1. GFAM 200 9 Ma rket O utloo k

We believe that the recession that began in

December 2007 will likely persist through

much of 2009, followed by a tepid recovery

at best. Given this timing, we expect the

capital markets to remain challenged,

making defensive positioning and bargain

hunting the major focus for our asset

allocation decisions this year.

Before we can develop that forecast further,

we need to ask deeper questions: Are we

in a “typical” cyclical recession or is the

slowdown phase of a deeper structural

change? Has the bursting of the credit

bubble coincided with a new paradigm of

savings instead of consumption? Finally,

what will be the impact of government

stimulus and the debt it entails?

G ov e r n m e n t st i m u l u s p l a n s

Government spending through fiscal

stimulus plans is often an effective countercyclical means of dealing with recessions.

The government does not directly affect

consumer spending, a key component of

the current slowdown, but it can create

spending programs that may be effective if

the multiplier effect (the ripples created in

the broader economy) is sufficient.

Currently, investors worldwide have funded

the US government’s efforts by snapping up

Treasurys at almost any yield for the safety

of principal. At some point, however, foreign

investors may see a greater need for using

their funds for their own domestic stimulus,

Chart 1. Fed Balance Sheet

2150

$ Billion

1950

1750

+$1.2t

1550

1350

1150

950

750

550

350

150

1990

035 (02/08)

1992

1994

1996

1998

2000

Genworth Financial Asset Management

2002

2004

2006

2008

2. or they may seek better yields elsewhere.

The likely effect would be some combination

of a falling dollar and rising interest rates.

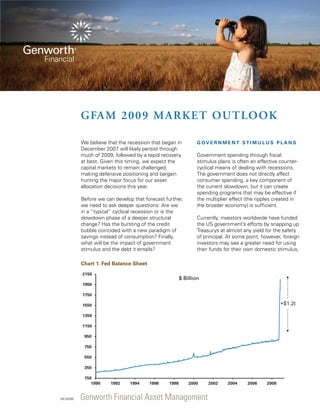

Meanwhile, the Federal Reserve has been

injecting new cash into the banking system

and buying debt in the financial markets,

including commercial paper and mortgage

related securities. This has increased the

money supply and Fed balance sheet

dramatically. (As seen Chart 1.) But when

the economy begins to turn around and

consumers and businesses are no longer

hoarding cash, the extra cash in the system

may be inflationary, sending interest rates

higher. If the Fed can extract the excess

cash from the system, inflation can likely

be avoided. The potential for higher interest

rates and higher inflation, however, must be

considered in our investment decisions.

Currently, however, the excess supply of

capital and capacity versus the demand

for finished products and services puts

the focus on deflation. Deflation can cause

consumers and business to postpone

spending, furthering the economic slow

down. As demand returns, however, the

Fed must remove the excess liquidity to

prevent inflation. In simple terms, supply

must be balanced with demand, and that is

a tricky prospect in an economy as large and

complex as that of the U.S.

The timing of these shifts is difficult to

forecast. However, while there is a strong

possibility that government bond yields

may head higher, there are two important

reasons why Treasury yields might not

rise. One is the traditional role of the U.S.

Treasury market as a safe haven investment

for investors around the globe. Recently,

investors have even accepted negative

yields on short term Treasury bills. Second,

the Fed is expanding its balance sheet to

pump money into the system, and may seek

to lower interest rates on longer term bonds

by buying US Treasurys.

The likely scenario is that investors will

eventually begin to migrate from safe-haven

instruments into those with higher yields

and credit risk. (We have already seen late in

2008 that foreign demand for longer dated

US government and agency bonds has

waned, with net selling by foreign holders.)

At that point, the Fed may want to remove

some of this money and sell securities from

its balance sheet to accomplish that task.

Meanwhile, the Treasury will likely continue

to issue securities for a fiscal stimulus

plan that will take at least two years to

accomplish its objectives, also putting

more bond supply on the market. (The

infrastructure and other projects floated by

the Obama administration will take some

time to plan, let alone implement.) This

balancing act likely will be resolved with

credit spreads contracting as Treasury yields

rise to a price that will clear the market,

the dollar falling, and corporate bond yields

remaining flat or even declining a little

if investors once again are comfortable

investing in corporate debt.

Consumers turn from

c o n s u m p t i o n t o s av i n g s

There is an added nuance to address in our

2009 Outlook. Consumers have begun to

save more and pay down debt. Every dollar a

consumer saves is a dollar that is not spent,

and that unspent dollar has a multiplier effect

in the real economy. Therefore, increased

savings may keep a lid on economic growth

– but it may help keep a lid on interest rates

as some of the savings are invested in fixed

income instruments.

The shock of the dot com bubble bursting,

followed by that of the housing bubble

bursting, has perhaps left an indelible mark

in the psyche of American consumers.

Now, with assets having fallen in value and

access to credit scarce or unaffordable,

future consumption is much less likely to be

supported by increasing debt or drawing on

inflated asset values. (See Chart 2) Add in

a generational shift as baby-boomers retire

and leave their peak consumption years

behind, and the shift from consumption to

savings may become more pronounced.

What does this mean for the investor?

Money formerly put toward discretionary

spending may be redirected to savings,

which in turn may lower the cost of capital

for corporations seeking to fund investments

in property, plants or equipment. However,

as the American consumer scales back on

consumption (as seen in Chart 3), profit and

sales growth may recede to a rate closer to

that of nominal GDP (with adjustments for

things like foreign trade). Corporate profits

per share will likely be lower, with future

returns to equity investors more in line with

nominal GDP growth. This is in contrast to

3. Chart 2. Household Borrowing

1400

1200

$ Billions

(Year-over-Year Change)

Chart 3. Discretionary Spending Growth

200

Annual $ Billions

160

1000

120

800

80

600

40

400

0

200

-40

0

-80

-200

-120

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

the higher returns seen during the 1980’s

and 1990’s, a period of strong growth, falling

interest rates, and healthy P/E multiples.

