Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (6)

Similar a Business organisations

Similar a Business organisations (20)

Más de ry_moore

Más de ry_moore (20)

Último

Último (20)

Business organisations

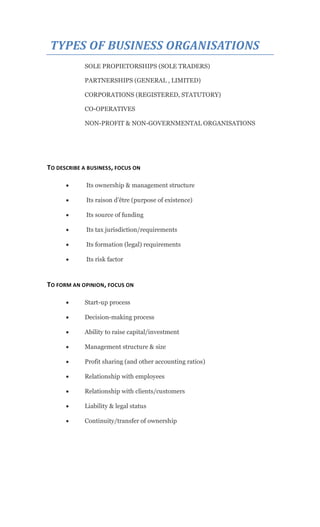

- 1. TYPES OF BUSINESS ORGANISATIONS SOLE PROPIETORSHIPS (SOLE TRADERS) PARTNERSHIPS (GENERAL , LIMITED) CORPORATIONS (REGISTERED, STATUTORY) CO-OPERATIVES NON-PROFIT & NON-GOVERNMENTAL ORGANISATIONS TO DESCRIBE A BUSINESS, FOCUS ON Its ownership & management structure Its raison d’être (purpose of existence) Its source of funding Its tax jurisdiction/requirements Its formation (legal) requirements Its risk factor TO FORM AN OPINION, FOCUS ON Start-up process Decision-making process Ability to raise capital/investment Management structure & size Profit sharing (and other accounting ratios) Relationship with employees Relationship with clients/customers Liability & legal status Continuity/transfer of ownership

- 2. SOLE PROPRIETORSHIP A separate and distinct organisation (business) with a single owner. Generally a small retail operation; or an individual professional service (eg dentist). Funded through owner’s efforts Profits treated as personal income (no tax) No specific legal regulations to start up Advantage Except for specific licences or certificates (eg liquor) one can start up the business at anytime with legal hindrances. It is recommended, however, that the business be registered (at minimal) with the business registry. Owner generally plays an active role in the management (often the only manager) Profits remain under the owner’s control Decisions can be put into effect at once without the necessity to consult The small size allows owner to be intimately involve with every aspect of the operation. The small size encourages a more personal relationship with employees Disadvantage Unlimited liability (claim on owner’s personal assets) Difficulty in raising ownership capital Lacks continuity (terminates with the owner) Difficult to transfer ownership Often impacted by owner’s absence

- 3. PARTNERSHIPS An incorporated association (business) with two or more co-owners. Has 2 to 20 persons; at least one must be a general partner Typically a small retail operation (e.g family store); or provision of professional service (eg, dentists, lawyers). Funded through the pooling of their resources and skills Profits are shared; and are subjected to personal income tax No specific legal regulations to start up; but are guided by the Partnership Act of 1890 (amended in 1907*). Advantage Except for specific licences or certificates (eg liquor) start up no legal hindrances. It is recommended, however, that the business be registered (at minimal) with the business registry; and partners sign a formal agreement* At least one owner must play an active role in the management Decisions are more consultative and reduces impulsive action The small size encourages a more personal relationship with employees The number of partners lend to greater specialisation and work distribution Disadvantage Unlimited liability (claim on owners’ personal assets) Difficulty in raising ownership capital as fewer people are interested in partnerships Lacks continuity (terminates with any change of owner) Difficult to transfer ownership (Agreement) Often impacted by poor decisions of any partner (Agency) Other comments General partners – has the right to manage the business (except forbidden by partnership agreement); and assume unlimited liability for the debts of the partnership. Limited partners – invest capital in the business but have no active role in its management. [also known as a sleeping partner]. Agency theory – implies that each partner acts as an agent of the partnership; and can thus bind the partners into a contract when acting within the scope of the business. Transfer of interest – a partner is free to dispose of his/her interest in the partnership in any legal way; but the current partners must approve of the incoming party in order for them to participate in the business.

- 4. CORPORATIONS (limited companies) A group of persons associated together to form a legal entity* to undertake some form of business activity. These are generally large businesses requiring heavy investment of capital (e.g a commercial bank) The capital required is divided into shares* and sold to interested individuals in variant amounts. The profits are divided in proportion to the amount and type of shares held by each shareholder*. The entity is required to pay corporation tax*; while shareholders pay income tax Subject to stringent legal rules and regulations in order to safeguard shareholder interest Must be registered with the Registrar of Companies or similar body Becomes an entity recognised as an individual under the law Owners elect a directorate (board) to ensure the investments are protected. They report to the others at the AGM* Decision making is left up to managers and other hired professionals. Employs high degree of specialisation of skills and management Owners are generally estranged from both employees and employers. Advantage Limited liability (claim on company assets only) Easier to raise ownership capital especially if business is doing well Has continuity as shareholders can transfer ownership interest Ownership (shares) can be easily transferred on the market at anytime. Disadvantage Impacted by double taxation; and government regulations Expansion in size leads to greater complexity and bureaucracy Other comments Public companies – can have as many owners (shareholders) as possible; the shares are bought and sold in a public securities market or stock exchange. Private companies – the number of owners are restricted [1 – 50]; the shares cannot be bought or sold in a public securities market or stock exchange. Statutory companies – are owned by the government (state) as established by act of Parliament.

- 5. CO-OPERATIVES An association of persons with common interest and goals to form a democratically controlled enterprise. It is self-governed (autonomous) – directors are chosen to manage its affairs Capital invested by members form the capital pool (base) of the organization Each member has his/her separate businesses; but pool funds to enjoy economies of scale (cheap inputs, advertising, etc) Economic returns (profit?) are mutually distributed Advantage Voluntary, non-discriminatory, and open membership policies Democratic control; one vote per member (regardless of contribution to the pool) Limited interest on capital invested* All surplus (less reserved deductions*) generated from operations belong to the members Act of continuous education and training to help improve the contribution of members Cooperating with other cooperatives to foster harmony and greater economies of scale Disadvantage Shares are not transferable Capital invested can be returned if person ceases to be a member New tax laws have impact this entity Limited liability of the cooperative itself Focus is not profit making but cost reduction and creation of investment opportunities.

- 6. NON-GOVERNMENTAL ORGANISATIONS (NGOs) & NON-PROFIT ORGANIZATIONS (NPOs) A large group of organisations that have been established as non-profit making entities. Its main focus is to work with people to achieve long-term improvements in the quality of their lives*. It can be a church, a youth group, a political party, a research institute, a professional association, a social club, a sports club, or a charity. Some NGOs have been created* by Acts of Parliament It can be incorporated* or unincorporated* Its management and operations are independent of government control It is managed by a of Board of Directors (elected to office for a specific period of time) It is a legal entity when it has been incorporated It has no (share) capital and is thus funded via restricted* and unrestricted* means. All of its funding must be declared and an account (preferably audited) given for the disbursement of said funds. NGOs operate on funds provided by donors who do not benefit directly from the organisations’ programmes. Sources of funding* include -: Donations Sponsors (special business events) legacies & bequests Fund-raising events (cake sales, fairs) Free rent & volunteerism Membership subscriptions Sales of publications or artifacts Government grants & subventions