The Power of Economic Science

•Descargar como PPT, PDF•

1 recomendación•982 vistas

This presentation highlights some of the powerful advances in economic science.

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (19)

Similar a The Power of Economic Science

Similar a The Power of Economic Science (20)

Más de Weydert Wealth Management

Más de Weydert Wealth Management (15)

Último

Último (20)

The Power of Economic Science

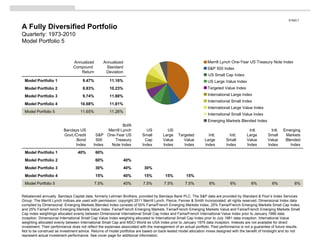

- 1. A Fully Diversified Portfolio Quarterly: 1973-2010 Model Portfolio 5 Rebalanced annually. Barclays Capital data, formerly Lehman Brothers, provided by Barclays Bank PLC. The S&P data are provided by Standard & Poor’s Index Services Group. The Merrill Lynch Indices are used with permission; copyright 2011 Merrill Lynch, Pierce, Fenner & Smith Incorporated; all rights reserved. Dimensional Index data compiled by Dimensional. Emerging Markets Blended Index consists of 50% Fama/French Emerging Markets Index, 25% Fama/French Emerging Markets Small Cap Index, and 25% Fama/French Emerging Markets Value Index. Fama/French Emerging Markets, Fama/French Emerging Markets Value and Fama/French Emerging Markets Small Cap Index weightings allocated evenly between Dimensional International Small Cap Index and Fama/French International Value Index prior to January 1989 data inception. Dimensional International Small Cap Value Index weighting allocated to International Small Cap Index prior to July 1981 data inception. International Value weighting allocated evenly between International Small Cap and MSCI World ex USA Index prior to January 1975 data inception. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See cover page for additional information. S1920.7 Annualized Compound Return Annualized Standard Deviation Model Portfolio 1 9.47% 11.16% Model Portfolio 2 8.83% 10.23% Model Portfolio 3 9.74% 11.88% Model Portfolio 4 10.68% 11.81% Model Portfolio 5 11.65% 11.26% Barclays US Govt./Credit Bond Index S&P 500 Index BofA Merrill Lynch One-Year US Treasury Note Index US Small Cap Index US Large Value Index Targeted Value Index Intl. Large Index Intl. Small Index Intl. Large Value Index Intl. Small Value Index Emerging Markets Blended Index Model Portfolio 1 40% 60% Model Portfolio 2 60% 40% Model Portfolio 3 30% 40% 30% Model Portfolio 4 15% 40% 15% 15% 15% Model Portfolio 5 7.5% 40% 7.5% 7.5% 7.5% 6% 6% 6% 6% 6% Merrill Lynch One-Year US Treasury Note Index S&P 500 Index US Small Cap Index US Large Value Index Targeted Value Index International Large Index International Small Index International Large Value Index International Small Value Index Emerging Markets Blended Index

