Payment Week - Andrew Barnes, Managing Director__Citi Ventures

PayPal Equity Research

1. 1 University of Oregon Investment Group

October 29h

, 2016

Technology

Covering Analyst:

Alex Marcinkowski – amarcin2@uoregon.edu

Key Statistics

52 Week Price Range

50-Day Moving Average $39.28

Estimated Beta

Dividend Yield

Market Capitalization

3-Year Revenue CAGR

Trading Statistics

Diluted Shares Outstanding (mm) 1,244

Average Volume (3-Month) 8,080,000

Institutional Ownership

Insider Ownership

EV/EBITDA (LTM)

Margins and Ratios

Gross Margin (LTM)

EBITDA Margin (LTM)

Net Margin (LTM)

Debt to Enterprise Value

$30.52 - 44.52

0.99

NA

52.22B

18.06%

19.95%

12.11%

0.00x

81%

0%

22.72x

100.00%

Investment Thesis

PayPal’s premier market share give them a competitive advantage over

pure-play competitors, who cannot compete in scale or profitability and will

be priced out of the market in the coming years.

PayPal’s diversification enables them to pursue growth in all facets of the

payments industry, securing their leadership position in both mobile and

online payments.

PayPal will see monetization in their previous acquisitions of Venmo,

Braintree and Zoom; allowing them to offset margin squeeze and achieve

synergies between various products.

PayPal has consistently proven themselves to be innovators in the electronic

payments industry, and will continue to be first-to-market with new

opportunities, like contextual commerce and PaaP.

Ticker: PYPL Rating: Overweight

Price Target: $48.60

Action Recommended: Enter Position

Current Price: $41.69

0

10000000

20000000

30000000

40000000

50000000

60000000

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

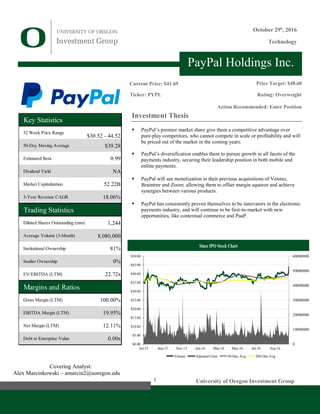

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

Volume Adjusted Close 50-Day Avg 200-Day Avg

Since IPO Stock Chart

PayPal Holdings Inc.

2. University of Oregon Investment Group

UOIG 2

October 29th

, 2016

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

2014 2015 2016 2017 2018 2019

Total Revenue %Growth

Medium-to-

Large

Enterprise,

48.4%

Small

Business,

46.3%

Consumer,

5.3%

1620.00 1790.00

3964.00

4928.00

2346.00

2818.00

2014 2015Total Customer

Accounts

Number of Transactions

Transactions per

Account

Growth

Business Overview

Company History

PayPal was founded in 1998 as a security software company, Confinity, by Peter

Thiel, Luke Nosek, Max Levchin and Ken Howery. In 2000, Confinity merged

with X.com, an online banking company and eventually changed its name to

PayPal in 2001 following Elon Musk’s decision to focus solely on money transfer

services. PayPal IPO’d in 2002, raising $61 million, but was acquired for $1.5

billion and taken private by eBay later that year. From 2002 to 2014, PayPal grew

under eBay as its primary payment method, acquiring VeriSign, Fraud Services,

Bill Me Later (PayPal Credit), Braintree, IronPearl and Zong during this period.

In 2011, PayPal broke into the offline payments world, allowing customers to pay

with PayPal at select stores; eventually furthered by a partnership with Discover

Card enabling payments with any retailer that accepts Discover.

On September 30, 2014, PayPal announced that it would spin off from eBay, and

become a separate public company; a move led by activist investor Carl Icahn.

The spin off was completed on July 17, 2015 and the IPO date was July 20, raising

$47 billion. On July 1, 2015 PayPal acquired money transfer service Xoom for

$1.09 billion. PayPal also made several other notable 2015 acquisitions, including

Paydiant and Venmo. Additionally, PayPal launched PayPal.me in late 2015, a

service that allows secure payments to be sent via a link on traditional messaging

platforms.

PayPal is headquartered in San Jose California and has European headquarters in

Luxemburg and international headquarters in Singapore. PayPal employs 16,800

people globally, 9,800 of whom are located in the U.S and 8,000 of which work

in their customer service organization.

Business Structure

PayPal is a payments technology company that facilitates and enables digital

payments for both consumers and merchants globally. PayPal’s overarching goal

is for people to be able to access and move their money quickly and securely,

regardless of location. They provide services to business to accept payments

though websites, mobile phones, applications and retail locations. In addition,

they provide peer-to-peer payments through PayPal, Venmo, and Xoom.

Altogether, PayPal, PayPal Credit, Xoom, Venmo, and Braintree make up the

company’s proprietary payments platforms.

PayPal provides payment solutions for over 192 million active accounts in over

202 markets worldwide. PayPal products have the ability for consumers to

purchase goods, get paid for sale of goods, transfer money and withdraw money.

