816.1

12.6

Vodafone Qatar

11.31

(1.0)

630.8

5.6

Qatar Navigation

88.90

1.0

25,254.3

7.1

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Source: Bloomberg (* in QR)

Close

1D%

WTD%

MTD%

YTD%

11,173.97

3,754.43

4,692.88

8,835.12

7,810.11

7,092.53

1,291.17

0.2

(0.4)

0.4

0.9

0.7

0.1

(0.2)

0.2

(0.4)

0.4

0.9

0.7

0.1

(0.2)

0.2

(0.4)

0.4

0.9

0.7

0.1

(0.2)

7.7

11.4

9.4

3.5

3.5

3.8

3.4

Exch. Val. Traded

($ mn)

97.06

302.53

277.20

1,914.84

112.99

28.16

1.72

Exchange Mkt.

Cap. ($ mn)

161,943.1

76,442.6

131,486.3

484,819.9

110,752.0

25,471.5

50,487.8

P/E**

P/B**

14.0

19.1

12.9

17.7

17.1

11.0

8.5

1.9

1.4

1.6

2.2

1.2

1.6

0.9

Dividend

Yield

4.1

2.4

3.8

3.3

3.6

3.7

3.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.2% to close at 11,174.0. The

Transportation and Industrials indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Gulf International Services and Mazaya Qatar Real Estate Dev.,

were top gainers, rising 5.0% and 3.2% respectively. Among the

top losers, Qatar Cinema & Film Dist. Co. fell 7.0%, while Qatar

General Ins. & Rein. Co. declined 4.2%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

59.78%

64.74%

(17,540,297.71)

Non-Qatari

40.23%

35.26%

17,540,297.71

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday rose by 6.6% to 11.0mn

from 10.3mn on Thursday. Further, as compared to the 30-day

moving average of 10.4mn, volume for the day was 6.2% higher.

Mazaya Qatar Real Estate Dev. and Salam International

Investment Co. were the most active stocks, contributing 23.3%

and 22.7% to the total volume respectively.

Earnings

Earnings Releases

Company

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

AED

1,511.6

10.5%

140.3

0.1%

235.8

9.9%

AED

850.0

5.2%

–

–

76.4

16.3%

Dubai

AED

310.8

11.9%

–

–

54.5

94.5%

Dubai

AED

1,331.7

18.3%

118.5

-46.5%

241.8

1.0%

Abu Dhabi

AED

303.1

6.7%

–

–

48.8

-1.1%

Abu Dhabi

AED

12.3

-1.6%

–

–

24.5

148.3%

Abu Dhabi

AED

219.9

0.4%

7.6

NA

7.9

NA

Abu Dhabi

AED

2,390.0

3.0%

–

–

571.0

-5.6%

Kuwait

KD

26.0

-22.5%

–

–

6.0

1965.4%

Kuwait

KD

–

–

–

–

9.0

125.0%

Oman

OMR

2.2

8.0%

0.7

5.2%

0.6

175.9%

Oman

OMR

4.4

4541.3%

–

–

–

–

Market

Currency

Orient Insurance Co. (OIC)*

Dubai

Aramex

AI Sagar National Insurance

Co.*

Oman Insurance Co.*

Dubai

Al Dhafra Insurance Co.*

Umm Al Qaiwain Cement

Industries Co.*

Ras AI Khaimah Cement Co.

(RAK Cement)*

Dana Gas Co. *

Al Mazaya Holding Co.*

Qurain Petrochemical

Industries Co. (QPIC)**

Oman Chromite Co. (OCC) *

Packaging Co. Ltd *

% Change

YoY

Source: Company data, DFM, ADX, MSM (*FY2013 results) (**9 months ended December 31, 2013)

News

Qatar

Qatar posts QR30.9bn trade surplus in November –

According to the preliminary data released by the Ministry of

Development Planning & Statistics, Qatar registered a foreign

trade surplus of QR30.9bn in November 2013. This indicates a

decline of QR1.3bn as compared to November 2012. Qatar‟s

total exports of goods – including exports of domestic origin and

re-exports – amounted to QR39.8bn in November 2013,

showing a drop of 0.9% over November 2012. However, total

imports in November 2013 stood at QR8.9bn, a 12.4% increase

over the value recorded in November 2012. Qatar‟s main

exporting destinations were Japan, with a share of 29% of total

exports, followed by South Korea (17%) and India (9%).

