Production of mea triazine m1

•

0 recomendaciones•3,018 vistas

The document is a project report for manufacturing MEA TRIAZINE from paraformaldehyde and monoethanol amine. MEA TRIAZINE is used as H2S scavanger in crude oilfields.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a Production of mea triazine m1

Similar a Production of mea triazine m1 (20)

Más de Chandran Udumbasseri

Más de Chandran Udumbasseri (20)

Último

Último (20)

Production of mea triazine m1

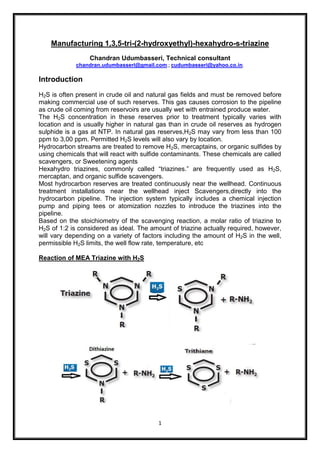

- 1. 1 Manufacturing 1,3,5-tri-(2-hydroxyethyl)-hexahydro-s-triazine Chandran Udumbasseri, Technical consultant chandran.udumbasseri@gmail.com.; cudumbasseri@yahoo.co.in. Introduction H2S is often present in crude oil and natural gas fields and must be removed before making commercial use of such reserves. This gas causes corrosion to the pipeline as crude oil coming from reservoirs are usually wet with entrained produce water. The H2S concentration in these reserves prior to treatment typically varies with location and is usually higher in natural gas than in crude oil reserves as hydrogen sulphide is a gas at NTP. In natural gas reserves,H2S may vary from less than 100 ppm to 3,00 ppm. Permitted H2S levels will also vary by location. Hydrocarbon streams are treated to remove H2S, mercaptains, or organic sulfides by using chemicals that will react with sulfide contaminants. These chemicals are called scavengers, or Sweetening agents Hexahydro triazines, commonly called “triazines.” are frequently used as H2S, mercaptan, and organic sulfide scavengers. Most hydrocarbon reserves are treated continuously near the wellhead. Continuous treatment installations near the wellhead inject Scavengers,directly into the hydrocarbon pipeline. The injection system typically includes a chemical injection pump and piping tees or atomization nozzles to introduce the triazines into the pipeline. Based on the stoichiometry of the scavenging reaction, a molar ratio of triazine to H2S of 1:2 is considered as ideal. The amount of triazine actually required, however, will vary depending on a variety of factors including the amount of H2S in the well, permissible H2S limits, the well flow rate, temperature, etc Reaction of MEA Triazine with H2S

- 2. 2 Certain length of the pipeline where the scavenger is injected is provided to allow contact between the scavenger and the H2S This product, on average, is three times more concentrated than the average competing scavenger treatment product This product is developed for drilling systems – protonated Triazine molecule reacts faster As Hydrogen sulfide is toxic its removal will improve safety in the drilling rig work place It is safe, effective and quick removal of hydrogen sulfide gas from process systems It greatly reduces corrosion of assets and maintains the flow pipeline’s life. The Dithaizine which is the reaction product as shown above can be removed easily from pipelines. preserve expensive drilling equipment from the corrosive effects of H2S gasses This Hydrogen Sulfide Scavenger for Water Based Systems converts H2S to safe, non‐solid byproduct Corrosion Inhibitor; 6 ppm Removes 1 ppm H2S. Reaction: Formaldehyde reacts with mono ethanolamine to form above product. Material Balance = 3x 61.08 g + 3x 30.026 g => 219.28g + 3x18g = 183.24 + 90.078 => 219.28 + 54 = 67.09% + 32.91% => 80.24% + 19.76% Product information Name 1,3, 5 tri-(2-hydroxyethyl)-hexahydro-s-triazine Formula C9H21N3O3 CAS No 4719-04-4 HS code 2933.69.90 Molecular weight 219.28g Boiling point: 360.1°C (rough estimate) Density 1.1269 (rough estimate)

- 3. 3 Refractive index 1.4830 (estimate) pka 14.16±0.10 (Predicted) Water Solubility Soluble (>=1 g/100 mL at 24 ºC) Appearance viscous yellow liquid Safety Hazard Codes Xn Risk Statements 22-43 Safety Statements 24-37 RIDADR 2810 Hazard Class 6.1(b) Packing Group III Toxicity LD50 oral in rat: 763mg/kg Raw material used 1. Paraformaldehyde Color white free flowing powder CAS No 30525-89-4 Content 96% Water content 4% +/- Particle size 250-350um Ash 0.05% Bulk density 650-850 kg/m3 Melting point 120-175o C pH 4-7 2. Mono ethanol amine Appearance colourless to light yellow slightly viscous liquid Color, APHA 25 CAS No 141-43-5 Formula C2H7NO Molecular weight 61.1 Purity >99% Distillation 166-178o C

