1. June 2015

Chart of the Month

Gareth Lewis

CHIEF INVESTMENT OFFICER

Louie French

RESEARCH ANALYST

MARKET COMMENTARY

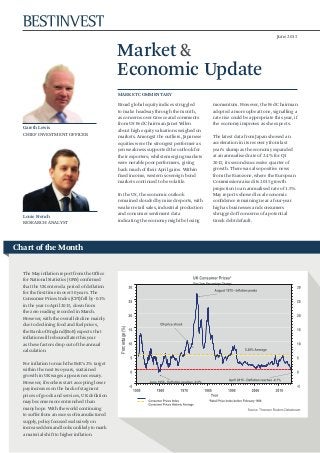

The May inflation report from the Office

for National Statistics (ONS) confirmed

that the UK entered a period of deflation

for the first time in over 50 years. The

Consumer Prices Index (CPI) fell by -0.1%

in the year to April 2015, down from

the zero reading recorded in March.

However, with the overall decline mainly

due to declining food and fuel prices,

the Bank of England (BoE) expects that

inflation will rebound later this year

as these factors drop out of the annual

calculation.

For inflation to reach the BoE’s 2% target

within the next two years, sustained

growth in UK wages appears necessary.

However, if workers start accepting lower

pay increases on the back of stagnant

prices of goods and services, UK deflation

may become more entrenched than

many hope. With the world continuing

to suffer from an excess of manufactured

supply, policy focused exclusively on

increased demand looks unlikely to mark

a material shift to higher inflation.

momentum. However, the Fed Chairman

adopted a more upbeat tone, signalling a

rate rise could be appropriate this year, if

the economy improves as she expects.

The latest data from Japan showed an

acceleration in its recovery from last

year’s slump as the economy expanded

at an annualised rate of 2.4% for Q1

2015, its second successive quarter of

growth. There was also positive news

from the Eurozone, where the European

Commission raised its 2015 growth

projection to an annualised rate of 1.5%.

May reports showed local economic

confidence remaining near a four-year

high as businesses and consumers

shrugged off concerns of a potential

Greek debt default.

Broad global equity indices struggled

to make headway through the month,

as concerns over Greece and comments

from US Fed Chairman Janet Yellen

about high equity valuations weighed on

markets. Amongst the outliers, Japanese

equities were the strongest performer as

yen weakness supported the outlook for

their exporters; whilst emerging markets

were notable poor performers, giving

back much of their April gains. Within

fixed income, western sovereign bond

markets continued to be volatile.

In the US, the economic outlook

remained clouded by mixed reports, with

weaker retail sales, industrial production

and consumer sentiment data

indicating the economy might be losing

Percentage(%)

Market &

Economic Update

2. June 2015

Our view – asset allocation summary

GENERAL SUMMARY

• Over the last seven years Central banks across the developed world have added over US$7 trillion

of additional liquidity to the global economy in an attempt to stave off the worst effects of the

banking crisis. While this stimulus has helped prevent a more severe downturn in activity, it is

clear that much of this monetary largesse has become trapped within the financial system.

• While the flow of liquidity will dwindle now the US Federal Reserve has ended its asset-purchase

programme, the pace of reduction will be mollified by the stimulative policies being pursued

within the Eurozone and Japan.

• The recent increase in bond and currency market volatility points to investor uncertainty over how

these two forces will play out.

EQUITIES

• Following the prolonged rally in prices most equity markets now look fair value relative to their

own history. The outlier is probably the US where the combination of aggressive share buybacks

and debt refinancing has driven corporate margins to historic highs.

• In contrast Eurozone equities valuations remain realistic, reflecting the more subdued levels of

economic activity. However, as ECB QE increases liquidity flows and pushes down the currency,

we would expect the region’s equity markets to benefit as investors reappraise prospects.

• Despite their strong performance last year, Japanese equities continue to look good value as rising

corporate earnings and strong investor flows sustain prices.

• We are cognisant that investment in the UK market exposes performance to commodity prices

from the large-cap mining stocks based here, but believe that much of the concern is already in

the price. The UK market also offers income in this low-growth, low-inflation environment.

