Achieving better value from suppliers through market intelligence

•

1 recomendación•314 vistas

As the pound heads towards parity with the Euro, and the cost of Marmite hits the headlines, it is imperative to ensure that you are getting best value from all of your suppliers. Expense Reduction Analysts focuses on Procurement, helping our clients to get the best cost, quality and service possible from suppliers. Our quarterly newsletters highlight opportunities to reduce costs, and also highlight changes in the procurement environment.

Recomendados

Más contenido relacionado

Similar a Achieving better value from suppliers through market intelligence

Similar a Achieving better value from suppliers through market intelligence (20)

Más de Alan Birse

Más de Alan Birse (8)

Último

Último (20)

Achieving better value from suppliers through market intelligence

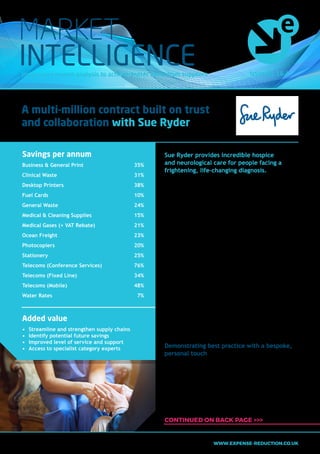

- 1. Issue No. 16.4Insight and market analysis to achieve better value from suppliers MARKET INTELLIGENCE Sue Ryder provides incredible hospice and neurological care for people facing a frightening, life-changing diagnosis. As with any charity, keeping costs down and securing the most competitive rates from suppliers is a high priority. However, for David White, Head of Procurement at Sue Ryder, a top-class procurement consultancy needed to offer much more than great savings. After a benchmarking exercise against another procurement consultancy, ERA’s fully engaged and highly personalised service completely overshadowed their competitors and the contract was awarded to ERA, led by St John Rowntree. Two years on and the relationship between Sue Ryder and ERA has become one cemented in trust. ERA’s team, now led by Client Manager Simon Dodson is currently tracking over £2 million of spend and delivering 23% savings across the board, with more on the horizon. Demonstrating best practice with a bespoke, personal touch David’s experience ensured he understood the value that a third-party procurement consultancy could bring to the charity. His approach was to invite a shortlist of two (ERA and A.N. Other) to perform a process demonstration on an existing cost centre in order to decide on an appointment. A multi-million contract built on trust and collaboration with Sue Ryder CONTINUED ON BACK PAGE >>> Savings per annum Business & General Print 35% Clinical Waste 31% Desktop Printers 38% Fuel Cards 10% General Waste 24% Medical & Cleaning Supplies 15% Medical Gases (+ VAT Rebate) 21% Ocean Freight 23% Photocopiers 20% Stationery 25% Telecoms (Conference Services) 76% Telecoms (Fixed Line) 34% Telecoms (Mobile) 48% Water Rates 7% Added value • Streamline and strengthen supply chains • Identify potential future savings • Improved level of service and support • Access to specialist category experts WWW.EXPENSE-REDUCTION.CO.UK

- 2. The Document Exchange (DX) system is a UK courier service established during the postal strikes of the 1970s and very quickly became the only alternative next-day delivery service. Its origins lie mainly within the legal sector, with its users’ network supplying a majority of legal firms within the UK. However, its tariff structure and the procedure behind DX’s calculation of the cost of the service to users are fraught with issues and sometimes not understood. The annual cost of the service is based on an estimate made by DX of the amount of mail anticipated to be dispatched during the forthcoming year to other DX users only. The user processes their DX mail by way of manually adding their unique number to each item dispatched and then delivering them to a nearby collection point, which is normally hosted by another DX user. The Member can become a host point by meeting certain criteria set by DX. The user is advised to monitor and manually record all of their outgoing mail over a two- week period each year. This annual monitoring should be completed over two weeks that typically reflect total annual usage, generally not in August or December. DX calculates the user’s next year’s subscription based on their own internal figures and the two-week monitoring period, which can only be viewed as accurate if completed properly by both parties. Therefore, the biggest problem with DX is that the fees are based on estimate, paid annually in advance, and generally unquantifiable, leaving the user with no knowledge as to whether they are getting value for money. There are very few options that enable DX users to accurately calculate the level of their subscription fee - apart from accurately recording manually every item sent whilst taking into consideration the varying weight, size and thickness of non-standard items. Rather than simply accepting the estimated annual DX invoice, it makes more financial sense to consider changes in procedure or methods of monitoring in order to confirm the actual cost of using the service instead of relying on the very limited information generally provided by DX. Do you really know whether you are getting the best value for money when using DX? Distribution by Zoe Willis WWW.EXPENSE-REDUCTION.CO.UK2 Market Intelligence Issue No. 16.4

