Recomendados

Recomendados

Más contenido relacionado

Último

Último (20)

Destacado

Destacado (20)

The Russian/CIS Fashion Retail Market

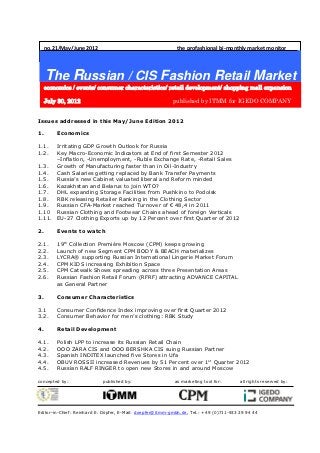

- 1. no.21/May/June 2012 the profashional bi-monthly market monitor The Russian / CIS Fashion Retail Market economics / events/ consumer characteristics/ retail development/ shopping mall expansion July 30, 2012 published by ITMM for IGEDO COMPANY Issues addressed in this May/June Edition 2012 1. Economics 1.1. Irritating GDP Growth Outlook for Russia 1.2. Key Macro-Economic Indicators at End of first Semester 2012 –Inflation, -Unemployment, -Ruble Exchange Rate, -Retail Sales 1.3. Growth of Manufacturing faster than in Oil-Industry 1.4. Cash Salaries getting replaced by Bank Transfer Payments 1.5. Russia’s new Cabinet valuated liberal and Reform minded 1.6. Kazakhstan and Belarus to join WTO? 1.7. DHL expanding Storage Facilities from Pushkino to Podolsk 1.8. RBK releasing Retailer Ranking in the Clothing Sector 1.9. Russian CFA-Market reached Turnover of € 48,4 in 2011 1.10 Russian Clothing and Footwear Chains ahead of foreign Verticals 1.11. EU-27 Clothing Exports up by 12 Percent over first Quarter of 2012 2. Events to watch 2.1. 19th Collection Première Moscow (CPM) keeps growing 2.2. Launch of new Segment CPM BODY & BEACH materializes 2.3. LYCRA® supporting Russian International Lingerie Market Forum 2.4. CPM KIDS increasing Exhibition Space 2.5. CPM Catwalk Shows spreading across three Presentation Areas 2.6. Russian Fashion Retail Forum (RFRF) attracting ADVANCE CAPITAL as General Partner 3. Consumer Characteristics 3.1 Consumer Confidence Index improving over first Quarter 2012 3.2. Consumer Behavior for men’s clothing: RBK Study 4. Retail Development 4.1. Polish LPP to increase its Russian Retail Chain 4.2. OOO ZARA CIS and OOO BERSHKA CIS suing Russian Partner 4.3. Spanish INDITEX launched five Stores in Ufa 4.4. OBUV ROSSII increased Revenues by 51 Percent over 1st Quarter 2012 4.5. Russian RALF RINGER to open new Stores in and around Moscow concepted by: published by: as marketing tool for: all rights reserved by: Editor-in-Chief: Reinhard E. Döpfer, E-Mail: doepfer@itmm-gmbh.de, Tel.: +49 (0)711-933 29 94 44

- 2. 4.6. Russian TSENROBUV expecting Credits from Sberbank and Gazprom 4.7. Russian PODIUM on the Verge of Insolvency 4.8. Russian DETSKIY MIR opening in Yaroslavl, Cheboksary and Karaganda 4.9. British PEACOCKS terminating Contract with MARATEX 4.10. Swiss PHILIPP PLEIN opened first Store in Baku 4.11. German OTTO-Group appointed new CEO for Russia 4.12. Russian GLORIA JEANS launched Stores in Makhachkala and Yaroslavl 4.13. Russian Shoe Chain OBUV.COM set for new Growth 4.14. Italian INCANTO Lingerie Retail increased Store Network 4.15. Russian ENDEA Women’s Wear growing under Franchise 4.16. Online Retailer Lamoda.ru established Infrastructure in Central Moscow 4.17. Russian INCITY building Retail Presence in Kazakhstan 4.18. German ADIDAS launches new Premium Store Format in Ekaterinburg 5. Shopping Mall Development 5.1. Moderate Growth of Street Retail Rental Fees in Moscow 5.2. BRANDCITY Outlet Center appoints Beatrice Pyubéle as CEO 5.3. New Shopping Center in Moscow to appear at Kazan Railway Station 5.4. Primorsky District of St. Petersburg to allocate new Fashion Mall 5.5. Shopping Center SOMBRERO launched in the South of Moscow 5.6. MANHATTAN MALL to appear in Kiev, Ukraine 5.7. Shopping Mall RIO opened in St. Petersburg 5.8. Construction of Shopping Center IZMAILOVO in Moscow completed End of May 2012 5.9. STOCKMANN’S NEVSKY CENTER to improve Tenant Quality 1.) Economics 1.1. Irritating GDP Growth Outlook for Russia IMF, Early July, 2012 Whereas the International Monetary Fund (IMF) raised growth forecast for Russia in April (see “The Russian Fashion Retail Market No. 20, May 29, 2012”) , the IMF has cut its forecast for Russia’s 2013 GDP growth outlook from 4 percent to 3,9 percent. But it left unchanged its 2012 economic growth rate at 4 percent. The IMF also downgraded its forecast on Russia’s budget to a surplus of 0,1 percent of GDP in 2012 from its original forecast of 0.6 percent of GDP, and to a deficit of 0,7 percent of GDP from 0,3 percent of GDP in 2013. The IMF expects Russia’s state debt to stand at 11,5 percent of GDP in 2012, compared with 8,4 percent of GDP projected in April, and at 11,3 percent of GDP in 2013 compared with the previous forecast of 7,9 percent. Russia's debt situation looks favorable compared to the other BRIC countries, where the state debt is expected at 22 percent of GDP in China, 68 percent of GDP in India and 64,2 percent of GDP in Brazil. The IMF’s forecast is above the projections of the Russian Economic Development Ministry, which in April cut its forecast for Russia’s economic growth in 2012 from 3,7 percent to 3.4 percent. In June, the Economic Development Ministry said it could possibly revise upward by fall its GDP growth forecast to 3,7-4 percent from 3,4 percent. 2

- 3. 1.2. Key Macro-Economic Indicators at the End of first Semester 2012: -Inflation, -Unemployment, -Ruble Exchange Rate, -Retail Sales Trading Economics; End of June 2012 The inflation rate in Russia was recorded at 4,3 percent in June of 2012, up from 3,6 percent in April 2012. Historically, from 1991 until 2012, the Russian inflation rate averaged 16 percent reaching an all time high of 23,33 percent in December of 1992 and a record low of 3,6 percent in April of 2012. The unemployment rate in Russia was last reported of standing at 5,4 percent in June of 2012. Historically, from 1998 till 2012, the Russian unemployment rate averaged 8,1 percent, reaching an all time high of 14,6 percent in February of 1999 and a record low of 5,4 percent in May of 2012. At the end of May 2012, fear was expressed by bankers and economic experts, that the Russian Ruble was about to enter a phase of depreciation against US $ and € at a rate of 15 percent. Reason was strong falling oil prices. However, this scenario did not come true. On the contrary, Rubel gained strength over month of June, reaching its peak on June 29, 2012 at an exchange rate against Euro of RR 41.4769. 3