• There is a performance differential between Emerging Markets and Asia Pacific, with the former

more closely correlated to commodity prices. Additionally, there is increasing dispersion between

country and region in terms of valuation and returns, with many Asia Pacific currencies pegged

to the US dollar, and competitiveness being eroded in the face of Japan and devaluation of

its currency.

FIXED INCOME

• As expected Eurozone bond markets have responded to the ECB asset purchase programme by

selling off aggressively. QE is an inherently pro-growth and pro-inflation policy which does not sit

easily with the low yields on offer across Europe during Q1.

• One worrying aspect that this has highlighted is the deteriorating conditions for all world bond

markets, with falling prices rapidly transmitting elsewhere, despite more rational valuations.

The resulting rise in yields in both the US and the UK leave Government bond markets in these

countries look realistically priced for the current uncertain economic climate.

• Emerging market hard currency debt is a concern, across sovereign, corporate and bank debt.

Many of these countries are commodity dependent, and the continued strength of the US dollar

is seen as a negative. There is a lack of liquidity in this market, which is likely to be accentuated

during risk-off periods.

• The Asset Allocation Committee reduced the weighting to fixed income by 3% in May adding the

3% to cash. High yield was reduced by 1.5% with the lack of liquidity in the high yield market a

particular concern.

COMMERCIAL

PROPERTY

• Commercial property prices remain well below their 2007 highs, and the IPD forecasts are positive.

The UK economy is relatively strong and property returns are believed to be more attractive. We

are overweight UK commercial property.

COMMODITIES • We believe the asset class remains relatively unappealing, even more so due to US dollar strength.

Market & Economic Update

2 Market & Economic Update • June 2015

3. NORTH AMERICA, UK AND WESTERN EUROPE

jobs data was positive in the month,

with the US non-farm payrolls data

showing 223,000 jobs were created

in April. The unemployment rate

was down from 5.5% to 5.4%, whilst

wages were up by only 0.1% month on

month. Retail sales were flat on the

previous month, missing expectations

of a 0.2% increase. Meanwhile the

Fed Chairman Janet Yellen adopted

a more upbeat tone, signalling in her

latest speech that a rate rise could be

appropriate this year, if the economy

improves as she expects.

• In the UK the second estimate of GDP

growth in the first quarter of 2015

disappointed, with growth confirmed

at only 0.3%, its lowest level since the

fourth quarter of 2012. The extent to

which the first quarter GDP figures

were affected by political uncertainty

is yet to be seen, but the Bank of

England did lower its UK growth

forecast in its quarterly inflation

report released in May. The BoE

estimates that full-year GDP growth

will be around 2.5%, down from the

2.9% estimated in February, and has

similarly downgraded the forecasts

for 2016 and 2017. However, in the

supporting commentary the BoE

did state that the outlook for growth

remains solid and that it expected

inflation to pick up towards the end

of the year (see chart of the month

text). Other data releases in May were

more positive on the health of the UK

economy. Firstly, the UK continued

its recent trend of strong job creation,

with the unemployment rate falling

again by 0.1% to 5.5%, whilst average

wages rose by 1.9% year on year. UK

retail sales were also up, rebounding

strongly in April and smashing

forecasts, with volumes up 1.2%

month on month and 4.7% year on

year. UK manufacturing PMI for May

remained in expansionary territory.

However, productivity growth and the

trade deficit remain a challenge for the

UK economy, as the rebalancing of the

UK economy remains a slow process.

• European economic data showed

signs of improvement as first quarter

GDP expanded by 0.4%, up 1%

from the same quarter last year. A

combination of low inflation and a

weaker euro – linked to the European

Central Bank’s quantitative easing

programme – clearly providing a boost

to the bloc’s fortunes as household

expenditure rose. Notable country

performance came from France,

which beat expectations by growing

0.6% in the first quarter. With

periphery countries such as Spain also

showing signs of improvement, the

European Commission has raised its

growth forecast for the Eurozone in

2015 to an annualised rate of 1.5%.

Flash estimates of May’s inflation data

were also up, with headline inflation

up from zero to 0.3% year on year, as

the price of food and services showed

modest increases. Core inflation,

which excludes energy, food, alcohol

and tobacco, was also up to 0.9% year

on year. However, with unemployment

in a number of countries still high

and the well reported Greek debt

crisis showing few signs of reaching a

resolution, the Eurozone bloc needs a

continued spell of economic growth.