- 3. To hedge or not to hedge? That is the question! Fuel by Duncan Rogers We are often asked by clients whether it is a “good idea” to hedge fuel purchases, and can one reduce costs as a result? Unfortunately, the simple answer is “it depends”, and the more complex answer is “it depends on luck”. Traditionally, transport operators, particularly big road fleets, airlines, and large shipping fleets have hedged their fuel purchasing in order to safeguard against unexpected sudden rises in fuel prices. However, we increasingly find that users of industrial fuel-oils such as Gasoil or Kerosene are considering whether a hedging strategy would be beneficial, particularly as volumes increase in the autumn/winter period. If a client is looking for absolute certainty in fuel costs for budgeting purposes for instance, a hedge can provide a very effective way to do this. It is likely to be marginally more cost- effective versus a fixed price offer for fuels, and normally does not require a commitment to buy minimum quantities of fuel - whereas fixed price deals normally do (adding a cost risk factor if volumes fall short of forecasts). The big cost risk However, in addition to the direct cost of the hedge, some hedging agreements require the client to pay the difference between the hedged price and actual price to the hedge provider, if the price of fuel falls below that price. There have recently been some quite spectacular cost penalties incurred by airlines in particular as kerosene prices tumbled. Hedges with less onerous conditions are available, but the premium payment for the hedge will be higher. Is hedging complicated? For most companies, a hedge is a very simple financial instrument available from not only specialist providers, but also banks and insurance companies. The key thing to remember about most of these hedge plans is that the price the client actually pays for their fuel is irrelevant. Because client-specific hedges would generally be prohibitively expensive to write and administer, most plans are based on fuel costs at wholesale markets (e.g. Rotterdam or Marseille). These markets price fuel in dollars per tonne, so it is important to realise that most hedges are against that measure and can exclude currency movements in sterling versus the dollar, and any increase in duty. Hedging plans generally therefore do not relieve users of following good procurement practice in buying their fuel. Fuel suppliers are constantly seeking opportunities to increase margin, whether at the pumps or in bulk deliveries. WWW.EXPENSE-REDUCTION.CO.UK3 Market Intelligence Issue No. 16.4

