Profitability and Cost Structure Analysis: External Data Analysis Frameworks

This Slideshare presentation is a partial preview of the full business document. To view and download the full document, please go here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-1703 DOCUMENT DESCRIPTION Profitability and cost structure analysis provides many invaluable insights. Obvious examples include identifying profitable products and projects and identifying key cost driving activities and resources--which lead to better strategic decisions. There are a number of business frameworks to conduct profitability and cost structure analysis. In this consulting training series, we will 4 common frameworks split into 2 categories: 1 External Data Analysis 2. Internal Data Analysis This deck will focus on External Data Analysis only. It also includes an overview to Profitability and Cost Structure Analysis. ABOUT FLEVYPRO FlevyPro is a subscription service for on-demand business frameworks and analysis tools. FlevyPro subscribers receive access to an exclusive library of curated business documents—business framework primers, presentation templates, Lean Six Sigma tools, and more—among other exclusive benefits.

Recomendados

Recomendados

Más contenido relacionado

Más de Flevy.com Best Practices

Más de Flevy.com Best Practices (20)

Último

Último (20)

Profitability and Cost Structure Analysis: External Data Analysis Frameworks

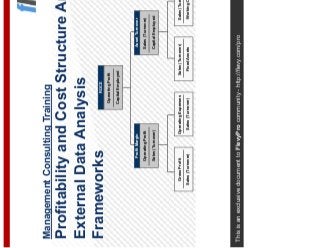

- 1. This is an exclusive document to FlevyPro community - http://flevy.com/pro Management Consulting Training Profitability and Cost Structure Analysis: External Data Analysis Frameworks ROCE Operating Profit Capital Employed Gross Profit Sales (Turnover) Operating Expenses Sales (Turnover) Sales (Turnover) Fixed Assets Sales (Turnover) Working Capital Profit Margin Asset Turnover Sales (Turnover) Capital Employed Operating Profit Sales (Turnover)

