![2 Types of Errors ,[object Object],[object Object],[object Object],Errors revealed by a trial balance ( errors in which amount Dr not = amount Cr ) Errors not revealed by a trial balance ( errors in which amount Dr = amount Cr )](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a Correction Of Errors

Similar a Correction Of Errors (20)

Último

Último (20)

Correction Of Errors

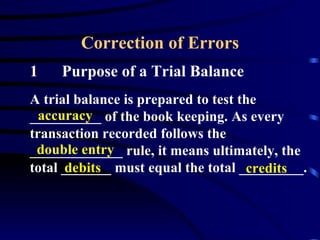

- 1. Correction of Errors 1 Purpose of a Trial Balance A trial balance is prepared to test the __________ of the book keeping. As every transaction recorded follows the _____________ rule, it means ultimately, the total _______ must equal the total _________. accuracy double entry debits credits

- 4. Example 2: a) How to reduce the balance in Account B by $80? b) How to increase the balance in Account B by $30? Answer: a) _________________________ b) _________________________ Debit Account B with $80 80 Credit Account B with $30 30 Account B Bal b/d 700

- 6. 4 Correction of Errors revealed by a Trial Balance A Error of recording in One account only Example (text page 340) Cash of $1,880 paid to Winston, a creditor, was recorded only in Winston’s account. Step 1: Right entry Creditor-Winston Dr 1,880 Cash Cr 1,880 Step 2: Wrong entry Creditor-Winston Dr 1,880 Step 4: Correcting entry Cash Cr 1,880 Step 3: Compare Put in missing entry

- 7. B Arithmetic Errors in ledgers Example (text page 340) Returns outwards account was overcast by $350 Step 1: Right bal Returns Outwards eg. Cr 1,000 Step 2: Wrong bal Returns Outwards eg. Cr 1,350 Step 4: Correcting entry Returns Outwards Dr 350 Step 3: Compare Enter on opposite side to reduce amount

- 8. C Error in recording unequal amounts in the accounts Example (text page 341) Cash purchase of equipment $1,000 was correctly credited in the Bank account but was incorrectly debited as $100 in the Equipment account. Step 1: Right entry Equipment Dr 1,000 Bank Cr 1,000 Step 2: Wrong entry Equipment Dr 100 Bank Cr 1,000 Step 4: Correcting entry Equipment Dr 900 Step 3: Compare Enter on same side to increase amount

- 9. D Error in recording on wrong side of a correct account Example (text page 342) Discount received of $60 had been posted to the wrong side of the account as a debit instead of as a credit. Step 1: Right entry Creditor Dr 60 Discount received Cr 60 Step 2: Wrong entry Creditor Dr 60 Discount received Dr 60 Step 4: Correcting entry Discount received Cr 120 Step 3: Compare Enter on opposite side to reduce amount

- 10. E Entry made in an incorrect account with double entry effect Example (text page 343) Payment of interest expense $100 had been credited to the Interest Revenue account. Step 1: Right entry Interest Expense Dr 100 Bank Cr 100 Step 2: Wrong entry Bank Cr 100 Interest Revenue Cr 100 Step 4: Correcting entry Interest Expense Dr 100 Interest Revenue Dr 100 Step 3: Compare Enter on opposite side to reduce amount

- 11. 5 Correction of Errors not revealed by a Trial Balance This type of errors have ________ equal to _______. A Errors of Omission Example (text book, pg 347) Cash payment of $400 for insurance expense was not recorded in the books. debits credits Step 1: Right entry Insurance expense Dr 400 Cash Cr 400 Step 2: Wrong entry No entry was made Step 4: Correcting entry Insurance expense Dr 400 Cash Cr 400 Step 4: Put in missing entries Step 3: Compare

- 12. B Error of Commission Example (text book pg 348) A purchase of goods of $500 from Karrim was posted to another supplier, Hassim’s account. Step 1: Right entry Purchases Dr 500 Creditor-Karrim Cr 500 Step 2: Wrong entry Purchases Dr 500 Creditor-Hassim Cr 500 Step 4: Correcting entry Creditor-Hassim Dr 500 Creditor-Karrim Cr 500 Step 3: Compare Enter on opposite side to reduce amount

- 13. C Error of Principle Example (text book pg 349) The purchase of equipment of $2,500 was posted incorrectly to the Repairs of Equipment account. Step 1: Right entry Equipment Dr 2,500 Bank Cr 2,500 Step 2: Wrong entry Repairs of Equipt Dr 2,500 Bank Cr 2,500 Step 4: Correcting entry Equipment Dr 2,500 Repairs of Equipt Cr 2,500 Step 3: Compare Enter on opposite side to reduce amount