- 4. Retail sales in Russia increased by 6,9 percent in June 2012 against the same month of 2011. Historically, from 2006 until 2012, Russian annual Retail Sales averaged 8,42 percent, reaching an all time high of 17,7 percent in December 2007 and a record low of – 9,8 percent in September of 2009. According to an article published by Financial Times in a mid-term outlook on Russia’s economy the trade surplus gained by high oil prices is evaporating. Throughout the decade of Putin rule, domestic consumption and imports outpaced GDP growth as Russians made up for the deprivations of Soviet life by splurging on everything from cars to fur coats and holidays. These habits have been buoyed by anti-crisis spending since 2009, when GDP fell by 8 percent amid a drop in oil prices. Budget funds earmarked for infrastructure were derivated to the state’s social safety net in an effort to prevent political unrest. Assuming oil prices of about US $ 100 a barrel the International Monetary Fund predicts that rising imports will overtake exports and Russia will show a small current account deficit in 2016. If the country cannot attract the foreign capital to finance a deficit, it will have to allow the rouble to devalue until imports fall enough to stay in balance. Ksenia Yudaeva, chief economist at Sberbank, is a believer in this scenario, predicting that once the current account surplus shrinks to 2 percent of GDP, from its current level of about 5,5 percent, the rouble will begin an orderly devaluation. That would “bring the system back into equilibrium” and head off a deficit. 1.3. Growth of Manufacturing faster than in Oil-Industry May 9, 2012; RT.com According to experts, diversification of the economy is going to be the main challenge for the new Russian Government. Retail and manufacturing are expected to become the main drivers of Russia’s economy in the near future. They agree that Russian non-commodity related industries have a great potential for growth, while the resource sector that has been pushing forward Russia’s economy for the last decade is slowing down. “Over several years since 2005, with the only exception being the crisis in 2009, the manufacturing sector has grown faster than the oil sector, which attests that the Russian economy is diversifying,” said Alexey Devyatov, Chief Economist at Uralsib in an interview with RT. “It is a kind of slow 4

- 5. process but we see it happening”. Indeed, the recent HSBC Purchasing Managers Index (PMI) report shows manufacturing in Russia is growing. April reported the best overall performance of the sector since March 2011 as the country grew to an index of 52,9 from 50.8 in March, 2012. Presidential aide Arkady Dvorkovich agrees that industries not related to oil and gas show a high growth rate. “As oil prices are still high on the global market, that’s why the share of the Russian oil and gas sector is still high and means a shelter for our diversification process”. The IT sector and retailers are showing impressive growth, according to Jeffrey Nicholson, Head of Consulting practice, at PriceWaterhouseCoopers (PwC) Russia. “I think most of the growth would come from the actions of Russian companies and not from the government,” he argued. 1.4. Cash Salaries getting replaced by Bank Transfer Payments May 16, 2012; RT.com Cash salaries may soon become a thing of the past in Russia, and all shops could be obliged to accept bank cash cards. This comes as part of an initiative to cut the amount of cash in the economy, estimated to account for US $17,5 bn. a year. Russia´s Ministry of Finance has prepared a draft regulation that obliges all companies across the country to transfer payments to their employees via bank accounts only, Vedomosti daily reports. According to the draft, cash salaries should be abandoned altogether, with a single exception made for small enterprises employing less than 35 people. A second draft regulation would bind all Russian shops to install special POS terminals allowing customers to pay by bank card. Smaller stores with annual revenues below US $64,500 are planned to get exempted from this obligation. Currently, cash settlements between Russian companies are subject to just one restriction implicating that contracts with a value of up to RR 100,000 (€ 2.500) may be settled in cash. “The share of cash accounts for 25 percent of the total money supply. In developing economies the figure stands at around 15 percent, in developed ones at about 7-10 percent,” said Russia’s Finance Minister Anton Siluanov. Such a huge amount of “live” money nourishes the shadow economy, which is estimated to account for about 30 percent of Russia’s GDP, experts say. 1.5. Russia’s new Cabinet valuated liberal and Reform minded May 22, 2012; RIA Novosti At the first meeting of his newly appointed Cabinet, new Prime Minister, Dmitriy Medvedev, said that Russia would accelerate the schedule of state property sell-offs to domestic and foreign investors, in a move likely to demonstrate the openness of the Russian economy and steer it towards better and more efficient management. The reappointment of Igor Shuvalov as first deputy prime minister in the new Cabinet to take charge of overall economic policy was also a positive signal for foreign investors. "We believe Shuvalov's appointment as First Deputy PM is a positive signal. As a major investor in Russia, we have always found our interaction with Shuvalov to be positive and constructive, and his continued role in the new government should be good news for foreign investors in the market, and for Russia as a whole," said Michael 5

- 6. Sherwood, Vice Chairman and Co-Chief Executive Officer of Goldman Sachs International. 1.6. Kazakhstan and Belarus to join WTO? June 4, 2012; RIA Novosti; June 7, 2012; RIA Novosti New-elect President of the Russian Federation, Vladimir Putin, pledged for immediate support of the European Union to accept the two members of the Customs Union, Kazakhstan and Belarus to become WTO members. He expressed htis at a press conference held after the last EU-Russia Summit, held from June 3-4 in St. Petersburg. “Concerning the Customs Union and Single Economic Space, created for Russia, Kazakhstan and Belarus, and our process of rapprochement with the European Union, we see no contradictions, because we formulated the rules of the customs union and single economic space entirely, I’d like to stress it, we prepared and signed documents entirely on the principles of the World Trade Organization. Moreover our partners Kazakhstan and Belarus took the unprecedented decision and agreed that the terms and conditions of Russia's accession to WTO would be accepted by these states,” Putin said. Right after the EU- Russia summit, Russia and Kazakhstan agreed to extend their bilateral Friendship Treaty, originally signed in 1992, for an additional 10 years. Moscow and Astana are planning to increase trade from the current US $ 24 bn to US $ 40 bn annually, over the next few years. 1.7. DHL expanding Storage-Facilities from Pushkino to Podolsk June 6, 2012; malls.ru German DHL, world leader in logistics’ services, currently operates 70.000 square meters of warehouse space in the logistics’ park of Pushkino, North of Moscow City. Due to the expansion of its business in Russia, DHL leased a further 11.600 square meters of warehouse space at MLP Podolsk, a class A warehouse complex, located in the South, 17 km from Moscow and 20 km from the second largest Russian cargo-airport Domodedovo. The total coverage of MLP Podolsk accounts for 204.00 square meters. A first tranche of warehouse space opened in 2007. The DHL transaction was implemented by CB Richard Ellis (CBRF), the Los Angeles based real estate broker and consultant. 1.8. RBK releasing Retailer Ranking in the Clothing Sector May 15, 2012; retail.ru “The Russian Market of Women’s Clothing 2012” is the title of a study compiled by RBK research. The study focuses on an assessment of retailer brand awareness of Russian female consumers in regard to women’s wear belonging to three categories of discern: “modern/contemporary”, “classic” and “quality” orientation. The ranking of “modern” women’s wear starts with H&M in first position, followed by BERSHKA, ZARA, BENETTON and CALVIN KLEIN. 50 percent of surveyed female consumers show consensus in this ranking. Further 25 percent mentioned THE THING, OLSEN, WESTLAND, and LAST NAME. Around 75 percent of respondents associate “classic” women’s wear with retailers starting with CATERINA LEMAN, WOOLLSTREET, MARKS & SPENCER, LADY & GENTLEMAN CITY and ZARINA. Ranking first as retailer of “Quality Clothing” are LACOSTE, 6

