1. TAIWAN

Pegatron

4938 TT Outperform

Price (at 05:46, 19 Mar 2013 GMT) NT$43.80 Solid phase II of its turnaround

12-month target NT$ 55.00 Event

Upside/Downside % 25.6 We reiterate our OP rating on Pegatron but raise our SOTP-based TP to

Valuation NT$ 55.00 NT$55 from NT$51, given our now more positive view (vs our

- Sum of Parts

GICS sector recommendation upgrade note on 24 Jan) on its iPhone mini shipments and

Technology Hardware & Equipment our higher 2013 margins and EPS assumption for its core as well as non-core

Market cap NT$m 100,302 (mainly Casetek) business. Pegatron remains our top pick in the ODM/EMS

30-day avg turnover US$m 17.6 space.

Market cap US$m 3,371

Number shares on issue m 2,290

Impact

Solid 1st source position in iPhone mini: While we believe Pegatron will be

Investment fundamentals the major supplier of Apple’s iPhone mini products, we now expect its

Year end 31 Dec 2011A 2012E 2013E 2014E shipments to likely come in higher than our original forecast of 7–8m units per

Revenue bn 500.6 768.1 930.1 1,075.2 quarter (from late 3Q13). We believe the company will also face lower risk of

Reported profit bn 0.1 6.1 9.8 11.6

Profit bonus exp bn 0.1 6.1 9.8 11.6 product transition in iPhone mini, given its progress along the learning curve

Bon exp/rep profit % 0.0 0.0 0.0 0.0 and good execution on iPhone 4/4S production. We forecast Pegatron’s

Adjusted profit bn 0.1 6.1 9.8 11.6

EPS rep NT$ 0.05 2.71 4.36 5.13 iPhone order allocation from Apple may approach 18–20% in 2013 (up from

EPS rep growth % -98.2 5,392.9 61.3 17.5 <10% in 2012), and expect this increase in shipments to expand its OPM.

EPS bonus exp NT$ 0.05 2.71 4.36 5.13

EPS bonus growth % -98.2 5,392.9 61.3 17.5 iPad mini demand better than expected: The street expects the iPad mini’s

PER rep x 889.4 16.2 10.0 8.5

PER bonus exp x 889.4 16.2 10.0 8.5 sales to decline from 12m units in 1Q13 to 8-10m in 2Q13, due to the launch

Total DPS NT$ 1.45 0.00 1.42 0.00 of re-fresh models in late 3Q12. However, our checks indicate that iPad mini

Total div yield % 3.3 0.0 3.2 0.0

ROA % -1.9 0.7 2.0 2.7 demand in 2Q13 remain strong, thanks to its better sales from emerging

ROE % 0.1 6.5 9.7 10.5 countries, especially in Asia. While we expect Pegatron’s 2Q13 iPad mini

EV/EBITDA x 115.5 14.4 8.9 6.9

Net debt/equity % 10.9 25.1 32.4 29.2 sales to likely come in better than consensus estimate, we think its improving

P/BV x 1.1 1.0 0.9 0.9 profit (from the break-even in Dec. 2012) could translate to earnings upside.

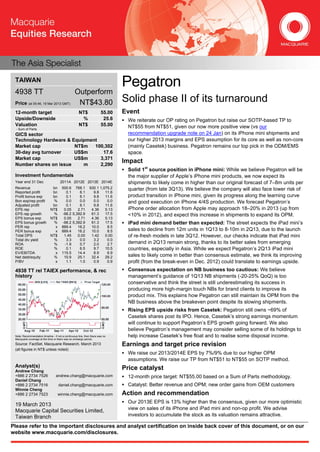

4938 TT rel TAIEX performance, & rec Consensus expectation on NB business too cautious: We believe

history management’s guidance of 1Q13 NB shipments (-20-25% QoQ) is too

conservative and think the street is still underestimating its success in

producing more high-margin touch NBs for brand clients to improve its

product mix. This explains how Pegatron can still maintain its OPM from the

NB business above the breakeven point despite its slowing shipments.

Rising EPS upside risks from Casetek: Pegatron still owns ~69% of

Casetek shares post its IPO. Hence, Casetek’s strong earnings momentum

will continue to support Pegatron’s EPS growth going forward. We also

believe Pegatron’s management may consider selling some of its holdings to

Note: Recommendation timeline - if not a continuous line, then there was no help increase Casetek’s free float and to realise some disposal income.

Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, March 2013 Earnings and target price revision

(all figures in NT$ unless noted)

We raise our 2013/2014E EPS by 7%/9% due to our higher OPM

assumptions. We raise our TP from NT$51 to NT$55 on SOTP method.

Analyst(s) Price catalyst

Andrew Chang

+886 2 2734 7526 andrew.chang@macquarie.com 12-month price target: NT$55.00 based on a Sum of Parts methodology.

Daniel Chang

+886 2 2734 7516 daniel.chang@macquarie.com Catalyst: Better revenue and OPM; new order gains from OEM customers

Winnie Cheng

+886 2 2734 7523 winnie.cheng@macquarie.com Action and recommendation

Our 2013E EPS is 13% higher than the consensus, given our more optimistic

19 March 2013

Macquarie Capital Securities Limited, view on sales of its iPhone and iPad mini and non-op profit. We advise

Taiwan Branch investors to accumulate the stock as its valuation remains attractive.

Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our

website www.macquarie.com/disclosures.

3. Macquarie Research Pegatron

Pegatron (4938 TT, Outperform, Target Price: NT$55.00)

Quarterly Results 3Q/12A 4Q/12E 1Q/13E 2Q/13E Profit & Loss 2011A 2012E 2013E 2014E

Revenue m 192,449 238,831 209,069 222,878 Revenue m 500,566 768,059 930,138 1,075,232

Gross Profit m 5,162 6,758 5,748 6,402 Gross Profit m 11,454 21,839 26,695 31,194

Operating Expenses m -5,002 -6,121 -4,976 -5,527 Operating Expenses m -15,739 -20,100 -21,457 -23,028

Operating Income m 160 637 772 875 Operating Income m -4,285 1,739 5,238 8,167

Net Non-operating income m 1,346 2,278 1,350 1,350 Net Non-operating income m 4,348 5,241 5,750 5,100

Pre-Tax Income m 1,506 2,915 2,122 2,225 Pre-Tax Income m 63 6,980 10,988 13,267

Tax Expense m -153 -263 -212 -267 Tax Expense m 48 -876 -1,143 -1,654

Exceptionals m 0 0 0 0 Exceptionals m 0 0 0 0

Minority Interests m 0 0 0 0 Minority Interests m 0 0 0 -42

Reported Earnings m 1,353 2,652 1,910 1,958 Reported Earnings m 111 6,104 9,845 11,571

Reported Earnings (bonus exp) m 1,353 2,652 1,910 1,958 Reported Earnings (bonus exp) m 111 6,104 9,845 11,571

Bonus exp / Reported Earnings % 0.0 0.0 0.0 0.0 Bonus exp / Reported Earnings % 0.0 0.0 0.0 0.0

Adjusted Earnings m 1,353 2,652 1,910 1,958 Adjusted Earnings m 111 6,104 9,845 11,571

EBITDA m 1,057 1,533 1,919 2,021 EBITDA m -932 5,324 9,823 13,552

EPS (rep) NT$ 0.60 1.18 0.85 0.87 EPS (rep) NT$ 0.05 2.71 4.36 5.13

EPS pcp growth (rep) % 269.9 171.9 49.6 138.3 EPS growth (rep) % -98.2 5,392.9 61.3 17.5

EPS (rep bonus exp) NT$ 0.60 1.18 0.85 0.87 EPS (rep bonus exp) NT$ 0.05 2.71 4.36 5.13

EPS pcp growth (rep bonus exp) % 269.9 171.9 49.6 138.3 EPS growth (rep bonus exp) % -98.2 5,392.9 61.3 17.5

EPS (adj) NT$ 0.60 1.18 0.85 0.87 EPS (adj) NT$ 0.05 2.71 4.36 5.13

EPS pcp growth (adj) % 269.9 171.9 49.6 138.3 EPS growth (adj) % -98.2 5,392.9 61.3 17.5

Revenue pcp growth % 23.3 55.0 40.1 18.8 PE (rep) x 889.4 16.2 10.0 8.5

Operating Income pcp growth % nmf 26.1 79.7 71.0 PE (rep bonus adj) x 889.4 16.2 10.0 8.5

