IVD Market Size and Growth Trend

•

2 recomendaciones•1,642 vistas

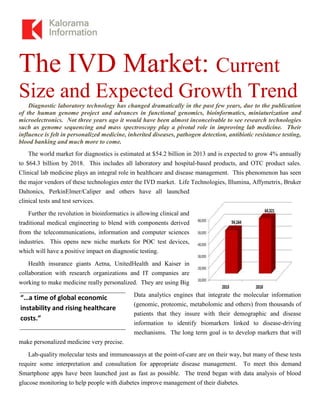

The document discusses the current state and expected growth trends of the in vitro diagnostics (IVD) market. It notes that the global IVD market was estimated at $54.2 billion in 2013 and is expected to grow 4% annually to $64.3 billion by 2018. Technological advances in areas like genomics, bioinformatics, and miniaturization have transformed diagnostic laboratory technology in recent years. Personalized medicine, infectious disease testing, and other applications are driving growth in the IVD market. However, economic instability, rising healthcare costs, and reimbursement changes pose challenges for the industry.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (7)

Similar a IVD Market Size and Growth Trend

Similar a IVD Market Size and Growth Trend (20)

Más de Bruce Carlson

Más de Bruce Carlson (10)

Último

Último (20)

IVD Market Size and Growth Trend

- 1. The IVD Market: Current Size and Expected Growth TrendDiagnostic laboratory technology has changed dramatically in the past few years, due to the publication of the human genome project and advances in functional genomics, bioinformatics, miniaturization and microelectronics. Not three years ago it would have been almost inconceivable to see research technologies such as genome sequencing and mass spectroscopy play a pivotal role in improving lab medicine. Their influence is felt in personalized medicine, inherited diseases, pathogen detection, antibiotic resistance testing, blood banking and much more to come. The world market for diagnostics is estimated at $54.2 billion in 2013 and is expected to grow 4% annually to $64.3 billion by 2018. This includes all laboratory and hospital-based products, and OTC product sales. Clinical lab medicine plays an integral role in healthcare and disease management. This phenomenon has seen the major vendors of these technologies enter the IVD market. Life Technologies, Illumina, Affymetrix, Bruker Daltonics, PerkinElmer/Caliper and others have all launched clinical tests and test services. Further the revolution in bioinformatics is allowing clinical and traditional medical engineering to blend with components derived from the telecommunications, information and computer sciences industries. This opens new niche markets for POC test devices, which will have a positive impact on diagnostic testing. Health insurance giants Aetna, UnitedHealth and Kaiser in collaboration with research organizations and IT companies are working to make medicine really personalized. They are using Big Data analytics engines that integrate the molecular information (genomic, proteomic, metabolomic and others) from thousands of patients that they insure with their demographic and disease information to identify biomarkers linked to disease-driving mechanisms. The long term goal is to develop markers that will make personalized medicine very precise. Lab-quality molecular tests and immunoassays at the point-of-care are on their way, but many of these tests require some interpretation and consultation for appropriate disease management. To meet this demand Smartphone apps have been launched just as fast as possible. The trend began with data analysis of blood glucose monitoring to help people with diabetes improve management of their diabetes. “…a time of global economic instability and rising healthcare costs.”

- 2. Now apps are available to help lab professionals consult with databases and experts worldwide. The widespread availability of communication devices such as Apple’s iPAD and iPHONE and other android phones and personal digital assistants are the most significant enablers of this phenomenon that will bring quality diagnostics to people in remote areas of developing and developed countries. However, these tests are being launched in Healthcare reform, the reformulation of reimbursement for the newest and most valuable tests and the reorganization of the regulatory process for these tests in the U.S. have created an environment of insecurity. The acute economic crisis in European countries has cut growth in the IVD industry to 1% at best. Payers are cutting reimbursement schedules to the bare minimum to keep from going broke. Japan has initiated its first pricing revision in ten years with an anticipated increase in payments. On the supply side, labs are challenged to add new tests with little increase in financial and human resources. For most labs it may even mean doing more with less. There is also a lack of trained lab technologists, so there is a decreasing availability of human resources needed to run the more complex new set of molecular and histological tests and immunoassays. Therefore there has been a proliferation of test and lab automation tools launched that remove precious human resources from mundane pre-analytical and sample tracking tasks to make time for more sophisticated ones. This phenomenon was once thought to be the purview of core lab biochemistry and immunoassays but automation is becoming a common feature hematology, blood banking, microbiology, and histology. This emphasis on automation has created further consolidation of laboratory testing to large core labs. More and more assays in coagulation, infectious diseases, proteins, diagetes and even HPV are developed for automated clinical analyzers used in the core lab. Systems for urinalysis, coagulation and microbiology are ready to take their place along side the hematology, chemistry and immunoassay instruments – all located in a single core lab. In larger labs they may be linked to a common track line. Getting information to care givers and patients is now not an added plus, it is a prerequisite of all lab operations. Thus the next 3-5 years will see an intensification of the healthcare industry's emphasis on informatics, wireless communications, data networking and cost/effective healthcare delivery. The reorganization of decentralized health care delivery worldwide and patient-focused medicine are having an enormous impact on the role of medical devices and diagnostic services in healthcare. Technological advancements, specifically those in device Growth Rate by IVD Sector

