24 April Daily market report

•

1 recomendación•391 vistas

The QE index in Qatar declined slightly, led by losses in the transportation and banking indices. Widam Food and Qatar International Islamic Bank were the top losers. In other GCC markets, Saudi Arabia's index rose slightly while Dubai and Abu Dhabi fell. Regional company earnings and global economic indicators were also reported.

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (8)

Similar a 24 April Daily market report

Similar a 24 April Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

24 April Daily market report

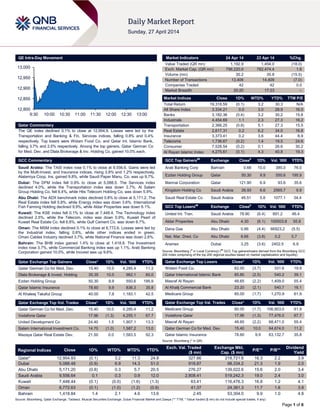

- 1. Page 1 of 6 QE Intra-Day Movement Qatar Commentary The QE index declined 0.1% to close at 12,954.9. Losses were led by the Transportation and Banking & Fin. Services indices, falling 0.8% and 0.4% respectively. Top losers were Widam Food Co. and Qatar Int. Islamic Bank, falling 3.7% and 2.5% respectively. Among the top gainers, Qatar German Co for Med. Dev. and Dlala Brokerage & Inv. Holding Co. gained 10.0% each. GCC Commentary Saudi Arabia: The TASI index rose 0.1% to close at 9,556.6. Gains were led by the Multi-Invest. and Insurance indices, rising 3.8% and 1.2% respectively. Alalamiya Coop. Ins. gained 9.8%, while Saudi Paper Manu. Co. was up 9.7%. Dubai: The DFM index fell 0.9% to close at 5,088.5. The Services index declined 4.0%, while the Transportation index was down 2.7%. Al Salam Group Holding Co. fell 6.4%, while Hits Telecom Holding Co. was down 5.9%. Abu Dhabi: The ADX benchmark index declined 0.8% to close at 5,171.2. The Real Estate index fell 5.8%, while Energy index was down 3.6%. International Fish Farming Holding declined 9.9%, while Aldar Properties was down 6.1%. Kuwait: The KSE index fell 0.1% to close at 7,448.4. The Technology index declined 2.5%, while the Telecom. index was down 0.9%. Kuwait Pearl of Kuwait Real Estate Co. fell 6.8%, while Gulf Cement Co. was down 6.7%. Oman: The MSM index declined 0.1% to close at 6,772.6. Losses were led by the Industrial index, falling 0.6%, while other indices ended in green. Oman Cables Industry declined 3.7%, while National Finance was down 2.6%. Bahrain: The BHB index gained 1.4% to close at 1,418.8. The Investment index rose 3.7%, while Commercial Banking index was up 1.1%. Arab Banking Corporation gained 10.0%, while Inovest was up 9.6%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar German Co for Med. Dev. 15.40 10.0 4,285.4 11.2 Dlala Brokerage & Invest. Holding 35.35 10.0 962.1 60.0 Ezdan Holding Group 50.30 9.9 550.6 195.9 Qatar Islamic Insurance 78.60 9.9 836.3 35.8 Al Khaleej Takaful Group 40.00 7.8 1,183.1 42.5 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Qatar German Co for Med. Dev. 15.40 10.0 4,285.4 11.2 Vodafone Qatar 17.96 (1.3) 4,255.1 67.7 United Development Co 24.40 1.5 1,907.1 13.3 Salam International Investment Co. 14.70 (1.0) 1,587.2 13.0 Mazaya Qatar Real Estate Dev. 21.50 0.0 1,583.5 92.3 Market Indicators 24 Apr 14 23 Apr 14 %Chg. Value Traded (QR mn) 1,192.9 1,454.0 (18.0) Exch. Market Cap. (QR mn) 796,220.0 782,474.4 1.8 Volume (mn) 30.2 35.8 (15.5) Number of Transactions 13,406 14,409 (7.0) Companies Traded 42 42 0.0 Market Breadth 20:20 17:23 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 19,318.59 (0.1) 3.2 30.3 N/A All Share Index 3,334.21 0.0 3.0 28.9 16.0 Banks 3,182.36 (0.4) 3.2 30.2 15.8 Industrials 4,454.69 1.1 2.3 27.3 16.2 Transportation 2,366.25 (0.8) 5.1 27.3 15.5 Real Estate 2,617.31 0.2 6.2 34.0 16.8 Insurance 3,373.41 0.2 3.6 44.4 8.9 Telecoms 1,736.67 (0.2) 1.4 19.5 24.6 Consumer 7,528.54 (0.2) 0.1 26.6 30.2 Al Rayan Islamic Index 4,275.61 (0.1) 4.3 40.8 19.3 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Arab Banking Corp Bahrain 0.66 10.0 385.0 76.0 Ezdan Holding Group Qatar 50.30 9.9 550.6 195.9 Mannai Corporation Qatar 121.90 6.9 93.6 35.6 Kingdom Holding Co Saudi Arabia 26.93 6.6 2565.7 9.9 Saudi Real Estate Co Saudi Arabia 46.51 5.6 1077.1 34.4 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% United Int. Tran. Saudi Arabia 78.80 (6.4) 891.2 46.4 Aldar Properties Abu Dhabi 4.30 (6.1) 100503.8 55.8 Dana Gas Abu Dhabi 0.86 (4.4) 66923.2 (5.5) Nat. Mar. Dred. Co Abu Dhabi 8.66 (3.8) 0.2 0.7 Aramex Dubai 3.25 (3.6) 2402.5 6.9 