- 2. In US dollars. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. US value and growth index data (ex utilities) provided by Fama/French. The S&P data are provided by Standard & Poor’s Index Services Group. CRSP data provided by the Center for Research in Security Prices, University of Chicago. International Value data provided by Fama/French from Bloomberg and MSCI securities data. International Small data compiled by Dimensional from Bloomberg, StyleResearch, London Business School, and Nomura Securities data. MSCI EAFE Index is net of foreign withholding taxes on dividends; copyright MSCI 2011, all rights reserved. Emerging markets index data simulated by Fama/French from countries in the IFC Investable Universe; simulations are free-float weighted both within each country and across all countries. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Values change frequently and past performance may not be repeated. There is always the risk that an investor may lose money. Small company risk: Securities of small firms are often less liquid than those of large companies. As a result, small company stocks may fluctuate relatively more in price. Emerging markets risk: Numerous emerging countries have experienced serious, and potentially continuing, economic and political problems. Stock markets in many emerging countries are relatively small, expensive, and risky. Foreigners are often limited in their ability to invest in, and withdraw assets from, these markets. Additional restrictions may be imposed under other conditions. Foreign securities and currencies risk: Foreign securities prices may decline or fluctuate because of: (a) economic or political actions of foreign governments, and/or (b) less regulated or liquid securities markets. Investors holding these securities are also exposed to foreign currency risk (the possibility that foreign currency will fluctuate in value against the US dollar). Size and Value Effects Are Strong around the World Annual Index Data S1220.8 Average Return (%) Standard Deviation (%) Annualized Compound Returns (%) US Large Value S&P 500 US Large Growth US Small Value CRSP 6-10 US Small Growth Intl. Value Intl. Small MSCI EAFE Intl. Growth Emg. Markets Value Emg. Markets Small Emg. Markets “Market” Emg. Markets Growth US Large Capitalization Stocks 1927–2010 US Small Capitalization Stocks 1927–2010 Non-US Developed Markets Stocks 1975–2010 Emerging Markets Stocks 1989–2010 14.03 11.88 11.35 19.17 15.98 13.95 18.48 19.17 13.67 11.29 25.01 21.98 19.46 17.05 27.01 20.51 21.93 35.13 30.94 34.05 24.56 28.13 22.29 22.21 42.01 40.67 36.40 34.89

- 4. Five Factors Help Determine Expected Return Annual Average Returns 1927–2010 Equity factors provided by Fama/French. Fixed factors provided by Ibbotson Associates. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. S1270.2 Market Factor All Equity Universe minus T-Bills Size Factor Small Stocks minus Large Stocks BtM Factor High BtM minus Low BtM Maturity Factor LT Govt. minus T-Bills Default Factor LT Corp. minus LT Govt.

- 5. The Risk Dimensions Delivered July1926–December 2010 Periods based on rolling annualized returns. 715 total 25-year periods. 775 total 20-year periods. 835 total 15-year periods. 895 total 10-year periods. 955 total 5-year periods. Performance based on Fama/French Research Factors. Securities of small companies are often less liquid than those of large companies. As a result, small company stocks may fluctuate relatively more in price. Mutual funds distributed by DFA Securities LLC. S1271.4 Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 99% of the time. Value beat growth 96% of the time. Value beat growth 86% of the time. US Value vs. US Growth OVERLAPPING PERIODS Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 95% of the time. Value beat growth 91% of the time. Value beat growth 82% of the time. Small beat large 96% of the time. Small beat large 83% of the time. Small beat large 78% of the time. Small beat large 68% of the time. Small beat large 60% of the time. US Small vs. US Large Small beat large 97% of the time. Small beat large 88% of the time. Small beat large 82% of the time. Small beat large 75% of the time. Small beat large 59% of the time.

- 6. The Risk Dimensions Delivered Based on rolling annualized returns. Rolling multi-year periods overlap and are not independent. This statistical dependence must be considered when assessing the reliability of long-horizon return differences. International Value vs. International Growth data: 133 overlapping 25-year periods. 193 overlapping 20-year periods. 253 overlapping 15-year periods. 313 overlapping 10-year periods. 373 overlapping 5-year periods. International Small vs. International Large data: 193 overlapping 25-year periods. 253 overlapping 20-year periods. 313 overlapping 15-year periods. 373 overlapping 10-year periods. 433 overlapping 5-year periods. International Value and Growth data provided by Fama/French from Bloomberg and MSCI securities data. International Small data compiled by Dimensional from Bloomberg, StyleResearch, London Business School, and Nomura Securities data. International Large is MSCI World ex USA Index gross of foreign withholding taxes on dividends; copyright MSCI 2011, all rights reserved. S1271.4 January 1975–December 2010 January 1970–December 2010 Small beat large 100% of the time. Small beat large 100% of the time. Small beat large 84% of the time. Small beat large 76% of the time. Small beat large 75% of the time. International Small vs. International Large Small beat large 100% of the time. Small beat large 97% of the time. Small beat large 82% of the time. Small beat large 78% of the time. Small beat large 78% of the time. Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 98% of the time. International Value vs. International Growth OVERLAPPING PERIODS Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 100% of the time. Value beat growth 98% of the time.