PayPal enables consumers to fund purchases through a bank account, PayPal

balance, PayPal Credit, or a credit or debit card. PayPal, Venmo and Xoom can

be used to send and receive money, including cross-border transactions, to friends

and family.

On the merchant facing side, merchants are offered “end-to-end” payments

solutions that authorize and settle transactions, as well as provide access to funds.

PayPal’s platform is connected to numerous global financial institutions and allow

payments regardless of where the merchant and customer are located, accepting

more than 100 currencies, allowing bank withdraws in 57 currencies and holding

balances in PayPal in 26 currencies.

Figure 1: Major Market Segmentation

Source: IBISWorld

Figure 2: Revenue Growth

Source: UOIG Spreads

Figure 3: PayPal Transaction Metrics

Source: PayPal Investor Relations

3. University of Oregon Investment Group

UOIG 3

October 29th

, 2016

0%

3%

6%

9%

12%

-300

0

300

600

900

1200

2016 2017 2018 2019

Capital Expenditures

Change in Net Working Capital

Capital Expenditure (% of Revenue)

Braintree 2013 - $800M

Venmo 2013 - Included in Braintree Deal

Paydiant 2015- $260M

CyActive 2015 - $60M

Xoom 2015 - $890M

Modest 2015 - Unknown

Recent Acquisitions

6%

4%

3%

3%

3%

81%

Vanguard Group

FMR LLC

State Street

Carl Icahn

T Rowe Price

Total Insitutional

Shares

PayPal generates revenue by charging fees for processing transactions and other

payment-related services, based primarily on total payment volume. Additionally,

PayPal earns revenues by providing value-add services, like PayPal Credit and

Paydiant. Transactions on PayPal’s ecosystem can involve a merchant, a

consumer, the consumer’s funding source provider, and PayPal.

Products and Services

PayPal

PayPal offers merchant and consumer payment services online, on mobile phones

or in-store. PayPal enables merchants to accept and process numerous forms of

payment types through their various payment platforms. Consumers can pay with

a PayPal balance, credit card, debit card or bank balance. PayPal merchant

accounts can be set up in minutes and do not generally require new or specialized

equipment. PayPal also offers in-store payments and POS solutions to merchants,

similar to offerings by Square. Furthermore, PayPal provides merchants value add

services to help manage cash flow, invoice clients, store sensitive customer

information and integrate with Braintree.

PayPal’s digital wallet allows consumers to draw funds from a variety of sources

in one location. PayPal does not generally charge to draw and fund accounts. In

addition, PayPal offers buyer protection programs that reimburse the consumer in

the case of fraudulent activity.

Braintree

Braintree provides business with the ability to accept payments online or on

mobile phones. Its payment platform is full-stack, meaning it replaces the

traditional model of using different providers for a gateway and merchant

provider. Braintree provides customers with both a merchant account and a

payment gateway and charges a fee and set amount per transaction processed.

Braintree’s white label nature means it is device agnostic and supports seamless

payments within apps or online. Braintree is fully integrated with PayPal and other

payment types.

Venmo

Venmo is a peer-to-peer payments application that lets users send and receive

money instantly from other Venmo users. Venmo is available for both Apple and

Android devices and is linked to a user’s email address. Transfers within the same

country that are not financed with a credit card are free of charge. Venmo lets you

link a bank account or card to pay, along with your Venmo balance. Transfers

from Venmo to bank accounts are completed within one business day. Venmo

recently initiated a feature that allows users to pay merchants with Venmo in-app,

although adoption is in its early stages.

PayPal Credit

PayPal Credit, formerly Bill Me Later, allows consumers to access a revolving

line of credit though their PayPal account to pay for online. PayPal credit can be

used at nearly anywhere PayPal is accepted. PayPal makes money on the set

interest rate that consumers are charged monthly for rolling balances. PayPal

Credit functions in much the same way as a traditional credit card.

Figure 4: PayPal Historic Acquisitions

Source: Capital IQ

Figure 5: PayPal Institutional Ownership

Source: Nasdaq.com

Figure 6: CapEx and Working Capital Projections

Source: UOIG Spreads

4. University of Oregon Investment Group

UOIG 4

October 29th

, 2016

-8

-6

-4

-2

0

2

4

6

8

10

12

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

2010 2011 2012 2013 2014 2015 2016

Total Revenue % Growth

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2013 2014 2015 2016 Q1-3

U.S. International

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2016 2017 2018 2019 2020 2021 2022 2023 2024

EBIT FCF

Xoom

Xoom enables money transfers from U.S. customers to international family and

friends online or on mobile phones. Users can fund their transfer with a bank

account, debit or credit card and send their transfer to any bank in the recipients’

country, deposited within 1 to 2 business days. Xoom offers money transfer

services from the U.S. to 41 countries and cross border bill payment to 7 countries.