- 4. What does your Modern Day Slavery Act Statement say? by Simon Dodson The UK Modern Slavery Act 2015 has left many organisations in the UK wondering how best to tackle their anti-slavery supply chain statement. Since October 2015, under Section 54, commercial organisations with a turnover of more than £36m must produce a ‘slavery and human trafficking’ statement for each financial year, setting out what they have done to ensure there is no modern slavery in their business or supply chains. The Government has issued guidance but little in the way of a template to follow. Though the legislation does set out the following: A slavery and human trafficking statement for a financial year is: a. a statement of the steps the organisation has taken during the financial year to ensure that slavery and human trafficking is not taking place: i. in any of its supply chains, and ii. in any part of its own business, or c. a statement that the organisation has taken no such steps. An organisation’s slavery and human trafficking statement may include information about: a. the organisation’s structure, its business and its supply chains; b. its policies in relation to slavery and human trafficking; c. its due diligence processes in relation to slavery and human trafficking in its business and supply chains; d. the parts of its business and supply chains where there is a risk of slavery and human trafficking taking place, and the steps it has taken to assess and manage that risk; e. its effectiveness in ensuring that slavery and human trafficking is not taking place in its business or supply chains, measured against such performance indicators as it considers appropriate; f. the training about slavery and human trafficking available to its staff. It is notable that organisations can say no steps have yet been taken, but this is unlikely to show the organisation in a good light, and should not be considered beyond the first year, where some leniency may apply. It’s also worth remembering that organisations have to give the statement a prominent position on their homepage, as customers and competitors will be looking out for it. Some organisations below the £36m t/o threshold have elected to publish a statement anyway, in order to emphasise their efforts in this area. Of course many of them will be suppliers to those larger organisations, so they are likely to come under scrutiny from their customers anyway, as they attempt to prove their own case. What have organisations done about the Act and what they have said? Vinci Construction UK is a construction and facilities company and part of a group with £2bn turnover a year, employing around 9,000 people. It says, where appropriate, its supply chain should be registered with Constructionline, or have completed the company’s pre-qualification process. Its statement adds that the company will: “carry out audits on supply-chain partners that incorporate physical audits of suppliers’ records pertaining to workers on our projects, to ensure that they are compliant with our requirements and expectations. Suppliers employing or providing non-UK nationals undergo appropriate investigation to understand their recruitment methods and their management of permits and working visas”. If you google ‘Vinci Modern Day Slavery’ you can see a pdf of the full statement, signed by the Chief Executive. Millennium & Copthorne Hotels is a leading global hospitality management and real estate group, with 120 hotels in 79 businesses around the world. It has several business models – for example, it owns hotels operated by third parties, such as Hilton and AccorHotels, while also franchising its brands for use by third-party hotel owners who, in turn, operate their hotels. So, as its statement notes, it has “varying degrees of control over operational policies and procedures and the review and selection of suppliers”. While the hotel group has many safeguards in place, it says: “We do not believe an organisation can ‘achieve compliance’ in this important area and will continue to look for ways to improve upon our existing policies and procedures.” Unusually, it also invites comment from employees and other stakeholders. The full statement can be found by googling ‘Millennium Hotels Modern Day Slavery’. London Universities Purchasing Consortium (LUPC) was the first UK public sector consortium to publish a slavery and human trafficking statement. A non-profit professional buying organisation owned by its members, LUPC made the move despite its annual turnover being below the legal £36m threshold. As its members spend around £200m annually through supply agreements, it was felt it warranted a statement. In it, LUPC identified the principal risk categories as office supplies, laboratory consumables, ICT equipment and some estates services, such as cleaning and security services. LUPC said many suppliers in higher risk categories have committed to the Base Code of the Ethical Trading Initiative, and it was trying to persuade its remaining suppliers in these categories to join them. It’s quite a read and can be found by googling ‘London Universities Purchasing Consortium Slavery and Human Trafficking Statement’. There are plenty more examples including Reynolds Catering Supplies, John Lewis Partnership, Haymarket Media Group, Pendragon, AB InBev and Gleadell Agriculture. Simply googling the organisation’s name and ‘Modern Day Slavery’ on any of these will show that there is a variety of different approaches. If you need further help, a register has been set up by CIPS and anti-trafficking charity Unseen to host a searchable database whereby you can find details of what companies are doing to combat slavery in their supply chains. This site can be found at tiscreport.org. WWW.EXPENSE-REDUCTION.CO.UK WWW.EXPENSE-REDUCTION.CO.UK4 5 Market Intelligence Market IntelligenceIssue No. 16.4 Issue No. 16.4