- 11. Mutual Fund Expenses “ After costs, the return on the average actively managed dollar will be less than the return on the average passively managed dollar for any time period.” — William F. Sharpe, 1990 Nobel Laureate William F. Sharpe, “The Arithmetic of Active Management,” Financial Analysts Journal 47, no. 1 (January/February 1991): 7-9. Mutual fund expense ratios as of April 9, 2010. Asset weighting based on net assets as of December 31, 2008. Data provided by Morningstar, Inc. Passive funds are those coded by Morningstar as Index Funds. Average of All Funds Weighted Average, Based on Fund Assets Active Passive Domestic Mutual Fund Expense Ratios Average of All Funds Weighted Average, Based on Fund Assets Average of All Funds Weighted Average, Based on Fund Assets Active Passive Average of All Funds Weighted Average, Based on Fund Assets International Mutual Fund Expense Ratios S1420.5

- 13. The Limits of Fund Rating Services Funds A, B, C, and D are actual funds. They are not identified because the purpose of this illustration is to emphasize that ratings, by themselves, do not provide enough information to make a sound investment decision. Morningstar: Five stars is highest rating; one star is lowest rating. US News & World Report: 100 is highest rating; 1 is lowest rating. S1440.1 Fund A Fund B Fund C Fund D Morningstar (Dec 2000) Forbes (Dec 2000) C A A+ D US News & World Report (Dec 2000) 34 50 10 93 Wall Street Journal (Jan 2001) E C A B BusinessWeek (Jan 2001) A No Rating B+ C

- 14. Innovations in Finance S1610.2 The Birth of Index Funds John McQuown, Wells Fargo Bank, 1971; Rex Sinquefield, American National Bank, 1973 Banks develop the first passive S&P 500 Index funds. Efficient Markets Hypothesis Eugene F. Fama, University of Chicago Extensive research on stock price patterns. Develops Efficient Markets Hypothesis, which asserts that prices reflect values and information accurately and quickly. It is difficult if not impossible to capture returns in excess of market returns without taking greater than market levels of risk. Investors cannot identify superior stocks using fundamental information or price patterns. Single-Factor Asset Pricing Risk/Return Model William Sharpe Nobel Prize in Economics, 1990 Capital Asset Pricing Model: Theoretical model defines risk as volatility relative to market. A stock’s cost of capital (the investor’s expected return) is proportional to the stock’s risk relative to the entire stock universe. Theoretical model for evaluating the risk and expected return of securities and portfolios. The Role of Stocks James Tobin Nobel Prize in Economics, 1981 Separation Theorem: 1. Form portfolio of risky assets. 2. Temper risk by lending and borrowing. Shifts focus from security selection to portfolio structure. “ Liquidity Preference as Behavior Toward Risk,” Review of Economic Studies, February 1958. Conventional Wisdom circa 1950 “ Once you attain competency, diversification is undesirable. One or two, or at most three or four, securities should be bought. Competent investors will never be satisfied beating the averages by a few small percentage points.” Gerald M. Loeb, The Battle for Investment Survival, 1935 Analyze securities one by one. Focus on picking winners. Concentrate holdings to maximize returns. Broad diversification is considered undesirable. 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 Diversification and Portfolio Risk Harry Markowitz Nobel Prize in Economics, 1990 Diversification reduces risk. Assets evaluated not by individual characteristics but by their effect on a portfolio. An optimal portfolio can be constructed to maximize return for a given standard deviation. Investments and Capital Structure Merton Miller and Franco Modigliani Nobel Prizes in Economics, 1990 and 1985 Theorem relating corporate finance to returns. A firm’s value is unrelated to its dividend policy. Dividend policy is an unreliable guide for stock selection. Behavior of Securities Prices Paul Samuelson, MIT Nobel Prize in Economics, 1970 Market prices are the best estimates of value. Price changes follow random patterns. Future share prices are unpredictable. “ Proof That Properly Anticipated Prices Fluctuate Randomly,” Industrial Management Review, Spring 1965. First Major Study of Manager Performance Michael Jensen, 1965 A.G. Becker Corporation, 1968 First studies of mutual funds (Jensen) and of institutional plans (A.G. Becker Corp.) indicate active managers underperform indices. Becker Corp. gives rise to consulting industry with creation of “Green Book” performance tables comparing results to benchmarks. Options Pricing Model Fischer Black, University of Chicago; Myron Scholes, University of Chicago; Robert Merton, Harvard University Nobel Prize in Economics, 1997 The development of the Options Pricing Model allows new ways to segment, quantify, and manage risk. The model spurs the development of a market for alternative investments.