Automobiles, aircraft spare parts, telephone sets, mobiles and

ancillaries were the main items imported by Qatar in November

2013. The US was the leading country exporting to Qatar with a

share of 11% of the total imports, followed by China (9%),

Germany and the UAE (7% each). (Gulf-Times.com)

QNB Group eyes MENA, Sub-Saharan Africa for expansion

– QNB Group – which now has presence in 26 countries – said

it will continue to invest strategically across the MENA region as

well as Sub-Saharan Africa. Further, QNB Group is also

planning to expand its retail banking operations in selected

markets and to extend its loyalty rewards program for overseas

transactions as well through additional partners. HE the Finance

Minister Ali Sharif al-Emadi said that the group‟s primary focus is

to retain its leading position by diversifying income sources and

expanding the range of activities across the group. Meanwhile,

during its AGM, QNB Group‟s shareholders approved the

board‟s proposal to distribute 70% cash dividend for 2013. (GulfTimes.com)

QNB expansion plans to focus on global deals – QNB

Group's expansion plans for the next three years will refocus on

global expansions while maintaining its dominant position in

Qatar. By 2017, the bank expects 60% of its net profit

contribution and 55% of net assets contribution from its

international operations, thus positioning QNB as a transactionbanking leader in the MENA region. QNB's Group Corporate &

Institutional Banking (GCI) continued to be the key engine of the

Group's profit and growth in 2013. The corporate banking

department within the GCI provided several bilateral financing

facilities last year for clients such as Nakilat, Halul Offshore and

Gulf LPG. The contracting unit of GCI financed a wide range of

key projects in 2013. These included a 10-year loan facility

agreement with United Development Company (UDC), the

master developer of The Pearl-Qatar, and a term loan financing

the development of the Mall of Qatar, a large mall under

construction near Qatar Foundation. A QNB Group-led

syndicate of banks was mandated for the provision of the full

banking facilities and associated requirements for the new Doha

Page 2 of 6

3. Metro Project-Red Line South package. GCI is highly supportive

of a key pillar of the Qatar National Vision 2030-nurturing growth

of SMEs. In 2013, GCI's Global Structure Finance (GSF)

department was involved in several significant transactions.

Within Qatar, QNB Group supported Ooredoo as general

financial adviser, documentation coordinator, facility agent as

well as initial mandated lead arranger in arranging a $1bn

Revolving Credit Facility, among others. (Peninsula Qatar)

Brand Finance: QNB Group is Middle East’s most valuable

bank brand – According to an annual study "The Brand Finance

Banking 500" conducted by Brand Finance, Middle East banks

have had an extremely successful year, almost all improving

their global rank with at least double-digit brand value % growth.

QNB Group leads the group for another year with a brand value

of $1.8bn. This is up 38.5% on 2013, an increase of over half a

billion dollars. This puts QNB just outside the global top 100, but

with such impressive growth, it is sure to break into that group

next year. (Bloomberg)

QFCRA implements changes to Controller Framework for

QFC-authorized firms – The Qatar Financial Centre Regulatory

Authority‟s (QFCRA) board has approved the changes in rules

relating to significant ownership positions in QFC-authorized

firms with effect from February 1, 2014. The implementation

follows a period of consultation with industry in 4Q2013, during

which the QFCRA issued a consultation paper seeking input on

the proposed changes. The amendments to the general rules

include the following: controller band threshold approval, letter of

comfort, and maintain systems & controls. QFCRA has

introduced thresholds for the approval of controller shareholding,

based on propriety and the financial capability of the

shareholder. Similarly, it has stipulated requirements for

significant controller shareholders who cross a 49% or 74%

shareholding threshold to provide a „letter of comfort‟ to QFCRA,

confirming the shareholders‟ capability to support the firm.