- 4. 4 Water content 0.5% Specific gravity, 20o C 1.015 – 1.02 3. Formaldehyde solution CAS No 50-00-0 Molecular weight 30.03 Code Flammable liquid (Class 3.1) Specification Formaldehyde, % w/w, min. 37.00 – 40 Iron, ppm max. 2.00 pH 2.603.00 Method of Manufacturing Reactor Reactor 2000 Lts Utilization 75% capacity (1500Lts) Quantities 1. Para formaldehyde 1106.5 Kg 2. Mono ethanol amine 566.24 Kg Process 1. Paraformaldehyde is reacted with mono ethanol amine at a low temperature of 10 to 25o C. Para formaldehyde is taken as 96% pure and mono ethanol amine >99% purity. 2. Mono ethanol amine is taken in the reactor and cooled to 10 to 20o C by jacketed cooling. 3. Agitate with anchor type agitator at 40 to 60 rpm. 4. Cool the MEA to below 15o C under agitation. 5. Start adding paraformaldehyde powder slowly keeping the temperature at 10 to 20o C. 6. Continue addition of paraformaldehyde with control on the temperature Complete the addition in 3 hours’ time. 7. Stop cooling towards the end of addition and allow the temperature slowly to go up to 40o C. 8. Continue the stirring for additional 1hour. 9. Stop stirring and draw a sample for testing 10.Discharge the product Expected output MEA + PF => MEA Triazine + water 1106.5Kg + 566.55(of 96% purity) Kg=> 1324 Kg + 326 Kg 1106.5/3 + 566.55x0.96/3 => 1324 + 324/3 368,8/61.08 + 181.3/30.026 => 1324/219.28 + 108/18

- 5. 5 6.038 + 6.038 => 6.038 + 6 The quantities are 6 times of Kg mols Expected output = 219.28 x 6.038 Kg = 1324Kg Per batch output is 1324 Kg theoretical quantities Practical (98% yield) 1324x0.98 = 1297.6 kgs Output/day No of shifts = 3 Per day output = 1297x3 = 3891 Kgs/day Per month output, (25days) = 3891x25 = 97,275 Kgs/month This is 80% MEA Triazine Dilution to 40% 80% Product 97275Kgs/month Water 97275Kgs 40% Product 194550 Kgs/month Per day production => 7782 kgs Raw material consumption/month Output = 97,275 Kgs./month Paraformaldehyde Per day 1700 kgs Per month 1700x25 = = 42,500 kgs MEA Per day 1106x3 = 3318 kgs Per month 3318x25 = 82,950 Kgs Raw material cost/month 1. Paraformaldehyde,@ Rs 60,42500 x 60 = 25,50,000 2. MEA @ Rs 90, 82950 x 90 = 74, 65,500 3. Water for dilution,@Rs 5, 97275 Kgsx5 = 486375 Test method: Analysis of tertiary amine content Aim: Triazine contains three tertiary nitrogen atoms. So the equivalent weight is one- third of molecular weight. Phenyl iso thiocyanate reacts with primary and secondary amine and leave tertiary amine unreacted. Required 1. Iso propyl alcohol 2. Phenyl isothiocynate 3. Bromocresol blue indicator(At pH 3.8, the indicator turns yellow and at pH 5.4, the indicator is blue-green) 4. 0.1N HCl standard solution 5. pH meter 6. Magnetic stirrer with magnetic rod