- 7. LEVI’S, ADIDAS and CALVIN KLEIN. Much less well positioned in “Quality Clothing” are chains like NEW YORKER, JENNYFER or TERRANOVA. 1.9 Russian CFA-Market reached Turnover of € 48,4 bn. in 2011 May 15, 2012; retail.ru; June 30, 2012; EFTEC According to research agency torgus.ru the retail market value of apparel reached RR 1 trillion in 2010 (€ 25 bn./US $ 33 bn.). In 2011 the research agency suggests an overall growth of 10 percent (€ 27,5 bn.). In 2010 the share of domestic apparel producers was estimated to account for 22 percent, implicating a moderate one-digit rise. This means that the share of imported apparel declined to 78 percent, with China in the lead, covering 50 percent market share. As torgus.ru further claims, the share of expenditure on apparel against total Russian expenditure on non-food products accounted for 12 % in 2010. This share is suggested of having declined to around 10 % over 2011, which is still quite higher than in Western Europe. PMR, the Krakow based research firm, projected a turnover of the total Russian Apparel, Footwear and Accessories’ Market having reached € 48,4 bn. in 2011, representing a growth against 2010 of 11,6 percent. Considering that the assessments of torgus.ru and PMR are quite close to each other, the consequence follows that an approximate € 20,9 bn was spent on footwear and accessories last year, with a suggested share of two thirds on shoes (€ 13,8 bn.) and one third on accessories (€ 7,1 bn.). 1.10 Russian Clothing and Footwear Chains ahead of foreign Verticals End of June 2012; PMR Consulting In its recently published study on the Russian Apparel, Footwear and Accessories’ s Market 2012, Polish PMR Consultancy reported, that this Russian retail sector is driven by rising demand of children’s articles and by general growth of the medium priced market segment. Concerning the Fashion Accessory Market, PMR says that this sub-segment is still far away from market saturation, in the medium price range in particular. As PMR further emphasizes, Russian clothing and footwear retail chains are gaining market share against foreign competitors with SPORTMASTER GROUP in the lead, operating more than 750 affiliated stores and an estimated revenue of € 1,15 bn. last year. The company’s portfolio consists of brands SPORTMASTER, O’STIN, SPORTLANDIA, COLUMBIA, FOOTTERRA and O’NELL. It’s former division NOMENAR controlled mono- brand store expansion for German S’OLIVER but replaced this venture by its own brand O’STIN. ADIDAS GROUP (ADIDAS, REEBOK, ROCKPORT) is second largest clothing and footwear retailer after SPORTMASTER in Russia, followed by the footwear chain CENTROBUV (CENTROBUV; CENTRO), the children’s articles department store DETSKIY MIR, MELON FASHION GROUP and Spanish INDITEX-GROUP (ZARA, BERSHKA, PULL & BEAR, MASSIMO DUTTI, OYSHO, UTERQÜE, STRADIVARIUS and ZARA HOME). Meanwhile all INDITEX brands operate in Russia controlled by brand-oriented own Russian OOO’s (LLCs), managing, white customs’ clearing, secure and quick response delivery and replenishment from the Spanish central warehouse in La Coruňa 7

- 8. 1.11. EU-27 Clothing Exports up by 12 Percent over first Quarter 2012 June 30, 2012; EFTEC In its most recent benchmark study on the development of EU apparel exports to Russia, the European Fashion and Textile Export Council (EFTEC) reported favorable results for the delivery period into the Spring/Summer Season 2012 during the first quarter of 2012 compared to the same period of 2011. Shipments of textile clothing and accessories from the Member States of EU-27 to Russia increased by 12 percent to an ex-works-/DAP value of € 833,7 mn. Related to the traditional member states of EU-15, exports rose by 11 percent to reach a value of € 703,4 mn. The balance of € 130 mn. went on the account of the new Eastern Member States, representing a growth of 17 percent. This figure includes trans-shipments of western European textile clothing, effected through Lithuania and Latvia. The three first ranking European supplier nations, Italy, Germany and France accounted significant differences in their export development. Whereas Italy managed a growth of 16 percent to € 319 mn., Germany registered an increase of 12 percent (€ 190 mn.) and France arrived at a comparatively low plus of 3 % (€ 60 mn.). The fourth ranking supplier nation, Spain, reached an equal growth of just 3 percent amounting to a shipment value of € 39 mn. Different to the rest, United Kingdom and The Netherlands registered a decline of their textile clothing exports to Russia at a rate of 5 percent for the UK (€ 32,5 nm.) and at 9 percent for The Netherlands (€ 15,2 mn.). Instead, Finland and Austria managed to increase shipments by 20 % and 10 %, respectively. 2.) Events to watch 2.1. 19th Collection Première Moscow (CPM) keeps growing End of June; IGEDO Company Exhibition space of the 19th edition of CPM will stretch across eleven pavilions of Krasnaya Presnya Expocenter, providing a gross leased area of over 54.000 square meters. Compared to the last September edition of 2011, this means an increase of exhibition space of more than 2.500 square meters. According to the organizer, IGEDO Company, Dusseldorf, next CPM will allocate over 820 exhibition stands, up by 15 percent against September 2011. Exhibitors will originate 30 countries presenting the current collections for the retail season Spring/Summer 2013 comprising women’s wear, men’s wear, children’s wear, young fashion, denim and casual wear, leather and fur clothing, evening and club wear, Lingerie, Shape wear, underwear, swim and beachwear, as well as fashion accessories. “We are closely watching our growth performance from season to season, because we have to bear in mind the overall market growth” said Philipp Kronen, Managing Partner and CEO of CPM. Last year Russian demand for men’s wear increased at 26 percent for women’s wear at 20 percent and for Intimate Apparel at 19 percent”, Kronen explained. “Growth of CPM should always be kept under the average segment growth” he concluded. 8

