14 06-05 Real Estate Investors - Income Tax, Asset Protection, Estate Tax and Succession Planning

•

1 recomendación•1,561 vistas

cost segregation; Nevada Non-Grantor Trusts; pension plans; captive insurance companies; capital gains tax planning (installment sales; deferred sales trusts; section 453(e); charitable remainder trusts; Section 1031 exchanges); non-California entities; problem with California LLCs; prejudice against children as trustees; deferred payment of estate tax; entity planning; valuation; Graegin notes; equalization; independent board of diretors.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (8)

Similar a 14 06-05 Real Estate Investors - Income Tax, Asset Protection, Estate Tax and Succession Planning

Similar a 14 06-05 Real Estate Investors - Income Tax, Asset Protection, Estate Tax and Succession Planning (20)

Último

Último (20)

14 06-05 Real Estate Investors - Income Tax, Asset Protection, Estate Tax and Succession Planning

- 1. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION SUITE 445 12100 WILSHIRE BOULEVARD LOS ANGELES, CALIFORNIA 90025 www.GivnerKaye.com www.MajorTaxProblems.com BRUCE GIVNER (bruce@GivnerKaye.com) OWEN D. KAYE (owen@GivnerKaye.com) KATHLEEN GIVNER (kathy@GivnerKaye.com) NEDA BARKHORDAR (neda@GivnerKaye.com) PHONE (310) 207-8008 (818) 785-7579 FAX (310) 207-8708 (818) 785-3027 June 5, 2014 Real Estate Investors: Income Tax Planning, Asset Protection Planning, Estate Tax Planning, Succession Planning 1. Background. 1.1. Goals v. Solutions. The professional’s job is to meet with the client and confirm all of the facts: (i) names, dates of birth and feelings about each family member; (ii) client’s view of each asset’s FMV, basis, goal (sell or hold); (iii) existing entities and trusts (review tax returns, corporate documents, etc.); and the client’s goals and objectives:1 (a) asset protection planning for themselves? (b) asset protection for their heirs? (c) ordinary income tax planning? (d) capital gains tax planning for a particular asset? (e) estate planning (who gets what and how do they get it)? (f) estate tax planning? Do not assume that, just because you have learned some new strategy, your client will like it. Do not sell “solutions” or “strategies.” If you do you are a peddler, not a counselor. You can’t sell a solution to an undiagnosed problem.2 Put another way: if you have a hammer, the world looks like a nail.3 1 Must also rank the goals and objectives from highest to lowest. There may be more than one that is the “highest.” The highest is always to “maintain dictatorial control of all of my assets until the day I die.” 2 Simon Singer, Simon@ADVCG.com. 3 Psychologist Abraham Maslow, The Psychology of Science (1966).

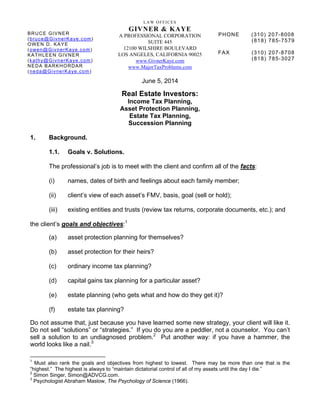

- 2. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 2 of 10 1.2. Wealth. Most wealth in the L.A. metropolitan area (Santa Barbara to San Diego, east to the Desert) has been created in real estate. That which has not been created in real estate has been invested in real estate and transmitted to the next generations in the form of real estate. 1.3. Tax Planning vs. Wealth Creation. Paying taxes is often a cost of wealth creation. Sometimes you must pay taxes on income to accumulate a downpayment. Sometimes you can acquire real estate through tax- favored vehicles, e.g., pension plans and captive insurance companies. 1.4. Interrelationship Of Planning Goals. Often the accomplishment of one goal, e.g., income tax planning, also achieves another goal, e.g., gift tax planning. This is true, for example, in the case of a captive insurance company when it is owned by a children’s or dynasty trust. 2. Ordinary Income Tax Planning. 2.1. Cost Segregation (formerly Component Depreciation). Underused.4 Must hire an appraiser or engineer. 4 Katz, “Cost Segregation: The Art of Maximizing Depreciation Deductions,” 13 Daily Tax Report J-1 (BNA 1/23/09). Mom and Dad Real Estate Management Company Own 100% Children’s Trust $50,000 corpus Series LLC Captive Insurance Company (taxed as a “C” Corporation) Montana $60,000 initial capitalization Own 100% $300,000 per year deductible premium

- 3. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 3 of 10 Subject to several exceptions, MACRS property (placed in service after 12/31/86) is assigned to one of 10 recovery periods: • 3-year property; • 5-year property; • 7-year property; • 10-year property; • 15-year property; • 20-year property; • 25-year water utility property; • 27.5-year residential rental property; • 39-year nonresidential real property; or • 50-year railroad grading or tunnel bore. Caveat: The degree to which the IRS will accept the outcome of so-called “cost segregation studies,” in which commercial firms aggressively categorize building components as personalty in order to obtain much shorter recovery periods, is questionable. The IRS has expressed a concern and has proposed strategies for curtailing what it considers to be an abusive practice. Taxpayers who attempt this strategy are most likely expecting to escape audit, possibly on account of a perceived lack of resources in the IRS for examination of these voluminous studies. BNA Portfolio 531-3rd , VII.G.2.