- 2. 2This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Contents Cost Management Overview Profitability Analysis Cost Structure Analysis The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 3. 3This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability and cost structure analysis provides many invaluable insights—there are numerous frameworks to conduct these analyses Presentation Overview Profitability and cost structure analysis provides many invaluable insights. Obvious examples include identifying profitable products and projects and identifying key cost driving activities and resources—which lead to better strategic decisions. There are a number of business frameworks to conduct profitability and cost structure analysis. In this consulting training series, we will 4 common frameworks split into 2 categories: External Data Analysis Internal Data Analysis This deck will focus on External Data Analysis only. It also includes an overview to Profitability and Cost Structure Analysis. The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 4. 4This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability and cost analysis are clearly linked—the level of analysis will depend on access to financial information Profit Formula If we had perfect information, we could calculate the individual profitability of every item sold to every customer through every channel. Profit = Revenue - Cost How you define ‘costs’ will define which profitability you are measuring: – E.g. Gross profit is turnover less costs of good sold The accuracy with which you can measure or estimate revenues and costs will define how insightful your analysis can be: – Often we only have access to publicly available information, which is presented at the Group level in broad categories – With internal data or management information, we can do much more meaningful and insightful analysis The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 5. 5This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro With access to internal information, we can conduct a much greater range of analysis General Ledger Overview Information held on General Ledger systems—this is the system that track revenue and costs at the most detailed level within the company: – “Journal entries” are posted to the general ledger The General Ledger is usually broken down by department and by cost/revenue type Examples of cost types: – Revenues from individual customers, rebates, trade discounts, etc – Salary, pension, national insurance costs – Utility costs – Building rental / insurance / maintenance – Consumables / Stationary – Raw material costs, etc. The financial accounts (including Profit and Loss statement) are built up from this system. The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 6. 6This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Our usual starting point for profitability analysis is the annual profit and loss statement Typical Profit and Loss Account Structure FOCUS OF OUR ANALYSIS Turnover - Cost of Sales Gross Profit - Distribution Costs - Administrative Expenses Operating Profit + Other operating income Operating Profit including share of joint ventures and associates + Profit on disposal of businesses Profit on ordinary activities before interest - Interest Payable - Tax Payable Profit on ordinary activities after tax + Minority Interests +/- Extraordinary items Profit for financial year The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 7. 7This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro The type of analytics we can do will depend on the available sources of our data Data Sources Lack of data should not constrain us from being creative—we can usually apply all of these frameworks with limited data to identify meaningful insights. Internal DataExternal Data Data Sources: − Annual Reports − Brokers Reports − Industry Journals / Studies Type of Analyses: − Profitability − Cost Structure Data sources: − Company management accounts − General Ledger Type of Analyses: − Cost Drivers − Activity Based Management The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 8. 8This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Contents Cost Management Overview Profitability Analysis Cost Structure Analysis The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 9. 9This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Market value is influenced by both financial & non-financial performance & the recognition of intangible value drivers Introduction to Profitability Analysis OVERVIEW & INSIGHTS This is an analysis of company’s or business unit’s profitability Can use various ratios to examine underlying profitability: − Profit Margins − ROCE Complete graphical outputs to review relative profitability: − Over time − Between units Can also form the basis of economic models to forecast future performance and value It helps us understand how well companies are performing Establish consistent comparisons between companies, identifying further areas for study STRENGTHS Allows high level identification of performance Quickly allows identification of areas of further investigation LIMITATIONS Limited real insight into underlying issues—only starting point for real analysis The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 10. 10This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability Analysis – Illustrative Output Regus’ EBIT, 1997-2000, vs. HQ’s EBIT, 1999-2000a (£m) -4.6 -15.2 -43 12.412.4 26.2 -50 -25 0 25 50 75 1997 1998 1999 2000 HQ Regus Source: Regus’ Annual Report, 2000; David O’Neill, “Frontline Capital Group”, William Blair & Company, 14/1200; www.regus.com, 20/09/01. a. Converted from $ using average 1999 rate £1 = $1.6164, average 2000 rate £1 = £1.5258 (International Financial Statistics, IMF, January 2001, 2000 = estimated). b. Revenue divided by number of business centres at end 2000 (HQ = 470, Regus = 335). The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 11. 11This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability Analysis – Illustrative Output Source: Aer Lingus Group Annual Reports and Accounts; British Airways Annual Reports and Accounts; FAME. Operating Margin, % 3.5 6.3 2.4 1.8 -4.2 5.5 3.4 5.6 7.1 8.6 9.4 6.5 0.8 0.5 -0.4 0.3 1.6 -5 0 5 10 1991 1992 1993 1994 1995 1996 Aer Lingus British Airways British Midland The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 12. 12This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability Analysis – Illustrative Output Note: Exceptional items in 1993 amount to over IR£136m including provisions for restructuring and the revaluation of GPA shares. Source: Aer Lingus Group Annual Reports and Accounts, 1991-1996; 1993 figures as restated; 1994 figures scaled to compensate for 21 month accounting period. Group Profit (IR£m) 38.6 27.4 15.7 -34.2 19.9 49.8 41.8 27.6 8.3 -11.8 -191.1 -74.2 15.0 32.0 -200 -150 -100 -50 0 50 1990 1991 1992 1993 1994 1995 1996 Operating Profit Profit after Tax and Exceptional Items The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 13. 13This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability Analysis – Illustrative Output Source: Aer Lingus Group Annual Reports and Accounts, 1991-1996; 1993 figures not restated; 1994 figures scaled to compensate for 21 month accounting period. Operating Profit by Division (IR£m) -16.8 -16.2 -22.9 36.6 43.6 42.2 44.2 31.8 23.7 4.1 -3.4 -0.4 0.8 27.4 15.7 41.8 40.240.6 -30 -20 -10 0 10 20 30 40 50 1991 1992 1993 1994 1995 1996 Air Transport Airline Services and Other Total Operating Profit The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 14. 