- 9. 2.2. Launch of new Segment CPM BODY & BEACH End of June, 2012; IGEDO Company CPM BODY & BEACH – MORE THAN LINGERIE is the title of the fourth segment addition to CPM. The new show-in-show will be launched in the centrally positioned pavilions 2/4 and 2/5 providing exhibition space for over 80 registered brands in a stylish sector-specific ambience. Among many others renowned brands like ALLESANDRO DELL’ACQUA, AMERICAN BEAUTY, GUESS, HANRO, LINGERIE LOUIS FERAUD, MARYAN BEACHWEAR, PAIN DE SUCRE, PARAH, RITRATTI, and TRIUMPH INTERNATIONAL will participate in this first event. One of the highlights of CPM BODY & BEACH is marked by launch of the first edition of “INTIMODA” Magazine published in Russian language by Milan based INTIMA GROUP, affiliated to Pisani Editore. “We are excited that IGEDO offered us the opportunity to promote INTIMODA at CPM BODY & BEACH said Francesca Spinetta, Editor-in-Chief of the new Magazine. Further highlights accompanying CPM BODY & BEACH are lingerie catwalk shows in Pavilion 8/3, the catwalk center, where TRIUMPH INTERNATIONAL will produce its own catwalk-show during the first three days of the exhibition. 2.3 LYCRA® supporting Russian International Lingerie Market Forum June 25, 2012; INTIMA GROUP/INVISTA After a period of negotiating between ITMM GmbH, INTIMA GROUP and INVISTA, manufacturers and distributors of world famous LYCRA® Elastan fibers, KOCH INDUSTRIES of Wichita, Kansas, USA, the mother-company of INVISTA, agreed to support RUSSIAN INTERNATIONAL LINGERIE MARKET FORUM, being held on the occasion of the launch of CPM BODY & BEACH on September 5, 2012. INVISTA will delegate the Global Segment Leader Lingerie, Arnauld Ruffin, to hold a key note address on the SHAPEWEAR PHENOMENON, based on a global consumer survey recently conducted by INVISTA. Giulio D’Erme, Managing Director of OOO TRIUMPH INTERNATIONAL, Moscow will act as testimonial speaker reporting on SHAPEWEAR experience of TRIUMPH in Russia. Further confirmed speakers at the Forum are Sergey Kusonski, Vice-Chairman of MILAVITSA, Marco Turano, Brand Executive of Italian INTIMISSIMI Retail Chain, among other key executives from Lingerie Trade and Industry. 2.4. CPM KIDS increasing Exhibition Space End of June; IGEDO Company CPM KIDS, the oldest special section of CPM, located in pavilion 2/3 will require a substantial extension of exhibition space. There is an ever growing demand for space from leading international brands of children’s wear” said Christian Kasch, Project Director for CPM with IGEDO. “Last year in September we had to accommodate a space increase of 89 percent to 2,072 square meters and we are now getting another 800 square meters on top”, Kasch explained. As he further admitted, he had to install a waiting list for exhibitors. According to Kasch growth of the CPM KIDS segment is a mirror of the strong retail market development in Russia with DETSKIY MIR as a trend setter. Key brands of children’s wear exhibiting at next CPM KIDS are: AGATHA RUIZ DE LA PRADA, ASTON MARTIN, BEN 9

- 10. SHERMAN KIDS, BOBOLI, CONDOR, FALKE KIDS, FERRARI JUNIOR COLLECTION, GUESS KIDS, HILFIGER KIDS, KENZO, MARC O`POLO, MISS BLUMARINE SHOES, PEPE JEANS KIDS, ROBERTO CAVALLI, SANETTA. One of the highlights of CPM KIDS is continuation of the Kid’s Wear catwalk shows which will be integrated in pavilion 2/3 with two presentations per day. 2.5. CPM Catwalk Shows spreading across three Presentation Areas End of June, 2012; IGEDO Company At the last edition of CPM in February 2012, 42 fashion catwalk shows were produced by IGEDO over four days. “It’s amazing how exhibitors keep responding positively on participation in multi-label catwalk shows, country-shows and individual mono-brand catwalks” said Christian Kasch, Project Director CPM of IGEDO. “We even get requests from brands not even participating in CPM” Kasch added. As a consequence, IGEDO is forced to build and provide catwalk-areas outside the catwalk-center in Pavilion 8/3. Apart from the separate catwalk at CPM KIDS, the organizers will construct a further separate catwalk area in pavilion 3, the new location for the segment CPM FASHION & DENIM. “We shall produce our IGEDO FASHION & DENIM multi-brand show together with company individual mono-brand catwalks”, commented Kasch. He also attested that this segment, launched in September 2011, is expanding as well from season to season. Key brands moving to pavilion 3 are: BEN SHERMAN, DESIGUAL,DIESEL, FRUIT OF THE LOOM, MAVI, NOIZE, PEPE JEANS LONDON, RED FOX and VOLCANO, among many others. 2.6. RUSSIAN FASHION RETAIL FORUM (RFRF) attracting ADVANCE CAPITAL as General Partner End of June 2012, Fashion Consulting Group/IGEDO Company The next edition of RUSSIAN FASHION RETAIL FORUM will be held from September 5 until September 7, in parallel to CPM in a co-operation partnership between IGEDO Company, MESSE DUESSELDORF, FASHION CONSULTING GROUP (FCG) and ITMM GmbH. The over-running title of RFRF is “TURBULENT MARKET – PROCESS OPTIMIZATION in Fashion Retail Merchandising. FCG was in a position to attract ADVANCE CAPITAL, a leading Russian private Investment Company to act as General Partner of RFRF. RFRF will be split in four parts, RUSSIAN – INTERNATIONAL LINGERIE MARKET FORUM on September 5, the traditional EXECUTIVE CONFERENCE followed by EXPERT SEMINAR SESSIONS on September 6 and by WORKSHOP SESSIONS on September 7, 2012. Key workshops are being prepared by ADVANCE CAPITAL, DHL Global Forwarding, DHL Global Mail and by Spanish AMICHI Clothing Retail Chain addressing Franchise Store-Partnership opportunities. 3.) Consumer Characteristics 3.1. Consumer Confidence Index improving over first Quarter 2012 End of June 2012, Federal State Statistical Office Indicators of consumer expectations of population (individual and generalized indices) are calculated on the basis of a special sample survey, 10