- 4. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 4 of 10 2.2. Nevada Non-Grantor Trusts. California taxes irrevocable trusts on 3 bases: (i) residence of trustees; (ii) residence of beneficiaries;5 and (iii) California source income. Is the sale of a California apartment building California source income to a non- California resident? R&T Code §17952: “income of nonresidents from stocks, bonds, notes, or other intangible personal property is not income from sources within this State unless the property has acquired a business situs in this State….” Valentino v. FTB, 87 CA4th 1284 (2001): “[p]artnership interests are intangible property….” SBE opinions, though technically nonprecedential, have also construed an LP interest as an intangible. Appeal of Amyas and Evelyn P. Ames, 87-SBE-042: limited partnership formed under Missouri law had a principal business activity concerning real property located in L.A. The GPs were located in California. While the partnership was in existence, the LPs did not pay any California taxes because rental income from the property was offset by accelerated depreciation. Just before foreclosure several LPs sold their LP interests to the GPs. There were gains due to the reduction in bases. The FTB demanded they that file California returns for the sale of the LP interests. The LPs argued that the sale of the LP interests was a sale of intangible personal property and not taxable in California but, instead, in their home states. The FTB argued that those LP interest acquired a business situs in California. The SBE concluded that the LPs had made no attempt to localize their LP interests in California; the gain did not result from the partnership operations but from the Limited partners’ sale of intangible property. Bruce E. Colegrove, Case No. 32604 (2000). Is income derived from a partnership’s operation of an apartment building in California and the later sale of the building California source income to a non-resident partner? Yes. Here it was the sale of the building that was California source. The sale of his partnership interest would not have been California source. 2.3. Pension Plans. Having a pension plan adopted by the family management company cover the parents and possibly even the children. To the extent that the children are covered, that is free gift/estate tax planning. 5 FTB TAM 2006-002 (2/17/07): if a non-California trustee can make distributions in the trustee’s discretion to a California beneficiary, the trust’s undistributed income is not subject to California tax. There is no resident beneficiary and the trust is not a resident trust.

- 5. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 5 of 10 2.4. Captive Insurance Company. Some owners do not have earthquake coverage. Some owners have 12 or more (not disregarded) LLCs which qualify them to not need to participate in the captive manager’s pool. To the extent that the captive insurance company is owned by a children’s or dynasty trust, that is free gift/estate tax planning. 3. Capital Gains Tax Planning. 3.1. Installment Sales. The problem with a regular installment sale. 3.2. Deferred Sales Trusts. The problem with Deferred Sales Trusts. 3.3. Sales To A Children’s Trust. The problem with a sale to a children’s trust. 3.4. §453(e). The problems with §453(e). 3.4.1. §453A. 3.4.2. Bona Fide Sale? Down payment? Interest rate (is AFR enough)? The Karmazin, Davidson and Woelbing audits and CCA 201330033. 3.5. CRTs. Income for life on what would have otherwise been paid in capital gains tax. Taxes saved on the charitable deduction. Savings due to the tax-exempt nature of a CRT. $10,000,000 for a 66 and 60 year old:

- 6. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 6 of 10 Courtesy of Stu Katz, Vice President, Bernstein: Stu.Katz@Bernstein.com. 310-286-6074.

- 7. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 7 of 10 3.6. §1031. Drop and Swaps: “FTB continues to assert substance over form as a key basis for challenging drop and swap transactions, although they can be done via careful advance planning and execution.” California CPA (May 2014), page 26. By contrast, the IRS has apparently determined that while it does not agree with Bolker, in a 1999 FSA (19995104) re- released 4/29/05: “Although we disagree with the conclusion that a taxpayer that receives property subject to a prearranged agreement to immediately transfer the property `holds’ the property for investment, we are no longer pursuing this position in litigation in view of the negative precedent.” The preferred method is to liquidate the partnership first and then have the partners enter into a contract of sale preferably several months later. 4. Asset Protection Planning. 4.1. Distinguish Three Types Of Creditor Issues. Up. The traditional “piercing the corporate veil.” Advice: the entity should have “adequate capital.” What is “adequate”? No one knows the answer. If the lawsuit is for personal injury it is more likely that the entity will be pierced. Consider one year’s gross revenue. If that is too much, consider one year’s net revenue. Down. You get in a car crash, as a result of which your personal assets are lost. Can the judgment creditor get your interest in the entity? If it is a single member LLC and they put you into bankruptcy, the answer is “yes.” In re Ashley Albright. If it is a multiple member California LLC, e.g., you 90% and a children’s trust 10%, the answer was “yes” for LLCs with “poison pill” operating agreements formed before 1/1/14. However, for California entities formed 1/1/14 going forward Corporations Code Section 17302(c)(2) has been replaced by