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Widam Food Co. 62.00 (3.7) 331.6 19.9 Qatar International Islamic Bank 85.80 (2.5) 540.2 39.1 Masraf Al Rayan 48.65 (2.2) 1,409.0 55.4 Al Khalij Commercial Bank 23.20 (2.1) 540.7 16.1 Medicare Group 85.00 (1.7) 1,270.9 61.9 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Medicare Group 85.00 (1.7) 106,903.0 61.9 Vodafone Qatar 17.96 (1.3) 77,476.0 67.7 Masraf Al Rayan 48.65 (2.2) 68,471.0 55.4 Qatar German Co for Med. Dev. 15.40 10.0 64,674.0 11.2 Qatar Islamic Insurance 78.60 9.9 63,132.7 35.8 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,954.93 (0.1) 3.2 11.3 24.8 327.66 218,721.6 16.3 2.2 3.9 Dubai 5,088.48 (0.9) 6.9 14.3 51.0 918.87 98,334.2 21.3 1.9 2.0 Abu Dhabi 5,171.20 (0.8) 0.3 5.7 20.5 276.27 139,022.6 15.6 2.0 3.4 Saudi Arabia 9,556.64 0.1 0.3 0.9 12.0 2,808.41 519,242.3 19.0 2.4 3.0 Kuwait 7,448.44 (0.1) (0.0) (1.6) (1.3) 63.41 116,476.3 16.8 1.2 4.1 Oman 6,772.63 (0.1) (1.0) (1.2) (0.9) 41.37 24,381.3 11.7 1.6 3.9 Bahrain 1,418.84 1.4 2.1 4.6 13.6 2.45 53,304.0 9.9 1.0 4.8 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,800 12,850 12,900 12,950 13,000 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QE index declined 0.1% to close at 12,954.9. The Transportation and Banking & Fin. Services indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Widam Food Co. and Qatar Int. Islamic Bank were the top losers, falling 3.7% and 2.5% respectively. Among the top gainers, Qatar German Co for Medical Devices and Dlala Brokerage & Inv. Holding Co. gained 10.0% each. Volume of shares traded on Thursday fell by 15.5% to 30.2mn from 35.8mn on Wednesday. However, as compared to the 30- day moving average of 26.8mn, volume for the day was 12.8% higher. Qatar German Co for Medical Devices and Vodafone Qatar were the most active stocks, contributing 14.2% and 14.1% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ragings, Earnings and Global Economic Data Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Arabia Insurance Cooperative Company (AICC) AM Best Saudi Arabia FSR/ICR B-/bb- C+/b- Negative – Kuwait Reinsurance Company (Kuwait Re) AM Best Kuwait FSR/ICR A-/a- A-/a- – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, ICR - Issuer Credit Rating) Earnings Releases Company Market Currency Revenue (mn)1Q2014 % Change YoY Operating Profit (mn) 1Q2014 % Change YoY Net Profit (mn) 1Q2014 % Change YoY Makkah Construction & Development Co. Saudi SR – – 339.0 -12.9% 324.0 -14.5% Finance House (FH) Abu Dhabi AED – – – – 35.5 37.6% First Dubai for Real Estate Development Co. Dubai AED 17.3 88.0% – – 8.1 NA National Securities Co. (NSC) Oman OMR 0.3 32.0% – – 0.7 NA Taageer Finance Co. Oman OMR – – – – 0.9 -9.9% A'Sharqiya Investment Holding Co. (SIHC) Oman OMR 1.0 12.3% – – 0.7 11.6% Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/24 US US Census Bureau Durable Goods Orders March 2.60% 2.00% 2.20% 04/24 US Department of Labor Initial Jobless Claims 19-April 329K 315K 305K 04/24 US Bloomberg Bloomberg Consumer Comfort 20-April -25.4 – -29.1 04/25 US Markit Markit US Composite PMI April 54.9 – 55.7 04/25 US Markit Markit US Services PMI April 54.2 55.5 55.3 04/24 France INSEE Production Outlook Indicator April -15 -12 -10 04/24 France INSEE Manufacturing Confidence April 100.0 100.0 101.0 04/24 France INSEE Business Confidence April 94.0 96.0 95.0 04/25 France French Labor Office Total Jobseekers March 3349.3k – 3347.7k 04/25 France French Labor Office Jobseekers Net Change March 1.6 – 31.5 04/24 Germany IFO IFO Business Climate April 111.2 110.4 110.7 04/24 Germany IFO IFO Current Assessment April 115.3 115.6 115.2 04/24 Germany IFO IFO Expectations April 107.3 105.8 106.4 04/24 UK CBI CBI Reported Sales April 30.0 17.0 13.0 04/25 UK UK Office for Nat. Statist Retail Sales Ex Auto MoM March -0.40% -0.50% 1.30% 04/25 UK UK Office for Nat. Statist Retail Sales Ex Auto YoY March 4.20% 4.50% 3.90% 04/25 UK BBA BBA Loans for House Purchase March 45933.0 48950.0 47196.0 04/25 Spain INE PPI MoM March 0.20% – -0.80% 04/25 Spain INE PPI YoY March -1.20% – -2.90% 04/25 Spain INE Total Mortgage Lending YoY February -11.60% – -25.80% Overall Activity Buy %* Sell %* Net (QR) Qatari 65.76% 71.81% (72,057,169.40) Non-Qatari 34.23% 28.20% 72,057,169.40