Further, QFCRA has stipulated requirements for authorized

firms to submit specific reports and maintain systems & controls

that allow the firm to monitor controller shareholder positions;

make required applications for approval; and prevent

shareholding increases across band thresholds. These

proposals are relevant to all QFC authorized firms and any firms

considering doing business in the QFC. (GulfBase.com)

ORDS: All buildings in Qatar to be fiber-connected by 2014end – Ooredoo‟s (ORDS) COO Waleed Mohamed al-Sayed

said that all residential and commercial buildings in the country

will be connected through optic fiber before the year-end. In

terms of migration of customers to the fiber network (FTTH),

Ooredoo plans to complete the work by end-2014. ORDS has

already connected around 100,000 customers to its fiber

network. The nationwide rollout of the fiber network is in line with

the country‟s ambitious Qatar National Vision 2030, which aims

to develop a knowledge-based economy built upon a strong

infrastructure foundation. (Gulf-Times.com)

QIFL to pay GMTN interest payments – Ooredoo (ORDS)

announced that its subsidiary QTEL International Finance

Limited (QIFL) will pay interest payments to its global medium

term note (GMTN) holders on February 18 & 21, 2014. (QE)

MERS’ BoD to meet on February 17 – Al Meera Consumer

Goods Company‟s (MERS) board of directors will meet on

February 17, 2014 to discuss the company‟s financial results

ending on December 31, 2013. (QE)

AKHI opens candidacy for board directorship – Al Khaleej

Takaful Group‟s (AKHI) board has announced the opening of

candidacy for its board directorship for the next three years,

which is open for applications from January 26, 2014 until

February 9, 2014. (QE)

IQCD announces dates for board meeting, AGM – Industries

Qatar Company‟s (IQCD) board will meet on February 16, 2014

to discuss the company‟s financial results ending on December

31, 2013. Meanwhile, IQCD‟s AGM will be held on March 10,

2014. (QE)

QOIS’ BoD to meet on February 26, AGM on March 24 –

Qatar Oman Investment Company‟s (QOIS) board will meet on

February 26, 2014 to discuss the company‟s financial results

ending on December 31, 2013. Meanwhile, QOIS‟ AGM will be

held on March 24, 2014. (QE)

International

ECB set to reveal further detail of bank health checks – The

European Central Bank (ECB) will reveal more detail on how it

plans to go about checking that top Eurozone banks have the

risks on their balance sheets under control. The ECB's asset

quality review (AQR) is part of a broader examination that also

includes a stress test to see how banks hold up under shock

scenarios, to avoid nasty surprises once the ECB takes up

responsibility for supervising them from November. It aims to

encourage banks to recognize losses on loans or investments

that have soured over time, allowing them to regain investors'

trust and free up capacity to grant new loans to help along the

euro zone's fragile economic recovery. (Reuters)

China's January official services PMI falls to 53.4 – Growth

in China's services sector cooled in January to its slowest pace

in at least a year. The official non-manufacturing Purchasing

Managers' Index slipped to 53.4 from December's 54.6, the

lowest reading in at least a year but still above the 50-point level

that indicates growth. (ET)

Regional

GPCA: GCC petrochemicals set for export surge – The Gulf

Petrochemicals & Chemicals Association (GPCA) stated that the

petrochemical industry in the GCC region is set to record a rapid

increase in exports in 2014 due to the World Trade

Organization's (WTO) Bali Package. According to the WTO, the

benefits accruing to the world economy from the Trade

Facilitation Agreement adopted as part of WTO‟s Bali Package

are estimated to be anywhere between $400bn and $1tn. Costs

of trade are set to decrease by 10-15%, contributing to

increased trade flows and higher revenues while creating a

stable business environment. (GulfBase.com)