- 14. D Error of Original Entry Example (text book pg 349) A purchase of goods of $800 from Ali was entered in the Purchases journal as $880 and the amount was posted to the ledger accounts. Step 1: Right entry Purchases Dr 800 Creditor-Ali Cr 800 Step 2: Wrong entry Purchases Dr 880 Creditor-Ali Cr 880 Step 4: Correcting entry Creditor-Ali Dr 80 Purchases Cr 80 Step 3: Compare Enter on opposite side to reduce amount

- 15. E Error of Complete Reversal Example (text book pg 350) A cheque of $400 received from Pipi was credited in the Bank account and debited in Pipi’s account. Step 1: Right entry Bank Dr 400 Debtor-Pipi Cr 400 Step 2: Wrong entry Debtor-Pipi Dr 400 Bank Cr 400 Step 4: Correcting entry Bank Dr 800 Debtor-Pipi Cr 800 Step 3: Compare Enter on opposite side to reduce amount

- 16. F Compensating Errors Example (text book pg 351) The Purchases account and the Sales account are each overstated by $600. Step 1: Right bal Purchases eg. Dr 1,000 Sales eg. Cr 4,000 Step 2: Wrong bal Purchases Dr 1,600 Sales Cr 4,600 Step 4: Correcting entry Sales Dr 600 Purchases Cr 600 Step 3: Compare Enter on opposite side to reduce amount

- 17. 6 Effects of correction of errors on net profit Where errors are detected / corrected before the Trading, Profit and Loss a/c and the Balance Sheet have been prepared, the corrections would involve the correcting journal entries in the _______________ and correction of the ________________. general journal ledger accounts

- 18. However, where the Trading, Profit and Loss a/c have been prepared before the errors have been detected / corrected, it would mean that the __________ and some items in the ______________ have been wrongly stated. net profit Balance sheet The correction of such errors would involve correcting journal entries, restatement of the __________ and restatement of some items in the ______________. net profit Balance sheet

- 19. Analysis of corrections on Net Profit Net profit = __________ - ___________ Revenue Expenses Rule 1: Debiting any expense / revenue account would __________ net profit. reduce Rule 2: Crediting any expense / revenue account would __________ net profit. increase

- 20. Effects of Errors on Net Profit and Balance Sheet Trading, Profit and Loss Account for the year ended 31 Dec 20X2 Opening stock 500 Sales 8,000 Purchases 6,100 6,600 less Closing stock 700 COGS 5,900 Gross profit c/d 2,100 8,000 8,000 Rent 200 Gross profit b/d 2,100 Insurance 120 Discount received 250 Lighting and heating 180 Depreciation 250 Net Profit 1,600 2,350 2,350

- 21. Balance Sheet as at 31 Dec 20X2 Fixed Assets $ Owner’s Equity $ Fixtures 2,200 Capital 1,800 less Prov for depn 800 Add Net Profit 1,600 1,400 3,400 Current Assets Less Drawings 900 Stock 700 2,500 Debtors 600 Current liabilities Bank 340 Creditors 600 1,640 3,040 3,100

- 22. Subsequently, the following errors were discovered: i) Sales were overcast by $70 ii) Rent was undercast by $40 iii) Cash $50 received from a debtor was entered in the cash book only iv) A purchase of $59 from Abel is entered in the books, debit and credit entries, as $95 Required: a) Correcting journal entries for the above errors; b) A Statement of Corrected Net Profit for the year ended 31 Dec 20X2; c) The Corrected Balance Sheet as at 31 Dec 20X2

- 23. a) Correcting Journal entries i) Sales Dr 70 ii) Rent Dr 40 iii) Debtor Cr 50 iv) Creditor-Abel Dr 36 Purchases Cr 36

- 24. b) Statement of Corrected Net Profit for yr ended 31 Dec 20X2 $ Net Profit as per accounts 1,600 Add (iv) Purchases under stated 36 1,636 Less (i) Sales overcast 70 (ii) Rent undercast 40 Corrected Net Profit 1,526

- 25. Corrected Balance Sheet as at 31 Dec 20X2 Fixed Assets $ Owner’s Equity $ Fixtures 2,200 Capital 1,800 less Prov for depn 800 Add Net Profit 1,526 1,400 3,326 Current Assets Less Drawings 900 Stock 700 2,426 Debtors (-50) 550 Current liabilities Bank 340 Creditors (-36) 564 1,590 2,990 2,990 d)