The extent to which loose monetary

policy from the ECB will help the

underlying economies in the long run

is yet to be seen.

DEVELOPED EQUITY

MARKET VALUATIONS:

S&P 500 – PE: 20.4x, Yield: 2.1%

FTSE All Share – PE: 16.0x, Yield: 3.3%

*DataStream Total European Market –

PE: 18.0x, Yield: 3.0%

*Includes the UK.

• Developed market equities struggled

to make headway in May, with the

FTSE 100 TR returning only 0.72%

in the month. After a strong month

in April, key large-cap sectors, such

as basic materials and oil & gas,

were down in May, returning on a

total return basis -2.60% and -3.48%

respectively. UK mid and small caps

delivered stronger returns in May as

investor confidence in the UK rose

following the Conservative’s surprise

majority victory in the UK General

Election. The FTSE 250 TR was up

4.20% over the month, whilst the

FTSE Small Cap TR returned 3.20%.

• Meanwhile, in Europe the FTSE World

Europe ex UK TR index returned

1.30% in local currency terms and

-0.19% in sterling terms, highlighting

a weaker month for the euro versus

sterling. The earnings outlook for

European equities appears much

brighter, but uncertainty over Greece

continues to dampen investor

confidence. In the US the S&P 500 TR

was up 1.29% in local currency terms

and 2.0% in sterling terms in May.

• In the US, the economic outlook

remained clouded by mixed reports.

Firstly, already weak Q1 GDP data was

revised down from an annualised rate

of 0.2% to -0.7%, as a strong dollar

and unfavourable weather conditions

saw GDP growth drop dramatically

from the 2.2% recorded in the fourth

quarter of 2014. The Chicago PMI,

which is a leading economic indicator,

was also sharply down in May, falling

to 46.2 from 52.3 in April, casting

doubts over the expected rebound

of the US economy in the second

quarter of 2015. However, the latest US

Source: FactSet

Performance(%)

DEVELOPED MARKETS, PERCENTAGE GROWTH, TOTAL RETURN

FTSE 100 TR S&P 500 TR FTSE World Europe ex UK TR

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15

90

95

100

105

110

115

120

Market & Economic Update

3

4. ASIA, JAPAN AND THE EMERGING MARKETS

Source: FactSet

Performance(%)

MSCI AC Asia Pacific ex Japan TR

Topix TR

MSCI Emerging Markets TR

ASIAN & EMERGING MARKETS, PERCENTAGE GROWTH, TOTAL RETURN

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15

90

95

100

105

110

115

120

125

sterling terms. In US dollar terms,

the MSCI AC Asia Pacific ex Japan TR

index was down -2.65%, whilst the

MSCI Emerging Markets TR index

fell -3.99%. Notable poor performers

in the Emerging Markets were

the Brazilian and Russian equity

markets, which fell -11.7% and -5.7%

respectively in US dollar terms. In

Asia the Shanghai Composite index

was again one of the strongest

performers over the month rising

4.0% in US dollar terms. However,

with the MSCI still not including

domestic Chinese A shares in its

index calculations, the MSCI China

TR was down -3.69% in May following

a weaker month for Hong Kong’s

Hang Seng index and highlighting

some of the complexities of investing

in China.

• Staying in China, the People’s Bank of

China cut interest rates for the third

time in six months as its economy

continued to show signs of slowing.

The Central bank cut the benchmark

deposit and lending rates by 25bps

whilst at the same time also relaxing

some of the controls around interest

rates as part of another step towards

rate liberalisation. The news followed

softer-than-expected inflation data,

which was 1.5% year on year, and

the latest producer price index data,

which was down -4.6% year on year.

The Chinese property market also

continued to show signs of weakness,

with the average house price down

-6.1% from a year ago.

Topix PE: 19.7x, Yield: 1.6%

• Japanese equities led the way

again in May, with the Topix TR

returning 5.08% in local currency

terms and 2.05% in sterling terms.

With the Nikkei 225 index above

20,000 index points for the first

time in 15 years and the yen trading

around its ten-year low versus the

US dollar, Japanese equities have

evidently been supported by the

Bank of Japan’s asset-purchase

programme. Additionally, with a

number of Japanese pension funds

reportedly set to transfer a large

percentage of their asset allocation

from government bonds to domestic

stocks, this momentum appears set

to continue.

