Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (12)

Similar a L1 flashcards portfolio management (ss12)

Similar a L1 flashcards portfolio management (ss12) (20)

Más de analystbuddy

Más de analystbuddy (16)

Último

Último (20)

L1 flashcards portfolio management (ss12)

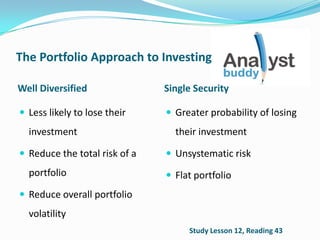

- 1. The Portfolio Approach to Investing Well Diversified Single Security Less likely to lose their investment Reduce the total risk of a portfolio Reduce overall portfolio volatility Greater probability of losing their investment Unsystematic risk Flat portfolio Study Lesson 12, Reading 43

- 2. Types of Investors Individual Investors Short-term goals of individual investors can be children’s education expenses, or lumpy purchases Long term goals can be retirement plans paid such as a defined benefit contribution plan. Under a defined benefit contribution plan, the employee receives a fixed cash pension payment at the time of retirement Study Lesson 12, Reading 43

- 3. Types of Investors Institutional Investors Includes commercial banks, investment banks, insurance companies, asset management companies, etc. Endowment funds by universities Banks invest in excess financial reserves Study Lesson 12, Reading 43

- 4. The Portfolio Management Process An Investment Policy Statement maps out an investors needs and restrictions. It is designed to allow investment advisors to make investment recommendations which suit that particular investor’s objectives. Study Lesson 12, Reading 43

- 5. Stages in Developing an Investment Policy Statement Step 1: Planning. Understanding the client’s goals and preparing the IPS. Step 2: Execution. Deciding the asset allocation, undertaking security analysis, and portfolio construction. Step 3: Feedback. Monitoring and rebalancing of portfolio, measurement, and reporting performance. Study Lesson 12, Reading 43

- 6. Mutual Funds It is a pool of investment capital from individuals and institutions that is managed by a fund manager. Two types of mutual funds: open-end and closed-end Open-end funds: when new investors invest by investing capital with asset managers at the latest net asset value. Closed-end funds: when new investors can only gain exposure to the fund by purchasing existing shares in the fund from another investor. Mutual funds exist for investments in money markets, bonds, stocks, and balanced funds. Study Lesson 12, Reading 43

- 7. Mutual Funds Money Market Funds: Investments in high-quality, short term, corporate or government debt. Bond Funds: Invest in all types of rated debt from low to high quality debt and does not have a maturity restriction. Stock Market Funds: Invest in a portfolio of equity securities. Can be either Active or Passive Balanced Funds: Invest in a portfolio across a range of asset classes and securities. Study Lesson 12, Reading 43

- 8. Measures of Investment Returns: Calculating Returns The Holding Period Return of an investment in a single security is calculated as: Where: D is the dividend, P is the price, t-1 is the date of the initial investment, and t is the date the investment is exited or the measurement end date. Study Lesson 12, Reading 44

- 9. Measures of Investment Returns: Calculating Returns The HPR of an investment over three years can be calculated as: Study Lesson 12, Reading 44

- 10. Measures of Investment Returns: Money Weighted Return The money weighted return weights the returns achieved by each asset in a portfolio by the weight of capital invested in each security. The formula is identical to the IRR formula: Study Lesson 12, Reading 44

- 11. Measures of Investment Returns: Annualizing Returns Investors can annualize return measures using the following formula: In the formula above, c is the number of periods in the investment horizon. For example, if quarterly returns are being annualized, c=4. Study Lesson 12, Reading 44

- 12. Measures of Investment Returns: Returns of a Portfolio The return of a portfolio can be calculated by weighting returns generated by the portfolio: Where w is the weight, R is the return, and i represents a single security in the portfolio. Study Lesson 12, Reading 43

- 13. Measures of Investment Returns: Arithmetic vs. Geometric Returns The arithmetic average of investment returns is simply the mean of the returns over a number of periods. The geometric average returns need to be calculated over a sequential period of investment. For example, assume the returns on an investment portfolio over 5 periods were 90%, 10%, 20%, 30% and -90%. Using the geometric average returns formula ([(1.9 x 1.1 x 1.2 x 1.3 x 0.1) ^ 1/5] – 1), the geometric return can be calculated as -20.1%. Study Lesson 12, Reading 43