- 5. Communications Industry news Communications by the Communications Team Apple has announced the iPhone 7 which is very similar to the iPhone 6S, but it has a much improved camera with dual lens, a new jet black glossy finish and a new ‘home’ button. The headphone jack has also disappeared, so wireless headphone sales are no doubt going to shoot up as well as adding a cost for users - although we understand Apple will supply a converter with the phone. How much are wireless headphones needed for business use? Is an improved camera needed for business use? Also announced were changes to iPads, a new Apple Watch 2 which is “swimproof” complete with a built-in GPS in case you get lost at sea. IOS10 was also announced. Depending on your phone renewal cycle, you might like to consider the rumour that Apple will have a major 10-year anniversary iPhone update in 2017. Samsung, presumably in an effort to beat Apple to market with its new Samsung 7, has hit the buffers with a recall due to exploding batteries. US Civil Aviation has advised passengers not to turn on these devices during flight. Mobile networks continue to evolve the charging structures for data and roaming which seem to be more and more complicated with each new announcement. Presumably revenue lost from the regulated cost reductions over the last few years, the latest in July 2016, mean the revenue bubble has to pop up elsewhere. How Brexit will affect roaming costs in Europe no-one knows. Apple’s new operating system IOS10 may also change the landscape and encourage more tariff changes, as it now allows you to call your contacts (seamlessly using the green button), via WhatsApp, Facetime and other apps which use your data allowance. So you should watch out for a switch from voice minutes to data if you have no control over how your users use their company phones. All companies really need a mobile phone policy these days which is written to take account of their mobile contract. Without giving employees any advice/instructions on how to use their phones, you may end up with extra costs. Do you plan for staff to use free hotel wifi whilst travelling to save costs? Many hoteliers are struggling with the increasing demands of guests who wish to consume more and more data. Cheap hotels are unlikely to have invested in a big data pipe to keep all guests happy. Download the app ‘Hotel wifi Test’ and contribute to crowd knowledge of how good hotel wifi is. Just got used to 4G? Vodafone is already conducting trials of 4.5G to significantly increase the capacity and efficiency of its 4G network in urban areas, as well as laying the foundations for the introduction of 5G by 2020. EU regulations have been reducing roaming charges over the last few years, and earlier this year announcements were made that roaming charges would be scrapped in 2017 and all charges incurred would be the same as your home country. Critics of the ban suggest the loss of revenue for mobile phone companies could push up prices in general, including prices for non-travellers. When the draft proposals were announced, consumer groups were outraged that only 90 days of ‘free’ roaming per year would be allowed. In September 2016, the draft proposals were scrapped on the instruction of Commission President Jean-Claude Juncker and a new version was to be produced. The EU Commission said that they had been listening and now were going back to the drawing board, but roaming charges would still disappear by June 2017. BT has increased some call prices from 1st September 2016, and will be increasing network feature prices from 1st October 2016. For example, BT Business Plan increases local and mobile inland calls by 1p/min and international calls go up too and on the BT Business One Plan, local and mobile are increasing. As always, keeping up with BT plans and prices is both an art and a science. If you don’t know what your current communications contracts pricing is or what commitments you have you should carry out a contracts review. This is often only done when a reason for change arises through another project or initiative and often there are surprises. With BT these can be caused because termination charges have been increasing over the last few years. Phone book entries – when was the last time you looked in a phone book? One standard entry comes free with your line rental but many businesses historically have paid for additional entries in non-local directories, or to bold their entries. BT last increased these prices on 1st January 2016. These costs are usually small in relation to the overall bill and go unnoticed until perhaps the line associated with the number is cancelled. Often unknown though is that you are committed to pay for your entry until the next print run of the relevant directory. BT says: “If the customer cancels the entry or ceases the exchange line to which the special entry applies, he/she may be liable for charges until this time, up to a maximum of six quarterly rental payments”. WWW.EXPENSE-REDUCTION.CO.UK WWW.EXPENSE-REDUCTION.CO.UK6 7 Market Intelligence Market IntelligenceIssue No. 16.4 Issue No. 16.4

- 6. Are you getting value from your exhibition budget? Events by Alastair Baker When exhibitions don’t deliver on commercial expectations, it’s common practice to blame the exhibition organiser for not delivering the right people to your door. But it’s worth considering whether you have done everything possible to get value from your investment. Spending time, money and effort on an impressive bespoke stand will only be profitable if it is reinforced with strong promotional materials. It’s a common mistake for companies to fail to provide consistent marketing materials within their exhibition design. Even worse, some companies fail to use them at all! From brochures, to displays, to hand-outs, this is your opportunity to reinforce your brand’s messaging and promote your company through marketing they can take home. Ignore the use of promotional material and your customers will have nothing to remember you by. If you haven’t bagged the most prominent plot in the hall, you’ll need to work a little harder to stand out. A poorly lit, disengaging, unexceptional stand in a prime position will still fail to attract visitors. Produce an eye-catching stand with high- level branding, designed for optimum visibility at every angle of the hall, and you’ll entice visitors wherever in the exhibition they may be. Appealing to different senses with a variety of textures, lighting and sounds can help to immerse your customers in your stand and capture their imagination. Attracting your customers to your stand is just one part of the sales process. You then need to concentrate on giving them a superb visitor experience, whether that’s through engaging interactive displays, memorable large-scale demonstrations or, critically, well prepared and enthusiastic staff. Your team should look the part and behave professionally throughout; it’s unlikely they will do so if they have been on their feet for 24 hours over the past 2 days! Equally staff should only be seated when talking ‘one to one’ to visitors. So make sure your team has time off, and introduce fresh blood every day if possible. Make sure your available budget is being fully utilised. When did you last change your supplier? How much of the spend does your audience really see? Would the purchase of a modular display system reduce labour and transport costs, and enable you to attend more exhibitions? Keep your target market in mind at all stages of the concept, design and exhibition process. Are you looking to sell to a broad audience, or is your market a very specific, lucrative group? Combine this with committed follow-ups to leads, and you’ll ensure your exhibition experience isn’t a wasted one. WWW.EXPENSE-REDUCTION.CO.UK8 Market Intelligence Issue No. 16.4