- 15. Innovations in Finance S1610.2 Variable Maturity Strategy Implemented Eugene F. Fama With no prediction of interest rates, Eugene Fama develops a method of shifting maturities that identifies optimal positions on the fixed income yield curve. “ The Information in the Term Structure,” Journal of Financial Economics 13, no. 4 (December 1984): 509-28. Multifactor Asset Pricing Model and Value Effect Eugene Fama and Kenneth French, University of Chicago Improves on the single-factor asset pricing model (CAPM). Identifies market, size, and “value” factors in returns. Develops the three-factor asset pricing model, an invaluable asset allocation and portfolio analysis tool. “ Common Risk Factors in the Returns on Stocks and Bonds,” Journal of Financial Economics 33, no. 1 (February 1993): 3-56. A Major Plan First Commits to Indexing New York Telephone Company invests $40 million in an S&P 500 Index fund. The first major plan to index. Helps launch the era of indexed investing. “ Fund spokesmen are quick to point out you can’t buy the market averages. It’s time the public could.” Burton G. Malkiel, A Random Walk Down Wall Street, 1973 ed. International Size Effect Steven L. Heston, K. Geert Rouwenhorst, and Roberto E. Wessels Find evidence of higher average returns to small companies in twelve international markets. “ The Structure of International Stock Returns and the Integration of Capital Markets,” Journal of Empirical Finance 2, no. 3 (September 1995): 173-97. The Size Effect Rolf Banz, University of Chicago Analyzed NYSE stocks, 1926-1975. Finds that, in the long term, small companies have higher expected returns than large companies and behave differently. Integrated Equity Eugene F. Fama and Kenneth R. French Increasing exposure to small and value companies relative to their market weights and integrating the portfolio across the full range of securities may reduce the turnover and transaction costs normally associated with forming an asset allocation from multiple components. “ Migration,” CRSP Working Paper No. 614, Center for Research in Security Prices, University of Chicago, February 2007. 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Nobel Prize Recognizes Modern Finance Economists who shaped the way we invest are recognized, emphasizing the role of science in finance. William Sharpe for the Capital Asset Pricing Model. Harry Markowitz for portfolio theory. Merton Miller for work on the effect of firms’ capital structure and dividend policy on their prices. Database of Securities Prices since 1926 Roger Ibbotson and Rex Sinquefield, Stocks, Bonds, Bills, and Inflation An extensive returns database for multiple asset classes is first developed and will become one of the most widely used investment databases. The first extensive, empirical basis for making asset allocation decisions changes the way investors build portfolios.

- 19. MSCI Disclosure S2000.5 Copyright MSCI 2011. Unpublished. All rights reserved. This information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an “as is” basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates, nor any other person involved in or related to compiling, computing or creating this information makes any express or implied warranties or representations with respect to such information or the results to be obtained by the use thereof, and MSCI, its affiliates, and each such other person hereby expressly disclaims all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any other person involved in or related to compiling, computing, or creating this information have any liability for any direct, indirect, special, incidental, punitive, consequential, or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have anticipated, the possibility of such damages.

