1. The Need For Power In Texas

Natural Gas Fundamentals And Reliance On Gas-Fired …That Is Further Complicated By Rapidly Growing Demand

Generation Have Placed Texas’ Power Supply At Risk… And An Aging Generation Fleet

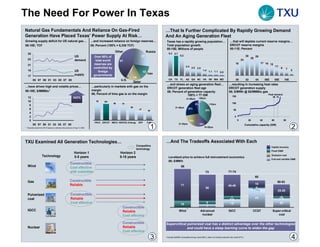

Growing supply deficit for US natural gas… …and increased reliance on foreign reserves… Texas has a rapidly growing population… …that will deplete current reserve margins…

95-10E; TCF 05; Percent (100% = 6,338 TCF) Total population growth ERCOT reserve margins

00-15E; Millions of people 00-11E; Percent

Other Russia

25 6.3 5.7

US Over 80% of 27 5.2 30 29

23 Over 80% of 26

demand total world 41 23

total world

reserves are 16 17 16 15

21 reserves are 2.4 11

controlled by

controlled by 2.0 2.0 9 7

19 US foreign 1.4

1.1 1.1 0.9

5

foreign 15

supply Iran

17 governments

governments 3 14

95 97 99 01 03 05 07 09 U.S. CA TX FL AZ GA NC VA NV WA MD 00 02 04 06E 08E 10E

Qatar

…and stress an aging generation fleet… …resulting in increasing heat rates

…have driven high and volatile prices… …particularly in markets with gas on the ERCOT generation fleet age ERCOT generation supply

95-10E; $/MMBtu1 margin 06; Percent of generation capacity 06; $/MWh @ $8/MMBtu gas

06; Percent of time gas is on the margin 100% = 77 GW Peak demand

150 06 10

12 343%

343% 41-50yrs >50yrs

10 92 90+ 2%

80 79 6% <10yrs 100

8

58 31-40yrs

6 47 22%

40 35% 50

4

2 0

0 19% 0 20 40 60 80

FRCC ERCOT WECC NEPOOL Entergy SPP PJM

95 97 99 01 03 05 07 09 21-30yrs 16% Cumulative capacity (GW)

1 Projected prices from 06-10 based on calendar strip prices as of Aug 31, 2006 1 10-20yrs 2

TXU Examined All Generation Technologies… …And The Tradeoffs Associated With Each

Competitive Capital recovery

technology

Fixed O&M

Horizon 1 Horizon 2

Technology Emission cost

0-5 years 5-15 years Levelized price to achieve full reinvestment economics

Fuel and variable O&M

06; $/MWh

Constructible

Wind Cost effective 86

with subsidies 73 71-74

60

Gas Constructible 50-53

Reliable 71 15

45-48

58 2

0.2 25-28

Pulverized Constructible

7 43 4

coal Reliable 0.6 1.0

Cost effective 15

8 18 20

Constructible 7

1

IGCC Reliable Wind Advanced IGCC CCGT Super-critical

Cost effective nuclear coal

Constructible Supercritical pulverized coal has a distinct advantage over the other technologies

Supercritical pulverized coal has a distinct advantage over the other technologies

Nuclear Reliable and could have a steep learning curve to widen the gap

and could have a steep learning curve to widen the gap

Cost effective

3 1Includes $3/MWh renewable energy credit (REC); does not include production tax credit (PTC)

4

2. The Need For Power In Texas

TXU’s Plan Will Help Meet These Challenges In Texas TXU’s Program Will Help Ensure Reliability And Reduce

Reliance On Natural Gas In Texas…

Historical and projected ERCOT Generation capacity by fuel type

Ensuring reliability and reducing reliance of natural gas reserve margins 06-10E; Percent

through a plan to bring on 9 GW of new capacity by 2010, 00-11E; Percent

1 rebalancing the Texas supply stack and helping to maintain

40

Impact of TXU Power 100%= 1,070 GW 77 GW 90 GW

adequate reserve margins through 2014 Generation Program

30

30 29

26 35 42

23 Other 58

19

Lowering prices by leveraging a scale power generation 20 16 17 16 17

2 program to displace high cost generation and share savings

with our customers

15

11 12

12

10 3 12 65

Gas 58

42

9 7 5

0

Improving the environment through the largest ever 00 03 06E 09E US Texas 06E Texas 10E

3 voluntary offset program and displacement of less efficient

generation capacity

2000 – 2004

2000 – 2004

22 GW of natural gas fired

22 GW of natural gas fired

generation added;

generation added;