Paydiant

Paydiant is a cloud based, white label mobile wallet platform that enables

merchants and banks to create their own mobile wallet solutions under their own

brands and in their own apps. Paydiant powers payment apps for businesses like

Subway and Capital One Bank. Paydiant yields more point-of-sale volume for

PayPal and drives in-store sales for PayPal merchant partners by providing quick

and seamless payment for customers.

Revenue segments

Transaction Revenues

Transaction revenues are net transaction fees charged to consumers and merchants

based on volume of activity processed through PayPal, PayPal Credit, Venmo,

Braintree and Xoom. The revenues are based off of total payment volume, and

pricing varies among merchants and regions.

Other Value Added Services

Value add revenues are derived principally from interest and fees earned on

PayPal Credit loans portfolio, subscription fees, gateway fees, interest earned on

PayPal customer account balances, fees from Paydiant, revenue share through

partnerships and gain on sale of interest in certain consumer loans.

Industry

Overview

PayPal’s unique market positioning and myriad of different products means it

competes in several distinct yet overlapping industries. First, it competes with

other credit card processors and money transferor’s, who process financial

transactions and provide liquidity services for consumers and merchants. Major

players in this space are American Express, Visa, MasterCard and First Data Corp.

Perhaps more directly though, PayPal competes in the online payment processing

software industry. Companies in this space enable merchants and consumers to

pay, process and authorize online transactions. Major players in this space are

Square, Google and Stripe.

Outlook

The outlook of their overarching industry looks extremely promising over the

coming years. IBISWorld anticipates revenue for the Credit Card Processing and

Money Transferring industry to grow at an annualized rate of 4.4% to $72 billion

in the five years to 2021.The decline of cash and checks is a natural progression

in today’s technologically oriented society and directly correlates to growth in

electronic payments. Continued advances in mobile technology allow users to

access banking information, pay bills, and complete transactions on-the-go; a

Figure 7: PayPal EBIT & FCF Projections

Source: UOIG Spreads

Figure 8: Historical Revenue by Geography

Source: UOIG Spreads

Figure 9: Payment Industry Growth

Source: IBISWorld

5. University of Oregon Investment Group

UOIG 5

October 29th

, 2016

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

0

2

4

6

8

10

12

2014 2015 2016 2017 2018 2019

E-Commerce % Change

0

2

4

6

8

10

12

14

16

75

80

85

90

95

100

105

2014 2015 2016 2017 2018 2019

CCI %Growth

Competition

Concentration

Life Cycle

Capital Intensity

Technology Change

Regulation

Industry Assistance

Medium

Medium

None

Barriers to Entry

High

Low

Growth

Low

significant advantage over cash and check. More specifically, technologies

produced by Apple, Google and PayPal have allowed consumers to sync credit

cards with a mobile phone for in-store purchases and have gained ground in the

credit card space at an alarming rate; and are now supported by almost all major

credit cards and banks in the United States.

Macro factors

Consumer Spending and Consumer Confidence

Consumer spending is an extremely important factor in industry demand, as

volume of purchases drives revenue for the industry. As consumers spend more

on products, PayPal and others have the opportunity to process more transactions

and experience greater transaction volume. This spending is largely influenced by

consumers’ expectations of future economic conditions, measured by consumer

confidence. Consumer confidence is expected to increase by 3% over the next 4

years, which is an opportunity for payment processors.

E-Commerce Sales

E-commerce sales represent the percentage of consumer retail purchases done

online as compared to retail stores. As PayPal conducts nearly all business online,

the growth of e-commerce means PayPal and others will process higher payment

volumes. E-commerce sales have been steadily increasing for years, and have a

5.4% expected growth from 2016-2021 according to IBISWorld. As e-commerce

continues to grow, the shift away from cash and check payments will by further

extenuated and consumers will naturally move towards electronic methods as the

primary form of payment.

Mobile Phone Usage

Mobile phone applications continue to be a growing source of revenue in the

global payments industry. Mobile payment processing represents the biggest

growth opportunity in this industry, as consumers continually use P2P transferring

services, in-store phone payment technologies and mobile shopping applications.

As more people internationally gain access to the internet and mobile phones,

more payments will be initiated via mobile applications, and less people will be

incentivized to hold cash or physical credit cards

Regulatory Environment

PayPal is not classified as a bank within the U.S. because they do not engage in

fractional reserve banking. In the U.S., PayPal is licensed as a money transmitter

and is therefore subject to some of the regulations that banks are, most notably

Regulation E consumer protections. In Europe, PayPal is registered as a bank and

is governed by Luxembourg’s banking supervisory authority. They are allowed to

conduct banking business throughout the EU. Internationally, PayPal has

permission to operate in nearly all major countries, including China and India,

with nearly identical functions to that seen in the U.S. service. Because of the

relatively new nature of this industry, increasing regulation, especially in the U.S.

could materially harm PayPal’s business. Specifically, new limits on transaction

fees or reclassification to a bank could hurt PayPal’s and the industry’s future.