- 11. which is conducted by state statistical offices to study peculiarities of changes of consumer expectation of population in Russia. To determine these indices main principles of the European Commission methodology, implemented for the harmonized survey of customers, is being used. Results of the survey for the first quarter of 2012 compared to the same period of 201) reveal the following positive changes of indices: Index of changes occuring in economic situation of Russia: -3 (-12) Index of expected changes in economic situation of Russia: +4 (- 5) Index of expected changes in prices over the current year: -69 (-78) Index of expected changes in the number of unemployed: -21 (-32) Index of current personal financial situation: -12 (-15) Index of changes in personal financial situation over the past: -4 (-14) Index of expected changes in personal financial situation: -0,1 ( -8) Index of conditions favourable for major purchases: -20 (-28) Index of conditions favourable for money savings: -37 (-43) 5 0 -5 -10 balance, percentage -15 -20 -25 -30 -35 -40 quarter I II III IV I II III IV I 2010 2011 2012 Consumer confidence index Components of the generalized indicator: Assessment of changes occurred in economic situation of Russia Assessment of expected changes in economic situation of Russia for short-term perspective Assessment of changes occurred in personal financial situation Assessment of expecting changes in personal financial situation Assessment of conditions favorable for major purchases 3.2. Consumer Behavior for Men’s Clothing: RBK Study May 24, 2012; retail.ru; May 31, 2012; retailer.ru Body-fit is the main criteria for the wide majority of Russian consumers purchasing men’s wear. This is the result of a new study on the Russian Men’s Wear Market, assessed by RBK research. But it is not only body-fit but also wearing comfort, ranking first in buying decisions, followed by style/fashion content and quality of sewing and stitching, quality of fabric, co-ordination capability with other pieces of men’s wear, and mentioned last, price of the item. However, if characteristics of a specific piece of 11

- 12. men’s wear determining the selling price in a store can not get explained by the seller, Russians tend to buy cheaper. Price fairness therefore is a further shopping criterion, Russians pay attention to. If retailers discount higher priced items of men’s wear rather early in the season, the fair value criterion is put under question. Moreover, as notified in the study, the “overwhelming” majority (up to 62 %) of Russian consumers prefer to shop men’s wear from malls and shopping centers, less (< 40 %) from street retail speciality stores. These rations apply to Moscow and St. Petersburg in particular, where the supply of shopping malls is vast. As the study further attests, buying men’s wear from online-stores is a fast expanding trend now reaching provincial cities, where the offer of men’s wear in specialty stores is very limited. 4.) Retail Development 4.1. Polish LPP to increase its Russian Retail Chain May 2, 2012; russiaretail.ru LPP S.A., listed on the Warsaw stock exchange since 2001, plans to expand its clothing retail activities in Russia. The first store under LPP’s brand RESERVED was launched at MEGA TEPLIY STAN mall in 2001. At the end of 2011 the company operated 80 stores in Russia under its brands RESERVED, CROPPTOWN and HOUSE. LPP also introduced its home textile brand HOME & YOU in Russia, at present counting five such stores. The most recent launch of a RESERVED Store took place at MEGA SAMARA mall. Expansion plans are eager. At the end of 2012 LPP envisages 99 more stores to open all across the country. LPP operates three separate own distribution centers in Russia, OOO ReTrading, OOO Es Style Russia, OOO Fashion Point Russia. Last year’s Russian retail sales revenues reached US $ 96,4 mn. against US $ 75,1 mn. in 2010, representing a growth of 28 percent. 4.2. OOO ZARA CIS and OOO BERSHKA CIS sued Russian Developer May 4, 2012; retail.ru In a law case against “Gals-Invest-Development” OOO ZARA CIS and OOO BERSHKA CIS claimed compensation payment for store interiors and installation (furniture and shelving) in two stores located at the “Summer” Mall of St. Petersburg, which the developer had to committed to provide, but did not deliver. Both OOOs, belonging to Spanish INDITEX Group had advanced foreign funds to the developer to pre-finance such investment. The claim for returning the lended money plus interest accounted for RR 96,4 mn. (€ 2,41 mn./US $ 3,21 mn.). Recently, Moscow Arbitration Court decided the case against the developer as legitimate. The defendant agreed to pay a compensation amount of RR 44 m. (€ 1,1 mn./US $ 1,5 mn.) related to the claim of OOO ZARA CIS but he objected to the claim of OOO BERSHKA CIS. Earlier Moscow Arbitration Court had filed a similar law case claimed by OOO STRADIVARIUS CIS in which the court decided “Gals-Investment Development” to effect a compensation payment of RR 15,6 mn. (€ 391.000/ US $ 522.000). 12

- 13. 4.3. Spanish INDITEX launched fiver stores in Ufa May 4, 2012; retail.ru New Shopping mall JUNE in the city of Ufa attracted INDITEX Group as anchor tenant. The company opened five stores on April 27, 2012: ZARA on 2.100 square meters, PULL & BEAR on 480 square meters, OYSHO on 220 square meters, STRADIVARIUS on 320 square meters and BERSHKA on 550 square meters, which adds up to a total of 3.670 square meters. Shopping Mall June provides four floors covering a lease area of 25.000 square meters. Developer of the mall is GROUP REGIONS, a vertical conglomerate holding the fourth position in the ranking of the largest Russian owners of retail space. The company operates 27 facilities in 22 cities of Russia on a gross area of 600.000 square meters. 4.4. OBUV ROSSII increased Revenues by 51 Percent over 1st Quarter 2012 June 4, 2012; russiaretil.ru, June 14, 2012; russiaretail.ru The Russian footwear producer & retailer Obuv Rossii gained revenues of RUB 544.3m (€ 13,6 mn. / US $ 17,2 mn) in the first quarter of 2012, a growth of 51 percent year on year. Furthermore, company net profit rose during the period by 69,5 percent year on year while its EBITDA profitability reached 14,71 percent. Such results were obtained due to the company policy, focusing assortment improvement and increase of number of footwear related goods twice. As Retail Update Russia informed in March 2012, the company intends to triple its sales of accessories to RR 300m (€ 7,5 mn / US $ 10,2 mn) to reach a 10% share of overall company turnover in 2012. The accessories are offered under the company's “Emilia Estra” and “Vestfalika” private labels, and include shoe polish, insoles, antiperspirants, foot care products, stockings and socks. In 2011, Obuv Rossii generated revenue of approximately RUB 100 mn (€ 2,5 mn. / US $ 3,3 mn.) from associated sales, representing 5 percent of consolidated revenue. In addition, during the period of January-March 2012 the company network grew by nine outlets, and at the end of this period its store count included a total of 178 units including franchise stores, operating under Vestfalika and Peshekhod brands. Obuv Rossii is to invest RR 80 mn (€ 2 mn /US $2,43 mn) in restyling the format of its Vestfalika shops. The changes will involve renewing the design of the stores, as well as increasing the share of premium merchandise in their assortment of goods. The primary driver for changes is to locate more of Vestfalika stores in shopping centres. Currently, the majority of the chain's units operate in street retail. Obuv Rossii intends to balance the proportion between street-retail units and those in shopping centres at a rate 50/50 within 5-7 years. New outlets in shopping centres are planned on areas of 100-120 sq.m, and the first outlets of this kind are expected to open in August 2012. Overall, by the end of 2012, the company is to launch 10 new Vestfalika store locations in Krasnoyarsk, Novosibirsk, Tyumen and St. Petersburg. 13

