Financial Cartography - Center for Financial Research

•Descargar como PPT, PDF•

1 recomendación•554 vistas

This document summarizes a presentation given by Dr. Kimmo Soramäki on financial cartography and mapping systemic risk and financial markets. The presentation discusses how existing economic models failed during the financial crisis and the need for better tools to understand financial linkages and systemic risk. It then outlines different mapping techniques like heat maps, asset trees, networks, and dimensional reduction techniques that can be used to visualize complex financial data and reduce dimensionality to aid decision making. Examples are provided mapping markets around the collapse of Lehman Brothers.

![“When the crisis came, the serious limitations of existing

economic and financial models immediately became apparent.

[...]

As a policy-maker during the crisis, I found the available

models of limited help. In fact, I would go further: in the face of

the crisis, we felt abandoned by conventional tools.”

in a Speech by Jean-Claude Trichet, President of the

European Central Bank, Frankfurt, 18 November 2010

2](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recomendados

Recomendados

Más contenido relacionado

Similar a Financial Cartography - Center for Financial Research

Similar a Financial Cartography - Center for Financial Research (20)

Más de Kimmo Soramaki

Más de Kimmo Soramaki (16)

Último

Último (20)

Financial Cartography - Center for Financial Research

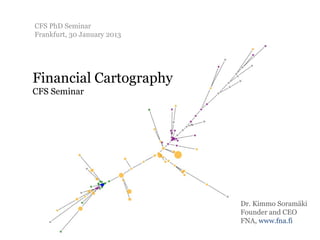

- 1. CFS PhD Seminar Frankfurt, 30 January 2013 Financial Cartography CFS Seminar Dr. Kimmo Soramäki Founder and CEO FNA, www.fna.fi

- 2. “When the crisis came, the serious limitations of existing economic and financial models immediately became apparent. [...] As a policy-maker during the crisis, I found the available models of limited help. In fact, I would go further: in the face of the crisis, we felt abandoned by conventional tools.” in a Speech by Jean-Claude Trichet, President of the European Central Bank, Frankfurt, 18 November 2010 2

- 3. We did not have maps … 3

- 4. Eratosthenes' map of the known world4 c. 194 BC

- 5. … but what are maps “A set of points, lines, and areas all defined both by position with reference to a coordinate system and by their non-spatial attributes” Data is encoded as size, shape, value, texture or pattern, color and orientation of the points, lines and areas – everything has a meaning Political map of Europe 5

- 6. … but what are maps (contd.) Cartographer selects only the information that is essential to fulfill the purpose of the map Maps reduce multidimensional data into a two dimensional space that is better understood by humans Maps are intelligence amplification, they aid in decision making and build Map by John Snow showing the clusters of cholera cases in the London epidemic of 1854 intuition 6

- 7. I. Mapping II. Mapping Systemic Risk Financial Markets 7

- 8. Systemic risk ≠ systematic risk News articles mentioning “systemic risk”, Source: trends.google.com The risk that a system composed of many interacting parts fails (due to a shock to some of its parts). In Finance, the risk that a disturbance in the financial system propagates and makes the system unable to perform its function – i.e. allocate capital efficiently. Not: Domino effects, cascading failures, financial interlinkages, … -> i.e. a process in the financial network 8

- 9. Network Theory can be to Financial Maps what Cartography is to Geographic Maps Main premise of network theory: Structure of links between nodes matters To understand the behavior of one node, one must analyze the behavior of nodes that may be several links apart in the network Topics: Centrality, Communities, Layouts, Spreading and generation processes, Path finding, etc. 9

- 10. Network aspect is an unexplored dimension of data e Tim Variables Observations 10

- 11. First Maps Fedwire Interbank Payment Network, Fall 2001 Around 8000 banks, 66 banks comprise 75% of value,25 banks completely connected Similar to other socio- technological networks Soramäki, Bech, Beyeler, Glass and Arnold (2007), M. Boss, H. Elsinger, M. Summer, S. Thurner, The Physica A, Vol. 379, pp 317-333. network topology of the interbank market, Santa See: www.fna.fi/papers/physa2007sbagb.pdf Fe Institute Working Paper 03- 11 10-054, 2003.

- 12. More Maps: Federal Funds 1997 - 2006 Source: Bech, M.L. and Atalay, E. (2008), “The Topology of the Federal Funds Market”. ECB Working Paper No. 986. • 2600 loans worth $335 billion per day • First Circle: 165 Second Circle: 271 Rest: 42 12

- 13. More Maps: Italian money market Italian (very small) Italian (small) Italian (large) Foreign Source: Iori G, G de Masi, O Precup, G Gabbi and G Caldarelli (2008): “A network analysis of the Italian overnight money market”, Journal of Economic Dynamics and Control, vol. 32(1), pages 259-278 13