Slower global trade, whether from weak

demand or government policy, also affects

cross border capital flows. As we buy

Chinese goods, they send the dollars back to

buy US Treasurys. This has helped fund our

budget deficit, but now that we are importing

less, they are sending fewer dollars back to

buy our government debt. Given a backdrop

of massive issuance of US Treasurys to

finance not only the existing trillion-dollar-plus

deficit but also the stimulus plan, we must

hope that we have enough buyers.

A vulnerable corporate profit outlook

and heightened equity volatility point to

alternatives such as investment grade

bonds that offer attractive yields relative to

Treasurys. Care must be taken, however, to

monitor signs of excess money supply and

the resultant inflation that could erode fixed

income returns.

T h e g l o b a l i m pa c t: c a s h

f low s

The recession is not confined to the U.S.;

Europe and Japan are also in a significant

and serious recession, with demand for

exports waning and manufacturers cutting

production. The ripple effects are then

seen in emerging markets that supply the

commodities or export finished goods to

developed markets. Even China is proposing

a fiscal stimulus plan to help employ the

people migrating into the cities by building

out infrastructure (which it certainly needs).

This internal focus around the globe means

a few things for trade and international

capital flows.

Countries import less due to weaker

local demand. Other countries respond

by devaluing their currency to make their

exports more attractive, which inspires

more aggressive responses as countries

seek to promote their trade and defend

against imports. If this is carried to the

extreme, trade wars may develop and

protectionism may result. Protectionism is a

highly dangerous element that can subvert

economic growth globally.

On a different front, a devaluing of the

dollar may present a mixed blessing for the

US economy. On one hand, it will make

imports more expensive and decrease our

purchasing power abroad, ultimately leading

to an increase in inflation. On the flip side,

it will generally make US companies more

competitive overseas, boosting exports.

These forces working in tandem would

continue to narrow the U.S. trade deficit.

The price of oil, difficult to forecast because

of many variables including geopolitical risk,

is an important wildcard in the trade deficit

equation.

Another effect of a falling dollar is that it

will enhance the profitability of investments

made abroad when repatriated into US

dollars. Should US investors become

concerned about the potential for rising

US Treasury interest rates later in 2009,

investing in fixed income instruments

overseas may be appealing, especially when

factoring in the currency gains from a falling

dollar. While overseas equity markets will

likely face similar challenges as those of the

US, at some point entry to those markets

may be compelling. In the US alone a

mountain of cash is sitting on the sidelines

that may be deployed in any number of

instruments as the investing climate shifts

from risk aversion to risk taking.

4. Lo o k i n g a h e a d

When will a shift in risk attitude happen?

The capital markets typically begin

recovering four to eight months before the

real economy, and we do believe that we

are perhaps halfway through the current

market difficulties. But we also believe that

there are several preconditions before the

economy recovers, including:

• Credit must flow smoothly through the

economy, so that homebuyers can get a

mortgage or a business can invest in a

new plant or equipment.

• Housing prices can therefore stabilize,

even if prices do not rebound for several

years.

• That will in turn renew consumer

confidence in the economy and markets,

sparking consumer spending…

• ... which will in turn bring about rising

employment. This is not a precondition for

the markets to recover, but it is still very

important nonetheless.

We do not see these conditions being met

until 2010, which suggests a potential for

market recovery in mid-2009. The rebound

off the November low may ultimately be

seen as a bear market rally spurred by

optimistic hopes regarding federal fiscal

stimulus spending. Tax cuts are temporary,

however, and are likely to be saved

rather than spent. Also, investments in

infrastructure require considerable planning

and overcoming logistical hurdles before

any money is actually dispersed. It might

be 2010 before a significant amount of the

stimulus actually reaches the economy.

While we believe opportunities may present

themselves at various points during 2009

we are positioned realistically for what we

believe to be another challenging year. We

favor companies with strong balance sheets,

demonstrable earnings, and stable cash flow

– in a word, “quality”

.

We are also attracted to securities that rank

higher up on the corporate structure, such

as investment grade corporate bonds, which

we may favor over the equity of the same

issuer. Yields are compelling in our view.

The chart (Chart 4) shown here isolates

the additional yield for Baa-rated corporate

debt over Treasurys, demonstrating a

widening spread in favor of corporate debt

in recent months. And, as debt ranks higher

than equity on corporate balance sheets,

investment grade bonds may offer an

additional measure of safety and potentially

less volatility relative to equities.

We are beginning to see potential

opportunities in emerging economies

with developing consumer societies less

dependent on exports to a weakened

industrialized world. In addition to, or

instead of, investing directly in emerging

markets, we may invest client assets in

companies that export to them, such as the

Domestic Export mandate. We may also

revisit commodities as a way to play the

infrastructure stimulus sometime in 2009

(This will require careful consideration as

the tangible effects of building programs on

commodities may be offset by continued

global economic weakness.) We also may

place greater emphasis on convertible

bonds, which can offer equity upside in

addition to the income characteristics of

bonds.

Chart 4. BAA Bond Yield minus T-Bill Yield

925

Yields on corporate debt very attractive compared to Treasurys

840

755

670

585

500

415

330

245

160

75

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008