- 14. 4.5. Russian RALF RINGER to open new Stores in and beyond Moscow May 4, 2012; retail.ru Shopping Center RIO in Reutov, near Moscow is a new location for the city's first brand shop RALF RINGER. The investment in this retail outlet accounted for RR 1 mn. (€ 25.000/ US $ 33.000) excluding inventory. The company plans to recover the investment in one year. The new store presents collections of shoes for men and women. The company plans opening of 5 to 6 stores in Moscow and Moscow region, until the end of this year, allocated to shopping centers, RIO (Dmitrovskoe), JUNE (Mytischi) and OUTLET VILLAGE (Belaya Dacha). Further 20 RALF RINGER branded retail stores are planned to be launched in regional cities of Russia. RALF RINGER is a purely Russian manufacturer of men's shoes. In 2010 the company introduced its first collection for women. Since its founding in 1996 the volume of production increased by 47 times from 30.000 pairs in the first season to 1 million 382 thousand pairs in 2011. Ralf Ringer belongs to the top three most recognized footwear brands in Russia. Production is located in 3 own factories in Moscow, Vladimir and Zaraisk. The retail network includes over 1,500 points of sales, including 92 stores under the own brand of RALF RINGER. 4.6. Russian TSENTROBUV expecting Credits from Sberbank and Gazprom May 11, 2012; russiaretail.com Shareholders of the Russian shoe producer and retailer TSENTROBUV are under negotiations with Sberbank and Gazprombank for credit allowances on a total sum of RR 7 bn (€ 175 mn. / US $ 233 mn). Sberbank may support the company with RUB 5bn ($165.7m), while the rest of the sum (RR 2bn ($66.3m) would be provided by Gazprom. The company's credit needs relate to recent announcements that it intends to increase its revenue by at least 35% year on year in 2012 and sell 60 million pairs of shoes against 40 million in 2011. Also, as Retail Update Russia recently reported, the company considered an IPO at foreign stock market exchanges. However, as the management announced, it does not have a specific foreign IPO plan. Nevertheless, the business continues to be reorganised to meet the necessary international IPO standards. 4.7. Russian PODIUM on the Verge of Insolvency May 12, 2012; sostav.ru/Izvestia Joint Stock Company PODIUM, Moscow, has applied to Moscow Arbitration Court for declaring insolvency of its premium multi-brand retail chain. Obvious reason is overdebt resulting from unpaid leases and unpaid fashion supplies imported by FASHION HOUSE GROUP and TRIVIAL on behalf of PODIUM. Debt accumulated to a total of RR 58 mn. (€ 1,45 mn. / US $ 1,9 mn.). The company already tried to recover its debt burden by selling street retail property on Kuznetskiy Most, Tverskaya and Bolshaya Dmitrovka, all highstreets of Moscow. A big position of debt goes on the account of lease owed to a shopping center on Kutuzov Avenue. The insolvency proceedings also include realization of vending real estate in Kazan and Samara. PODIUM opened its first store in 1994 as a multi-brand concept store for premium brands. It was one of the best stores in 14

- 15. Moscow. Experts believe that PODIUM’s latest venture, opening of its PODIUM FASHION DEPARTMENT STORE integrated in the renovated building of Hotel Moscow, was too much an investment for the company. Owners of PODIUM are Igor Krayushkin and Edward Kitsenko. 4.8. Russian DETSKIY MIR opening in Yaroslavl, Cheboksary and Karaganda May 14, 2012; retail.ru; June 4, 2012; malls.ru The by far largest Russian Children’s Good’s retailer DETSKIY MIR continues its expansion process. In May the company opened a store on 1.600 sq.m. at Shopping Centre RIO GRANDE in the city of Yaroslavl. A further large size store of 1.200 sq.m. was inaugurated at the mall CASCADE in Cheboksary. DETSKIY MIR is also strengthening its market position in Kazakhstan, where it launched its third store in the city of Karaganda, located at the popular shopping and entertainment center CITY MALL. The first Kazakh store of DETSKIY MIR appeared in December 2011 in Astana, the capital of Kazakhstan, at Shopping Center TULPAR on more than 2000 sq.m. The second one opened in Almaty at the shopping center APORT, in April 2012. To-day the chain comprises 161 stores in 78 cities of Russia and three in Kazakhstan. The coverage exceeds 316.000 square meters. 4.9. British PEACOCKS terminating Contract with MARATEX May 16, 2012; retail.ru Getting out of Russia and Ukraine is the directive of the new investor in the popular PEACOCKS lower medium priced mono-brand fashion retail chain, Scottish Edinburg Woollen Mill. In Russia PEACOCKS was distributed and master-franchised by MARATEX. Over the past seven years, this company had built 42 stores in Russia and 9 stores in Ukraine, comparing to 388 stores operated under the PEACOCKS brand in the UK market, in which the new investor sets its focus. MARATEX replaces PEACOCKS by the Italian brand OVIESSE (OVS), belonging to GRUPPO COIN, operating 589 stores in Italy. The license for MARATEX to distribute OVS is restricted to Russia. In Ukraine, the company is distributed by ARGO GROUP which opened a first OVS flagship in March 2012 in Kiev. Several of the PEACOCKS’ stores in Russia will be converted in OVS outlets. In Ukraine ARGO may take over 4 PEACOCKS’ Stores and replace these by OVS. 4.10. Swiss PHILIPP PLEIN opened first Store in Baku May 24, 2012; fashionunited.de The capital of Azerbaijan, Baku, with more than 2 million inhabitants, attracts more and more fashion designers, premium and luxury fashion brands. The city’s popularity benefited from the EUROVISION SONG CONTEST in May this year. “Baku is a mystic, special city for me with a cultural history alongside its borders of the Caspian Sea, a great hospitality of people and a very relaxed atmosphere in the down-turn pedestrian area” said Philipp Plein, when he reasoned about the launch of his first mono-brand store in Baku. “I want to develop my brand and get new cultural influence from there”, Plein added. The new store in Baku 15

