Recomendados

Recomendados

Más contenido relacionado

Similar a Breakeven Formula Derivation

Similar a Breakeven Formula Derivation (17)

Más de TatianaMajor22

Más de TatianaMajor22 (20)

Último

Último (20)

Breakeven Formula Derivation

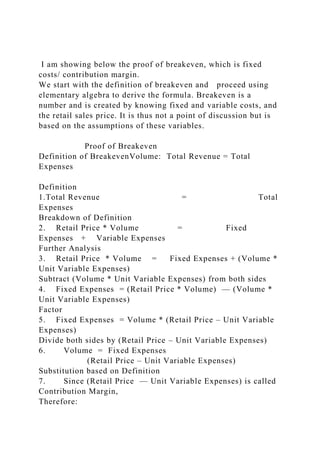

- 1. I am showing below the proof of breakeven, which is fixed costs/ contribution margin. We start with the definition of breakeven and proceed using elementary algebra to derive the formula. Breakeven is a number and is created by knowing fixed and variable costs, and the retail sales price. It is thus not a point of discussion but is based on the assumptions of these variables. Proof of Breakeven Definition of BreakevenVolume: Total Revenue = Total Expenses Definition 1.Total Revenue = Total Expenses Breakdown of Definition 2. Retail Price * Volume = Fixed Expenses + Variable Expenses Further Analysis 3. Retail Price * Volume = Fixed Expenses + (Volume * Unit Variable Expenses) Subtract (Volume * Unit Variable Expenses) from both sides 4. Fixed Expenses = (Retail Price * Volume) — (Volume * Unit Variable Expenses) Factor 5. Fixed Expenses = Volume * (Retail Price – Unit Variable Expenses) Divide both sides by (Retail Price – Unit Variable Expenses) 6. Volume = Fixed Expenses (Retail Price – Unit Variable Expenses) Substitution based on Definition 7. Since (Retail Price — Unit Variable Expenses) is called Contribution Margin, Therefore:

- 2. Breakeven Volume = Fixed Expenses / Contribution Margin NAME_______________________________________________ __ DATE ____________ 1. Explain some of the economic, social, and political considerations involved in changing the tax law. 2. Explain the difference between a Partnership, a Limited Liability Partnership (LLP) and a Limited Liability Company (LLC). In each structure who has liability? 3. How is “control” defined for purposes of Section 351 of the IRS Code? 4. What are the advantages and disadvantages of using debt in a firm’s capital structure? 5. Under what circumstances is a corporation’s assumption of liabilities considered boot in a Section 351exchange? 6. What are the tax consequences for the transferor and transferee when property is transferred to a newly created corporation in an exchange qualifying as nontaxable under Section 351? 7. Why are corporations allowed a dividend-received deduction? What dividends qualify for this special deduction? 8. Provide 3 examples of a Constructive Dividend. Are these Constructive Dividends taxable? 9. Discuss the tax consequences of a new Partnership Formation and give details to gain and losses and basis? 10. Provide 2 similarities and 2 differences when comparing

- 3. Sections 351 and 721 of the IRS Code. 11. What is the difference between inside and outside basis with a partnership? 12. ABC Partnership distributes $12,000 of taxable income to partner Bob and $24,000 of tax-exempt income to Partner Bob. As a result of these two distributions, how does Bob’s basis change? 13. On January 1, Katie pays $2,000 for a 10% capital, profits, and loss interest in a partnership, which has recourse liabilities of $20,000. The partners share economic risk of loss from recourse liabilities in the same way they share partnership losses. In the same year, the partnership incurs losses of $6,000 and the recourse liabilities increase by $5,000. Katie and the partnership use a calendar tax year-end. What is Katie’s basis at year-end? 14. Stephen and Baily form an equal partnership. Stephen makes a cash contribution of $60,000 and a property contribution (adjusted basis of $120,000; fair market value of $130,000) in exchange for her interest in the partnership. Baily contributes property (adjusted basis of $11,000; fair market value of $250,000) in exchange for his partnership interest. What is Stephen and Bailey’s basis in the new partnership? 15. Thomas and Richard formed the Happy Go Lucky Partnership four years ago. Because they decided the company needed some expertise in multimedia presentations, they offered Sarah a 1/3 interest in partnership capital and profits if she would come to work for the partnership. On July 1 of the current year, the unrestricted partnership interest (fair market value of $225,000) was transferred to Sarah. How should Sarah treat the receipt of the partnership interest in the current year? Remember that Sarah is just contributing her services! 16. Jimmy had investment land that he purchased in 1995 for

- 4. $85,000. Two years ago, when the land was contributed to the FUN partnership, the FMV was $40,000. The land is inventory in the lands of the FUN partnership. The partnership then sells the land in the current year for $36,000. What is the partnership’s recognized loss. 17. Gabriella, a widow, has an extensive investment portfolio that has appreciated in value. Starting in 2012, she initiates a policy of making annual gifts of securities to her grandchildren who are attending college. Evaluate Gabriella’s policy in terms of what she should do with regards to Federal Estate Tax and Gift Tax. 18. Harriet and Josh are husband and wife and have several adult children. Harriet has a net worth in excess of eight million dollars, while Josh’s assets are negligible. Suggest several planning procedures that will maximize the use of estate exemption equivalents (i.e., bypass amounts) in transferring Harriet’s wealth to the children under the following assumptions. Remember that the 2014 exemption for estate taxes is $5,250,000. 19. What is the Unified Tax Credit and how is it beneficial with wealth transfer? 20. Samuel is considering the purchase of a $10,000,000 life insurance policy for the benefit of his 2 children if case anything happens to him. From an Estate Planning what is the best use of a Life Insurance Policy to minimize Estate Taxes?

- 5. 21. Describe two types of trusts that can be used if a Grantor has charitable intent and wants to provide for that charity after death. 22. If grandmom gives you $14,000 in cash in 2014 so that she can use her annual exclusion, what are the tax consequences to you? . . 23. Suzanne and Philip are married and have a 9-year old grandson, Basil. They want to contribute to a § 529 plan on behalf of Basil’s’s education. For 2009, what is the maximum amount they can transfer to the plan without making a taxable gift? Assume Basil will be attending a 5 year university. 24. Melissa established a revocable trust with son Gilbert as remainder beneficiary. The value of assets was $80,000 when the trust was created and $12,500,000 when Melissa died. Based on these facts, what is included in Melissa’s estate 25. What advice would you give a wealthy family with 5 children and a prosperous family business so that they can do successful tax planning? Give me 5 planning ideas. 26. Clifford is an 80 year old wealthy business man who will probably live another 10 years. He has vast wealth including a 10 million home in Florida and $5mm worth of Apple common stock. He has a loving family including 3 children and 5 grandchildren and he is very much involved with with his charity work with the American Red Cross. What estate

- 6. planning techniques would you recommend to him based on what we discussed in class? Internal Use Only