- 3. miniaturization, data digitization, wireless communications and the Internet, form a technical synergy that will permit IVD tests and devices to maintain a central role in disease management. In the area of test economics, outcomes based disease management establishes guidelines and directives for patient care. This is having a significant effect on the use of new tests, which have to prove their added value to patient care. It also affects how many and which tests are recommended and thus reimbursed for a specific disease group. Health insurance companies such as Kaiser Permanente, Aetna and UnitedHealth along with pharmacy benefit organizations such as Medco are mining their extensive databases to look for correlations between testing patterns and patient outcome. It is expected that these would then be translated into test usage guideline. For More Information, readers will want to consult Kalorama Information’s The Worldwide Market for In Vitro Diagnostic Tests, 9th Edition. This updated report presents the trends, technologies, customer needs and major suppliers with an eye on how they are shaping the IVD industry. “…A number of world events bode well for the future of medical devices including IVDs.”

- 4. The Worldwide Market for In Vitro Diagnostic Tests 9TH EDITION The biennial edition of Kalorama’s comprehensive look at the in vitro diagnostic market is coming soon. Total Market Coverage In nine best-selling editions, Shara Rosen has detailed the market for in vitro diagnostic (IVD) testing, throughout the world, in one complete volume. Market numbers for business planning matched with a discovery of the trends that are impacting the industry in every IVD segment: Clinical Chemistry – Core Lab, Molecular Diagnostics, Point of Care, Histology and Cytology, Testing Services, IT in IVD, Test Services, CTCs, Blood Banking Diagnostics, Microbiology and Virology, Hematology and Immunoassays. The report, The Worldwide Market for In Vitro Diagnostic Tests, combines real industry knowledge with an exhaustive review of the medical, business, and company literature. Market sizes, forecasts and shares are provided, as well as a geographic breakdown of the segments, where possible. Superior Trend Coverage There are many sources for what happened in a market last year. Kalorama Information’s unique report provides the reasons ‘why’ events happened. Changes in technology development, regulatory and reimbursement issues, clinical care, and business environments are discussed. Current market numbers are presented for 2011, with projections given through 2016. A Truly Global Resource From the first edition, this report was designed as a global resource in order to give market-watchers a true picture of the industry. IVD is a worldwide business. While the US is a large healthcare market, much of the dynamism, the growth, and also competition is occurring in other areas. Many of the most interesting opportunities for companies are occurring in emerging markets. As part of its coverage, the report breaks down the entire IVD market for North America, Europe (EU countries, incl. IVD market sizes by country), Eastern Europe, South America, Asia (Japan, China and India) and Rest of World

- 5. IVD changes constantly. This report keeps up with those changes. The need to know is what’s driving diagnostics. 6 Billion Tests are performed each year. There are over 4,000 test products. Just 2% of the costs of healthcare are spent on testing, but 70% of clinical decisions are made using a diagnostic test product. For infectious disease and cancer, test makers with innovative products can expect opportunities for new business. Personalized medicine is finally on its way and not just for cancer patients. Why? Because pharma companies are getting it – you can’t have a targeted therapeutic without an assay to select a potential user. There has been a significant increase in pharma/Dx collaborations in the areas of neurological disorders, autoimmune diseases and others. For many years, we have heard about investment in emerging markets, the BRIC and others. In some ways it was a lot of rhetoric – it is now a reality and all of the companies involved in emerging markets have reported at least a 15%-20% increase in revenues there and in some cases more. Mobile phones help us all find each other in big box stores, send Instagrams and generally keep in touch. For healthcare providers – laboratory professionals, physicians and nurse practitioners – mobile phone Apps are proving to be an invaluable tool to keep up to date, to research disease guidelines and more. Big data is all the buzz – let us not forget that data mining finds correlations – many of which may have absolutely no significance for the problem to be solved. It is only a beginning to finding real answers that can improve patient care. Is the liquid biopsy using either CTCs or cfDNA coming to routine lab medicine? A sure sign of increased interest and uptake is when test controls and standards are commercialized. In the past few years several companies that market molecular test controls have increased their offerings in this way. The reimbursement conundrum continues – governments want better outcomes but also lower costs, and developed countries are developing new reimbursement methods to counter these forms. “the core lab of biochemistry, immunoassays and hematology still account for most IVD sales but the last few years have seen quite a bit of movement in some areas.” –Author, Shara Rosen