- 16. presents the PHILIPP PLEIN women’s wear and men’s wear collections as well as the home collection. 4.11. German OTTO-GROUP appointed new CEO for Russia June 5, 2012; fabeau.de Martin Schierer (44), has been appointed CEO of OTTO GROUP RUSSIA on May 1, 2012. Before, Mr. Schierer acted as CEO of NADOM GROUP, a leading distance retailer which has been taken over by OTTO GROUP in 2008 out of the QUELLE bankruptcy. Mr. Schierer follows Josef Teeken who stepped out of the Russian Top Management of OTTO for personal reasons. Within 5 years OTTO GROUP RUSSIA is the by far largest distance retailer in Russia based on catalogue- and B2C online-sales with an annual revenue of € 500 million (US $ 610 mn.). Mr. Schierer’s CEO position at NaDom Group has been taken over by Natalia Loreonova (35) who served the company as Marketing Director and deputy to Mr. Schierer. 4.12. Russian GLORIA JEANS new Stores in Makhachkala and Yaroslavl June 6, 2012; shopandmall.ru GLORIA JEANS belongs to the most dynamically developing apparel retail chains in Russia, specializing on casual wear with a focus on Denim. On June 9, 2012, started a new store at OASIS shopping center in the Caucasian city of Makhachkala, on a floor space of 415 sq.m. On June 10, a further store opening took place in Yaroslavl, as a street retail venture covering 750 sq.m. positioned on Prospect Tolbukhinin,47. At the end of the first semester of this year GLORIA JEANS operates stores in 450 cities of Russia and Ukraine, comprising a total retail space of 155.000 sq.m. Until the end of next year, GLORIA JEANS plans to operate a total of 600 stores. Sales projected in 2012 should exceed RR 28 bn. (€ 700 mn. / US $ 933 mn.) 4.13. Russian Shoe Chain OBUV.COM set for new Growth June 8, 2012; shopandmall.ru The St. Petersburg based multi-brand footwear chain OBUV.COM has started operating over 60 stores all across Russia, since 2010. Until the end of this year further 60 stores are scheduled to open in shopping malls and in street retail formats of in between 150 and 300 square meters. In Spring 2012, the former owners of St. Petersburg based LENTRA Hypermarket chain, A. Meyer and D. Kostygyn, purchased 40 % of the shares of OBUV COM, representing an investment of around US $ 25 million. The average amount of investing in an OBUV COM footwear store accounts for RR 4 mn. (€ 10.000/US $ 12.500), excluding merchandise inventory. 4.14. Italian INCANTO Lingerie Retail increased Store Networks June 15, 2012; shopandmall.ru At the beginning of 2012, the Italian Retail Chain INCANTO selling lingerie, swim- and beachwear, homewear and men’s underwear, started a new store expansion campaign in Russia. Over the first five months of this year a total of 20 new shops have been opened all across Russia. On June 15, 16

- 17. INCANTO inaugurated two new affiliates at shopping center RIO and at shopping center PETERLAND, bringing the total of stores in St. Petersburg up to 14. On June 16, INCANTO launched a further store in Ufa at the new MEGA MALL. INCANTO stores usually cover a floor space in between 65 and 80 square meters 4.15. Russian ENDEA Women’s Wear growing under Franchise June 18, 2012; shopandmall.ru A new medium priced women’s wear collection was introduced to the market in 2009, the crisis year, by OOO FASHIONSTYLE, Moscow, which is designed and manufactured at the company’s own factory and by sub- contractors in the Vladimir region. FASHION STYLE set a focus on wholesale and franchising its mono-brand store concept under the label ENDEA. The first stores opened at the beginning of 2012 in the city of Arkhangelsk at PYRAMID MALL and in the city of Voronezh at the shopping center ARENA, comprising floor spaces of up to 100 sq.m. Main customers are found in regional cities with a population of around 200.000, stretching from Kaliningrad in the west to Yuzhno-Kurilsk in the Far-East. Over the next five years the company plans to open 60 shops under franchise with partners. Further openings are planned this year in Tyumen, Barnaul, Irkutsk, Kursk and Orenburg. The business concept of ENDEA is very different to sector traditions. The collection for the retail season A/W 2012/13 was put on pre-order sales promotion at the end of June 2012, for delivery in September, similar to the pronto-moda concept. This is possible because ENDEA can count on its local production together with flexibility reserves provided by small sub-contractors located around the factory. 4.16. Online Retailer Lamoda.Ru established Infrastructure in Moscow June 27, 2012; malls.ru According to CB Richard Ellis (CBRE), the online retailer www.lamoda.ru selling footwear, clothing and accessories, leased a 1.200 square meter infrastructure to accommodate offices and warehouse at 4th Avenue Roshinsky, 20, near the metro station “Tula”. The total commercial real estate in which lamoda.ru has now found its headquarters comprises 8.400 sq.m. and was constructed by ALM Development. This online retailer started off in Russia under the name of Kupishoes.ru but added soon the lamoda.ru appendix to get better introduction to clothing suppliers. Behind lamoda.ru stands the German ZALANDO e-commerce platform, one of the leading online shops for footwear and fashion. Lamoda.ru has no relation to moda.ru/fashion.ru the Russian Internet Communication platform owned and managed by Anton Alfer. 4.17. Russian INCITY building Retail Presence in Kazakhstan June 27, 2012; malls.ru FASHION CONTINENT a leading Russian multi-brand apparel retail chain keeps on developing its own brand fashion stores under the name of INCITY across the Russian border to the Republic of Kazakhstan. In June, two new INCITY stores opened at APORT MALL in Almaty on 434 sq.m. as well as in the shopping center ASIA PARK in Astana on 350 sq.m. Last year 17