2005 – 2007

2005 – 2007

Rapid

Rapid

demand

demand

2008 – 2011+

2008 – 2011+

Dangerously

Dangerously

low supplies

low supplies

Reduction in gas

Reduction in gas

reliance and

reliance and

volatility by shifting

volatility by shifting

adequate supplies growth require 1.5 GW the stack away from

adequate supplies growth require 1.5 GW the stack away from

eliminates

eliminates per year

per year gas towards solid

gas towards solid

reserve fuel

reserve fuel

5 Source: ERCOT, 10/1/05 and 6/19/06

6

…Allowing TXU To Deliver Lower Cost Power To Its …While Continuing To Improve The Texas Environment

Customers…

Breakeven power prices for TXU’s Power Generation Program Total annual ERCOT market

Estimated key emissions

SO2 NOX Hg

06E; $/MWh savings Thousands of tons

Forward power price 11E; $ billions 2005 emissions (nine existing facilities) 273.1 42.1 .0025

76-79 17

1.7

Emissions after new development and

218.5 33.7 .0020

5 4

voluntary reductions

50-53 Total TXU reductions 54.6 8.4 .0005

Reduction relative to 05 TXU emissions (20%) (20%) (20%)

Additional reductions from displacement of 3rd

0.0 12.1 0.0

party units

US ranking1 among 20 largest coal generators 1st 1st 2nd

Market savings TXU emissions rates1 relative to US average (63%) (82%) (30%)

Expectations Decreased Decreased Operational TXU

for subscale capital costs fuel costs advantages target

builder

TXU has committed to the largest voluntary emissions reduction in U.S. history

TXU has committed to the largest voluntary emissions reduction in U.S. history

Without scale, it would be virtually impossible for TXU TXU’s plan will more than double its capacity in Texas while cutting key

TXU’s plan will more than double its capacity in Texas while cutting key

Without scale, it would be virtually impossible for TXU

to deliver needed cost savings to its customers emissions by 20% and its emission rates by 70%

emissions by 20% and its emission rates by 70%

to deliver needed cost savings to its customers

7 1 TXU after new power generation development program and retrofits; relative to average US coal plant

8

3. Coal Is The Fuel Of Choice

While TXU Believes A Portfolio Of Technologies Is Needed To …Today, Supercritical Coal Appears To Have The Economic

Meet America’s Energy Challenges… Advantage

Horizon 1 Horizon 2

Capital recovery

Technology 0-5 years 5-15 years

Fixed O&M

Levelized price to achieve full reinvestment economics

Constructible 06; $/MWh Emission cost

Wind Fuel and variable O&M

Cost effective 86

with subsidies

73 71-74

Gas Constructible 60

Reliable

50-53

71 15

45-48

SCPC Constructible 58 2

Reliable 0.2 25-28

Cost effective

7 43 4

Constructible 0.6 1.0

IGCC Reliable 8 18 20

Capacity additions Cost effective 15

7

represent 12% of 06-20 1

US demand growth Constructible Wind Advanced IGCC CCGT Supercritical coal

Nuclear Reliable nuclear

Cost effective

Technology GW Technology GW

TXU aspiration: Wind 1.5 Wind 3.0 Supercritical pulverized coal has a distinct advantage over the other technologies

Supercritical pulverized coal has a distinct advantage over the other technologies

balanced portfolio of

SCPC 23.0 SCPC 30.0 and could have a steep learning curve to widen the gap

and could have a steep learning curve to widen the gap

IGCC 0.0 IGCC 6.0

state of the art Nuclear 2.5 Nuclear 8.0

generation 1Includes

1 2

$3/MWh renewable energy credit (REC); Does not include production tax credit (PTC)

Total 27.0 Total 47.0

While The Characteristics Of Wind Generation Make It …Wind Must Be Part Of The Solution

Difficult To Meet Long-Term Baseload Demand…

TXU plans to double its wind …furthering Texas as the nation’s

portfolio by 2010… leader in wind generation capacity

Wind availability versus hourly electricity demand in ERCOT

06; Percent TXU wind generation purchases Total wind generation capacity

05-10E; MW 06; MW

100 146%

146%

80 1,425 2,370 2,325

Hourly 1,260

1,100

At peak demand demand 930

60 periods wind

averages less than

40 20% capacity 580

Wind 825 800

capacity

20

0

1 5 9 13 17 21

06E 07E 08E 09E 10E TX CA IA MN

Hours

Not only does wind peak in the off-peak hours, it peaks in the shoulder months

Not only does wind peak in the off-peak hours, it peaks in the shoulder months TXU is the largest purchaser of wind generation in Texas