ABCC: Brazilian imports from Arab nations reach $11.4bn

in 2013 – According to the Arab-Brazilian Chamber of

Commerce (ABCC), Brazilian imports from Arab nations in 2013

were recorded at $11.4bn. These imports consisted of

petroleum, fertilizers, plastic, glass and glassware, seafood, and

electric machinery. Arab countries collectively accounted for a

2.72% growth in Brazilian imports in 2013 over the previous

year. Saudi Arabia was the biggest exporter with $3.2bn,

followed by Algeria ($3.1bn), Morocco ($1.4bn), Kuwait

($1.0bn), and Iraq ($691mn). (GulfBase.com)

SEC raises SR4.5bn from sukuk – The Saudi Electricity

Company (SEC) has raised SR4.5bn from the sale of an Islamic

bond. The sukuk was priced at 70 basis points over the threemonth Saudi Interbank Offered Rate (Saibor). In early January,

SEC stated that it had chosen banks to arrange for the riyaldenominated transaction. (GulfBase.com)

Al Khodari renews SR290.1mn Islamic credit facilities with

GIB – Abdullah A. M. Al Khodari Sons Company has renewed

its Islamic credit facilities agreement worth SR290.1mn with Gulf

Page 3 of 6

4. International Bank (GIB). These credit facilities provide bonding

commitments and fund the company‟s working capital and

capex requirements. Around 36% of these facilities are funded

under Murabaha modes of financing, whereas 64% limits are for

multipurpose bonds and documentary credits. The credit limits‟

tenor ranges from 6 months to 48 months, depending upon the

purpose of their utilization. (Tadawul)

Saudi Orix’s BoD recommends SR25.5mn dividends – Saudi

ORIX Leasing Company‟s board of directors has recommended

the distribution of dividends worth SR25.5mn to its shareholders

for FY2013. The dividend per share will be SR0.75, representing

7.5% of the face value of the share. Shareholders registered on

the day of the general assembly meeting will be eligible for this

dividend. (Tadawul)

SAMA approves UCA’s insurance products – The United

Cooperative Assurance Company (UCA) has obtained SAMA‟s

approval for the extension of its temporary approval for its motor

insurance – all risks both commercial and private and motor

third party liability insurance for three months until April 30,

2014. (Tadawul)

Knight Frank: Dubai’s prime industrial rents rise – According

to a report by Knight Frank, the prime industrial rents in Dubai

appear to be on a firm path to recovery. In the last six months of

2013, the average rental values for class 1 property rose by

12% semi-annually and were up 18% as compared to the same

period the year before. (GulfBase.com)

Emaar to launch 98 new villas in Dubai on February 8 –

Emaar Properties is set to launch its first Arabesque-style villa

community named “Yasmin” in Arabian Ranches in Dubai on

February 8, 2014. The Yasmin villa community features 98 villas

to be built in five different types of four-to-six bedrooms and

nestled in landscaped green spaces and private gardens. Emaar

has launched numerous new residential units over the past few

weeks including Vida Residence, The Hills, Lila in Arabian

Ranches, Vida Residence in Downtown Dubai, Rasha in

Arabian Ranches, Boulevard Point in Downtown Dubai.

(GulfBase.com)

Arqaam becomes Nasdaq Dubai trading member – Arqaam

Capital has become an equities trading member of Nasdaq

Dubai, enabling it to offer its clients any opportunity to trade

shares directly on Nasdaq Dubai. Arqaam is already a member

of NASDAQ Dubai's equity derivatives market, which comprises

futures on the FTSE NASDAQ Dubai UAE 20 index and on 20

companies listed in the UAE. (GulfBase.com)

DFM proposes 5% cash dividend – The Dubai Financial

Market (DFM) has proposed a cash dividend of 5% of the

capital. Meanwhile, DFM‟s AGM will be held on March 3, 2014.