- 3. Page 3 of 6 04/25 Spain INE House Mortgage Approvals YoY February -33.00% – -32.40% 04/24 Japan Bank of Japan Corporate Service Px Index YoY March 0.70% 0.70% 0.70% 04/25 Japan MIA Natl CPI YoY March 1.60% 1.60% 1.50% 04/25 Japan MIA Natl CPI Ex Fresh Food YoY March 1.30% 1.40% 1.30% 04/25 Japan MIA Natl CPI Ex Food, Energy YoY March 0.70% 0.70% 0.80% 04/25 Japan METI All Industry Activity Index MoM February -1.10% -0.70% 1.70% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar QGTS posts net profit of QR207mn in 1Q2014 – Qatar Gas Transport Company (QGTS) posted a net profit of QR207mn vs. our estimate of QR206mn. On a YoY basis the earnings are up 17% from QR177mn in 1Q2013. (Peninsula Qatar, QNBFS Research) ERES net profit surges 82.3% in 1Q2014 – Ezdan Holding Group (ERES) announced its financials for 1Q2014, reporting jump of 82.3% in its profits to QR460.67mn as compared to QR252.72m for the corresponding period last year. (Peninsula Qatar) QGRI reports net profit of QR47.3mn in 1Q2014 – Qatar General Insurance & Reinsurance Company (QGRI) reported a net profit of QR47.3mn in 1Q2014 vs, QR44.1mn in 1Q2013, indicating a YoY growth of 7.2%. (QE) Qatar Rail gets first TBM for Doha Metro – The Qatar Railways Company (Qatar Rail) has taken delivery of the first of the 21 tunnel boring machines (TBMs), which will dig through a distance of 8 kilometers in 22 months for the Doha Metro. The TBM S-865 machine, also known as ‘Lebretha’, was manufactured by Herrenknecht in Germany, and is the first of the four TBMs that will be launched for the Doha Metro as part of the Red Line North Underground project. TBM Lebretha will be assembled and launched from the Al Wahda site toward West Bay Central, where it will be disassembled and re- assembled at Al Wahda and then travel toward the Doha Golf Course. The machine will bore the west tunnel of the drive, while another machine will bore the east tunnel. (Bloomberg) DIA handled 2.12mn passengers in March – Doha International Airport (DIA) has seen a 13.8% growth in March 2014, as compared to March 2013. DIA said that the total number of passengers stood at 2.12mn in March, which included all travelers who departed, transferred and arrived into Qatar. Cargo numbers also remained buoyant with an additional 14.83% traffic YoY. (Gulf-Times.com) Doha Port container capacity to expand by 50% – The Minister of Transport HE Jassim Seif Ahmed al-Sulaiti said that the annual container handling capacity of the existing Doha Port will be expanded by 50% to meet the country’s growing requirements due to ongoing developments in different areas. HE al-Sulaiti hoped that the port’s container handling capacity would reach 750,000 TEUs from the existing 500,000 TEUs. This will eventually be developed further to reach 1mn TEUs. He said until the opening of the New Doha Port the developmental works at Doha Port will continue. The minister also expressed the hope that the first phase of the New Doha Port, which is currently under construction near Al Wakrah, will be ready by mid-2016. (Gulf-Times.com) QIA eyeing investments in healthcare sector – According to sources, the Qatar Investment Authority (QIA) is planning to launch a fund for investing in healthcare companies. The sovereign wealth fund is in talks to appoint a financial adviser to assist with the process. QIA is seeking to profit from growth prospects in the healthcare industry and also diversify its investments. However, the size of the fund has not yet been decided. (Gulf-Times.com) International QNB Group: Markets calm in emerging economies – QNB Group said in its weekly analysis that capital flows to emerging markets (EMs) recovered in February and March 2014, leading to calmer financial markets. However, the fundamental weaknesses in specific EM economies have not been fully addressed, leaving them exposed to further rounds of capital outflows, weaker currencies and falling asset prices. Some EMs are likely to fare better than others, depending on their underlying fundamentals and the policy measures taken so far to address their imbalances. (Peninsula Qatar) Reuters: Rating agencies buy into Eurozone recovery story – Ratings agencies gave a broadly upbeat assessment of the Eurozone's creditworthiness last week, contrasting sharply with their reviews of recent years and reflecting growing confidence in the region's fiscal and economic recovery. On a day of credit updates scheduled for three of the bloc's top four economies, S&P affirmed its ratings on France, while Fitch Ratings raised its outlook on Italy and was expected to boost its view of Spain as well. S&P also raised its rating on Cyprus, suggesting the recovery is spreading to the peripheral regions left most exposed to the zone's financial crisis, which is its second upgrade of the bailed-out country since last year. Borrowing costs for those countries worst hit by the crisis have fallen sharply this year as the European Central Bank's loose monetary policy has encouraged investors hunting for returns to bet on their recovering economies. Fitch's outlook upgrade on Italy to 'stable', with the sovereign rating affirmed at 'BBB+', follows a rise earlier this month of its outlook on bailed-out Portugal to 'positive' from 'negative.' Italy was the fulcrum of the debt crisis a couple of years ago together with Spain, whose sovereign rating many investors and analysts in Madrid expect Fitch to upgrade or underpin with an improved outlook later. S&P confirmed France's long-term rating at 'AA' with a stable outlook. (Reuters) Yellen concerned fed model fails to predict price moves – The US Federal Reserve Chair Janet Yellen is concerned that the standard models used by central banks to forecast inflation may be broken. Behind her disquiet lies the failure of these models in foreseeing prices in the US during the last recession and its aftermath as well as in Japan during its deflationary period from 1998 to 2012. Inflation in the US has been higher than the simulations suggested, while Japanese price declines proved more persistent. Yellen stated that the Fed has to observe carefully to see if inflation picks up just as the way the central bank projects over the next few years. If it does not happen, Yellen suggested that the Fed would have to keep short-term interest rates near zero as it seeks to avoid Japan’s experience of a prolonged period of falling prices, wages and a stagnant economy. (Bloomberg) Tokyo inflation quickens to fastest since 1992 – Japanese statistics bureau data showed that consumer prices in Tokyo rose 2.7% in April from a year earlier, the biggest jump since