Reported Earnings pcp growth % 269.9 171.9 49.6 138.3 PE (adj) x 889.4 16.2 10.0 8.5

Gross Profit Margin % 2.7 2.8 2.7 2.9 Total DPS NT$ 1.45 0.00 1.42 0.00

Operating Income Margin % 0.1 0.3 0.4 0.4 Total Div Yield % 3.3 0.0 3.2 0.0

Reported Earnings Margin % 0.7 1.1 0.9 0.9 Weighted Average Shares m 2,256 2,256 2,256 2,256

EBITDA Margin % 0.5 0.6 0.9 0.9 Period End Shares m 2,256 2,256 2,256 2,256

Profit and Loss Ratios 2011A 2012E 2013E 2014E Cashflow Analysis 2011A 2012E 2013E 2014E

Revenue Growth % 14.9 53.4 21.1 15.6 Reported Earnings m 111 6,104 9,845 11,571

Gross Profit Growth % -27.5 90.7 22.2 16.9 Depreciation & Amortisation m 3,353 3,585 4,585 5,385

Operating Income Growth % nmf nmf 201.2 55.9 Chgs in Working Cap m -7,246 -13,685 -10,872 -9,740

Reported Earnings Growth % -98.2 5,392.9 61.3 17.5 Other m -2,370 -2,780 -3,782 -3,828

EBITDA Growth % nmf nmf 84.5 38.0 Operating Cashflow m -6,152 -6,777 -223 3,388

Acquisitions m 0 0 0 0

Gross Profit Margin % 2.3 2.8 2.9 2.9 Capex m -2,400 -10,000 -8,000 -8,000

Operating Income Margin % -0.9 0.2 0.6 0.8 Asset Sales m 0 0 0 0

Reported Earnings Margin % 0.0 0.8 1.1 1.1 Other m 0 0 0 0

EBITDA Margin % -0.2 0.7 1.1 1.3 Investing Cashflow m -2,400 -10,000 -8,000 -8,000

Dividend (Ordinary) m -3,264 0 -3,205 0

Payout Ratio % 2,937.4 0.0 32.6 0.0 Equity Raised m 0 0 0 0

EV/EBITDA x 115.5 14.4 8.9 6.9 Debt Movements m 480 2,000 1,600 1,600

EV/EBIT x -53.2 24.9 13.3 10.0 Other m 875 -841 -673 -420

Financing Cashflow m -1,909 1,159 -2,277 1,180

Balance Sheet Ratios

ROE % 0.1 6.5 9.7 10.5 Net Chg in Cash/Debt m -10,461 -15,618 -10,500 -3,432

ROA % -1.9 0.7 2.0 2.7

ROIC % -8.1 1.5 3.8 5.2 Free Cashflow m -8,552 -16,777 -8,223 -4,612

Net Debt/Equity % 10.9 25.1 32.4 29.2 FCF per Share NT$ -3.79 -7.44 -3.64 -2.04

Interest Cover x nmf nmf nmf nmf P/FCF x -11.6 -5.9 -12.0 -21.4

Price/Book x 1.1 1.0 0.9 0.9

Book Value per Share NT$ 40.6 43.3 46.2 51.4

Balance Sheet 2011A 2012E 2013E 2014E

Cash m 24,074 11,538 3,838 4,814

Receivables m 69,689 87,932 106,488 123,099

Inventories m 51,899 57,402 69,496 80,311

Investments m 39,402 41,561 44,511 47,561

Fixed Assets m 30,223 36,638 40,053 39,668

Intangibles m 0 0 0 0

Other Assets m 12,318 15,754 18,503 20,221

Total Assets m 227,605 250,825 282,888 315,674

Payables m 83,812 93,872 113,651 131,337

Short Term Debt m 15,919 16,919 17,719 18,219

Long Term Debt m 18,165 19,165 19,965 20,465

Provisions m 0 0 0 0

Other Liabilities m 18,125 23,181 27,225 29,753

Total Liabilities m 136,021 153,137 178,560 199,774

Total S/H Equity m 91,584 97,688 104,328 115,899

Total Liab & S/H Funds m 227,605 250,825 282,888 315,674

All figures in NT$ unless noted.