- 6. Extensive Coverage TABLE OF CONTENTS 1 EXECUTIVE SUMMARY Introduction – Doing more with less Scope and Methodology Size and Growth of the Market Market Trends 2 INTRODUCTION Background Report Design Lab Medicine Disciplines And Applications Market Analysis of IVD Market Segments The lure of IVD – new majors and entrants Licenses and distribution agreements Test Services Top Suppliers and Niche players Point of View 3 OVERVIEW OF GLOBAL IN VITRO DIAGNOSTIC MARKETS Background Population and Disease Demographics, Worldwide Chronic Diseases as a Market Driver Cancer Diabetes Allergy The BRIC Effect World Segments of the IVD Market and IVD Market Evolution Specific Country Information The United States of America – a world in flux RUO/IUO Issues The Patient Protection and Affordable Care Act Accountable Care Organizations LDT Oversight Accent on Preventative Care In Patient Bundling Molecular test reimbursement Japan Europe – effects of austerity IVD Directive Update China India Brazil Russia 4 TRENDS AND INNOVATION Background Looking to the East Looking Past the Hospital ER Telemedicine and Home Care Trends Commercialization of Novel Tests EMR Update Wireless Connectivity and Healthcare Efficiencies IVD Apps 5 POINT-OF-CARE TEST PLATFORMS Overview of POC Tests The Major POC Test Players Market Analysis Blood Glucose Monitoring Blood Glucose Self Testing Continuous Self Testing Blood Glucose Testing by Professionals Diabetes Testing – Glycated Hemoglobin The Genetics of Diabetes The Commercial Outlook for POC Tests 6 THE CORE LAB: Core Lab Overview Overview of Chemistry Tests Market Analysis : Leading Suppliers and Growth Potential Lab-based Chemistries Critical Care Analysis Urinalysis The Commercial Outlook for the Core Lab 7 IMMUNOASSAYS Overview of Immunoassays Market Analysis Immunoassay Test Segments - Mature and Emerging Point-of-care OTC and Professional Use The Commercial Outlook for Immunoassays 8MOLECULAR ASSAY PLATFORMS Overview of Molecular Assays Worldwide Opportunities for Molecular Tests Molecular Test User Markets Next generation Sequencing Mass Spectroscopy Molecular Technologies And Players Market Analysis Oncology Inherited Diseases Pharmacodiagnostics Prenatal Chromosome Analysis Tissue Typing The Commercial Outlook for Molecular Tests 9 HEMATOLOGY Overview of Hematology Automation and IT Digital Evolution Decentralized Hematology Testing Market Analysis : Leading Suppliers The Commercial Outlook for Hematology Tests

- 7. 10 COAGULATION Overview of Coagulation / Immunohematology Tests Special Topic Genetics and Personalized Medicine Warfarin Plavix Market Analysis Lab-based Testing Genetic markers of hypercoagulopathies Decentralized Coagulation testing – Professional Use Decentralized Coagulation testing – OTC Platelet Testing Leading Suppliers The Commercial Outlook for Coagulation Tests 11 MICROBIOLOGY AND VIROLOGY Overview of Microbiology / Virology Tests Special Topics Antimicrobial Drug Resistance Genome Sequencing and Mass Spectrometry Sepsis Serology Market Analysis Supplies Chromogenic Media Microbial Identification and Antimicrobial Sensitivity Tests Liquid Microbiology Blood Culture Immunoassays – lab based Immunoassays – rapid Molecular Tests The Commercial Outlook for Microbiology / Virology Tests 12 BLOOD BANKING SERVICES Overview of Blood Banking Blood Management – are all these transfusions good medicine Blood Tracking Chagas Disease Platelet Safety Market Analysis Blood Grouping Immunoassay Screens Nucleic Acid Testing Continues to Grow Leading Suppliers The Commercial Outlook for Blood Banking 13 HISTOLOGY AND CYTOLOGY Overview of Histology / Cytology Special Topics Companies expand with test services Market Analysis Histology/Cytology Traditional Stains Pap and HPV Tests Immunochemistry and In Situ Hybridization Pharmacodiagnostic Histology Digital Imaging Tissue Microarrays Circulating Tumor Cells Chromosome Analysis Flow Cytometry The Commercial Outlook for Histology and Cytology Tests 14 COMPANY PROFILES – THE TOP TIER 15 COMPANY PROFILES – THE SECOND TIER 16 COMPANY PROFILES – NICHE PLAYERS 17 COMPANY PROFILES – BLOOD BANK SPECIALISTS 18 COMPANY PROFILES – COAGULATION SPECIALISTS 19 COMPANY PROFILES – DIABETES SPECIALISTS 20 COMPANY PROFILES – HEMATOLOGY SPECIALISTS 20B – COMPANIES SPECIALIZING IN CIRCULATING TUMOR CELLS 21 COMPANY PROFILES – HISTOLOGY SPECIALISTS 22 COMPANY PROFILES – IMMUNOASSAY SPECIALISTS 23 COMPANY PROFILES – MICROBIOLOGY SPECIALISTS MICRO.DOC 24 COMPANY PROFILES – MOLECULAR ASSAY SPECIALISTS 25 COMPANY PROFILES – POINT-OF-CARE SPECIALISTS 26 COMPANY PROFILES – TEST SERVICE PROVIDERS 27 COMPANY PROFILES – INFORMATION TECHNOLOGY SPECIALISTS 28 COMPANY PROFILES – CORE LAB AND OTHER COMPANIES