2015 Private label sourcing survey

•

4 recomendaciones•5,885 vistas

Deloitte’s 2015-2016 Private Label sourcing survey highlights shifts in market trends and uncovers leading Private Label sourcing practices. With 388 respondents from apparel, general merchandise, and grocery retailers, the 2015-2016 survey builds on the findings of our 2012-2013 assessment and dives deeper into industry trends. For more information, please visit: www.deloitte.com/us/2015privatelabel.

Recomendados

Recomendados

Más contenido relacionado

Más de Deloitte United States

Más de Deloitte United States (20)

Último

Último (20)

2015 Private label sourcing survey

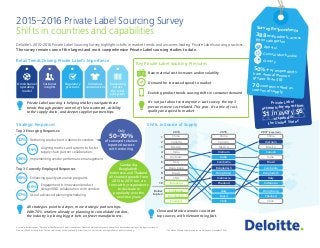

- 1. 2015–2016 Private Label Sourcing Survey Shifts in countries and capabilities Deloitte’s 2015–2016 Private Label Sourcing Survey highlights shifts in market trends and uncovers leading Private Label sourcing practices. The survey remains one of the largest and most comprehensive Private Label sourcing studies to date. As used in this document, “Deloitte” means Deloitte LLP and its subsidiaries. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Key Private Label Sourcing Pressures Shifts in Source of Supply Raw material cost increases and/or volatility Demand for increased speed to market Evolving product trends causing shifts in consumer demand Cambodia, Bangladesh, Indonesia and Thailand all showed growth from 2013 to 2015 but are forecast by respondents to decrease in popularity over the next two years Private Label accounts for more than $1 in every $6 of spend in the United States* 1 2 3 4 5 6 7 8 9 10 Below top ten Bangladesh Canada Cambodia Indonesia Hong Kong Thailand Vietnam Italy Chile India Mexico China Brazil Vietnam China Mexico Cambodia Bangladesh Hong Kong Indonesia Thailand Italy India Chile China Canada Mexico India Italy Hong Kong Brazil Chile Indonesia Bangladesh Cambodia Thailand Vietnam 20152013 2017 (expected) Brazil Canada * The state of Private Label around the world (Nielsen, November 2014) It’s not just about cost anymore: Last survey, the top 3 pressures were cost-related. This year, it’s a mix of cost, quality and speed to market All strategies point to deeper, more strategic partnerships. With 76% retailers already or planning to consolidate vendors, the industry is placing bigger bets on fewer manufacturers. China and Mexico remain consistent top sources, with Vietnam rising fast. Strategic Responses Top 3 Emerging Responses: 32% Reshoring production to domestic vendors 28% Implementing vendor performance management Top 3 Currently Employed Responses 60% Enhancing quality assurance programs 57% Use of advanced planning/scheduling 29% Aligning metrics and systems to foster supply chain partner collaboration 60% Engagement in innovation/product design/R&D collaboration with vendors Only 50–70% of surveyed retailers reported success with reshoring Survey Respondents 388 respondents acrossthree categories: 50%+ of respondentshave annual revenue greater than $1B 70 countries noted assources of supply Apparel General Merchandise GroceryRetail Trends Driving Private Label’s Importance Private Label sourcing is helping retailers navigate these trends through greater control of the assortment, visibility to the supply chain, and deeper supplier partnerships. Innovating across the retail ecosystem Omnichannel operating model Customer insights Regulatory pressures Conscious consumerism

- 2. This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering business, financial, investment, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates, and related entities shall not be held responsible for any loss sustained by any person who relies on this publication. Copyright © 2015 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited. About The 2015–2016 Private Label Sourcing Survey was conducted online by Deloitte in 2015. Over 388 respondents provided input across three spend categories (Apparel, General Merchandise and Grocery). Because respondents could submit responses for multiple sub-categories, over 700 responses were collected. Approximately 53% of respondents are from companies with annual revenues greater than $1B, and 42% of the companies represented have more than 10,000 employees. Learn more Visit us: www.deloitte.com/us/2015privatelabel Engage Follow us on Twitter: @DeloitteCB #PrivateLabel15