- 7. Business Rates appeal window looming Property by Paul Giness After a two year delay, the Government is finally due to publish its Draft Rating List in October. The rating list, which applies a rateable value – which in turn determines the property rates payable – had been due in 2015, but was delayed for two years following the financial crash, by the Coalition Government. This opens the window for its new ‘Check, Challenge, Appeal’ process, which allows organisations to challenge the rateable value applied to their properties, ahead of the publication of the final Rating List in April of next year. The Valuation Office is currently collecting rental info and preparing draft valuations, and we have created a timeline depicting the key events from now until the start of the new Rating List in April 2017. Business Rates – what are they? This is the commercial version of Council Tax and applies to all non-domestic occupiers and landlords (if the property is vacant), including businesses and educational establishments. The new rateable values that will be published in October, are in preparation for the April Revaluation, which will be based on the hypothetical rent of a property at a fixed valuation date. The existing valuations are based on pre-credit crunch rents from April 2008, whilst the new List is based on rents in 2015. So, with minimal overall growth since the economy collapsed, it will be interesting to see what is calculated. Within the current Revaluation period, savings can still be obtained for payments already made between 2015 and 2017 and, where appropriate, our team can review scope for these additional savings. Check, Challenge, Appeal The Government is concerned there are too many appeals in the rating system, causing unnecessary delays. Therefore in an attempt to improve the review process, it is introducing a new ‘Check, Challenge, Appeal’ (CCA) system. The Enterprise Act provides the framework for this to take place. The aims are to provide a more streamlined and efficient system in which the key issues are identified early by the ratepayer/agent and are resolved as quickly as possible. Be warned though! The new landscape is littered with risk. Opponents of the system say there is a lack of transparency from government on how rates are calculated and that the appeals process is lengthy and cumbersome. Since the latest revaluation of business rates was enforced in 2010, there have been appeals on 590,850 of the 1.8m commercial properties in the UK eligible to pay business rates. That means around 1/3 of the invoices are challenged, and our experience tells us that you are more likely to be successful if you use a dedicated specialist who knows the process inside-out. How can ERA Property help? Both clients and prospects will likely receive a plethora of information from the authorities leading up to the Revaluation. As well as Forms of Return from the Valuation Office, we can help clients make sense of the draft Rating List and predict the impact on their future budgets. In fact, if you send us a list of your UK properties, we can produce a five year forecast for you, as well as assess the scope for a successful appeal. We will ensure that cases are sufficiently supported in order to achieve the result wanted by both parties, i.e. a reduction in rateable value, savings and where possible a refund! WWW.EXPENSE-REDUCTION.CO.UK9 Market Intelligence Issue No. 16.4