Figure 10: E-commerce Growth

Source: IBISWorld

Figure 11: Industry Barriers

Source: IBISWorld

Figure 12: CCI Projection

Source: Capital IQ

6. University of Oregon Investment Group

UOIG 6

October 29th

, 2016

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

$15,000

$15,500

$16,000

$16,500

$17,000

$17,500

$18,000

$18,500

$19,000

$19,500

$20,000

2017 2018 2019 2020 2021 2022

Total Revenue % Growth

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

SQ SHOP TSS V MA AXP GOOGL AAPL AMZN

29.9%

70.1%

PayPal

Others

Competition

Internal

This industry is highly competitive due to its attractive growth prospects and

strong margins. Competition from this industry occurs both internally and

externally. Internal competition among processors is focused around price, as

most operators charge a percentage of the transaction plus a set fee. Merchants

want a processor who offers competitive pricing so it does not eat into their

margins. Additionally, features like security, prominence among consumers, and

reliability are further points of differentiation.

External

Externally, firms compete with other payment forms like credit and debit cards

and bank transfers. These substitute forms of payment have been hurt by online

growth as consumers increasingly prefer one consolidated platform to hold

sensitive information. In addition, retail and in-person purchases, both of which

have been steadily declining, eliminate the need for online payment processors.

As the world increasingly shifts to electronic payment methods over cash and

check, this will spur the entrance of new competitors seeking to capitalize on this.

Most importantly, the ability to have excellent mobile and e-commerce

technology will by key to sustained success in this industry. The ability to provide

cost-effective, easy-to-use and secure platforms will be a differentiator among

firms going forward. Credit card companies like Visa have already begun to

recognize this trend and have created mobile/online payment platforms.

Barriers to entry

Barriers to entry in this industry are rapidly increasing as many firms are expected

to be forced or bought out of the market in the coming years. Due to the new

nature of the industry, there is a relatively low level of concentration,

compromised of many non-profitable firms. As these firms subside, barriers to

entry will become increasingly high. In the future, lesser known firms will

struggle to gain the acceptance and trust of merchants, meaning the barrier to entry

reinforces itself. As firms cannot gain trust without attracting a large user base of

partners, they can’t establish trust without a large user base. Therefore, small firms

won’t be able to compete and larger players will command benefits from

economies of scale and will be able to offer better pricing

Strategic Positioning

Market Share

PayPal controls much of the global market for electronic payments, accounting

for nearly one third of global market share, according to IBISWorld. Because of

this, they have built and maintained a strong client base of the biggest merchants

in the world, counting firms like Nike, eBay Alibaba and Walmart as clients. The

PayPal brand has become synonymous with online payments and is the preferred

way to pay for many consumers globally. Market share is of particular importance

in this industry because the success of PayPal depends on the universal acceptance

of their payment platform. As more merchants use their platform, it incentivizes

other merchants to follow because of the popularity of PayPal among consumers

and the fear of losing out on business to competing online sites.

Figure 13: Comparables Enterprise Value ($B)

Source: UOIG Spreads

Figure 14: Online Payment Industry Projections

Source: IBISWorld

Figure 15: PayPal Market Share

Source: Capital IQ

7. University of Oregon Investment Group

UOIG 7

October 29th

, 2016

PayPal Online Solutions

PaPal Credit

PayPal Working Capital

PayPal POS Solutions

PayPal Shopping

PayPal Here

Modest/PayPal Commerce

Xoom

Venmo

Paydiant

Braintree

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2013A 2014A 2015A 2016E

EBITDA Margin EBITDA Growth

Diversification

PayPal’s acquisition and growth strategy have created a diversified business by

offering solutions across the payment ecosystem. Venmo gives them exposure to

the growing P2P payments industry, and is currently the largest and most

recognized player in this space. Braintree allows them to compete directly with

Stripe and Shopify by accepting all payment types in a white label, customizable

package. PayPal Credit competes with credit cards by allowing users to create a

revolving line of credit and Xoom is currently the most used and recognized way

to send money internationally. By diversifying their offerings, PayPal has

exposure to all elements of the electronic payments world and is not beholden to

growth in a certain area.

Financial Strength

PayPal has shown to be one of the very few players in this industry that has a track

record of making money and being consistently profitable. Their low debt and

high cash balnce allow them to aggressively pursue growth opportunities without

increasing firm risk to shareholders. PayPal has little going concern risk and can

therefore outlast or buy-out pure-play competitors. Contrast that with PayPal’s

more pure-play competitors like Shopify, Stripe, and Skril, who have shown no

ability to turn a profit and are supported by V.C. funding or their equity capital

raises, both of which are not legitimate long-term strategies to maintain

operations.

Security

PayPal is widely viewed as the most secure payment method for both consumers

and merchants. The 2015 acquistion of CyActive further enhances PayPal’s

security cababilites. Because PayPal transactions only need a login and password,

personal bank account and card info are not sent to merchants, meaning a hack to

a merchant site does not compromise consumer information. PayPal also offers

buyer protection policies in which it covers the cost of a purchased good if the

transaction meets certain criteria. The PayPal site itself is heavily encrypted and

PayPal itself offers rewards to white hat hackers for finding vulnerabilities in the

site.

