Job Order Slides CMA

•Descargar como PPT, PDF•

2 recomendaciones•2,144 vistas

stages of production and flow of cost

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a Job Order Slides CMA

Similar a Job Order Slides CMA (20)

Más de Zoha Qureshi

Más de Zoha Qureshi (20)

Último

Último (20)

Job Order Slides CMA

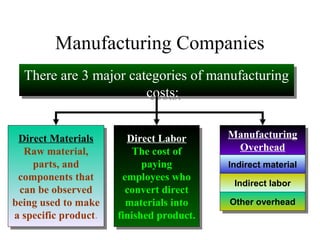

- 1. Manufacturing Companies There are 3 major categories of manufacturing costs: There are 3 major categories of manufacturing costs: Direct Materials Raw material, parts, and components that can be observed being used to make a specific product. Direct Materials Raw material, parts, and components that can be observed being used to make a specific product. Direct Labor The cost of paying employees who convert direct materials into finished product. Direct Labor The cost of paying employees who convert direct materials into finished product. Manufacturing Overhead Manufacturing Overhead Indirect materialIndirect material Indirect laborIndirect labor Other overheadOther overhead

- 2. Manufacturing Companies Prime Costs include:Prime Costs include: Direct MaterialsDirect Materials Direct LaborDirect Labor Manufacturing Overhead Manufacturing Overhead

- 3. Manufacturing Companies Conversion Costs include:Conversion Costs include: Direct MaterialsDirect Materials Direct LaborDirect Labor Manufacturing Overhead Manufacturing Overhead Nonmanufacturing Costs are all the costs not used to produce products. Nonmanufacturing Costs are all the costs not used to produce products.

- 4. Stages of Production and the Flow of Costs

- 5. Stages of Production and the Flow of Costs - Example What is EndingWhat is Ending Inventory inInventory in February?February? What is EndingWhat is Ending Inventory inInventory in February?February? Axel Electronics makes toasters. OnAxel Electronics makes toasters. On February 1, Axel has $15,000 of rawFebruary 1, Axel has $15,000 of raw material on hand. Axel’s purchasematerial on hand. Axel’s purchase and transfers to the production floorand transfers to the production floor are indicated below.are indicated below. Axel Electronics makes toasters. OnAxel Electronics makes toasters. On February 1, Axel has $15,000 of rawFebruary 1, Axel has $15,000 of raw material on hand. Axel’s purchasematerial on hand. Axel’s purchase and transfers to the production floorand transfers to the production floor are indicated below.are indicated below.

- 6. Axel Electronics makes toasters. OnAxel Electronics makes toasters. On February 1, Axel has $15,000 of rawFebruary 1, Axel has $15,000 of raw material on hand. Axel’s purchasematerial on hand. Axel’s purchase and transfers to the production floorand transfers to the production floor are indicated below.are indicated below. Axel Electronics makes toasters. OnAxel Electronics makes toasters. On February 1, Axel has $15,000 of rawFebruary 1, Axel has $15,000 of raw material on hand. Axel’s purchasematerial on hand. Axel’s purchase and transfers to the production floorand transfers to the production floor are indicated below.are indicated below. Stages of Production and the Flow of Costs - Example Now let’s look atNow let’s look at Work-in-Process.Work-in-Process. Now let’s look atNow let’s look at Work-in-Process.Work-in-Process.

- 7. Stages of Production and the Flow of Costs - Example What is theWhat is the amount of costamount of cost transferred totransferred to Finished Goods inFinished Goods in February?February? What is theWhat is the amount of costamount of cost transferred totransferred to Finished Goods inFinished Goods in February?February? On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP. On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP.

- 8. Stages of Production and the Flow of Costs - Example On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP. On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP. Now let’sNow let’s look atlook at FinishedFinished Goods.Goods. Now let’sNow let’s look atlook at FinishedFinished Goods.Goods. TransferredTransferred to Finishedto Finished GoodsGoods

- 9. Stages of Production and the Flow of Costs - Example On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February? On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February?

- 10. Stages of Production and the Flow of Costs - Example On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February? On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February?

- 11. Process Costing Job Order Costing Used for production of large, unique, high-cost items. Built to order rather than mass produced. Many costs can be directly traced to each job. Basic Cost Accounting Procedures

- 12. Typical job order cost applications: Special-order printing Building construction Also used in service industry Hospitals Law firms Basic Cost Accounting Procedures Process Costing Job Order Costing

- 13. Used for production of small, identical, low-cost items. Mass produced in automated continuous production process. Costs cannot be directly traced to each unit of product. Basic Cost Accounting Procedures Process Costing Job Order Costing

- 14. Typical process cost applications: Petrochemical refinery Paint manufacturer Paper mill Basic Cost Accounting Procedures Process Costing Job Order Costing

- 15. THE JOB Direct materials Direct labor Traced directlyto each job Traced directly to each job Manufacturing overhead (OH) Applied to each job using a predetermined rate (POHR) Job Order Costing

- 16. The primary document for tracking the costs associated with a given job is the job cost sheet. Let’s investigate Job Order Costing

- 17. The Job Cost Sheet RoseCo Job Cost Sheet Job Number A - 143 Date Initiated 3-4-X9 Date Completed Department B3 Units Completed Item Wooden cargo crate Direct Materials Direct Labor Manufacturing Overhead Req. No. Amount Ticket Hours Amount Hours Rate Amount Cost Summary Units Shipped Direct Materials Date Number Balance Direct Labor Manufacturing Overhead Total Cost Unit Cost

- 18. The Job Cost Sheet RoseCo Job Cost Sheet Job Number A - 143 Date Initiated 3-4-X9 Date Completed Department B3 Units Completed Item Wooden cargo crate Direct Materials Direct Labor Manufacturing Overhead Req. No. Amount Ticket Hours Amount Hours Rate Amount X7-6890 116$ Cost Summary Units Shipped Direct Materials 116$ Date Number Balance Direct Labor Manufacturing Overhead Total Cost Unit Cost

- 19. The Job Cost Sheet RoseCo Job Cost Sheet Job Number A - 143 Date Initiated 3-4-X9 Date Completed Department B3 Units Completed Item Wooden cargo crate Direct Materials Direct Labor Manufacturing Overhead Req. No. Amount Ticket Hours Amount Hours Rate Amount X7-6890 116$ 36 8 88$ Cost Summary Units Shipped Direct Materials 116$ Date Number Balance Direct Labor 88$ Manufacturing Overhead Total Cost Unit Cost Accumulate direct labor costs by means of a work record, such as a time ticket, for each employee.

- 20. The Job Cost Sheet RoseCo Job Cost Sheet Job Number A - 143 Date Initiated 3-4-X9 Date Completed 3-5-X9 Department B3 Units Completed 2 Item Wooden cargo crate Direct Materials Direct Labor Manufacturing Overhead Req. No. Amount Ticket Hours Amount Hours Rate Amount X7-6890 116$ 36 8 88$ 8 4$ 32$ Cost Summary Units Shipped Direct Materials 116$ Date Number Balance Direct Labor 88$ Manufacturing Overhead 32$ Total Cost 236$ Unit Cost 118$ Apply manufacturing overhead to jobs using a predetermined overhead rate (POHR) based on direct labor hours (DLH).