TXU is the largest purchaser of wind generation in Texas

Source: AWEA Second Quarter Market Report, July

3 Source: AWEA Second Quarter Market Report, July

4

4. Coal Is The Fuel Of Choice

There Must Be Regulatory And Capital Breakthroughs To …As Well As Solutions For Long-Term Storage Of Spent Fuel

Make Nuclear Generation Competitive In The Long Term… Escalating costs with expectations of …and concerns about storage capacity have made

additional increases…. nuclear capacity additions uncertain

Estimated construction cost for the Estimated U.S. used nuclear fuel accumulation

High construction costs… …combined with long …result in a high total Yucca Mountain Project 00-50E; Thousands of tons of heavy metal (tHM)

lead times… cost relative to coal 86-00; $ billion1

200

MIT “global

76% growth”

Construction costs Installation time Breakeven power price 76% Nuclear

scenario

06E; $/KW 127% 06E; Months 167% 06E; $/MWh 43% growth

127% 167% 43% 60 150 scenario

Yucca Mountain

2,500 120 70-73 73 capacity according to

DOE 01 study (83,800

20 100 tHM)

34

1,100 45 CO21 50-53

50 Yucca Mountain

legal capacity

(63,000 tHM)

SCPC coal Nuclear SCPC coal Nuclear SCPC coal Nuclear

0

86 00 00 05 15 25 35 45

The lack of a long-term spent fuel solution also makes

The lack of a long-term spent fuel solution also makes

nuclear a longer-term generation solution

nuclear a longer-term generation solution A solution for spent fuel must be defined before nuclear can be a long-term

A solution for spent fuel must be defined before nuclear can be a long-term

solution for America

solution for America

5 6

1 Based on potential carbon scenario with current European ETS pricing 1 02 dollars

Today, IGCC Is Uncompetitive With The Supercritical Coal Gas Fundamentals And Improvements In Supercritical Coal

Technology Make It The Winning Economic Technology Today

Coal is a relatively low cost fuel source… …in abundant supply in the US

Breakeven power price of SCPC and IGCC in Texas Commodity prices US reserves

06; $/MWh 99-06; $/MMBtu 04; Years of remaining reserves

12 191%

200 1,900%

1,900%

3 2 71-74

13 4 1 9 Natural Gas

50-53 1 6

1

3

Coal 29%

0 10

Sep- Sep- Sep- Sep- Sep- Sep- Sep- Sep-

99 00 01 02 03 04 05 06 Gas Coal

TXU PC Lower Lower Higher Lower Longer Longer Higher IGCC

reference emissions heat rate capital capacity ramp up time to operating estimate

Coal technology has become more cost …and emissions have been reduced

plant cost cost factor time build cost effective… dramatically

PC ref plant Per TXU

9,130

$1,100/KW 94% None 38 months $42/KW/yr Improvements in construction cost NOX emissions from US power plants

MMBtu/ 95-05; Percent reduction 05; Lbs/MMBtu

estimate nominal (online 01/10)

MWh

IGCC baseline Per TXU 8,520 $1,800/KW 85% 6 Months 62 months $56/KW/yr

estimate MMBtu/ nominal (online 01/12) 45 85%

MWh 104% 0.33

85%

104%

22

IGCC is unproven on coal available in Texas

IGCC is unproven on coal available in Texas

Longer construction time makes it difficult to hedge output

Longer construction time makes it difficult to hedge output 0.03-0.13

0.05

Cost of carbon capture is not necessarily advantaged

Cost of carbon capture is not necessarily advantaged

US average TXU new Gas

Source: GE; EPRI, academic literature; press reports

7 Gas Coal coal coal 8

5. Coal Is The Fuel Of Choice

TXU Is Investing In The Newest Technology… …To Ensure The Plants Are Part Of The Environmental

Solution

SO2

Building the most efficient plants in the country… …designed for potential future carbon capture Average emission rates