Notas del editor

- Talking Points: Model Portfolio 5 completes this multifactor construction by diversifying outside the US. All four US asset classes are reduced by half, from 15% to 7.5% allocations, and the balance is apportioned equally to five non-US asset classes—international large, small, large value, and small value indexes, and emerging markets blended index. The portfolio’s 60% equity allocation is now evenly split between the US and international markets, with roughly equal exposures to size and BtM. The historical data for the performance period shows Model Portfolio 5 producing the highest annualized compound return of all the portfolios, without an increase in volatility. In fact, adding the global component reduces the variability in the portfolio’s return due to the lower correlation of international and US risk dimensions. Compared to the original 60/40 balanced strategy, Model Portfolio 5 offers higher annualized return with only slightly higher volatility. A globally diversified allocation harnesses the power of markets, manages the risk-return tradeoff, provides broad diversification, and offers calculated exposure to compensating risk factors through structured investing.

- Talking Points: The size and BtM effects appear in both US and international markets—strong evidence that the risk factors are systematic across the globe. This graph demonstrates the higher expected returns offered by small cap stocks and value (high-BtM) stocks in the US, non-US developed, and emerging markets. Note that the international and emerging markets data is for a shorter time frame. Small cap stocks are considered riskier than large cap stocks, and value stocks (as defined by a higher book-to-market ratio) are deemed riskier than growth stocks. These higher returns reflect compensation for bearing higher risk. A multifactor approach incorporates both size and value measures—and exposure to non-US markets—in an effort to increase expected returns and reduce portfolio volatility. An effective way to capture these effects is through portfolio structure.

- Talking Points: Research shows that most of the variation in returns among equity portfolios can be explained by the portfolios’ relative exposure to three compensated risk factors: • Market factor—Stocks have higher expected returns than fixed income securities. • Size factor—Small cap stocks have higher expected returns than large cap stocks. • Book-to-Market (BtM) factor—Lower-priced “value” (high BtM) stocks have higher expected returns than higher-priced “growth” stocks (low BtM). Structuring a portfolio around compensated risk factors can change priorities in the investment process. The focus shifts from returns chasing (through stock picking or market timing) to diversification across multiple asset classes in a portfolio. The model in this slide illustrates this multifactor approach. Investors receive an average expected return (above T-bills) according to the relative risks they assume in their portfolios. The main factors driving expected returns are sensitivity to the market, sensitivity to small cap stocks (size factor), and sensitivity to value stocks (as measured by book-to-market ratio). Any additional average expected return in the portfolio may be attributed to unpriced risk. Average explanatory power (R 2 ) is for the Fama/French equity benchmark universe. R 2 describes the goodness of fit of a regression model by indicating the proportion of the total variance of the dependent variable explained by the model.

- Academic research has identified five risk dimensions that explain most of the relative performance between portfolios. The three equity risk factors are: Market—Stocks have higher expected returns than fixed income securities. Size—Small cap stocks have higher expected returns than large cap stocks. Book-to-Market (BtM)—Lower-priced “value” (high BtM) stocks have higher expected returns than higher-priced “growth” stocks (low BtM). Two additional factors reflect compensated risk in the fixed income markets. These are: Maturity—Longer-term bonds are riskier than shorter-term instruments. Default—Instruments of lower credit quality are riskier than instruments of higher credit quality. The historical return premiums for these risk factors are documented in the graph. Equities have offered a higher expected return than fixed income, but these stronger premiums come with higher risk. Structuring a portfolio around compensated risk factors can change many aspects of the investment process. Rather than focusing on individual stock or bond selection, investors work to achieve diversified, controlled exposure to the risk factors that drive expected returns. An investor first determines his portfolio’s stock/bond mix, and then decides how much additional small cap and value to hold in pursuit of higher expected returns. The level of risk assumed in the fixed income component may depend on why an investor is holding fixed income. For example, an equity-driven investor who wants to reduce portfolio volatility may hold less risky debt instruments, while an investor pursuing higher yield or income may take more maturity and default risk.