• On the economic front, the latest

data from Japan showed an

acceleration in its recovery from

last year’s slump as the economy

expanded at an annualised rate of

2.4% in the first quarter of 2015,

its second-successive quarter of

growth. Lower oil prices and higher

investment income have also resulted

in Japan having its largest current

account surplus in seven years at ¥2.8

trillion. The labour market continued

to tighten with the unemployment

rate falling again in April to 3.3%.

• Outside Japan, broader Asia Pacific

and Emerging Market indices had

a poor month after performing

strongly in April. The MSCI AC Asia

Pacific ex Japan TR index returned

-2.0% and the MSCI Emerging

Markets TR index returned -3.3% in

Market & Economic Update

4

Market & Economic Update

5. June 2015

Source: FactSet

BofA Merrill Lynch Global High Yield TR

BofA Merrill Lynch Sterling Corporate Bond TR

Performance(%)

FIXED INTEREST MARKETS, PERCENTAGE GROWTH

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 1594

96

98

100

102

104

106

108

• In Europe bond yields continued to

rise amid the backdrop of the ECB’s

inflationary quantitative easing

programme and the ongoing

Greek debt crisis. German 10-year

bund yields rose 18bps in May,

starting the month at 0.36% before

finishing May at 0.54%. Yields had

reached 0.73% in the middle of

the month.

FIXED INCOME

• The BofA Merrill Lynch Sterling

Corporate Bond TR and the

BofA Merrill Lynch Global High

Yield TR indices were both up

moderately in sterling terms during

May, returning 0.5% and 0.7%

respectively.

• However, May was a subdued

month for high yield returns in

local currency terms following a

relatively strong start to 2015. The

BofA Merrill Lynch Global High

Yield TR index returned 0.04% in

May and is up 2.90% year to date in

US dollar terms.

• Meanwhile, the removal of political

uncertainty following the UK

General Election was positive for

gilts in May, with the Barclays

Sterling Gilt TR index returning

0.45% over the month. UK 10-year

gilt yields ended the month roughly

where they began at around 1.86%,

but had reached 2.0% in the middle

of the month before a late rally.

• US treasuries experienced similar

movements to their European

counterparts in May, with US

10-year yields finishing the month

15bps up at 2.18%, after reaching

2.29% towards the middle of

the month.

Market & Economic Update

6. June 2015

CURRENCIES

• After a weak month in April, the US

dollar was up 0.70% versus sterling

in May, with sterling starting the

month strongly following the

Conservatives surprise election

result before weakening against the

dollar towards the end of the month

as US interest rate expectations rose.

• Meanwhile, the euro and the

Japanese yen were weak in May, with

the backdrop of their individual

quantitative easing programmes

continuing to impact currency

valuations. The euro was down

-1.47% in sterling terms and -2.16%

in US dollar terms, whilst the

Japanese yen fell -2.88% in sterling

terms and -3.57% in US dollar terms.

• Lastly, the Russian rouble was down

-1.92% against the US dollar in May,

as its rebound from a weak 2014

showed signs of slowing.

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15

85

90

95

100

105

110

Source: FactSet

Euro

Japanese yen

US dollar

Performance(%)

CURRENCY RETURNS RELATIVE TO GBP, PERCENTAGE GROWTH

Market & Economic Update

6 Market & Economic Update • June 2015

7. COMMODITIES PERFORMANCE – 1st

- 31st

MAY 2015

Index Total Return Level % Change

-12 -10 -8 -6 -4 -2 0 2 4 6

Aluminum

Nickel

Sugar

Coffee

Natural Gas

Copper

Cotton

Soybeans

Brent Crude

Corn

Bloomberg Commodity Index

S&P GSCI

Platinum

Heating Oil

Gas Oil

Crude Oil

Kansas Wheat

Wheat

Unleaded Gas

Live Cattle

Lean Hogs

Silver

Feeder Cattle

Cocoa

Gold

Zinc

Lead

COMMODITIES

S&P GSCI Industrial Metals sector,

which fell dramatically by -7.70%

after a positive month in April. The

Agriculture and Energy sub-sectors

were also down in the month, falling

-3.49% and -0.64% respectively. The

Livestock and Precious Metals sub-

sectors produced positive returns of

1.87% and 0.93% respectively.