- 14. Characteristics of Major Asset Classes Equities: Investing in equities or stocks is an investment in a security representing an ownership interest in a business. Fixed Income: Fixed Income securities provide a return in the form of fixed periodic payments (coupons) and the eventual return of principal at maturity. Cash and Cash Equivalents: Assets such as cash or those that can be converted into cash immediately Study Lesson 12, Reading 44

- 15. Geometric Mean Return Average of returns over a number of period. The geometric mean return can be calculated as: where is the return of period ‘t’ , and T is the total number of periods. Gross return is the returns calculated before any deduction of expenses is made and Net Return is what the investor eventually earns after all the expenses are accounted for. Study Lesson 12, Reading 44

- 16. Variance of a Portfolio Variance is an indicator of the historical riskiness of returns of a various asset. High variance in historic returns signals a high risk investment. where R is return over period ‘t’, and T is the total number of periods, while is average of T returns, supposing T represents the population of returns. Study Lesson 12, Reading 44

- 17. Variance of a Portfolio If a sample is provided, then the following formula is used to calculate the sample variance: The Standard Deviation of an asset’s returns is square root of the variance. Study Lesson 12, Reading 44

- 18. Variance of a Portfolio The variance of portfolio can be calculated using the following formula: Covariance measures the tendency for returns of two assets to move in the same direction at the same time. It is calculated using the following formula: Study Lesson 12, Reading 44

- 19. Risks Aversion and Its Implications For Portfolio Selection Risk aversion is the willingness of an investor to accept risk in the pursuit of higher returns. Risk-Seeking investors Risk-Neutral investors Risk-Averse investors Risk tolerance is the opposite of risk aversion. Study Lesson 12, Reading 44

- 20. Risks Aversion and Its Implications For Portfolio Selection Each investor has a Utility Function which helps investment advisors select investments which maximise the investor’s utility. The Utility Function is calculated as: U = utility of one investment E(r) = expected return = investment’s variance A =risk aversion measure of an investor Study Lesson 12, Reading 44

- 21. Risks Aversion and Its Implications For Portfolio Selection The following chart highlights the different indifference curves for different types of investors: Study Lesson 12, Reading 44

- 22. Return of a Portfolio The return of a portfolio can be calculated as the weighted average of the returns of each asset which makes up the portfolio. It can be calculated as: Study Lesson 12, Reading 44

- 23. Risk of a Portfolio The risk of a portfolio can be measured by the variance and standard deviation of returns. The variance of returns of a portfolio can be calculated as: The standard deviation of a two asset portfolio can be calculated as: Study Lesson 12, Reading 44

- 24. Covariance and Correlation In order to calculate the variance and standard deviation of a multi-asset portfolio, we need to consider the covariance of returns between the assets. The covariance of returns can be calculated as: Cov (R1, R2) = p12σ1σ2 Where p12 is correlation of R1, R2; p12 =+1: The returns of two assets are exactly the same through; p12 = -1: The returns of two assets are exactly inverse of each other through time; p12 = 0: The returns of two assets are not related to each other. Study Lesson 12, Reading 43

- 25. Risk and Return of a Portfolio with >2 Assets The return of a multiple asset portfolio can be calculated as: Assuming all assets have an equal variance and equal correlation, the equation above can be restated Study Lesson 12, Reading 43

- 26. Impact of Portfolio Risk of Investing in Less Than Perfectly Correlated Assets An investor can reduce the total risk of a portfolio by combining assets in a portfolio which have a correlation of returns <1. This is the key driver of the benefits of Diversification. How Diversification Benefits are Achieved The lower the correlation between the assets, the greater the diversification benefits. Study Lesson 12, Reading 43

- 27. Minimum-Variance and Efficient Frontiers of Risky Assets and the Global Minimum-Variance Portfolio Study Lesson 12, Reading 44

- 28. Minimum-Variance and Efficient Frontiers of Risky Assets and the Global Minimum-Variance Portfolio The leftmost point on the minimum-variance frontier is known as the global minimum-variance portfolio. This is the portfolio of risky assets with the lowest possible risk (ie standard deviation). The Markowitz Efficient Frontier is the minimum-variance portfolio at all points above the Global Minimum Variance Portfolio. As an investor moves along the Markowitz Efficient Frontier, the return for each unit of risk decreases. Study Lesson 12, Reading 44