- 8. Does Brexit bring any changes to card payments? Banking & Payments by Stephen Whitlam, Paul Davidson and Paul Lucraft Since the Brexit decision was taken, most business leaders simply want clarity so key decisions are not delayed due purely to uncertainty. Because the dramatic change in card interchange costs in 2015 was an EU-led initiative and impacts directly on margins, clients have been asking us if we see the benefits being unwound in the UK – and if so, on what timescale? The simple answer is “no!” – we do not see any meaningful changes leading up to actual Brexit, nor for the medium-term of, say, five years after that - related to the UK leaving the EU. But there are already such enormous changes taking place, and inevitably that means the cost of taking card payments should be actively considered by all organisations. So, why do we think that Brexit will bring no change in the foreseeable future? Primarily because the UK Government was not only an active supporter of all aspects of the changes, but also because the spin they put on it was one of maximising the reduction in retailers’ costs. It is difficult to see them back- tracking on that as, crudely, the beneficiaries would be seen as the politically unpopular banks, and the cost would potentially fall onto consumers through the risk of increased retail prices. Secondly – whatever one’s politics – it is unlikely an alternative government would favour banks over consumers in the post-Brexit five-year horizon that we are considering. So, we are drawn to the conclusion that the primary aim of the interchange changes – that of potentially driving £750m of costs per annum out of retail prices – is going to remain. What does ERA’s Payments Team think needs to be looked out for? Credit Card costs should fall from levels seen prior to December 2015. The clearest impact of the changes has been a fall in interchange from the widely-accepted average of 0.85% of transaction size to 0.3%. Of course the acquirers have other costs to consider, but any business that has not seen the relevant tariffs fall by at least 0.5% of transaction values, needs to consider why that is the case. Debit cards are a little trickier than credit cards. Here interchange costs averaged around 8.5p per transaction for Visa Debit cards, which account for about 80% of such transactions in the UK. The changes led to a cost of 0.2% of value plus 1p, with an overall cap of 50p for secure transactions effective March 2015. That means that any business where transactions are less than £35 on average should have seen the cost of such activity fall. Debit cards have been complicated further as – effective 1st September this year – the cap is being removed. This implies that high- ticket retailers need to be really sure of their ground before proactively challenging tariffs. Equally, thought needs to go into accepting or challenging any proposed changes notified by acquirers. ERA expects the card schemes to develop and introduce other charges to replace the income lost through the interchange regime changes. Or existing “other” charges to be increased or more widely applied. The interchange environment is in a state of considerable flux just now, and the situation is not helped by the fact that not only was (is?) the IT of many of the acquirers not fully up to the task now needed, but in some instances a strategic way forward is not clear. Whilst maintaining a constant awareness of both the market and the costs faced by that market, our actions are solely with our clients’ interests in mind. We believe that any work starts with gaining a full understanding of current and planned activity, and only then seeking to negotiate changes. WWW.EXPENSE-REDUCTION.CO.UK WWW.EXPENSE-REDUCTION.CO.UK10 11 Market Intelligence Market IntelligenceIssue No. 16.4 Issue No. 16.4

- 9. Temporary Labour – asset or overhead? by Steve Stiles According to the most recent CIPD UK Labour Market report, most employers are projecting a steady-as-it-goes and ‘business as usual’ approach when it comes to recruitment. However, the indications are towards a deterioration in hiring intentions over the next few months as a result of the Brexit vote. Significant numbers of employers are also signalling higher costs, greater recruitment difficulties and lower investment in the future as a result of Brexit. Interestingly, this view is not necessarily supported by the latest Office for National Statistics UK Labour Market Report. Between January and June 2016, the number of people in work in the UK increased. There were 31.75 million people in work - 172,000 more than for January to March 2016 and 606,000 more than for a year earlier. Furthermore, a recent report by the Association of Professional Staffing Companies indicated that this increase in market demand was fulfilled by both permanent and temporary placements, with temporary job placements up 8% and permanent positions up 6% on the previous year. With such a backdrop of uncertainty, the labour market shift towards a more flexible approach to staffing, including temporary labour, is likely to continue so that companies can scale their business performance. This change is being driven by a number of factors, and for businesses the benefits are clear. Labour is one of the biggest costs for businesses and, in an uncertain economy, the last thing they want is a high headcount when orders are falling. A workforce including temporary staff enables businesses to have greater flexibility in managing changes in demand for products or services. It also enables businesses to quickly inject talent to meet specific shortfalls or competitive challenges, without incurring the costs and time delays of training. This also opens the talent pool - temporary workers can be drafted in to fill positions left open by any skills shortage. Having a more transient workforce can also keep a business innovative. New and different injections of ideas bring with them fresh thinking, new approaches to problem solving and varied experience. It can also be a screening device for potential recruits to their permanent workforce. Research findings from the UK Commission for Employment and Skills suggests a projection of strong growth in construction, information technology, health & social work and service sector positions over the next five years. These sectors are typically considerable areas for temporary labour usage. With the recent Brexit vote, the temporary labour industry is likely to evolve further. Recent changes to government legislation around minimum wages and pension contributions will increase temporary staff rates and put a further pressure on the bottom line for businesses. Typically the average cost of temporary labour to the business is greater than the equivalent permanent member of staff, so it does require an element of planning and process to ensure the contractors arrive when needed and depart once the requirement has passed. Streamlining the HR processes supporting recruitment, succession planning and internal skills development, in support of the business strategy, will also help increase staff engagement. Improving demand and supply resource forecasting processes will help reduce the reactive demand for recruitment, including temporary labour, which can sometimes lead to uncompetitive commission rates being charged. In our experience, which includes a wide range of UK and International workforce planning, ERA are well placed to provide independent advice and guidance around all aspects of recruitment with a focus on improved value for money. WWW.EXPENSE-REDUCTION.CO.UK WWW.EXPENSE-REDUCTION.CO.UK12 13 Market Intelligence Market IntelligenceIssue No. 16.4 Issue No. 16.4