• Unsurprisingly, the worst-performing

individual commodity indices in

May were Aluminium and Nickel,

which like a number of commodities,

have seen their prices fall as supply

continues to outweigh demand,

particularly from China.

• After leading the way in April, the

individual oil commodity indices

were down moderately in May on a

total return basis. Prices rose towards

the end of the month following news

of further reductions in the US rig

count, but with little prospect of

OPEC cutting production, prices are

unlikely to rise dramatically in the

near future without some form of

geopolitical crisis occurring.

• Overall May was a weak month for

commodity markets, with only a

relatively small number of individual

commodity indices producing

positive returns.

• The two headline indices, the

Bloomberg Commodity index and

the S&P GSCI index, had previously

produced positive returns in April.

However, both were down in May,

falling -2.70% and -2.00% respectively

in US dollar terms.

• Performances of the S&P GSCI sub-

sectors were mixed in May, with

the worst returns coming from the

Commodity monthly performance, May 2015. Indices highlighted in yellow. Data in the above table in US dollars. Source: FactSet

Market & Economic Update

7 Market & Economic Update • June 2015

8. June 2015

Source: FactSetHFRX Global Hedge Fund GBP

Performance(%)

HEDGE FUND RETURNS, TOTAL RETURN

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15

96

97

98

99

100

101

102

103

HEDGE FUNDS

• May was a relatively flat month for

the HFRX sub-indices, with returns

ranging from 0.34% to -1.01% in

sterling terms.

• The worst-performing sub-index in

the month was the HFRX Equity

Market Neutral returning -1.01% in

sterling terms.

• The best-performing sub-index in

May was the HFRX Macro/CTA, which

returned 0.34%.

• The headline index, the HFRX Global

Hedge Fund GBP, returned 0.3%

in May.

Source: FactSet

0

0.5

1

1.5

2

2.5

Performance(%)

Capital growth

Income return

Jul 14Jun 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15 Apr 15

MONTHLY IPD RETURNS*

Source: FactSet

0

0.5

1

1.5

2

2.5

Performance(%)

Capital growth

Income return

Jul 14Jun 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15 Apr 15

MONTHLY IPD RETURNS*PROPERTY

• The IPD UK Property Monthly Total

Return index increased by 0.99%

in April, compared to 1.3% in the

previous month.

• Whilst income returns remained

stable at 0.46%, capital returns were

down from 0.83% in March to 0.53%

in April.

• The Office and Industrial sectors

were once again the best performing

in April, increasing by 1.4% and 1.2%

respectively on a total return basis

over the month. The Retail sector

produced a total return of 0.6%

in April.

*Index data is released mid-month and therefore figures are only available

with a one month lag.

Market & Economic Update

8 Market & Economic Update • June 2015

10. IMPORTANT INFORMATION

The value of your investments, and the income derived from them, can go

down as well as up, and you can get back less than you originally invested.

Any indication of past performance or quoted yields is not an indicator of future

returns. Before investing in funds, please check the specific risk factors on the key

features document or refer to our risk warning notice, as some funds can be high-

risk or complex, or can be susceptible to risks particular to the geographical area or

industry sector in which they invest. Prevailing tax rates and relief are dependent on

your individual circumstances and are subject to change.

Any research or analysis contained in this document has been undertaken by us for

our own use and may be acted on in that connection. The contents of the document

are based on sources of information believed to be reliable; however, save to the extent

required by applicable law or regulations, no guarantee, warranty or representation

is given as to its accuracy or completeness. The document may include forward-looking

statements which are based on our current opinions, expectations and projections.

It is provided to you only incidentally, and should not be considered a personal

recommendation or advice to invest. Any opinions expressed are subject to change

without notice.

150615-1415

Market & Economic Update

10 Market & Economic Update • June 2015

Bestinvest (Brokers) Limited (Reg. No. 2830297) and Bestinvest (Consultants) Limited(Reg. No. 1550116)

are both registered in England and are authorised and regulated bythe Financial Conduct Authority.

Registered office: 6 Chesterfield Gardens, Mayfair, London W1J 5BQ.