VIP Independent Call Girls in Mumbai 🌹 9920725232 ( Call Me ) Mumbai Escorts ...

China is set to meet growth targets despite stock market volatility

1. Page 1 of 2

Economic Commentary

QNB Economics

economics@qnb.com

02 August, 2015

China is set to meet growth targets despite stock market volatility

China’s economy is holding up despite the

recent crash in the stock market, which has

fallen 27% from its peak on 8th

June. Q2 real

GDP growth was released on July 15th

at 7.0%,

above consensus of 6.8% and in line with the

government target of around 7.0% for 2015.

Other economic data has also been positive.

Retail sales and industrial production year on

year growth numbers both picked up in June

having slowed earlier in the year.

Furthermore, property markets have turned a

corner with average prices for new residential

buildings in 70 cities rising in both May and

June, the first time they have risen since April

2014.

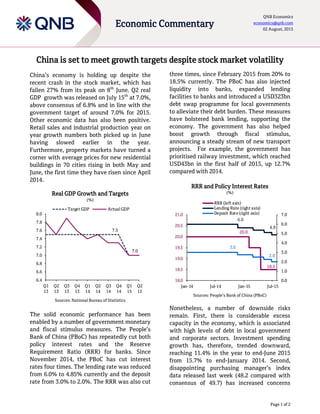

Real GDP Growth and Targets

(%)

Sources: National Bureau of Statistics

The solid economic performance has been

enabled by a number of government monetary

and fiscal stimulus measures. The People’s

Bank of China (PBoC) has repeatedly cut both

policy interest rates and the Reserve

Requirement Ratio (RRR) for banks. Since

November 2014, the PBoC has cut interest

rates four times. The lending rate was reduced

from 6.0% to 4.85% currently and the deposit

rate from 3.0% to 2.0%. The RRR was also cut

three times, since February 2015 from 20% to

18.5% currently. The PBoC has also injected

liquidity into banks, expanded lending

facilities to banks and introduced a USD323bn

debt swap programme for local governments

to alleviate their debt burden. These measures

have bolstered bank lending, supporting the

economy. The government has also helped

boost growth through fiscal stimulus,

announcing a steady stream of new transport

projects. For example, the government has

prioritised railway investment, which reached

USD43bn in the first half of 2015, up 12.7%

compared with 2014.

RRR and Policy Interest Rates

(%)

Sources: People’s Bank of China (PBoC)

Nonetheless, a number of downside risks

remain. First, there is considerable excess

capacity in the economy, which is associated

with high levels of debt in local government

and corporate sectors. Investment spending

growth has, therefore, trended downward,

reaching 11.4% in the year to end-June 2015

from 15.7% to end-January 2014. Second,

disappointing purchasing manager’s index

data released last week (48.2 compared with

consensus of 49.7) has increased concerns

7.5

7.0

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Target GDP Actual GDP

20.0

18.5

6.0

4.9

3.0

2.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

18.0

18.5

19.0

19.5

20.0

20.5

21.0

Jan-14 Jul-14 Jan-15 Jul-15

RRR (left axis)

Lending Rate (right axis)

Deposit Rate(right axis)

2. Page 2 of 2

Economic Commentary

QNB Economics

economics@qnb.com

02 August, 2015

about growth. Finally, stock market volatility

could have repercussions in the real economy.

The recent astronomical rise in onshore

Chinese equity markets (up 151% in the year

to 15th

June) was followed by a sharp

correction (down 28.0% since mid-June). This

volatility could undermine financial stability

and erode consumer confidence.

To counteract these downside risks, the

government is likely to provide more stimulus

to the economy during the second half of the

year for a number of reasons. First, it is likely

to be needed to meet the growth target of

around 7%. Second, the authorities have

demonstrated the commitment and capacity to

support the economy. Third, with almost

USD4tn in international reserves, the

authorities have plentiful resources at their

disposal to provide substantial stimulus.

Finally, inflation is currently 1.4%, well below

the target of around 3.0%, leaving plenty of

room for monetary stimulus. Therefore,

additional RRR and interest rate cuts as well as

an expanded local government debt swap plan

and more fiscal stimulus measures can all be

expected during the second half of the year.

Additionally, the government has introduced a

number of measures to directly support the

stock market. The PBoC has said it will provide

ample liquidity to the stock market to ensure

no systemic risks. For example, it has provided

liquidity support and a USD12bn capital

injection to a state run securities company, the

Chinese Security Fund, which invested

USD32bn in equity funds on 8th

July alone.

Other measures include providing at least

USD200bn of liquidity to brokerages, halting

initial public offerings and encouraging

government organisations to buy shares,

including state insurance and pension funds as

well as state-owned-enterprises. With such

strong support for both the economy and the

stock market, we still expect China to meet its

growth target of around 7% in 2015 despite the

downside risks.

QNB Economics Team:

Ziad Daoud

Acting Head of Economics

+974-4453-4642

Rory Fyfe*

Senior Economist

+974-4453-4643

Ehsan Khoman

Economist

+974-4453-4423

Hamda Al-Thani

Economist

+974-4453-4642

Rim Mesraoua

Economist – Trainee

+974-4453-4642

* Corresponding author

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.