Business Growth Strategies

Overall Volume Growth through Braintree

PayPal’s long term strategy is to grow its core payment processing business

through taking smaller cuts of transactions in exchange for larger overall

payment volume. Braintree is the key driver behind volume growth, possessing

payment capabilities for mobile phones and websites. Braintree provides

merchant account, payment gateway, card storage and other services in 40

countries and over 130 currencies globally. Braintree has seen volume growth of

over 100% y/y and counts Uber, AirBnB, Netflix and GitHub as clients.

Braintree’s tokenization technology is superior to competitors like Apple Pay

and Stripe as it is device agnostic, implements seamless payments and supports

Venmo and PayPal. Although Braintree’s take rate is lower than PayPal’s

because it operates as both a full stack processor and payment gateway, this is

offset by its impressive growth and synergies with other PayPal products.

Figure 16: PayPal Product Breakdown

Source: PayPal.com

Figure 17: PayPal EBITDA Margins

Source: UOIG Spreads

8. University of Oregon Investment Group

UOIG 8

October 29th

, 2016

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

V MA AXP PYPL TSS

Revenue Growth 2016 Revenue CAGR

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

EBIT Margin EBITDA Margin

Strategic Partnerships

PayPal has announced partnerships with MasterCard, Visa and First Data over

the past year. The First Data partnership enables PayPal’s payments products to

be used in-store by First Data’s clients and businesses. First Data has a 40%

market share in the U.S. for payment processing and will drive the availability

of PayPal at the point-of-sale. PayPal’s recent MasterCard partnership will yield

undisclosed financial incentives based on volume of MasterCard transactions

PayPal processes, and PayPal will now be able to be used at over 5 million

contactless merchant locations globally. PayPal’s Visa deal will yield similar

financial incentives and will yield non-increasing payment fees for PayPal.

Xoom and Venmo Expansion

PayPal has shown their ability to aquire new businesses, leverage their scale,

increase the user base and then monetize the service. Venmo’s payment volume

has grown at a CAGR of 138% to $4.9 billion in Q3 alone and PayPal is now

ready to cash in on Venmo’s massive user base. This year, PayPal implemted

Pay with Venmo feature that allows users to pay with in-app purchases through

their Venmo account. Merchants will pay a 2.9% transaction fee plus $0.30,

effectively monetizing the service. PayPal has also announced that they are

adding in-store payments to both their mobile apps as soon as 2017.

Xoom is PayPal’s next acquistion money-maker; a service that lets users send

money internationally, charging between $5-10 for the exchange and the

difference in the exchange rate. Xoom has now been integrated into PayPal’s

platform, meaning the potential user base has increased exponentially to all

PayPal account holders. In addition, Xoom’s services can now be expanded to

all of PayPal’s 200+ markets globally. PayPal projects Xoom will add $200

million to revenue for 2016, and higher margins in their Xoom buiness going

forward, offsetting some transaction margin squeeze.

Long-Term Product Innovation

PayPal has shown continued initiative to expand and even re-create the

electronic payments industry. PayPal aims to expand mobile shopping by being

a merchant services solution that powers merchant apps. PayPal wants to

provide an unbranded platform that is technology agnostic and can process any

payment type. Their Paydiant acquisition directly supports this long term vision

and will create innovation in mobile wallet technology.

Perhaps most importantly, PayPal is also the first mover in the contextual

commerce field. Contextual commerce is the idea that allows merchants to

implement buying opportunities into natural online activities. Braintree acts as

the enabler of contextual commerce and has already begun to work, along with

their subsidiary, Modest, with social media platforms. Braintree has the

capabilities to power PayPal’s contextual commerce platform and leverage

PayPal’s 14 million merchants and 190 million customers

Management and Employee Relations

Dan Schulman – President and CEO

Dan Schulman joined PayPal in 2014 to lead the PayPal through and after their

split with eBay. He served as the Group President of Enterprise Growth at

American Express Company from August 2010 to September 30, 2014. At

American Express, he was responsible for the its global strategy to expand

Figure 18: Selected Comparables Revenue

Source: UOIG Spreads

Figure 19: Selected Comps Margin Analysis

Source: UOIG Spreads

Figure 20: PayPal Value Proposition

Source: PayPal Investor Relations

9. University of Oregon Investment Group

UOIG 9

October 29th

, 2016

Prepaid Card

Services

7.0%

Check

Processing

15.0%

ACH

Products

18.0%

Credit Card

Services

22.0%

Debit Card

Services

38.0%

$0

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

2014 2015

Salary Stock-Based Other

Corporate

Data security

40%

Security

Threat

Protection

40%

Cost

Reductionand

Risk

Management

20%

alternative mobile and online payment services, He has a record of high

performance in the consumer-marketing arena and almost two decades of

experience in the wireless industry. Total 2015 Compensation = $14,444,941.