- 10. Dealing with post-Brexit IT price rises Information Technology by Simon Atkinson There have been many warnings and predictions about the outcome of the Brexit vote and its ongoing consequences, both on a macro-economic level and also in more specific areas of business in the United Kingdom. For consumers of IT, whether personal or business, there are already consequences. For example, Dell introduced a double-digit price rise in the summer, blaming Brexit. HP has followed suit, paving the way for others. But why those manufacturers? The reasons are quite simple. Hardware manufacturers operate on low margins and source products form the Far East, in a market dominated by the US dollar. When the Brexit vote was confirmed, sterling fell sharply against the dollar, instantly wiping out a chunk of the margin from sales in the UK. Further margin is eroded by discounting and by the indirect sales channels favoured by many of the low margin, high volume vendors in the IT hardware space. Therefore, an adjustment had to be made to compensate for the abrupt change in circumstances – which meant raising prices. It is also worth noting that the same vendors are struggling to sell equipment more than ever before, due to the shift towards cloud adoption. This has reduced the volume of sales to corporates and even though the pound is now showing signs of recovery against the dollar, the general picture for PC manufacturers remains fairly grim. Because of this, it is unlikely prices will be reduced, even if sterling recovers fully. In any case, the mood of uncertainty surrounding Brexit is likely to continue for some time, thus discouraging discretionary investment – a further blow to them. So, it is actually far more likely we will see further price rises, rather than falls, over the next two to three years. So what can clients do about this? Well, there are three options: 1. Increase IT budgets by at least 10% to compensate for the unplanned additional cost you will have to bear. 2. Reduce expenditure to stay within the existing budget structure – in other words reduce the actual number of projects you were going to undertake. 3. Take steps to find savings in the costs paid, so that money saved can be reinvested in planned projects – that means no budget increase and no reduction in planned efforts either. The third option sounds like a utopian view. However, it is possible in some circumstances. Expense Reduction Analysts are presently running a number of IT projects with this goal in mind – and more importantly we are succeeding. Savings are being identified and/or retrieved from vendors, which is having the effect of nullifying price rises and in some cases going beyond that to create a significant net gain. This does not only apply to hardware. Software, support and services also have a part to play in optimising spend, without reducing quality, as do hosting, data centres and communications. By taking a holistic view of the IT budgetary requirement, we are able to focus in on the areas where we can make the greatest impact, delivering budgeted cash back to clients and helping them to continue necessary IT provision and investment in their businesses. WWW.EXPENSE-REDUCTION.CO.UK14 Market Intelligence Issue No. 16.4