- 4. Page 4 of 6 1992, due to a sales-tax increase and a year of unprecedented stimulus from the Bank of Japan. Inflation excluding fresh food accelerated from 1% in the previous month, while the same price gauge for the nation rose 1.3% in March 2014 from March 2014, showed today. The data provided a first look at the effects of the April 1 tax rise that is dampening consumer demand and is projected to tip the Japanese economy into a one-quarter contraction. Ahead of the BoJ’s release of updated growth and inflation forecasts next week, investors are assessing whether price gains, fueled by a weaker yen and higher energy costs, will spread throughout the economy. (Bloomberg) Regional MCDC’s BoD recommends SR412mn dividends – Makkah Construction & Development Company’s (MCDC) board of directors has recommended the distribution of 25% dividend (SR2.5 per share), amounting to SR412mn for the financial year ended. (Tadawul) SAMA approves Al Alamiya’s capital increase – The Saudi Arabian Monetary Agency (SAMA) has approved Al Alamiya for Cooperative Insurance Company’s (Al Alamiya) request to raise its capital by SR200mn through a rights issue. The final approval from SAMA is subject to meeting the requirements within a period of four months. (Tadawul) CIDIC, Trans Sadara to develop 11 hospitals in Kingdom – Hong Kong-based China International Development & Investment Corporation Ltd (CIDIC) has entered into a cooperation agreement with the Saudi-based Trans Sadara Company, to set up Lana Medical Services Projects Company. This new company will develop 11 hospitals with a total of 200 beds in various cities of Saudi Arabia such as Dammam, Riyadh, Jiazan and Yanbu. Each of these hospitals will have patient & rehabilitation center, well-equipped surgical units including pharmacy, servicing patients with both Chinese and Western medical treatment methods. The project’s first phase will start in Jubail in the Eastern Province in an area of 20,000 square meters with total investment of SR350mn. (GulfBase.com) Tharawat to acquire majority stake in Quantum – Saudi- based Tharawat Holding Company is acquiring a majority stake of around 54% in Quantum Investment Bank Ltd. Quantum’s platform would help Tharawat Holding to expand its geographical presence by moving to international markets. The acquisition will enhance Quantum’s presence in Saudi Arabia. (GulfBase.com) SWCC launches operations at SR27bn desalination plant – The Saudi Water & Electricity Minister, Abdullah Al-Hussayen has launched the first phase of operations at the world’s biggest desalination plant project costing SR27bn. The minister stated that the Ras Alkhair plant was considered the biggest desalination plant for Saline Water Conversion Corporation (SWCC) with a production capacity of 1.025mn cubic meters of desalinated water a day and 2,600 MW of electricity. The plant located 60 km northwest of Jubail will supply 800,000 cubic meters of water to Riyadh and 100,000 cubic meters of water to Al-Washm, Sudair, Majma, Alzulfi and Al-Ghat areas. (GulfBase.com) Etihad appoints new GM for Cyprus – Etihad Airways has appointed Abdelrahman Abdullah Al Madhloum Al Suwaidi as the new General Manager for its Cyprus operations. (GulfBase.com) EIB’s profit surges to AED94mn in 1Q2014 – Emirates Islamic Bank’s (EIB) net profit for 1Q2014 has surged to AED94mn as compared to AED33mn in 1Q2013. The bank’s total income grew to AED512mn in 1Q2014 from AED443mn in 1Q2013. EPS