John Rainey – CFO and Senior VP

John Rainey has been CFO and Senior Vice President of PayPal Holdings, Inc.

since August 24, 2015. John has an extensive background in corporate finance,

treasury, financial planning and analysis, tax, investor relations, strategic planning

and risk. He served as the Chief Financial Officer and Executive Vice President

of United Continental Holdings, Inc. from April 2012 to July 30, 2015. Total 2015

Compensation = $10,682,546.

William Ready – COO and Executive VP

William Ready has been the Chief Operating Officer and Executive Vice

President at PayPal Holdings, Inc. since September 30, 2016 and served as its

Global Head of Product & Engineering and Senior Vice President since

September 15, 201. Mr. Ready serves as a Senior Advisor at Silversmith Capital

Partners. He has in-depth knowledge of both the payments and technology space,

having built and grown multiple cutting edge payments companies. Total 2014

Compensation = $31,378,935.

Sripada Shivananda – CTO and Executive VP

Sripada Shivananda has been the Chief Technology Officer and Senior Vice

President at PayPal Holdings, Inc. since April 1, 2016. Mr. Shivananda served as

Vice President of Global Platform & Infrastructure at PayPal Holdings, Inc. He

served as Vice President of Platform & Infrastructure - eBay Marketplaces at

eBay Inc. from 2010 to 2015.

Management Guidance

Management guidance has been historically accurate, leaning on the conservative

side; with slight average over performance of expectations. Management provides

yearly and quarterly guidance on many metrics, including free cash flow, revenue,

operating margin and EPS among others. Management has typically hit these

targets within a reasonable level of error. PayPal also places heavy emphasis on

non-GAAP metrics, for which they also provide for. Management guidance was

factored into revenue projections and margin calculations.

Portfolio Strategy

PayPal operates as a large-cap financial technology company. Given its size,

PayPal cannot be pitched to the Alumni Fund. The Tall Firs Portfolio is currently

underweight large-cap and overweight technology. Given PayPal’s financial

exposure, a currently underweight sector, it is being pitched to Tall Firs as a large-

cap stock that can help increase the portfolio’s exposure to financials. In addition,

the analyst conviction, risk profile and growth of PayPal signify a fit for the

DADCO portfolio. Therefore, it is being pitched as a buy for DADCO as well.

Figure 21: Primary Electronic Payment Methods

Source: IBISWorld

Figure 22: Executive Compensation

Source: Morningstar

Figure 23: Corp. Concerns of Online Processing

8

Source: IBISWorld

10. University of Oregon Investment Group

UOIG 10

October 29th

, 2016

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Large Cap Mid Cap Small cap

IVW Tall Firs

Multiple Implied Price Weight

EV/Revenue $56.23 0.00%

EV/Gross Profit $86.88 0.00%

EV/EBIT $29.30 0.00%

EV/EBITDA $58.82 100.00%

EV/(EBITDA-Capex) $55.49 0.00%

Market Cap/Net Income = P/E $41.33 0.00%

Price Target $58.82

Current Price 43.22

Undervalued 36.09%

32%

14%

5%

41%

5%

3%

IME

TMT

Healthcare

Consumer

Financial

Cash

Recent News

PayPal's Long-Term Outlook Helps Validate a Questioned Growth Strategy

– TheStreet

Though its results and short-term guidance weren't particularly strong, PayPal

was more upbeat than ever about its ability to deliver strong long-term growth in

a changing online payments landscape, and managed to soothe some margin

concerns along the way. With investors taking the long view, that has shares

flying to their highest levels since the online payments giant split from eBay last

year.

Catalysts

Upside

PayPal has ideal market positioning in the online and mobile payments

industry, going forward they will benefit from increased economies of scale

and increased barriers to entry in the industry.

PayPal’s former acquisitions will continue to drive growth and become

monetized, diversifying PayPal’s offerings and ensuring innovation in a

rapidly changing industry.

PayPal’s strategic partnerships show willingness to work with and profit from

larger competitors and a desire to expand into POS activities.

Downside

Changing regulations or potential litigation, specifically in the U.S., could

hurt margins and force PayPal to restructure their business model.

Encroachment by larger competitors like Amazon, Apple and Visa into the

mobile payments space could adversely affect growth and margins.

Divergence from PayPal’s core business could result in lack of direction by

management and a fragmented business that cannot realize potential

synergies between products.

Comparable Analysis

I valued Visa’s common stock using comparable companies that, collectively,

best represent PayPal’s services, market positioning and future growth. As PayPal

is extremely diversified, almost no pure-play competitors exist, and I therefore

separated comparable into 3 baskets. The first being e-commerce and mobile

payment processors. I selected companies for this basket based on capital

structure, growth and likeness of services. The second basket is credit card

companies that compete with PayPal as alternative methods of payment. Selection

within this category was based on market size, singularity of offerings, capital

structure and future growth. The final basket is comprised of diversified tech

companies that offer services that compete with PayPal’s core business. Selection

for this basket is based on market size, threat of competing service and reasonable

future growth.