- 11. 6 Steps to maximise your revenues from scrap metal Waste by Pete Bramhall Take control of the relationship I am often struck by how unbalanced the relationship can be between companies who produce scrap metal and the scrap merchants who buy it from them. For example, it is common for the scrap merchant to decide how much they are going to pay (per tonne) at the end of the month following collection and inform the supplier how much to invoice them. No negotiation; no prior notification. Would manufacturers sell any other product to customers on these terms?! Understand the market Of course, it is hard to negotiate effectively without knowing the market value of your scrap. Given that around 60% of UK-produced scrap is now exported to markets such as Turkey and India, it is necessary to keep abreast of both domestic and export market trends. Non-ferrous metals are traded on the London Metals Exchange, which can give rise to scrap price volatility from trading in commodity investments. Currency fluctuations can also play a part in export pricing and have clearly done so since the Brexit vote hit the value of sterling. Ensure you see the benefits of market upswings Scrap metal processors inevitably try to pass on to suppliers the full amount of each drop in price and have done so in recent months. When prices rise again they invariably try to hold on to a chunk of any increase in order to increase margins. The vast majority are able to get away with this, as most contracts are not tied into market movements. Check your weight data Another area of concern is with weight recording. Rebates are typically paid based on the weights recorded by the scrap merchant’s weighbridge and computer systems. It is important that regular auditing is carried out to minimise the chance of errors resulting from missing tickets and under-reporting of weights either through error or deceit. Whilst we aren’t suggesting that systematic fraud is commonplace, it isn’t exactly unheard of either. Keep it clean The value paid for scrap metal depends partly on the ‘grade’ of the material. Higher quality grades naturally attract higher prices. Often it is in the scrap merchant’s interests for scrap to be well segregated and both parties can benefit from this. However, sometimes they are happy to let you downgrade your material by contaminating or mixing grades together, especially if they can easily process or clean it and upgrade it themselves before selling it on. Keep it safe Theft of scrap metals, especially the more valuable non-ferrous grades, was enough of an issue a few years ago to cause the police to set up a national task force to tackle the crime. The success of this operation, helped by declining prices in the interim, means that the situation is no longer acute and headlines about cancelled trains due to theft of cables have thankfully subsided. But nevertheless this remains a significant issue. High value materials need to be kept under lock and key. WWW.EXPENSE-REDUCTION.CO.UK15 Market Intelligence Issue No. 16.4

- 12. The cost centre allocated was ‘Waste’, so Pete Bramhall conducted ERA’s no-nonsense, fully-engaged process, whilst Simon ensured a dialogue between the two for maximum clarity for the charity. And it didn’t go unnoticed. “The difference in how the two companies approached the demonstration project was stark. ERA really stood out not just for the levels of saving achieved, but the manner in which they handled the process from start to finish. That’s what led me to work with them. They were incredibly thorough, collaborative and communicative throughout and I could see they offered a truly managed service, which is exactly what I was looking for,” explains David White. Providing specialist troops on the ground Following appointment, ERA has now delivered 14 successful projects, with a further three in the pipeline and more to follow. For David, a key attribute in this successful partnership is ERA’s presentation of the very best, tailored solutions, with absolutely no pressure to commit: “Despite the fact that they get more money the more we save, there is absolutely no pressure at all from ERA – that’s very special. Not only do we have the final choice when results of a project are presented to me, there’s also no pressure to change suppliers if we don’t want to. Simon and his team come in as part of the project and benchmark everything we are buying. They really get a good grip on how much you are spending. Then, unlike other companies who just say, ‘here’s your price and we’ll take a percentage’ they remain fully engaged with you for the duration of the process. They assist with supplier transitions and they do follow-up audits to ensure you’re getting the saving you were promised. If there are problems, it’s ERA who goes back to the supplier. They basically do all the hard work so that we can get a report to see the final savings”. ERA’s client relationships don’t end with identifying the best supplier and saving costs. Each specialist manages any changes to new suppliers or improvements to services with existing providers to ensure seamless transitions. Ongoing reviews validate that the promised service levels are being met, and at ERA we pride ourselves on an open channel of communication between all parties. Trust and collaboration The level of trust and collaboration that has been built up within the business has resulted in an open book policy between ERA and Sue Ryder. So much so that David regularly provides Simon with a copy of his purchase ledger for review to identify new opportunities. Simon and the team assess the expenditure and commercial commitments in order to analyse what that spend is made up of. They identify potential savings or, where there is no or limited opportunity for savings or improvements, they recommend staying with the current suppliers and arrangements. CONTINUED FROM FRONT PAGE >>> To read the case study in full, please visit: expense-reduction.co.uk/sue-ryder/ WWW.EXPENSE-REDUCTION.CO.UK16 Market Intelligence Issue No. 16.4 WWW.EXPENSE-REDUCTION.CO.UK