- 29. Optimal Portfolio of Risk-Free and Risky Assets Study Lesson 12, Reading 44

- 30. Optimal Portfolio of Risk-Free and Risky Assets A risk-free asset lies on the Y-axis. An investor can combine the risk free asset with a portfolio of risky assets, in order to reach a satisfactory risk/return trade off. All points on the efficient frontier can be grouped with the risk-free asset to highlight the potential portfolio combinations. In the following chart, CAL (P) dominates CAL (A) given it has a higher return for a given level of risk. Investors risk preferences can be illustrated by the use of indifference curves. Study Lesson 12, Reading 44

- 31. The Capital Allocation Line Study Lesson 12, Reading 45

- 32. The Capital Allocation Line The Capital Allocation Line (CAL) graphs the potential risk and return portfolios that an investor can achieve by combining a portfolio of risky and risk-free assets. The CAL can also be known as the "reward-to-variability ratio". The Optimum Risky Portfolio falls at the intersection of an indifference curve and the capital allocation line Study Lesson 12, Reading 45

- 33. Implications of Combining a Risk- Free Asset With a Portfolio of Risky Assets The Capital Asset Pricing Model can be used to predict the expected return of an optimised risky portfolio. While different investor’s have different risk preferences, the CAPM assumes homogeneity of expectations Study Lesson 12, Reading 45

- 34. The Capital Market Line The Market Portfolio contains all available risky assets that have a value attached to them and are tradeable. A Capital Allocation Line (CAL) maps of potential risk and return profiles of portfolios which combine a risk-free asset and a risky portfolio. The Capital Market Line (CML) is a special case of a Capital Allocation Line (CAL) where the risky asset is the market portfolio. Study Lesson 12, Reading 45

- 35. The Capital Market Line Study Lesson 12, Reading 45

- 36. Systematic vs. Non-Systematic Risk Systematic risk is the market risk that an investor assumes by investing in risky assets. It is driven by fluctuations in economic conditions etc. Non-systematic risk is specific to an industry or asset class. Total Risk = Systematic Risk + Non-Systematic Risk Study Lesson 12, Reading 45

- 37. No Additional Return For Bearing Non-Systematic Risk Given that systematic risk is diversifiable, investors are not rewarded for bearing this type of risk. This suggests that investors are better off investing in a fully diversified portfolio in order to maximize the risk/return trade off. Study Lesson 12, Reading 45

- 38. Return Generating Models The quality of the estimated returns depends solely on the quality of inputs and how robust the prediction model is. Multi-factor models estimate returns by attributing returns to more than one risk factor. One type of multifactor model is a macroeconomic model which estimates returns by considering a range of economic factors. “Fama and French models” multifactor models typically contain 3 or 4 factors that contribute to returns. Single-index model only uses one factor. Study Lesson 12, Reading 45

- 39. The Market Model The market model is an example of a single factor model. The market model can be expressed as: Study Lesson 12, Reading 45

- 40. Beta Calculating and Interpreting Beta Beta measures the sensitivity of an asset to fluctuations in the market. Variances and correlation used in the calculation of beta are estimates from historic returns. An asset with a positive beta suggests that returns of the underlying asset tend to move in the same direction as the market. A negative beta suggests that returns generated by the asset tend to be inverse to returns achieved by the market, leading to low systematic risk. Study Lesson 12, Reading 45

- 41. Beta Calculating and Interpreting Beta A single-index model also known as the Capital Asset Pricing Model (CAPM) can be used to calculate beta: The market model can also be used to estimate beta (by rearranging the following formula): Study Lesson 12, Reading 45

- 42. Capital Asset Pricing Model Assumptions: Investors are risk averse, that they know balance of risk-return trade off. Frictionless markets are markets with no transactional costs or taxes, hence borrowing and lending happens at risk-free rate. Single period planning by investors is where an investor makes an investment for a single period. The homogenous belief of investors is that every investor has the same method to analyse. Investments are divisible infinitely. Price taking investors are investors who do not dictate pricing, thus trading does not affect pricing of the underlined asset. Study Lesson 12, Reading 45