Square Inc. - SQ (10%)

“Square, Inc. develops and provides payment processing, point-of-sale (POS),

financial, and marketing services worldwide. It provides Square Register, a POS

Figure 24: Tall Firs Weightings

Source: UOIG Drive

Figure 25: Tall Firs Weightings

Source: UOIG Drive

Figure 26: Comparables Weighting

Source: UOIG Spreads

11. University of Oregon Investment Group

UOIG 11

October 29th

, 2016

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16

Adjusted Close 50-Day Avg 200-Day Avg

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Cards In circulation (millions) % of Total

0

5

10

15

20

25

30

35

40

Weighted Average PayPal

software application for iOS and Android; Square Analytics that shows its sellers

how their businesses are performing; and Square Reader for magnetic stripe cards,

EMV chip cards, and NFC, which connects wirelessly to mobile devices. The

company also offers Square Stand that transforms an iPad into a POS terminal;

Square Cash, a peer-to-peer payments service. Square was founded in 2009 and

is headquartered in San Francisco, California.” – Capital IQ

Total System Services Inc. - TSS (10%)

“Total System Services, Inc. provides payment processing, merchant, and related

payment services to financial and nonfinancial institutions in the United States,

Europe, Canada, Mexico, and internationally. The company offers account

processing and output services, including processing the card application,

initiating service for the cardholder, processing card transaction for the issuing

retailer or financial institution, and accumulating the account’s transactions.,

Georgia.” – Capital IQ

Visa Inc. - V (15%)

“Visa Inc., a payments technology company, operates an open-loop payments

network worldwide. The company facilitates commerce through the transfer of

value and information among financial institutions, merchants, consumers,

businesses, and government entities. It operates VisaNet, a processing network

that enables authorization, clearing, and settlement of payment transactions.” –

Capital IQ

MasterCard Inc. - MA (15%)

“MasterCard Incorporated, a technology company, provides transaction

processing and other payment-related products and services in the United States

and internationally. It facilitates the processing of payment transactions, including

authorization, clearing, and settlement, as well as delivers related products and

services. The company also offers value-added services, such as loyalty and

reward programs, and information and consulting services.” – Capital IQ

American Express Company - AXP (15%)

“American Express Company provides charge and credit payment card products

and travel-related services to consumers and businesses worldwide. The

company’s products and services include charge and credit card products;

network services; expense management products and services; travel-related

services; and stored value/prepaid products.” – Capital IQ

Alphabet Inc. - GOOGL (15%)

“Alphabet Inc., through its subsidiaries, provides online advertising services in

the United States, the United Kingdom, and rest of the world. The company offers

performance and brand advertising services. It operates through Google and Other

Bets segments.” – Capital IQ

Apple Inc. - AAPL (10%)

“Apple Inc. designs, manufactures, and markets mobile communication and

media devices, personal computers, and portable digital music players to

consumers, small and mid-sized businesses, education, and enterprise and

government customers worldwide. The company also sells related software,

Figure 27: Visa 5 Year Stock Chart

Source: Yahoo! Finance

Figure 28: Multiple Comparison

Source: UOIG Spreads

Figure 29: Credit Card Comparables

Source: UOIG Spreads

12. University of Oregon Investment Group

UOIG 12

October 29th

, 2016

$0.00

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

$700.00

$800.00

$900.00

Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16

Adjusted Close 50-Day Avg 200-Day Avg

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

0.0

100,000.0

200,000.0

300,000.0

400,000.0

500,000.0

600,000.0

2013A 2014A 2015A 2016E 2017E 2018E

TPV Growth % Growth

Revenue $10,848

EBIT $1,532

Net Income $1,368

Operaing Cash Flow $2,023

NWC $4,232

FCF $765

EBITDA $2,258

services, accessories, networking solutions, and third-party digital content and

applications.” – Capital IQ

Amazon Inc. – AMZN (15%)

“Amazon.com, Inc. engages in the retail sale of consumer products in North

America and internationally. The company sells merchandise and content

purchased for resale from vendors, as well as those offered by third-party sellers

through retail. The company was founded in 1994 and is headquartered in Seattle,

Washington.” – Capital IQ

Discounted Cash Flow Analysis

In order to evaluate the intrinsic value of PayPal, I constructed a DCF analysis

with a projection period through a 2024 fiscal year. After determining enterprise

value, debt (less non-operating cash) was subtracted and divided by diluted shares

outstanding to obtain an implied price.

Revenue Model

PayPal breaks their revenue out into 2 segments, transaction and value add

services. Unfortunately, PayPal does not give illumination on revenue by service

or product line. Therefore, revenue was forecast for both segments through 2019

based on recently released management guidance, which has been historically

accurate. Following 2019, revenue growth is trended down towards the terminal

year at close to 9% as the firm becomes larger but has expansion opportunities in

a still growing industry and pursues international growth.