- This slide documents the frequency with which the value and size premiums have been positive over various time periods in the US stock market from 1926 to 2010. As the results illustrate, US value stocks have outperformed US growth stocks—and US small cap stocks have outperformed US large cap stocks—in a majority of all the rolling return periods measured. The US value premium has been positive more often than the size premium. The time periods, which range from five to twenty-five years, are based on annualized returns for rolling 12-month periods (e.g., January-December, February-January, March-February, etc.). The total number of 12-month periods for each time frame is indicated in the footnotes.

- This slide documents the frequency with which the value and size premiums have been positive over various time periods in the international (non-US) developed stock markets from 1975-2010. In the international markets, value stocks have outperformed growth stocks—and small cap stocks have outperformed large cap stocks—in a majority of all rolling return periods measured. The value premium has been strongly positive more often than the size premium. The time periods, which range from five to twenty-five years, are based on annualized returns for rolling 12-month periods (e.g., January-December, February-January, March-February, etc.). The total number of 12-month periods for each time frame is indicated in the footnotes. The set of available data for non-US developed markets is considerably shorter than US markets. As a result, the smaller set of observations can amplify the effect of sustained periods of negative or positive premiums. This may explain part of the frequency difference between the 20-year and 15-year periods for the international small cap premium.

- Talking Points: The difference in returns among portfolios is largely determined by relative exposure to the market, small cap stocks, and value stocks. Stocks offer higher expected returns than fixed income due to the higher perceived risk of being in the market. Many economists further believe that small cap and value stocks outperform large cap and growth because the market rationally discounts their prices to reflect underlying risk. The lower prices give investors greater upside as compensation for bearing this risk. Investors who want to earn above-market returns must take higher risks in their portfolio. The cross-hair map illustrates that tilting a portfolio toward small cap and value stocks increases the exposure to risk and expected return. Decreasing this exposure relative to the market results in lower risk and lower expected return.

- This analysis offers further insight into the potential consequences of both successful and failed market timing. The graph plots the S&P 500’s annualized compound return since 1970. The green bar (far left) shows what a buy-and-hold investor would have earned in annualized return for the entire period. The bars to the right show the incremental return impact if an investor had missed the best or worst day, month, quarter, or longer sequence during the period. For example, the worst market day since 1970 occurred on October 19, 1987. An investor who avoided the worst day would have earned a 10.57% annualized return, but missing the best day would have reduced the return to 9.70%. If daily market returns are random, market timing is a flip of the coin. Investors who attempt to predict market drops are just as likely to avoid them as to miss out on strong return periods.

- Talking Points: The key ingredients for investment success: • Diversification. A diversified strategy captures the compensated risk dimensions of the markets in the most reliable fashion. • Low costs. Management fees, trading commissions, market impact costs, bid/ask spreads, administrative expenses, and sales commissions (if any) directly reduce net investment returns. The combined effect of these costs can be difficult to compute and can consume a surprisingly high proportion of the gross investment returns offered by the capital markets. • Disciplined policy. Portfolio structure is the key determinant of results. The principal challenge for investors is to develop an asset allocation policy that matches an investor's risk preferences with returns offered by the capital markets. A successful policy is one that can be adhered to without anxiety in both good and bad markets.

- Talking Points: In both US and non-US strategies, the average actively managed mutual fund is considerably more expensive than the average passively managed fund. The graph compares average expense ratios of actively managed funds to those of passive funds. The ratios are presented as simple averages and weighted averages. The weighted average calculation indicates that larger funds tend to have lower expenses than smaller funds. Active managers, on average, charge more than twice the fees of passive managers. This is also true in the international fund universe, although the differences are not as large due to the higher costs of investing in non-US markets. Nobel laureate William Sharpe has pointed out that active management in aggregate must underperform passive management, not due to controversial financial theories but by the simple laws of arithmetic.

- Talking Points: Active managers seek to beat the market through stock selection and market timing. They generally charge higher fees than passive managers as compensation for their perceived “skill.” These fees can inflict a significant penalty on net investment returns and terminal wealth, as the above graph demonstrates for various cost levels.