- 8. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 8 of 10 Section 17705.03(d) so we now use limited partnerships (with an LLC as the GP) with a “poison pill” feature. Sideways. Both pieces of property are owned by the same entity. If someone dies in one property, can the judgment creditor (heirs of deceased tenant) get the equity in the other property? That’s why each property is in a separate LLC owned by the main entity. 4.2. Non-California Entities. Does a Delaware (or Nevada) LLC help a California owner of a California apartment building? 4.3. Umbrella Policies. March 5, 2012 Forbes: “based on a survey of folks with assets of $5 million and up. One in five of those surveyed don’t have an umbrella policy, and of those who do have a policy, nearly one in four reported having less than $5 million in coverage. … The typical annual cost quoted by ACE for a client with one home, two cars and two drivers is $383 for $1 million in coverage, $474 for $2 million in coverage, $608 for $5 million in coverage and $999 for $10 million in coverage. Add two more homes, two more cars, one boat under 26 feet, and a driver under age 25, and it costs $563 for $1 million in coverage, $1,578 for $10 million in coverage, for example.” 4.4. The Problem With LLCs. January 1, 2014: repeal of the Beverly-Killea LLC Act and its replacement by the Revised Uniform LLC Act. Old §17302(c)(2) replaced by §17705.03(d). Limited partnerships have §15907.03(d). 5. Estate Tax Planning. 5.1. Prejudice Against Children As Trustees. 5.2. Deferred Payment Of Estate Tax. 5.2.1. §6166: Mandatory Deferral. Planning while the clients are alive to meet the 35% of the adjusted gross estate test. Rev. Rul. 2006-34: day-to-day operations and activities are often performed by independent contractors, such as property management companies. That fact will not prevent the business from qualifying as an active trade or business, provided that the activities of the independent contractors are not so extensive as to reduce the activities of the business to the level of merely holding investment property. Situation 3: the decedent owner

- 9. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 9 of 10 20% of the stock of the management company which provided all necessary services as to the management and maintenance of the office park and that was sufficient to conclude that the management company was actively managing the office park. Therefore, the decedent’s interest in the office park qualified as an active trade or business under §6166. 5.2.2. §6161: “Discretionary” Deferral. It is not really discretionary. 5.3. Entity Planning. GRATs. Private Annuities. SCINs. Part-gift, part-sales. See above discussion of Karmazin, Woelbing and Davidson audits. 5.4. Valuation. 5.4.1. Mellinger. 5.4.2. Attorney-Client Privilege. 5.5. Generational Split Dollar. 5.6. Irrevocable Insurance Trusts. 5.7. Graegin note. Ensure that a grandchildren’s trust has a lot of assets to act as the lender. 5.8. Testamentary Charitable Lead Annuity Trust. Do no planning while you are alive and eliminate estate tax through an amendment to the family trust. 6. Succession Planning. 6.1. Equalization. 6.1.1. The Problem. Will one child inherit the investment real estate while the other inherits liquid assets and/or the residence? Is there a need for a life insurance or a promissory note to effect the equalization?

- 10. LAW OFFICES GIVNER & KAYE A PROFESSIONAL CORPORATION Real Estate Investors June 5, 2014 Page 10 of 10 6.1.2. Insurance As One Solution. 6.2. Prejudice Against Children As Trustees. CPAs. California Professional Fiduciaries. Drafting lawyer as sole trustee: certificate of independent review. 6.3. Independent Board of Directors. Starting it while the parents are alive and healthy. 6.4. Control. Is one child going to control the real estate empire while others are going to merely collect rent? Does that increase the importance of having an independent third party, e.g., the CPA, as the trustee? 7. Conclusion. 7.1. Process. Planning is a process, not an answer. It is best started early, while the parents are healthy. The CPA should raise it early in the relationship with the client. 7.2. Maintenance. You must revisit the process annually. The parents’ feelings will evolve over time, as their assets change and as their feelings about their heirs evolve. The child who is perfect at 25 becomes a problem at 45 when married to that evil in-law. 7.3. Dispute Resolution Mechanism. Assume no planning can be implemented because the parents cannot reach a solid decision. At least implement something in their estate plan documents or in the entity documents, e.g., the partnership agreement or in the operating agreement, that provides for a dispute resolution mechanism that avoids the need for the children to address their grievances in court. That might be nothing more than having an independent third party as trustee in control of all of the assets. Recognize that “no contest clauses” are effectively unenforceable in California since 1/1/10.