14This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Return on capital employed (ROCE) is a key measure of a company’s underlying performance ROCE Formula Note: Capital employed is usually taken at year end, as this reflects conservative view; it may be taken as average of capital employed at beginning and end of year—analyst discretion is need; Note: Telenor define ROCE as (PBT + financial expenses)/Average (total assets – non-interest bearing debt) a. Source: “The Meaning of Company Accounts”, Reid and Myddelton, 1992. b. Clear definitions are required for what items are included or excluded; consistency is paramount. Return on Capital Employed (ROCE) = Operating Profit (PBIT) Capital Employed (Net Operating Assets) DEFINITION / FORMULAa Where… • Operating Profit (PBIT) = Gross Profit – Operating Expenses • Capital Employed (Net Operating Assets) = Fixed Assets + Net Working Capital Return on capital employed (ROCE) is also known as return on net (operating) assets (RONA)b. The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 15. 15This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Measuring ROCE can also provide key insight for many management decisions ROCE Overview However, there are lots of alternative measures of profitability—Return on Equity (ROE), Risk adjusted Return on Capital (RAROC), etc. ROCE is an important measure of profitability: − Reflects return to all stakeholders investing capital in company. − A low return on capital employed can easily be wiped out in a downturn. − ROCE serves as a guide to potential investment or acquisition: If potential ROCE isn’t attractive, investment/acquisition should be avoided. − A consistently low ROCE for any division/business unit suggests it could be a candidate for disposal if not part of core business. The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 16. 16This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Breaking ROCE to its constituent ratios allows us to focus on real drivers of performance ROCE Ratios ROCE Operating Profit Capital Employed Gross Profit Sales (Turnover) Operating Expenses Sales (Turnover) • Materials • Labour • Overheads • R&D • Distribution • Administration Sales (Turnover) Fixed Assets Sales (Turnover) Working Capital • Land and buildings • Plant machinery • Stocks • Debtors • Cash • Trade creditors Profit Margin Asset Turnover Sales (Turnover) Capital Employed Operating Profit Sales (Turnover) The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 17. 17This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Profitability Analysis – Illustrative Output Source: Aer Lingus Group Annual Reports and Accounts; British Airways Annual Reports and Accounts; FAME. Return on Capital Employed, % 2.4 5.4 2.0 1.3 -3.3 5.0 6.2 6.9 7.0 9.2 10.1 7.5 8.9 4.8 -3.0 1.1 8.4 -5 0 5 10 1991 1992 1993 1994 1995 1996 Aer Lingus British Airways British Midland The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 18. 18This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro The type of analytics we can do will depend on the available sources of our data Tips Hints and PitfallsPotential Insights Long-term trends in company performance Outcomes of strategic decisions— pursuing low cost strategies, moving up-scale Intra-company comparisons Compare like with like: − Adjust data to ensure consistency of definitions—profitability, capital employed, etc. Complete analysis on a spreadsheet— it will save time later and will ensure error free calculations Beware exceptional items—understand what they are for and make judgments as to their materiality The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 19. 19This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Contents Cost Management Overview Profitability Analysis Cost Structure Analysis The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 20. 20This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Cost Structure Analysis is a way to intuitively visualize a company’s cost structure—and the relative magnitudes of the cost components/drivers Introduction to Cost Structure Analysis OVERVIEW & INSIGHTS This framework graphically presents a company’s cost structure Builds cost bars taking account of: The various components of the cost structure The importance (relative or in absolute terms) of the components in the cost structure Understand where revenues, costs and profits are incurred Establish comparisons between cost structures for: − A product/business over time − A product/business in each of several companies − Several product lines in the same company for one time period STRENGTHS Allows a quick appreciation of trends and differences. Provides a homogeneous basis for comparison. LIMITATIONS None The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 21. 21This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Cost Structure for One Product over Time Cost Structure Analysis – Illustrative Output 0 20 40 60 80 100 1977 1979 1981 1983 0 20 40 60 80 100 Company A Company B Client Company C 0 20 40 60 80 100 120 Product A Product B Product C Product D Materials Advertising Sales R&D Annual sales ($mm) Percentage of total sales 100 19 120 22 150 28 170 31 Cost components as percent of sales Current Dollars Current Dollars Current Dollars Cost Structures for Same Product in Different Companies Cost Structure for Different Products in One Company The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 22. 22This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Cost Structure Analysis – Illustrative Output Cost Categories as a Percentage of Sales, 1996 - 2000 (%) 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1996 1997 1998 1999 2000 Operating Margin Administrative Costs Distribution Selling Costs Cost of Goods Sold The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 23. 23This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro When comparing different cost structures and drawing insights, make sure you are comparing “apples to apples” Tips Hints and PitfallsPotential Insights Assesses cost drivers: − Helps identify which cost components have increased or decreased the most − Triggers questions for further research and analysis Identifies potential areas for value differentiation Do: − Make sure you use correct measures of a company’s costs (especially with costs shared among products or business units) − Check accuracy of competitors’ data − Consider pure play benchmarks from other markets if competitor example not available Don’t: − Compare competing products that are not truly comparable The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 24. 24This document is an exclusive document available to Flevy Pro members - http://flevy.com/pro Flevy (www.flevy.com) is the marketplace for premium documents. These documents can range from Business Frameworks to Financial Models to PowerPoint Templates. Flevy was founded under the principle that companies waste a lot of time and money recreating the same foundational business documents. Our vision is for Flevy to become a comprehensive knowledge base of business documents. All organizations, from startups to large enterprises, can use Flevy— whether it's to jumpstart projects, to find reference or comparison materials, or just to learn. Contact Us Please contact us with any questions you may have about our company. • General Inquiries support@flevy.com • Media/PR press@flevy.com • Billing billing@flevy.com The content on this slide has been partially hidden. FlevyPro members can download the full document here: http://flevy.com/browse/flevypro/profitability-and-cost-structure-analysis-external-data-analysis-frameworks-170 3

- 25. 1 Flevy (www.flevy.com) is the marketplace for premium documents. These documents can range from Business Frameworks to Financial Models to PowerPoint Templates. Flevy was founded under the principle that companies waste a lot of time and money recreating the same foundational business documents. Our vision is for Flevy to become a comprehensive knowledge base of business documents. All organizations, from startups to large enterprises, can use Flevy— whether it's to jumpstart projects, to find reference or comparison materials, or just to learn. Contact Us Please contact us with any questions you may have about our company. • General Inquiries support@flevy.com • Media/PR press@flevy.com • Billing billing@flevy.com