- 18. franchise partners opened INCITY STORES in Almaty, Astana, Karaganda, Aktube and Atyrau. Another store launch is planned in Astana by the end of this year. In 2013 further INCITY Stores are scheduled for implementation in Almaty, Karaganda and Temirtau. 4.18. German ADIDAS launches a new Premium Store Format in Ekaterinburg June 28, 2012; russiaretail.ru German sports- and footwear retailer ADIDAS is to open a new-format store in the RADUGA PARK shopping mall in Ekaterinburg. Specifically, the new store will offer a broadened range of ADIDAS premium brands, including “Adidas Performance” and “Originals”, as well as “Adidas Style by Porsche Design” and “Adidas Neo”. The new store is to operate on an area exceeding 780 sq.m. The new format's concept is based on separating display areas within the store, where separate Adidas collections (sub- brands) are offered. ADIDAS plans to open the new store-format in other large Russian cities, aimed at clients with a relatively high income. 5.) Shopping Mall Development 5.1. Moderate Growth of Street Retail Rental Fees in Moscow June 4, 2012; malls.ru According to a study on street retail conducted by RRG real estate brokerage, availability of street retail facilities in Moscow, status of end of April 2012, accounted for 183 objects covering 70.000 square meters. 25 objects were located within the Garden Ring (“Sadovoe Kolco”) and 158 outside this ring road. The availability corresponds with the March survey. The average rental fee for objects inside the garden ring rose by 3 percent to US $ 15.661 per square meter per year. Outside the garden ring lease rates dropped by 2 percent to US $ 8.046 per square meter per year. 5.2. BRANDCITY Outlet Center appoints Beatrice Pyubèle as CEO June 4, 2012; shopandmall.ru The shopping center WAYMART, which was constructed in 2002 alongside IKEA’s MEGA TEPLIY STAN, is being converted into a factory outlet center on a gross lease area of 30.000 square meters until the end of 2013. It will be named BRANDCITY. End of May 2012 the developer, VALUE RETAIL GROUP appointed French-Canadian Beatrice Pyubèle as CEO to administrate the conversation from a shopping mall to an outlet center. Some of the tenants of WAYMART will adopt their store presence to the new concept. The minimum lease at BRANDCITY goes from US $ 400 to US $ 1.000 per square meter per year. If an outlet store reaches a revenue subject to negotiation, the lease terms change to a percentage of turnover from 8 to 15 percent. The changing of WAYMART to BRANDCITY is coming at a moment when three other outlet centers are getting in operation: BELAYA DACHA OUTLET VILLAGE (July 2012), VNUKOVO OUTLET VILLAGE (Q3, 2012) and FASHION HOUSE MOSCOW (Q4, 2012), all located beyond the Moscow Ring Road belt. BRANDCITY expects an advantage against its competitors because the location is based right on 18

- 19. the ring road in close vicinity to IKEA BELAYA DACHA and CROCUS’s VEGAS MALL both attracting up to 300.000 consumers per month. 5.3. New Shopping Center in Moscow to appear at Kazan Railway Station June 7, 2012; malls.ru A unique shopping center is expected to open at the end of the third quarter of 2012 at Kazan Railway Station in Moscow. Consulted by RRG real estate, this investment of RR 150 mn. (€ 3,75 mn / US $ 5 mn.) comes out of the state owned Russian Railway (RR), providing a total of 3.370 square meters of retail space. One of the first tenants to sign a lease contract was German ADIDAS, which booked 780 square meters on a five year agreement. Kazan Railway Station has a frequency of 90.000 people per day, adding up to 3 million per month. RR plans further shopping centers of this kind at Leningrad and Yaroslavl railway and bus stations. 5.4. Primorsky District of St. Petersburg to allocate new Shopping Mall June 13, 2012; shopandmall.ru A new retail and entertainment center is under development in the center of Primorsky District of St. Petersburg on a rentable area of 65.000 sq.m., near the Metro Station “Pioneer”. The object is due to open in the fourth quarter of 2014. JonesLangLaSalle has been appointed as lease agent. The new shopping mall is setting a focus on fashion, sporting goods (1.500 sq.m.) and children’s goods (2.000 sq.m). 5.5. Shopping Center SOMBRERO launched in the South of Moscow June 15, 2012; malls.ru On June 15, the technical opening of shopping center SOMBRERO took place in the Southern District of Moscow at the interaction of highways to Warsaw and Yangel. The four level center provides a gross lease area of 17.000 sq.m. Official Inauguration was on June 18, 2012. Tenants are Ile de Beaute, O’stin, Gloria Jeans, Henderson, Incity and a children’s goods supermarket. 5.6. MANHATTAN MALL to appear in Kiev, Ukraine June 15, 2012; malls.ru The infrastructure of shopping centers in the capital of Ukraine keeps growing. FORUM EVALUTION, a local commercial real estate developer appointed UTG as exclusive marketing agent and broker for a new mall, providing a gross lease area for retail of 67.800 square meters under the name of MANHATTAN MALL. The object will be linked with the subway station “Vydubychi”. Among the anchor tenants is a department store on 2.300 sq.m. According to experts it will take two years to open MANHATTAN MALL at the end of the third quarter of 2014. 19

- 20. 5.7. Shopping Mall RIO opened in St. Petersburg June 15, 2012; malls.ru TASHIR GROUP, a Russian commercial real estate developer opened its fourteenth shopping center under the name of RIO in St. Petersburg. Located in the Frunze District of the city on Ulitza Fuchik, the complex covers a ground space of 70.000 sq.m. from which more than half is reserved for retail. Anchor tenants are H&M, C&A, MOTHER CARE and DETSKIY MIR. Fashion stores presently operating include polish LPP Group (RESERVED, CROPPTOWN, MOHITO, HOUSE), L’ETOILE cosmetics, O’STIN, GLORIA JEANS, KIDSGARDEN, SNOW QUEEN, INCITY, LEE-WRANGLER, CENTRO footwear and RENDEZ-VOUZ, among others. 5.8. Construction of Shopping Center IZMAILOVO in Moscow completed End of May 2012 June 21, 2012; malls.ru The new Shopping Center IZMAILOVO is part of the high-end “businessclass” residential complex, developed under the same name by DON-STROY-INVEST at 4th Street Park in Moscow. Lease area for retail comprises 12.250 sq.m. positioned on two floors. Anchor tenant is MOTHERCARE on 600 square meters. Most of the tenants from the clothing and footwear sector are Russian mono-brand retail chains, known for dynamic expansion. 5.9. STOCKMANN’S NEVSKY CENTER to improve Tenant Quality June 27, 2012; RBC Daily/malls.ru NEVSKIY CENTER, owned by Finish STOCKMANN, a unique combination between Department Store and mono-brand upmarket fashion and lifestyle stores and boutiques needs a clean-out. First objective is to increase the store shopping mall from 80 tenants by 10-12 percent. Second objective is to improve the quality and the exposure of tenants. COLLIERS INTERNATIONAL has been appointed by STOCKMANN to conduct the upgrading process. STOCKMANN is happy with just 60 percent of its tenants to which belong LONGCHAMP, PANDORA, RAYBAN, TOMMY HILFIGER, NAPAPIJRI, among others. Expected newcomers are GERARD DAREL, PINKO, CACHAREL. STOCKMANN’S NEVSKIY CENTER was opened in late 2011. Obviously, in order to cover the space for rent, tenants were accepted not meeting the upper-medium-to-premium standard, originally planned. It is quite unusual that after 8 months of operation, the upgrading campaign is implemented. Experts believe that it will take a couple of years to reach the standard STOCKMANN wants to achieve. Düsseldorf, Moscow, Stuttgart July 30, 2012 Editor-in-Chief : Reinhard E. Döpfer Tel.: +49-711-933 2994-44; Fax: +49-711-933 2994-50 E-mail: doepfer@itmm-gmbh.de Publisher: IGEDO Company, Duesseldorf Contact: Ingrid Kahlfuss Tel.: +49-(0)-211-4396-302 E-Mail: kahlfuss@igedo.com 20