- 43. The Security Market Line A graphical representation of the CAPM where the expected return is plotted on the y-axis and the beta is plotted on x-axis. Study Lesson 12, Reading 45

- 44. Application of the CAPM The risk and hence expected return of an investment opportunity can be calculated using the CAPM. The CAPM can be used to estimate the appropriate discount or hurdle rate to be used in capital budgeting . Study Lesson 12, Reading 45

- 45. The Sharpe Ratio and Treynor Ratios Indicators of risk adjusted returns based on the CAPM. Sharpe Ratio: Treynor Ratio: Study Lesson 12, Reading 45

- 46. The M2 Ratio The M2 is an extension of the Sharpe ratio. It suggests that a portfolio that outperforms the market on a risk adjusted basis will have a positive M2 and a negative M2 if it underperforms. The M2 can be calculated as: Study Lesson 12, Reading 45

- 47. The Information Ratio Measures portfolio returns above the returns of a benchmark, relative to the volatility of those returns. Measures a portfolio manager's ability to generate excess returns relative to a benchmark, but also attempts to identify the consistency of the relative performance. The Information Ratio can be calculated as: A large information ratio suggests that the investor is able to generate positive risk adjusted returns. Study Lesson 12, Reading 45

- 48. The Information Ratio Measures portfolio returns above the returns of a benchmark, relative to the volatility of those returns. Measures a portfolio manager's ability to generate excess returns relative to a benchmark, but also attempts to identify the consistency of the relative performance. The Information Ratio can be calculated as: A large information ratio suggests that the investor is able to generate positive risk adjusted returns. Study Lesson 12, Reading 45

- 49. Investment Policy Statement The key objective of the Investment Policy Statement (IPS) is to outline the investor’s objectives, and willingness/ability to take risk. The IPS of an investor must be reviewed on a regular basis. The objectives of the investor need to be explained in terms of both risks and rewards. For each client, the IPS should be well defined, and all constraints regarding liquidity, taxation, time period, regulatory and other unique needs should be addressed. Study Lesson 12, Reading 46

- 50. Major Components of IPS Introduction Statement of Purpose. Statement of Responsibilities Procedures Investment objectives Investment Constraints. Investment Guidelines Evaluation and review Appendices Study Lesson 12, Reading 46

- 51. Risk and Return Objectives Risk tolerance should be stated in the Investment Policy Statement. Risk objective should be stated whether they are fixed, variable, or a mixture of both. The return objective defines how much an investor wants to earn. The return objective should be realistic, and return expectations should be managed considering the investor’s risk profile. Study Lesson 12, Reading 46

- 52. An Investor’s Financial Risk Tolerance: Willingness Vs. Ability To Take Risk Risk bearing ability can be broken down into three major components: Time range Expected cash flows The ratio of wealth to liabilities. Study Lesson 12, Reading 46

- 53. Investment Constraints The Investment Policy Statement (IPS) of an investor should consider its investment constraints. There are 5 baskets of financial constraints: Liquidity Time Horizon Taxation Legal & Regulator Unique Circumstances Study Lesson 12, Reading 46

- 54. Strategic Asset Allocation Investors can strategically alter the weight of the investment portfolio across different asset classes in order to benefit from the returns of asset classes at different points of the economic cycle. Study Lesson 12, Reading 46

- 55. Asset Classes Traditional asset classes include: Bonds Equities Cash Real estate Alternative asset classes include: Commodities Hedge funds Private equity. Study Lesson 12, Reading 46

- 56. How Strategic Asset Allocation or Investment Policy Statement Translates into an Actual Portfolio An investor considers long-term capital market expectations and its Investment Policy Statement (IPS) to form its Strategic Asset Allocation. When investors choose between assets with similar expected return profiles, they tend to select the least risky asset. If assets with similar risk profiles are presented, investors choose the asset with the highest return. Study Lesson 12, Reading 46

- 57. How Strategic Asset Allocation or Investment Policy Statement Translates into an Actual Portfolio The following formula calculates the expected utility of an investor’s portfolio as the expected returns of the portfolio, adjusted for the portfolio’s risk levels and risk aversion. = Expected utility of investor portfolio = Portfolio’s expected return = Portfolio return’s standard deviation = The risk aversion of investor is measured by . Study Lesson 12, Reading 46