amounted to AED0.024 as against AED0.012 a year ago. Total assets stood at AED41.2bn at the end of 1Q2014 as compared to AED39.8bn a year earlier. (DFM) Emaar Properties declares 15% cash dividend, 10% bonus shares – Emaar Properties’ AGM has approved the distribution of 15% cash dividend amounting to AED975mn for FY2013. The AGM further approved 10% bonus shares (650mn shares) valued at AED7.12bn, amounting to AED10.95 per share as of April 23, 2014. (DFM, Gulfbase.com) Emirates NBD reports AED1bn net profit in 1Q2014 – Emirates NBD has reported a net profit of AED1.0bn for 1Q2014 as compared to AED837mn for 1Q2013, reflecting an increase of 25%. Net interest income grew to AED1.95bn from AED1.50bn in 1Q2013. EPS amounted to AED0.17 at the end of 1Q2014 as against AED0.14 a year earlier. The bank’s total assets stood at AED347bn in 1Q2014 as compared to AED342bn in 1Q2013. Loans were at AED239.7bn, while customer deposits stood at AED251.5bn. (DFM) CBD’s reports 16% growth in net profit in 1Q2014 – The Commercial Bank of Dubai (CBD) has reported a net profit of AED285mn in 1Q2014, which is 16% higher than AED246mn in 1Q2013. Net interest income grew to AED373mn in 1Q2014 as compared to AED359mn in 1Q2013. EPS amounted to AED0.13 as compared to AED0.11 a year ago. The bank’s total assets at the end of 1Q2014 stood at AED43.8bn as compared to AED38.9bn in 1Q2013. Loans & advances stood at AED29.9bn, while customer deposits stood at AED30.5bn as at March 31, 2014. (DFM) DP World in talks with banks for $3bn loan – According to sources, Dubai-based DP World is in talks with lenders to triple the size of its existing $1bn loan, as well as extend the lifespan and cut the interest rate. The firm is aiming to raise its loan to $3bn. The original five-year revolving credit facility was signed in April 2012 and has already been renegotiated once, adding a year to the loan’s lifespan in June 2013. (GulfBase.com) Marka’s IPO raises AED10bn – UAE-based retailer Marka’s first initial public offering (IPO) has been oversubscribed by more than 36 times, raising AED10bn instead of the AED275mn target on the Dubai Financial Market (DFM). The company is planning to spend the proceeds on opening 100 fashion stores, restaurants and cafes across the Gulf region over the next five years. Marka had offered for sale 55% of its capital or 275mn shares, at AED1 per share. The company’s founders notified that the allocation of shares would be 2.77% and it will start the refunds on May 8, 2014. (GulfBase.com) GMPC declares 5% dividend, 5% bonus shares – Gulf Medical Projects Company’s (GMPC) AGM has approved the board’s proposal for the distribution of 5% cash dividend and 5% bonus shares for the year ended December 31, 2013. (ADX) Aldar launches sale of penthouses at Gate Towers – Aldar Properties has launched the sale of 21 exclusive duplex penthouse apartments at Gate Towers, in Shams Abu Dhabi on Al Reem Island. The the Penthouse Collection is located in a curved sky-bridge spanning approximately 300 meters across three towers. (GulfBase.com) Abu Dhabi Airport’s passenger numbers rises 15.1% in 1Q2014 – According to latest statistics, Abu Dhabi International Airport has reported a 15.1% increase in its passenger traffic during 1Q2014 as compared to 1Q2013. A total of 4.56mn passengers used Abu Dhabi International Airport in 1Q2014 as compared to 3.96mn passengers in 1Q2013. Aircraft movements rose to 35,844 in 1Q2014, representing 11.8%