Coal plant steam outlet temperatures for plants NOX

under construction

70-15E; Lbs/MMBtu

06E; Degrees Fahrenheit 4.37

Meet EPRI IEA requirements to be

1,085 1,085 advanced considered carbon capture TXU

supercritical ready status

standard

Sufficient space in critical

access locations

>90%

>90%

1,050 1,050 1,050 Options for CO2 storage

1.08

0.78

Design studies on potential 0.29 0.35 0.29

separation methodologies 0.12 0.12 ~0.2 ~0.1 0.10 0.05

TXU Plant Plant Plant Plant Pre-investments including

US Avg US Avg Texas CAIR Oak Grove, Reference

plant siting

reference A B C D 1970 2004 2004 2015 Sandow 5 plants

plant

TXU is commercializing the most efficient coal plants and continues to ensure

TXU is commercializing the most efficient coal plants and continues to ensure TXU’s new plants will operate with the best available control technology,

TXU’s new plants will operate with the best available control technology,

the plants will be able to be retrofitted with carbon capture technology

the plants will be able to be retrofitted with carbon capture technology reinforcing Texas’ proven environmental track record

reinforcing Texas’ proven environmental track record

9 Source: EPA Acid Rain database and EIA 10

TXU Is Proactively Investing In Next Generation Technologies As In Europe, TXU Believes These Advances Will Continue To

Make Coal The Winning Technology

TXU is investing across technologies… …while working to commercialize

Horizon 1 Horizon 2 technologies across the entire value chain…

0-5 years 5-15 years Generation Demand Levelized breakeven power cost European announced new

Wind $/MWh build capacity

11+; Percent (100%=54 GW)

Gas Fuel

Combustion

Efficiency

Flue gas Customer IGCC Other

Gasification removal initiatives

Advanced coal 100 Wind Coal

• Coal • Waste to • R&D • Solid CO2 • Time of

Wind 5

cleaning energy partnership capture use retail

IGCC • Oxy- • Chilled products

firing NH3 • CO2 free 80 Nuclear

• MEA products 40

• Storage • Efficiency 33

Nuclear study solutions

60

…acquiring the lowest-cost carbon offsets …and starting an environmental ventures CCGT @

across the world economy… fund to spur investment in this area SCPC 6.50/MMBtu

40 5 4

06; $/ton Nuclear 13

TXU 0 5 10 15 20 25 30 35 IGCC

120 Transport Natural

Methane efficiency CO2 credit, $/ton

90 capture

gas

Bank $200M

Industrial

No-till

Advisory

60 gas fund Board

farming Equipment

capture It would take a combination of low gas prices and high sustained carbon prices to

It would take a combination of low gas prices and high sustained carbon prices to

30 supplier make the winning technology a non-coal technology

make the winning technology a non-coal technology

0 Venture

0 1 2 3 4 5 6 7 8 capital This gap will continue to widen as the coal construction learning curve is exploited

This gap will continue to widen as the coal construction learning curve is exploited

CO2 reductions (Billion tons) 11 12

6. TXU Development: Solving America’s

Energy Challenges

TXU Power Development Is Focused On Developing A TXU Announced 9.1 GW of New Coal Capacity To Meet The

Pipeline Of Origination Opportunities Future Power Needs Of Texas

To become the

Net

leading originator Capacity

Mission and constructor of

Unit MW Fuel County

baseload generation

throughout the US Oak Grove 1, 2 1,634 Lignite Robertson

Valley

Monticello Sandow 5 581 Lignite Milam

Morgan Creek Martin Lake

Big Brown Big Brown 3 858 PRB Freestone

Tradinghouse

Originate long-term

Develop steady Construct baseload Lake Creek Oak Grove Monticello 4 858 PRB Titus

off-take agreements

pipeline of baseload generation 35% Sandow

and equity sell Martin Lake 4 858 PRB Rusk

Objectives opportunities to add cheaper and faster

downs to ensure 30%

3 GW of new capacity and make 5% annual

of construction is Morgan Creek 7 858 PRB Mitchell

annually improvement

sold forward

Tradinghouse 3, 4 1,716 PRB McLennan

PJM Development Proprietary Construction Muni/Co-op Solutions

Program Whole System Approach Lake Creek 3 858 PRB McLennan

Industrial Solutions

Incumbent Customer Advantaged Relationships

Equity Partnership Valley 4 858 PRB Fannin

Solutions Strategy With Top Contractors and

Solutions

Manufacturers

Strategies Industrial Partnerships

National Advocacy

Global Low-cost Country, TXU is using its current, advantaged sites to expand capacity in ERCOT

