Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (20)

Similar a Critical Illness Presentation

Similar a Critical Illness Presentation (20)

Critical Illness Presentation

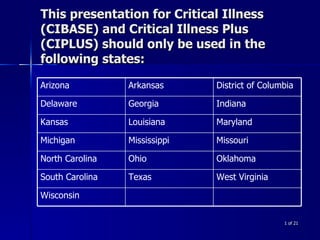

- 1. This presentation for Critical Illness (CIBASE) and Critical Illness Plus (CIPLUS) should only be used in the following states: of 21 Arizona Arkansas District of Columbia Delaware Georgia Indiana Kansas Louisiana Maryland Michigan Mississippi Missouri North Carolina Ohio Oklahoma South Carolina Texas West Virginia Wisconsin

- 2. The Western and Southern Life Insurance Company Cincinnati, Ohio of 21 Policy series numbers 0907-80, 0907-80-U It’s all about Survival! FA-722-A 0806

- 3. Life Expectancy of 21 Sources: National Association for Critical Illness Insurance “ Health, United States, 2007”, pp 50, Centers for Disease Control & Prevention 75 80 46 48 Average Life Expectancy 1900 – 47 years old 2002 – 77 years old MALE FEMALE 1900 2002 MALE FEMALE Avg. Age of Critical Illness Claimants 43 years old Today, we are living 30+ years longer

- 4. The Longer A Person Lives… of 21 The greater the chance of being diagnosed with a critical illness “ Heart Disease and Stroke Statistics: 2008 Update,” American Heart Association

- 7. Many Survivors Experience… of 21 “ Financial Hardship” because of the indirect costs associated with their illness

- 9. Can You Afford To Say… of 21 “ It won’t happen to me?”

- 18. of 21 Critical Illness Insurance Is….. Not about death, it’s about survival!

- 20. of 21 How Much Do You Need? If diagnosed with a critical illness… You will likely need 12 to 18 months of your gross monthly income to meet the cost of your indirect expenses. Source: “Heart Disease and Stroke Statistics: 2008 Update,” American Heart Association

- 21. What Is The Cost Of This Benefit? of 21

Notas del editor

- A critical illness, such as a heart attack, stroke or cancer, can be a hardship to most families. This kind of hardship is not so much by the actual illness, but by the indirect costs associated with it. My goal is to help you develop a plan to meet the needs of your family should a critical illness occur. This plan will help protect your quality of life and enable you to meet the costs that can occur with such an illness.

- Medical advances have led to increased life expectancy. The average life expectancy in 1900 was 47 years. By 2002, it had increased to 77 years. And it continues to rise.

- <no notes>

- The fact that Americans are living longer, along with the stress of modern life, has led to an increase in cancer, heart attacks and stroke.

- In the past, these illnesses were often fatal. Today, however, an increasing number of people survive. We are living through the physical challenges of our illnesses. But, what about the financial challenges?

- <no notes>

- Who do you know who has been diagnosed with cancer, had a heart attack or stroke? [ Probe for specific situations! This screen is vital because it connects the problems of critical illness to the prospect’s present situation. Help the prospect understand the possibility of a critical illness.]

- Can you afford not to take action?

- Survival has a price. Insurance is a way to pay for that price. Insurance is a way to control risk by sharing your risk with others. If you had a heart attack, cancer, or stroke and could not work, how would you pay your bills? your mortgage? [Talk about prospect’s current situation.]

- Most people are shocked to see that 2/3 of the costs associated with cancer are indirect. Indirect costs including modifications to your home, alternative treatments and home health care needs, usually are not covered by your health insurance.

- Let’s look at this list, how would each of these impact your family? [Spend time on each point.]

- Western & Southern Life’s Critical Illness insurance policy will pay you 100% of the maximum benefit amount in a lump-sum upon the diagnosis of life threatening cancer, heart attack, stroke, end stage renal failure, and major organ transplant. I think now is a good time to note something important. We are not talking about health insurance here; Critical Illness insurance is a different animal so it’s important to know that you still need to have health insurance.

- [Present the solution.] So you’ve indicated that you have a need. Western & Southern Life has a solution. Our Critical Illness plan can help you provide for the indirect expenses associated with an illness. This plan will help protect the quality of life and standard of living you’ve worked so hard to provide for yourself and your family.

- Most people ask, “What if I never have a critical illness?” Western & Southern Life assures you that even if you do not experience a covered illness, 100 percent of premiums paid, minus any claims paid, will be paid to your beneficiary at time of death. [Note: ADB rider premiums are not included in this calculation.]

- This is the real beauty of Critical Illness: it’s a “living benefit” that provides real choices. As a policyholder, you receive a lump sum benefit upon diagnosis. You can use your money for anything you choose -- even a once-in-a-lifetime vacation with loved ones. Actual alternatives available will depend on the amount of the benefit paid and the cost of the option.

- [Continue to emphasize the choices and flexibility that Critical Illness insurance provides.]

- Critical Illness insurance was not created by an insurance company, a sales person or a mathematician. It was created by a doctor who saw the need for it first hand. Dr. Marius Barnard who assisted his brother Dr. Christian Barnard in performing the first human heart transplant created the product in connection with an insurance company in South Africa (2008 Critical Illness Insurance Conference, LOMA). Dr. Barnard recognized that his patients were surviving their illnesses only to be destroyed financially. You are going to survive! You need the living benefit!

- Critical Illness Insurance provides a missing piece of your financial plan. [Close the sale by reiterating the real value that Critical Illness insurance provides.] PLEASE READ THE FOLLOWING DISLCOSURE TO THE CLIENT THIS POLICY IS A LIMITED BENEFIT HEALTH POLICY. It contains limitations, exceptions, terms for keeping the policy in force, and may contain a reduction of benefits, depending on the policy purchased. Product availability, benefits provided, coverage, exclusions and limitations vary by state. Complete details of the coverage available in your state will be explained by your sales representative or is available upon request from the company.

- Studies indicate you’ll need at least a year of income to cover the expenses of a Critical Illness. [This is where you help the prospect estimate the need. However, use the numbers the prospect feels comfortable with!]

- [Now move to your illustrations software.] We can use the Benefit Amount to calculate the premium required, or we can start with Premium Amount to calculate the Benefit Amount that can be purchased. I will key in these variables and amounts will appear -- with and without the Accidental Death Benefit rider. The Accidental Death Benefit rider is optional and provides for payment of the benefit amount should you die accidentally. This rider may not be available in all states. I need to point out that there is a 50 percent benefit reduction at age 65 [ five years after issue for those issued at ages above 60] with the Critical Illness policy. If you want to maintain a level benefit amount throughout the life of the policy you should consider the Critical Illness Plus policy.