- 5. Page 5 of 6 growth compared with 32,062 movements logged in 1Q2013. Cargo activity rose to 183,344 tons handled at the three terminals, a 15.8% increase over 1Q2013. (GulfBase.com) JLL: Abu Dhabi’s housing rents soar 17% in 2013 – According to a report by Jones Lang LaSalle (JLL), the Abu Dhabi real estate market continued to show signs of growth and recovery during 1Q2014. Demand for the residential rental market also continues to rise driven by new job creation and government policies, leading to 17% rental growth for prime, high quality units during 2013 and 4% growth during 1Q2014. The latest quarter continued to witness growth in the prime residential market and further stabilization of the office and hospitality sectors. Retail rents for malls on Abu Dhabi Island witnessed a slight increase during the quarter. (GulfBase.com) CBK: Kuwait’s BoP shows increase in overall surplus – According to the Provisional data from the Central Bank of Kuwait (CBK), Kuwait’s balance of payments (BoP) for 2013 has indicated continued surplus in the external balances. Developments in the financial account of Kuwait's BoP during 2013 demonstrated a slow growth in the net value of external assets owned by residents to reach KD21.7bn as against KD23.6bn during 2012. Consequently, the overall surplus of Kuwait's BoP amounted to KD954mn during 2013 against KD918mn during 2012. The overall position of Kuwait's BoP from a broader perspective shows a surplus of KD16.3bn during 2013 against KD20.7bn during 2012. The current account realized a surplus of KD20.3mn (39.7% of GDP) during 2013 against KD22.1bn (43.1% of GDP) during 2012. (GulfBase.com) AUB posts KD12.1mn net profit in 1Q2014 – Ahli United Bank (AUB) posted a net profit of KD12.1mn in 1Q2014, up 10.9% YoY. AUB noted that each share made gains estimated at 9.4 fils as compared to 8.5 fils in the corresponding period of 2013. AUB's Board Chairman Anwar Al-Mudhaf stated that the bank’s total operating revenues reached KD24.8mn and its total assets blossomed to KD3.37bn vis-a-vis KD3.16bn in the corresponding period of last year. He added that total deposits accounted for KD2.23bn, up 6.6% YoY. (Bloomberg) Arabian Sugar sees room for more refineries – Bahrain- based Arabian Sugar Company sees room for more sugar refining capacity in the Middle East and North Africa to fill a 7.5mn tons supply gap. Yves el-Mallat, CEO of the refinery said that the region is still short of refining capacity. El-Mallat said the Middle East & North Africa region is expected to consume 12.5mn tons of white sugar in 2014, with an annual rise in consumption of around 3% to 4%. Situated in Bahrain's Industrial Investment Park, the refinery will reach full production capacity of around 600,000 tons a year by early 2015. (Gulf- Times.com) KHCB expands with eighth branch in Bahrain – Khaleeji Commercial Bank (KHCB) has opened its eighth branch in Bahrain, in Zinj area. (GulfBase.com)