- 14. More Maps: DebtRank August 2007 to April 2008 October 2008 to April 2010 Nodes: Financial institutions Source: Battiston et al, Nature Links: Impact of an institution to another Scientific Reports 2-54, 2012 Nodes closer to center are more important (as are big and red) 14

- 15. Where are we today? Regulatory response to recent financial crisis was to strengthen macro-prudential supervision with mandates for more regulatory data “Big data” and “Complex Data”-> Providing tools and challenge to understand, utilize and operationalize the data (network is fictional) Financial Networks are starting to get their own literature and metrics different from Case: Oversight Monitor at Norges Bank other fields of Network Theory The monitor will allow the identification of systemically important banks and evaluation of the impact of bank failures on the system Intraday Liqudidy Network -example 15

- 16. I. Mapping II. Mapping Systemic Risk Financial Markets 16

- 17. Outline Purpose of the maps – Identify price driving themes and market dynamics – Reduce complexity – Spot anomalies – Build intuition The maps: Heat Maps, Trees, Networks and Sammon’s Projections Based on asset correlations or tail dependence These methods are showcased for visualizing markets around the collapse of Lehman Brothers 17

- 18. Collapse of Lehman Lehman was the fourth largest investment bank in the US (behind Goldman Sachs, Morgan Stanley, and Merrill Lynch) with 26.000 employees At bankruptcy Lehman had $750 billion debt and $639 billion assets Collapse was due to losses in subprime holdings and inability to find funding due to extreme market conditions Is seen as a divisive point in the 2007-2009 financial crisis 18

- 19. The Data Pairwise correlations of return on 118 global assets in 4 asset classes 9870 data points per time interval Time windows 2 months before and 2 months after Lehman collapse 19

- 20. i) Heat Maps January Corporate 2007 Bonds FX Rates Government Bond Yields Correlation -1 Stock Exchange 0 Indices +1 20

- 21. January 2007 t-2 t-1 Corporate Bonds FX Rates Government Bonds Stocks t+1 t+2 Corporate Bonds FX Rates Government Bonds Stocks 21

- 22. ii) Asset Trees Originally proposed by Rosario Mantegna in 1999 Used currently by some major financial institutions for market analysis and portfolio optimization and visualization Methodology in a nutshell 1. Calculate (daily) asset returns 2. Calculate pairwise Pearson correlations of returns 3. Convert correlations to distances 4. Extract Minimum Spanning Tree (MST) 5. Visualize (as phylogenetic trees) 22

- 23. Minimum Spanning Tree A spanning tree of a graph is a subgraph that: 1.is a tree and 2.connects all the nodes together Length of a tree is the sum of its links. Minimum spanning tree (MST) is a spanning tree with shortest length. MST reflects the hierarchical structure of the correlation matrix

- 24. Demo: Asset Trees Color of node denotes asset class: Dow Jones Size of node reflects volatility (variance) of returns Ireland 10 year Links between nodes reflect government bond 'backbone' correlations EMU Corporate AAA, 1-3 years - short link = high correlation - long link = low correlation EUR/USD Click here for interactive visualization 24

- 25. Correlation filtering PMFG Balance between too much and too little information, signal vs noise One of many methods to create networks from correlation/distance matrices –PMFGs, Partial Correlation Networks, Influence Networks, Granger Causality, Influence Network NETS, etc. New graph, information-theory, economics & statistics -based models are being actively developed 25

- 26. iii) NETS • Network Estimation for Time- Series • Forthcoming paper by Barigozzi and Brownlees • Estimates an unknown network structure from multivariate data • Based on partial correlations • Captures both comtemporenous and serial dependence (partial correlations and lead/lag effects) 26

- 27. iv) Sammon’s Projection Proposed by John W. Sammon in IEEE Transactions on Computers 18: 401–409 (1969) A nonlinear projection method to map a high dimensional space onto a space of lower dimensionality. Example: Iris Setosa Iris Versicolor Iris Virginica 27

- 28. Demo: Sammon Projection EMU Corporate AAA, 1-3 years Color of node denotes asset class: Dow Jones Size of node reflects volatility Ireland 10 year (variance) of returns government bond Distance between nodes reflects EUR/USD similarity of correlation profiles - close = similar - far apart = different Click here for interactive visualization 28

- 29. Tail dependence • Correlation is a linear dependence. The same visual maps can be extended to non-linear dependences. • Joint work with Firamis (Jochen Papenbrock) and RC Banken (Frank Schmielewski), see www.extreme-value-theory.com • Instead of correlation, links and positions measure similarity of distances to tail losses Tail Tree Tail Sammon (Click here for interactive visualization) (click here for interactive 29

- 30. “In the absence of clear guidance from existing analytical frameworks, policy-makers had to place particular reliance on our experience. Judgment and experience inevitably played a key role.” in a Speech by Jean-Claude Trichet, President of the European Central Bank, Frankfurt, 18 November 2010 30

- 31. Blog, Library and Demos at www.fna.fi Dr. Kimmo Soramäki kimmo@soramaki.net Twitter: soramaki