TXU is using its current, advantaged sites to expand capacity in ERCOT

Scaled Sourcing Program

Initiative

Learning Curve Codification

1 2

TXU Has Focused Its Near-Term Ex-ERCOT Growth On The TXU Is Also Working With Regulated Entities To Deliver New

Deregulated PJM and Northeast Markets Generation At Lower All-In Costs

Northeast coal investment return analysis Status of PJM development

TXU’s current origination efforts include up to …to provide potential customers with long-

06; IRR effort 10 GW of new generation… term, low-cost power

Breakeven power prices for TXU’s Power

Generation Program

Completed Outstanding

06E; $/MWh

Status Units GW 4 76-79

Target entry zones 5

3 GW of sites Final fuel plan 17

identified/secured Key Preliminary discussions 5 4

Preliminary stakeholder

transmission agreements 50-53

studies complete completed by

Advanced discussions 4 3.5

Site engineering end of 2006

complete Geo-technical Letters of intent1 3 2.5

Preliminary air evaluation

modeling complete Definitive agreements 0 0

Permit levels

identified and Total 12 10

discussed with

states TXU Increased Increased Operational Regulated

High

target capital fuel costs disadvan- cost

costs tages expecta-

tions

Low TXU has had more than 10 unsolicited requests for development projects in

TXU has had more than 10 unsolicited requests for development projects in

regulated markets

regulated markets

1 Letter of intent signed or in approval process.

3 4

7. TXU Development: Meeting America’s

Energy Challenges

Improving New Build Construction Performance Could …Potentially Opening Additional Markets For New Coal

Enable Displacement Of Existing, Inefficient Generation… Plant Developments…

US 7X24 power prices Designing a business

07E; $/MWh model for advanced coal

to compete in markets

Generation reinvestment economic comparison (PV/I = 1.3)

with coal on the margin

06; $/MWh

71-74 SOx

SOx

73

emissions

emissions

60 7 cost

cost

8 19 56

Variable ~50

cost 7

40-43 43 7X24

43 21 10

Fixed 19 53

prices

58

45-48 4 High

cost 4 15

2 28

Capital 23-26 7

15 17-20

recovery 8 3 5

CCGT Nuclear IGCC Advanced Advanced Nuclear Old CCGT Old un-

($6.50/ coal – TXU coal – (existing) ($6.50/ scrubbed

MMBtu reference potential next MMBtu coal

gas price) plant target1 wave gas price) plants

reference

plant2

Low

If TXU could lower capital costs by ~30% and/or improve heat rate by 7%, TXU’s

If TXU could lower capital costs by ~30% and/or improve heat rate by 7%, TXU’s

next wave of coal plants could displace both gas and old coal plants

next wave of coal plants could displace both gas and old coal plants Coal-on-coal competition represents a 78 GW market opportunity in the US

Coal-on-coal competition represents a 78 GW market opportunity in the US

1 $1,100/KW cost to build, 9.13 MMBtu/MWh heat rate

2 $800/KW cost to build, 8.5 MMBtu/MWh heat rate

5 6

…By Creating An Opportunity To Replace Existing Coal TXU Believes That Tougher Environmental Standards…

With New Efficient Advanced Coal

US coal fleet heat rates US coal fleet ages TXU is redefining environmental standards …and CO2 emissions over the long-term

06; Percent of US coal generation capacity 06; Percent of US coal generation capacity for regulated emissions...

CO2 emissions rate

100% = 313 GW 100% = 313 GW

20E; Tons/MWh

>12 HR 0.96 0.54

>50yrs

8-9 HR 41-50yrs <10yrs 0.80

4% 2% For every incremental 1 ton of

11-12 HR 8% 10-20yrs For every incremental 1 ton of

16% 1%

9% emissions of SO2, ,NOX, ,and Hg

emissions of SO NO and Hg

22% 2 X

from new generation, existing 0.42

34% from new generation, existing

9-10 HR emissions in Texas must be

emissions in Texas must be

reduced by 1.2 tons

reduced by 1.2 tons

34% 32%

Peaking Coal Reduction Long-term

38%

31-40yrs

10-11 HR 21-30yrs gas today levers vision -

(11 HR) CCGT

Almost 60% of generation capacity is more than 30 years old and has a heat

Almost 60% of generation capacity is more than 30 years old and has a heat TXU is working across the power value chain to commercialize

TXU is working across the power value chain to commercialize

rate of above 10.0

rate of above 10.0 technologies that will economically improve environmental performance

technologies that will economically improve environmental performance

7 8