Source: Company data, Macquarie Research, March 2013

19 March 2013 3

4. Macquarie Research Pegatron

Important disclosures:

Recommendation definitions Volatility index definition* Financial definitions

Macquarie - Australia/New Zealand This is calculated from the volatility of historical All "Adjusted" data items have had the following

Outperform – return >3% in excess of benchmark return price movements. adjustments made:

Neutral – return within 3% of benchmark return Added back: goodwill amortisation, provision for

Underperform – return >3% below benchmark return Very high–highest risk – Stock should be catastrophe reserves, IFRS derivatives & hedging,

expected to move up or down 60–100% in a year IFRS impairments & IFRS interest expense

Benchmark return is determined by long term nominal – investors should be aware this stock is highly Excluded: non recurring items, asset revals, property

GDP growth plus 12 month forward market dividend speculative. revals, appraisal value uplift, preference dividends &

yield minority interests

Macquarie – Asia/Europe High – stock should be expected to move up or

Outperform – expected return >+10% down at least 40–60% in a year – investors should EPS = adjusted net profit / efpowa*

Neutral – expected return from -10% to +10% be aware this stock could be speculative. ROA = adjusted ebit / average total assets

Underperform – expected return <-10% ROA Banks/Insurance = adjusted net profit /average

Medium – stock should be expected to move up total assets

Macquarie First South - South Africa or down at least 30–40% in a year. ROE = adjusted net profit / average shareholders funds

Outperform – expected return >+10% Gross cashflow = adjusted net profit + depreciation

Neutral – expected return from -10% to +10% Low–medium – stock should be expected to *equivalent fully paid ordinary weighted average

Underperform – expected return <-10% move up or down at least 25–30% in a year. number of shares

Macquarie - Canada

Outperform – return >5% in excess of benchmark return Low – stock should be expected to move up or All Reported numbers for Australian/NZ listed stocks

Neutral – return within 5% of benchmark return down at least 15–25% in a year. are modelled under IFRS (International Financial

Underperform – return >5% below benchmark return * Applicable to Australian/NZ/Canada stocks only Reporting Standards).

Macquarie - USA Recommendations – 12 months

Outperform (Buy) – return >5% in excess of Russell Note: Quant recommendations may differ from

3000 index return Fundamental Analyst recommendations

Neutral (Hold) – return within 5% of Russell 3000 index

return

Underperform (Sell)– return >5% below Russell 3000

index return

Recommendation proportions – For quarter ending 31 December 2012

AU/NZ Asia RSA USA CA EUR

Outperform 47.87% 54.89% 54.41% 41.93% 60.86% 44.14% (for US coverage by MCUSA, 6.10% of stocks followed are investment banking clients)

Neutral 37.94% 26.41% 38.24% 52.16% 33.70% 27.73% (for US coverage by MCUSA, 4.91% of stocks followed are investment banking clients)

Underperform 14.19% 18.70% 7.35% 5.91% 5.44% 28.13% (for US coverage by MCUSA, 3.33% of stocks followed are investment banking clients)

Company Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.

Analyst Certification:

The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the

compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The

analyst principally responsible for the preparation of this research receives compensation based on overall revenues of Macquarie Group Ltd ABN 94

122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken reasonable care to achieve and maintain

independence and objectivity in making any recommendations.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America

Ltd; Macquarie Capital (USA) Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd;

Macquarie Securities (NZ) Ltd; Macquarie First South Securities (Pty) Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities

(Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the

purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank

Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above

mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital

Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale clients of the Macquarie

Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or

disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We

do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has

established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to

regulatory requirements (including the FSA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in

this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In

preparing this research, we did not take into account your investment objectives, financial situation or particular needs. Macquarie salespeople, traders

and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the

opinions expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis,

macro-economic analysis, quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from

recommendations contained in other types of research, whether as a result of differing time horizons, methodologies, or otherwise. Before making an

investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate

in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities

can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in

international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of

the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty

that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject

to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising

from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions

through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise. The date and timestamp for above share price and

market cap is the closed price of the price date. #CLOSE is the final price at which the security is traded in the relevant exchange on the date indicated.

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the

Australian Securities Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm.

Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the

Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-

dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States

and sent to US persons. Any person wishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets

Canada Ltd should do so with Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie Capital Markets Canada

Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and

19 March 2013 4