(DFM)

Ras Al Khaimah DCA inks partnership deal with Air Arabia –

Ras Al Khaimah‟s Department of Civil Aviation (DCA) has

signed a strategic partnership with Air Arabia for operating

services from Ras Al Khaimah International Airport. This

partnership will increase the number of destinations accessible

to Ras Al Khaimah and neighboring Northern Emirates, and is

expected to support its standing as an attractive tourist

destination. Air Arabia will now become the official carrier for

Ras Al Khaimah Emirate. (DFM)

Orient’s BoD approves 20% cash dividend, recommends

capital increase – The Orient Insurance Company‟s (Orient)

board of directors has recommended 20% cash dividends for its

shareholders. Orient‟s BoD has also recommended increasing

the company‟s capital from AED405mn to AED500mn by issuing

bonus shares. (DFM)

UNB reports AED1,748mn profit for FY2013 – Union National

Bank (UNB) has reported a profit of AED1,748mn for FY2013,

an increase of 9% YoY. EPS for 2013 improved to AED0.62

from AED0.56 in 2012. Total assets increased by 1% YoY to

AED87.5bn in 2013. Customer deposits recorded a growth of

3% YoY reaching AED65.1bn as on December 31, 2013, while

loans & advances increased by 5% YoY in 2013 to reach

AED60.0bn. Meanwhile, the bank‟s board has recommended a

15% cash dividend and 5% bonus shares. (ADX)

Abu Dhabi renews buildings contract with ADCB unit – The

Department of Finance–Abu Dhabi (DoF) has renewed the

management agreement signed with Abu Dhabi Commercial

Properties (ADCP), a subsidiary of Abu Dhabi Commercial Bank

(ADCB). The contract aims to promote further stability across

the Abu Dhabi property market and the overall economy, by

ensuring first-class services for both commercial and residential

buildings. (GulfBase.com)

Etihad in final stage for Alitalia stake buy – Etihad Airways is

in the final phase of a due diligence process that may result in

an investment in the troubled Italian airline, Alitalia. According to

sources, Alitalia and Etihad have been in talks for several weeks

on a possible investment by the Abu Dhabi-based carrier, which

could involve Etihad buying a 40% stake in Alitalia for

$404.6mn. (GulfBase.com)

Bank of Sharjah’s BoD approves 12.5% cash dividend – The

Bank of Sharjah‟s board of directors has approved the

distribution of 12.5% cash dividend 60,000,000 buy back shares,

representing 2.86% of the paid-up capital. (ADX)

QCEM’s BoD recommends 7% cash dividend – Umm Al

Qaiwain Cement Industries Company‟s (QCEM) board of

directors has recommended a cash dividend of 7% of the paidup capital for 2013. (ADX)

CBK announces implementation of Basel III norms – HE the

Governor of the Central Bank of Kuwait (CBK), Dr. Mohammad

Y. Al Hashel announced the implementation of Basel III capital

adequacy standards by all Kuwaiti banks. CBK is raising the

minimum capital adequacy ratio requirement for Kuwaiti banks

from 12% in two stages: first to 12.5% by 2015 and then to 13%

by 2016. The Basel III norms include an increase in the total

ratio of the regulatory capital and a redefinition of the regulatory

capital. (GulfBase.com)

Dolphin Village adds 70 more villas, apartments – Yahya

Group has announced an addition of 70 villas and apartments

and a second swimming pool to its Dolphin Village in Bausher.