- 6. 6 Procedure: The percentage of tertiary amine present in the reaction product may be determined by titration with standard HCl solution. (Phenyl iso thiocyanate reacts with primary and secondary amine and leave tertiary amine unreacted). 1. Weigh 1 g of the sample in a 100ml beaker 2. Add 50ml of iso propanol and 5 ml of phenyl iso thio cyanate 3. Mix well by magnetic stirrer 4. Allow the mixture to stand for 30 minutes 5. Add 2 drops of bromophenol blue indicator 6. Take Standard 0.1N HCl in the burette 7. Place the beaker with magnetic rod on the magnetic stirrer 8. Stir the solution and start adding HCl drop wise from the burette 9. Note the pH of the solution and titrate with HCl until the solution pH is 3.5 (the indicator color changes from blue to yellow) 10.Note the volume of 0.1N HCl consumed and calculate percentage amine (Triazine) 11.Calculation: Equivalent weight of Triazine = Mol weight/3 = 219.28/3 = 73.09 (Three tertiary Nitrogen atoms) Costing Unit Raw material cost (URMC) Price of paraformaldehyde Rs 60/Kg Price of Monoethanol amine Rs 90/Kg Formula weight of raw materials Paraformaldehyde 67.09% Mono ethanol amine 32.91% URMC 0.6709x60 +0.3291x90 = 69.88/Kg Yield % = 98% URMC (Adjusting yield %) = 69.88/0.98 = 71.30 /Kg Add interest for 90 days at 12% = 0.0325x71.30 = 2.32/Kg Add Factory overhead at 10% = 10 Total = 71.30+2.32+10 = 83.62 Tax at 3.25% = 0.325x71.30 = 2.32 Ex-Factory Cost = Rs 85.94 /Kg Add profit margin, 15% = 83.62 + 2.32 +10.7 = 96.64 Ex-Factory Cost = Rs 85.94 /Kg; Selling price Rs 96.6/Kg Note: Costing should be modified based on new taxation rules and raw material cost

- 7. 7 Cost evaluation Fixed cost 1. Land cost, 600 sq ft = 2,50,000 2. Building cost, 500 sq ft = 9,00,000 3. Machinery cost,(machines + tanks) 3.1. SS304 jacketed reactor,2000 Lt = 2,00,000 3.2. SS304 Storage tank, 5000 Lt = 1,20,000 3.3. Chilling plant 75T = 5,00,000 3.4. Fork lift = 6.50,000 4. Laboratory instruments, = 3,00,000 5. Others (fittings, etc.) = 2,00,000 6. Office items = 2,00,000 ----------------------- Total fixed cost = 33, 20,000 Variable cost/month 1. Manpower 1.1. Supervisor cum chemist 1no , = 50000 1.2. Fork-Lift operator , 1no = 25000 1.3. Labour, 2nos = 40000 ---------------- Total labour cost = 1, 15,000 2. Overhead 2.1. Electricity (Rs 5.43/KWH) = 10,50,000 2.2. Tools & others = 1,00,000 ------------------ Total Overhead = 11.50,000 3. Raw material 3.1. Paraformaldehyde@ Rs 60/kg = 25,50,000 3.2. Monoethanolamine @ Rs 90/kg = 74, 65,500 3.3. Water @ Rs 5/kg = 04,86,375 ---------------------- Total =1, 05, 01,875 Total Variable cost , per month = 1,15,000 + 11,50,000 + 1,05,01,875 =1,17,66,875 Total variable cost per year = 11766875x12 = 14, 12, 02,500

- 8. 8 Working capital Per month =1, 17, 66,875 Per year =14, 12, 02,500 Total fixed capital investment (per year) 1. Fixed capital = 33,50,000 2. Working capital =14,12,02,500 --------------------- Total =14, 45, 52,500 Cost of production (per year) 1. Total recurring cost (working capital) 14,45,52,500 2. Depreciation building (5%)=9,00,000x0.05 45,000 3. Depreciation machinery (10%)=14,70,000x0.1 1,47,000 4. Depreciation Lab instruments (10%) = 3,00,000x0.1 30,000 5. Depreciation others (10%) =2,00,000x0.1 20,000 6. Depreciation Office items (25%)=2,00,000x0.25 50,000 7. Interest on total capital investment (15%) = 144552500x0.15 2,16,82,875 --------------------- Total 16, 65, 27,375 Turnover per year Per day production = 7782 Kgs Unit price = 102 (Taken ONGC price) Daily sales = 793764. Yearly = 793764x300 = 238129200 Net profit Turnover-cost of production = 238129200-166527375 = 71601825 Net Profit Ratio = = =30.07% Rate of return = = = 49.53% Break Even Analysis Fixed cost 1. Insurance 10,00,000 2. Depreciation building (5%)=9,00,00,000x0.05 50,000

- 9. 9 3. Depreciation machinery (10%)=1470,000x0.1 1,47,000 4. Depreciation Lab instruments (10%) = 3,00,000x0.1 30,000 5. Depreciation others (10%) =2,00,000x0.1 20,000 6. Depreciation Office items (25%)=2,00,00x0.25 50,000 7. Interest on total capital investment (15%) = 144552500x0.15 2, 16, 82,875 8. Salary and wages 40% = 115000x0.4x12 = 5,52,000 9. Other overheads 40% = 1150000x0.4x12 = 55,20,000 Total 2, 90, 51,875 Profit before tax = 7, 16, 01,825 Fixed cost + Profit = 29051875 + 71601825 = 100653700 Break Even Point = = = 28.86% Generated by Chandran Udumbasseri Consultant