State of Center City 2013 Press Briefing - Part Two

•

0 recomendaciones•271 vistas

Part two of Center City District President and CEO Paul Levy's press briefing for the State of Center City, 2013 report. It's Center City Philadelphia’s “annual report” that looks at all aspects of the downtown economy and makes recommendations to enhance its attractiveness and competitiveness. Download or order a copy at http://centercityphila.org/socc/

Recomendados

Más contenido relacionado

Similar a State of Center City 2013 Press Briefing - Part Two

Similar a State of Center City 2013 Press Briefing - Part Two (20)

Último

Último (20)

State of Center City 2013 Press Briefing - Part Two

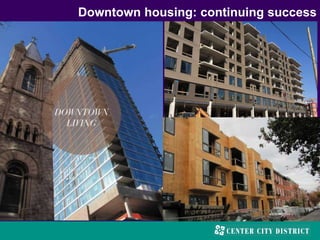

- 1. Downtown housing: continuing success

- 2. Continuing rebound from impact of recession Following dramatic drop in new condos since 2008 355 new units in 2011; 536 new units 2012 Steady production of rental units, increase in single family

- 3. Of the 3,871 condo units within CCD, 95% sold; The overhang of supply almost gone

- 4. In core developers shifted entirely to rental

- 5. That trend has continued

- 6. Rents have risen or held constant CORE CENTER CITY ONE-BEDROOM APARTMENT RENT

- 7. Rents have risen or held constant CORE CENTER CITY TWO-BEDROOM APARTMENT RENT

- 8. In extended neighborhoods of Center City townhouses continue to infill & reshape communities

- 9. Significant difference in geographic distribution September 2012 report

- 10. Center City: Girard Avenue to Tasker Street

- 11. Since 1997 added 13,409 new units of housing

- 12. Story in the core: 1998–2012: 171 buildings converted to residential use New construction starting in 2000

- 13. Central Business District is no longer just an office district 49 condo buildings with 3,871 units inside CCD 165 apartment buildings: 15,630 units 25,000 – 30,000

- 14. Significant volumes of returning empty nesters & they have driven up housing prices

- 15. Average residential sale price: 2 x citywide

- 16. Core substantially more expensive than extended

- 17. Younger home-buyers are moving outward

- 18. Queen Village

- 19. Bella Vista

- 21. Spring Garden & Fairmount

- 22. Passyunk Avenue

- 24. 2011 to 2012: 11% increase # sales in core 18% increase in # sales extended neighborhoods 12.5% increase in prices in the core 4.4% increase in extended

- 25. 2011 to 2012: Decrease in days on market 22.2% decrease in core 4% decrease in extended; velocity 20% greater

- 26. Long term appreciation in home values

- 27. All driven by steady increase in population to 175,000

- 28. Desire & economics of living close to work Well over 40% work downtown; 11% in University City 69% overall work in the city

- 29. The ability to get to work without a car 75% get to work 62% get to work without car without car

- 30. Changes in energy costs & cultural values working in our favor; significant percent want mixed-use, transit oriented & walkable places; bike ridership up 10.5%

- 31. Proximity to arts, entertainment, retail & restaurants

- 32. Values of sustainability & locally sourced food 14 Farmers’ markets + Reading Terminal & Italian Markets

- 33. Remain racially/ethnically diverse neighborhoods

- 34. 74% in core have at least a BA degree; 42% in extended

- 35. 42% have professional degrees 20% in extended

- 36. These are the well-educated workers that employers want But 22% downtown jobs held by those with no more than HS diploma

- 37. Educational levels closely tied to rising incomes

- 38. Center City has more than twice the national average of residents ages 25-34 (28.7%)

- 39. Big opportunity: 22,419 children were born to Greater Center City parents from 2000 to 2012

- 40. Greatest signs of change

- 41. Core dominated by single person households & families without children; 19% of households in extended neighborhoods now have school-age children

- 42. Expanded schools website to serve these families E

- 43. Redesigned with more information for parents www.KidsInCenterCity.com

- 45. Kids activities at cultural institutions; child friendly restaurants& summer camps

- 46. Families with children are influencing our priorities

- 47. Took a barren and forgotten space

- 48. Transformed it into magnet for families with children

- 50. Evolving role of CCD: from stage hands to place managers

- 51. Remain focused on the basics: 75% of budget: clean, safe & attractive

- 52. High-visibility deployment: 77% see CCD personnel “most or every time” they are downtown 3,282 respondents to customer satisfaction survey

- 53. 67% of survey respondents Say Center City “much cleaner” than rest of the city

- 54. Long-term partnership with police

- 55. Foot & bicycle patrol

- 57. Serious crimes per day from 20.2 to 10.6 Even as population and volume of people gone up

- 58. 78% feel safe “most of the time” or “always” Perception of safety

- 59. 1996: Streetscape Improvements • 761 trees; 100 planters

- 60. Visitor- friendly: 683 pedestrian maps & signs

- 61. Integrated with 233 signs for motorist that the CCD also maintains

- 62. Making Transit More Customer Friendly

- 63. Route maps and historic images On all 90 transit shelters

- 64. New graphics for 108 entrances to underground

- 65. 1 2,179 Pedestrian-scale lights Doubled nighttime illumination .

- 66. Completed 2/3 of all streets in last decade 124 new fixtures in 2012;

- 67. Most recently added 3 blocks in Chinatown

- 68. Maintained façade lighting on South Broad Street

- 69. 2012: 3,556 banners for 70 non-profit groups

- 70. Continue to make streetscape improvements throughout Center City; $14.3 million in 2012

- 71. 87% rate the overall atmosphere of Center City “good to excellent”

- 72. $30.8 million in CCD funding leveraged $52.1 million Federal, state, municipal, foundation & private since 1997

- 73. Taken on larger, more complex capital projects Broader range of customers

- 74. More components

- 75. More services

- 76. More moving parts to maintain & manage

- 77. Collins Park at 1707 Chestnut Street

- 78. Managing a quiet gathering place: 44 concerts; 24 days of Farmers Markets

- 79. Expanding into place marketing

- 80. Programming in the evenings

- 81. And in the winter months

- 83. A new civic space at Dilworth plaza

- 84. We’ve been underground for a while Reconstructing concourse & making platforms accessible

- 85. But the shape of the new plaza is coming into view

- 86. All steps & barriers are gone

- 87. One level: no steps from street & no depressed areas

- 88. Two transit entrances frame City Hall Gateway to regional transit

- 89. Covered glass stairways to the concourse

- 90. Enhancing one of our competitive strengths

- 91. Lawn panel & tree grove on the southern end

- 92. New green living room for the city

- 94. Fountain on the north Lawn

- 95. 3 foot high programmed jets

- 96. Setting for a major new installation of public art

- 98. Café at the northern end Lawn

- 99. New outdoor cafe

- 100. Visible from Convention Center; views up Parkway

- 103. Center stage for the city Completed summer 2014

- 104. Investing in quality public spaces pays dividends Attracting workers & residents Raising value of adjacent real estate

- 105. State of Center City has never been better

- 106. But our success is uneven

- 107. We weathered the recession but are now lagging in growth

- 108. Set the goal of adding 50,000 to 100,000 jobs citywide by 2023

- 109. Decrease dependence on wage & BIRT Get wage tax below 3%; cut Net income in half 2013 2023 64% 57.2%

- 110. What does a more competitive tax structure create?

- 111. Opportunity for start-up & minority firms to grow

- 112. State of Center City 2023: a tale of significant growth