By August 2014, the Dolphin Village‟s expansion will be

completed with 59 additional homes that are currently under

construction. This will take the total number of luxury housing

units at the Village to 337. (GulfBase.com)

Investcorp’s net income jumps 53% YoY to $60.1mn 1H

FY2014 – Investcorp Bank‟s net income for 1H FY2014

increased by 53% YoY to $60.1mn. Total assets decreased by

4.8% YoY to $2.357bn. Basic EPS grew to $100 from $66 in 1H

FY2013. (Bahrain Bourse)

KHCB reports BHD19.21mn net loss in 2013 – Khaleeji

Commercial Bank (KHCB) has reported a loss of BHD19.21mn

in 2013 as compared to the profit of BHD0.75mn a year earlier.

The bank‟s total assets grew by 14.6% YoY to BHD542.2mn.

EPS fell to -17.07 fils from 0.67 fils in 2012. Meanwhile, KHCB‟s

board announced that the bank would not be paying a dividend

for 2013. (GulfBase.com)

ASSB reports BHD12.4mn net profit – Al Salam Bank-Bahrain

(ASBB) has reported a net profit of BHD12.4mn in 2013,

Page 4 of 6

5. reflecting an increase of 20% YoY. Income from financing

contracts jumped by 27% YoY to BHD26.1mn in 2013 from

BHD20.5mn in 2012. Total assets grew by 15.5% YoY to

BHD1.088bn from BHD0.942bn. EPS stood at 8.3 fils in 2013 as

compared to 6.9 fils in 2012. (Bahrain Bourse)

Bapco’s output soars to 96.3mn barrels – The Bahrain

Petroleum Company‟s (Bapco) refinery processed 96.3mn

barrels of crude oil in 2013, an increase of 9.6% over the

previous year. Bapco‟s Chairman & Acting Chief Executive Adel

Khalil Almoayyed said that refining activities were once again

the focus of performance optimization efforts, with a number of

notable results last year. (GulfBase.com)

Page 5 of 6

6. Daily Index Performance

0.9%

0.7%

0.8%

0.2%

0.1%

0.0%

(0.4%)

Aug-11

QE Index

Mar-12

Oct-12

May-13

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

(0.4%)

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

1,244.55

0.0

0.0

3.2

19.18

0.0

0.0

(1.5)

106.40

0.0

0.0

5.01

0.0

157.00

Global Indices Performance

Close

1D%

WTD%

YTD%

15,698.85

0.0

0.0

(5.3)

S&P 500

1,782.59

0.0

0.0

(3.6)

(4.0)

NASDAQ 100

4,103.88

0.0

0.0

(1.7)

0.0

15.3

STOXX 600

322.52

0.0

0.0

(1.7)

0.0

0.0

24.1

DAX

9,306.48

0.0

0.0

(2.6)

154.00

0.0

0.0

13.4

FTSE 100

6,510.44

0.0

0.0

(3.5)

DJ Industrial

1.35

0.0

0.0

(1.9)

CAC 40

102.04

0.0

0.0

(3.1)

Nikkei

GBP

1.64

0.0

0.0

(0.7)

MSCI EM

CHF

1.10

0.0

0.0

(1.5)

SHANGHAI SE Composite

AUD

0.88

0.0

0.0

(1.8)

USD Index

81.31

0.0

0.0

RUB

35.15

0.0

0.0

BRL

0.41

0.0

0.0

(2.1)

Yen

Kuwait

Jan-11

(0.2%)

Qatar

(0.8%)

Dubai

127.8

0.4%

0.4%

Abu Dhabi

140.6

Saudi Arabia

Jun-10

1.2%

160.6

Oman

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

Bahrain

Rebased Performance

4,165.72

0.0

0.0

(3.0)

14,914.53

0.0

0.0

(8.5)

936.53

0.0

0.0

(6.6)

2,033.08

0.0

0.0

(3.9)

HANG SENG

22,035.42

0.0

0.0

(5.5)

1.6

BSE SENSEX

20,513.85

0.0

0.0

(3.1)

6.9

Bovespa

47,638.99

0.0

0.0

(7.5)

1,301.02

0.0

0.0

(9.8)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6