Consumer Industry M&A Roundtable Series

•

0 recomendaciones•463 vistas

We gathered a preeminent group of industry experts and leaders to discuss trends across the Fast Moving Consumer Goods (FMCG) industry, including wide variations in asset intensity and returns within and across Consumer subsectors for FMCG companies. Deloitte analysis shows that there is potential for great value creation for CPG companies by adopting asset-lite models. Explore our latest analysis and industry perspectives from the new Deloitte M&A Roundtable series. Visit us here to learn more: https://deloi.tt/3aB3959

Recomendados

Recomendados

Más contenido relacionado

Más de Deloitte United States

Más de Deloitte United States (20)

Último

Último (20)

Consumer Industry M&A Roundtable Series

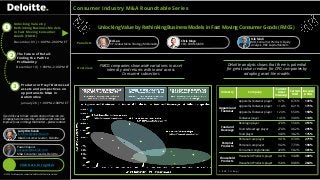

- 1. Unlocking Value by Rethinking Business Models in Fast Moving Consumer Goods (FMCG) © 2020. For information, contact Deloitte Touche Tohmatsu Limited. Larry Hitchcock lhitchcock@deloitte.com M&A Consumer Leader, Deloitte If you’d like us to have conversation on how can you company become asset lite, variabilize cost base and improve focus on things that matter – please contact: Consumer Industry M&A Roundtable Series Predator or Prey? Distressed assets and perspectives on opportunistic M&A in Automotive January 28 | 1:00PM–2:00PM ET The Future of Retail: Finding the Path to Profitability December 10| 1:00PM–2:00PM ET Unlocking Value by Rethinking Business Models in Fast Moving Consumer Goods (FMCG) December 03 | 1:00PM–2:00PM ET 1 2 3 Pawan Kapoor pakapoor@deloitte.com M&A Consumer Leader, Deloitte Click here to register Ed Lee VP, Global Menu Strategy, McDonalds Chris Moye CEO, CROSSMARK Nik Modi MD, Consumer Products Equity Analysis, RBC Capital Markets FMCG companies show wide variations in asset intensity and returns within and across Consumer subsectors Deloitte analysis shows that there is potential for great value creation for CPG companies by adopting asset-lite models Overview 1. (PPE, 3 Yr. Avg.) Industry Company Current Asset Intensity1 Current ROA1 Increase in ROA Apparel and Footwear Apparel & Footwear player 9.7% 87.6% 141% Apparel & Footwear player 11.4% 82.1% 171% Apparel & Footwear player 12.3% 65.0% 150% Footwear player 14.5% 39.0% 114% Food and Beverage Beverage player 27.0% 55.8% 351% Food & Beverage player 27.4% 46.2% 295% Food player 14.8% 38.2% 115% Personal Products Personal care player 14.1% 97.0% 271% Personal care player 13.2% 77.3% 198% Consumer conglomerate 22.9% 58.2% 301% Household Products Household Products player 14.1% 138.6% 389% Household Products player 15.8% 80.8% 264% Panelists

- 2. © 2020. For information, contact Deloitte Touche Tohmatsu Limited. Larry Hitchcock lhitchcock@deloitte.com M&A Consumer Leader, Deloitte If you’d like us to have conversation on how can you company become asset lite, variabilize cost base and improve focus on things that matter – please contact: Consumer Industry M&A Roundtable Series Pawan Kapoor pakapoor@deloitte.com M&A Consumer Leader, Deloitte Click here to register Panelists Consumer Products companies’ shareholder returns lag their peers in the Technology and Healthcare industries while simultaneously having higher asset intensity (35%, relative to 4% in Consumer Electronics). In this panel discussion, we explore how Consumer companies could shift towards asset-lite trends and how this shift to lower asset intensity could bolster returns. And much more… • TBD • TBD • TBD Key Insights What are the limitations of large FMCG companies (especially in Food and Beverage) to work with channel partners, specializing in parts of the value chain where they can create maximum shareholder returns Ways in which consumer brand owners compete with scaled retail players such as Amazon, Walmart through Direct to Consumer (DTC) infrastructure. With ecommerce at ~20% of consumer spend (even during COVID), is it apparent that Brick & Mortar and Online channels will co-exist in the near- and medium-terms? What opportunities emerge (for existing or new players) if consumer companies choose to adopt asset lite models emerge – for example, how can last mile delivery services provide opportunity to launch Direct to Consumer (DTC) models for consumer brands While Consumer sub-sectors (Apparel, Personal Products, Food & Beverage) exhibited wide variation in asset intensity and returns; Consumer Electronics companies move to extremely asset-lite models In consumer industry, quality risk associated with food safety was a barrier, however, now options exist (scaled TPMs, channel / merchandizing partners) to reduce asset intensity Outsourcing may be cost neutral or negative in some cases, however, it prevents heavy CAPEX investment that is needed to keep up with the changes /disruptions (such as technology advancements). Companies are operating at low R&D spend (2-3% of revenue) while spending huge sums on non-core activities Deloitte Provocation Unlocking Value by Rethinking Business Models in Fast Moving Consumer Goods (FMCG) Ed Lee VP, Global Menu Strategy, McDonalds Chris Moye CEO, CROSSMARK Nik Modi MD, Consumer Products Equity Analysis, RBC Capital Markets Predator or Prey? Distressed assets and perspectives on opportunistic M&A in Automotive January 28 | 1:00PM–2:00PM ET The Future of Retail: Finding the Path to Profitability December 10| 1:00PM–2:00PM ET Unlocking Value by Rethinking Business Models in Fast Moving Consumer Goods (FMCG) December 03 | 1:00PM–2:00PM ET 1 2 3