- Talking Points: True insight arises from scientific evaluation of the sources of return in a portfolio. A prospective investor should understand how much of a mutual fund’s performance is based on risk factor exposure and how much is the result of unexplained forces and random error. The chart suggests that mutual fund ratings offered through professional services and the financial media are anything but scientific. Funds A, B, C and D represent actual funds that received grades or ratings from the respective “expert” sources. Proper investment analysis requires a consistent and clearly explained methodology. Before relying on any mechanical rating system to select investment managers, investors should thoroughly understand how the rating was determined.

- Talking Points: Financial science is a relatively young academic field. But the theories, research, and applications have significantly influenced investment methodology over the last half-century. This timeline offers some of the high points in the evolution of modern finance. Prior to 1950, conventional investment managers shunned diversification in favor of securities analysis and concentrated stock picking. In 1952, Harry Markowitz introduced the modern investment age with his landmark work on building optimal portfolios using diversification and mean-variance analysis. The following two decades brought major developments in asset pricing and market efficiency.

- Talking Points: The rise of computing power and stock return databases gave academics the tools to empirically test their theories and develop more advanced models to explain securities behavior. Since the 1970s, this research has led to the introduction of advanced forms of passive investing, while casting increasing doubt on the value of active management. More recently, advanced quantitative methods have given rise to the multifactor approach in portfolio construction, and integrated equity.

- Talking Points: Active managers spend time and resources attempting to identify mispricing in the market, even though imbalances are not easily exploited on a consistent, cost-effective basis. An active manager's stock picking and market timing efforts may result in frequent trading and higher turnover, which can undermine asset class exposure and generate higher costs and fees in a portfolio. An index manager may provide more consistent asset class exposure at a lower cost to the portfolio. But an emphasis on reduced tracking error may force the manager to buy and sell when the commercial benchmark is reconstituted. This tracking commitment drives a manager’s strategy and often results in higher transaction costs and price impact experienced around reconstitution dates. An efficient market approach focuses on cost-effective asset class investing. Rather than chasing returns through stock picking and market timing, an asset class manager seeks to capture risk dimensions identified through academic research. Unlike a pure indexing approach, an asset class strategy allows a flexible portfolio composition and gives traders more freedom to pursue value in the transaction process. This can result in lower costs, more precise asset class exposure, and enhanced returns.

- Talking Points: These principles influence a structured passive approach to building portfolios around compensated risk factors: • Markets work—Intense competition drives the market to near-instant efficiency. Securities prices are fair and reflect the best estimate of the company’s actual value. Efforts to identify undervalued stocks or markets are not rewarded consistently. • Diversification is key—It reduces the impact of individual securities and enables investors to scientifically employ the risk factors that offer higher expected returns. • Risk and return are related—Only nondiversifiable risk is systematically rewarded over time. So, differences in the average returns of portfolios are due to differences in average risk. Multifactor investing brings a systematic approach to harnessing these risks to deliver above-market performance over time. • Portfolio structure explains performance—Asset allocation, not stock picking or market timing, accounts for most of the performance in a diversified investment strategy.

- Talking Points: Relative performance in fixed income is largely driven by two dimensions: bond maturity and credit quality. Bonds that mature farther in the future are subject to the risk of unexpected changes in interest rates. Bonds with lower credit quality are subject to the risk of default. Extending bond maturities and reducing credit quality increases potential returns, although these returns come with higher volatility, as measured by standard deviation. By understanding the dimensions of risk in the bond market, investors may better determine their risk/return profile and estimate the total risk exposure necessary to pursue their expected return goals. Investors seeking the greater expected returns of stocks may choose to focus on equities and keep their bond portfolio short and high in quality. Investors who prefer the lower risk of fixed income can still target higher expected returns by holding bonds with slightly longer maturities and slightly lower credit quality.

- This slide must be included in all presentations with slides that contain MSCI data. The disclosure indicates that MSCI data may only be used internally and cannot be distributed; however that message is meant for individual investors. Under a special agreement with MSCI, advisors may redistribute the data provided in these slides. The agreement only covers these slides.