Working Capital

Working capital was calculated as current assets (excluding cash and short term

investments) less comprehensive current liabilities. PayPal’s historical

receivables and payables associated with eBay were set to zero as PayPal does not

break out this working capital item after their split in 2015. Accounts receivable

and payable were kept near historical averages, projected based off days sales

outstanding. Loans and interest receivable represent receivables from consumers

under PayPal Credit and working capital advances to small and medium sized

businesses through PayPal Working Capital. Loans and interest receivable were

kept near historical averages based on days sales outstanding. Funds receivable

hand customer accounts and funds payable and amounts due to customers are

offsetting accounts representing the balances in customer accounts and timing

differences in transfers to and from accounts. As they are offsetting, this has no

material effect on the valuation, but was projected to increase off of days sales

outstanding as mean customer account values rise.

Beta

The final beta used in the valuation is .99. This was calculated as a weighted

average of PayPal’s historical beta, adjusted for cash, a representative ETF beta,

and a weighted comparables beta. A beta of essentially 1 is reasonable given

PayPal’s size and financial exposure; their current individual beta is higher due to

lack of data points and a short trading period. As time goes on, I fully expect their

individual beta to move closer to 1.

Figure 30: PayPal TPV Growth

Source: UOIG Spreads

Figure 31: AMZN 5 Year Stock Chart

Source: Yahoo! Finance

Figure 32: 2016 PayPal Analyst Estimates

Source: UOIG Spreads

13. University of Oregon Investment Group

UOIG 13

October 29th

, 2016

2025E 2026E 2027E 2028E 2029E

$4,245.57 $4,820.86 $5,304.56 $5,650.25 $5,819.76

2055.79 2158.33 2195.80 2162.53 2059.44

17.07% 13.55% 10.03% 6.52% 3.00%

Intermediate Growth Rate

Type Equity Beta Cash Adjusted SE Weighting

1Year Daily Beta 1.22 1.25 0.10 0.00%

Since IPO Daily 1.18 1.21 0.09 15.00%

Since IPO Weekly 1.31 1.34 0.20 0.00%

Since IPO Monthly (14Data Points) 1.13 1.16 0.39 0.00%

1Year Comps 0.96 0.96 NA 50.00%

1Year ETF 0.93 0.93 0.06 35.00%

FinalCash Adjusted Beta 0.99

Undervalued/(Overvalued)

Terminal Growth Rate

2.0% 2.5% 3.0% 3.5% 4.0%

0.80 24.51% 32.48% 42.14% 54.08% 69.21%

0.90 8.92% 14.85% 21.89% 30.36% 40.76%

1.00 (3.65%) 0.86% 6.12% 12.33% 19.78%

1.10 (13.99%) (10.49%) (6.47%) (1.80%) 3.70%

1.20 (22.61%) (19.86%) (16.73%) (13.14%) (8.99%)

AdjustedBeta

Transaction Expense

Transaction expense represents PayPal’s largest cost and is therefore crucial in

the valuation. This expense consists of the costs PayPal incurs to accept the

funding source of a customer’s payment. As PayPal recently inked partnerships

with Visa and MasterCard, 2 of the costlier funding options, their transaction

expense is poised to increase in the coming years as there is some margin squeeze.

Although some of this will be offset by the changing of PayPal’s revenue mix if

they can monetize higher margin activities like Xoom and Venmo. As such,

transaction expense is forecast to increase slightly relative to historical averages.

Transaction & Loan Losses

Transaction and loan losses consist of costs associated with fraud protection,

chargebacks and losses on the loans receivable balance. Losses are forecast to

increase as PayPal focuses on growing its PayPal Credit operations and maintains

its buyer protection programs.

Depreciation and Amortization

The majority of PayPal’s PP&E and intangible assets are hardware and software

equipment, meaning they are depreciated on a 1 to 3-year time table. Given the

high rate of historical deprecation based on net beginning PP & E, I kept this the

same given their ongoing investments in quickly depreciating assets.

Tax Rate

PayPal’s tax rate has been historically lower than the U.S. due to their significant

amount of revenue that is recognized internationally. As PayPal has stated that

they do not intend to repatriate earnings, and instead invest them internationally,

their tax rate should remain relatively the same into perpetuity. If the geography

mix stays relatively constant, then assuming a lower tax rate for PayPal is a

reasonable assumption. Analyst estimates and management guidance both purport

this assumption.

Capital Expenditures

Purchases of PP&E mainly represent investments in hardware, servers and

computers. PayPal gives very little illumination on this line item and the specifics

of capital expenditures. Therefore, I projected based on percent of revenue with a

slight decline as PayPal reaches maturity and tailors off reinvestment into new

services.

Recommendation

PayPal’s fundamental undervaluation warrants a buy for both the Tall Firs and

DADCO Portfolios. Their strong upside catalysts, market position and product

diversification in a rapidly expanding industry mean they will soon realize higher

valuation levels.

Figure 33: PayPal Intermediate Growth Rate

Source: UOIG Spreads

Figure 34: PayPal Beta

Source: UOIG Spreads

Figure 35: Price Sensitivity

Source: UOIG Spreads