- 6. Contacts Saugata Sarkar Keith Whitney Sahbi Kasraoui Head of Research Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC 0.1% (0.1%) (0.1%) 1.4% (0.1%) (0.8%) (0.9%) (1.6%) (0.8%) 0.0% 0.8% 1.6% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,303.20 0.8 0.7 8.1 DJ Industrial 16,361.46 (0.8) (0.3) (1.3) Silver/Ounce 19.69 0.1 0.4 1.1 S&P 500 1,863.40 (0.8) (0.1) 0.8 Crude Oil (Brent)/Barrel (FM Future) 109.58 (0.7) 0.0 (1.1) NASDAQ 100 4,075.56 (1.8) (0.5) (2.4) Natural Gas (Henry Hub)/MMBtu 4.70 (2.2) 3.0 8.2 STOXX 600 333.50 (0.8) 0.3 1.6 LPG Propane (Arab Gulf)/Ton 110.75 (1.2) (1.7) (12.3) DAX 9,401.55 (1.5) (0.1) (1.6) LPG Butane (Arab Gulf)/Ton 122.63 (0.9) (1.7) (10.2) FTSE 100 6,685.69 (0.3) 0.9 (0.9) Euro 1.38 0.0 0.2 0.7 CAC 40 4,443.63 (0.8) 0.3 3.4 Yen 102.16 (0.2) (0.3) (3.0) Nikkei 14,429.26 0.2 (0.6) (11.4) GBP 1.68 0.0 0.1 1.5 MSCI EM 993.35 (1.1) (1.8) (0.9) CHF 1.13 0.0 0.2 1.3 SHANGHAI SE Composite 2,036.52 (1.0) (2.9) (3.8) AUD 0.93 0.2 (0.6) 4.1 HANG SENG 22,223.53 (1.5) (2.4) (4.6) USD Index 79.75 (0.1) (0.1) (0.4) BSE SENSEX 22,688.07 (0.8) 0.3 7.2 RUB 36.04 0.8 1.3 9.6 Bovespa 51,399.35 (0.8) (1.4) (0.2) BRL 0.45 (1.3) (0.3) 5.4 RTS 1,119.37 (2.3) (6.7) (22.4) 186.2 155.9 141.5