FirstPartner 2015 Transformation of Retail Payments Market Map

•

6 recomendaciones•1,668 vistas

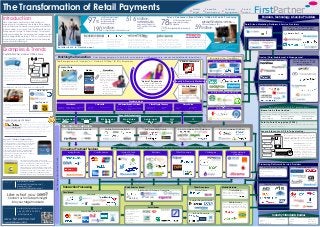

Download a free copy from our website at www.firstpartner.net. Omni-channel commerce is becoming an imperative for retailers as consumers increasingly mix on-line, mobile and in-store product selection & purchasing. As a result, the traditional Point of Sale payment model is transforming. This Market Map summarises the increasing convergence and interchangeability between PoS, m-commerce & e-commerce payment models and the complex value chain facilitating it.

Recomendados

Recomendados

Más contenido relacionado

Destacado

Destacado (15)

Último

Último (8)

FirstPartner 2015 Transformation of Retail Payments Market Map

- 1. Omnichannel strategy includes a range of innovative in store technologies, apps and early adoption of Apple Pay 97% of US consumers aged 18-29 actively use a smartphone while shopping in Store 2 Sources: 1) Accenture The Seamless Consumer Retail Survey Feb 2014 2) Thrive Analytics & Local Search Association 3) Alibaba Group satement Oct 2014 4) eMarketer estimate Aug 2014 5) Juniper Research NFC Mobile Payments 2014-2019 Image: Shopkick Initiatives include apps to enhance in-store experience & trials of virtual stores, loyalty linked mobile payments, beacons & a Goggle Glass shopping app Savvy Consumers Blend Online, Offline & Mobile Purchasing Retailers Rush to Omnichannel 78% 72% Buy digitally after browsing in store 516 Million mobile users of NFC contactless payment services by the end of 2019, up from 101 million in 2014 5 Active Alipay mobile wallet users190 3 Million estimated US Smartphone consumers redeeming a mobile coupon for online or offline shopping in 2014 Concept store to promote Hointer’s retail platform. Items are chosen via mobile app & robot pre-picked to try in- store. Self-service payment via tablet based kiosk in the changing booth Introduction Omni-channel commerce is becoming an imperative for retailers as consumers increasingly mix on-line, mobile and in-store product selection & purchasing. As a result, the traditional Point of Sale payment model is transforming. This Market Map summarises the increasing convergence and interchangeability between PoS, m-commerce & e-commerce payment models and the complex value chain facilitating it. Examples & Trends Enriching the Transaction The Emergence of “Hybrid” or “Online 2 Offline” (O2O) Payments Engaging the Consumer Branded Loyalty Shemes Combining payment choice & convenience with discovery, recommendations & incentives Proximity Marketing Transaction Processing www.firstpartner.net Richard Warren Helen Motha rwarren@firstpartner.net +44 (0) 870 874 8700 @firstpartner hello@firstpartner.net Like what you see? Contacts Authors www.firstpartner.net Copyright FirstPartner Ltd 2015 hmotha@firstpartner.net Contact us for in-depth insight into your target markets! Transaction Processing Card Based Card & Debit Networks Acquirers Retail Banks Retail banks still play a key role as the ultimate source of consumer funds in developed markets and as card issuers Mobile Wallet Platforms Enablers, Technology & Service Providers Other Data Driven Marketing Platforms & Service Providers Cross Channel Data Tracking, Analytics & Customer Profiling Loyalty & Couponing Industry Standards Bodies NFC Forum Sim Alliance Mobey Forum GSMA OMA ETSI Mobile Payments Payment Processing Mobile Money Platforms Token Service Providers Mastercard Digital Enablement System Visa Token Service Amex Most Leading PSPs & Processors Processing Platforms & Service Providers 4 59Million Transport as a Consumer Catalyst? Stored Value -PayPal -Skrill -StarBucks -M-Pesa Card on File - Amazon - iTunes - Visa Checkout Card Linked - Apple Pay - Samsung - Google Wallet - Vodafone Wallet -MasterPass -v.Me ACH Based/Bank Acc. Linked -MCX -Zapp -WeChat -iDeal -Bancontact/ Mister Cash Virtual/Crypto Currency - Blockchain - bitinvest - cryptex - xapo Wallets & Apps Consumer Payment Services Consumer Payment Services How it Works: Apple Pay How it Works: MCX PayPal & WeChat: Online 2 Offline Focus: Merchant PayPal Consumer Funding (PayPal balance/card/bank) $ Check in: ePoS $ Beacon or App PayPal & WeChat combine “online” payment experiences with physical transactions. PayPal uses beacons or app generated codes to check in & facial authentication. WeChat integrates into the retailers PoS through an API. Crypto Currencies At Retail merchants to use Bitcoin online and at Point of Sale. While processors are attracting venture funding, major value fluctuations & fraud risks will limit widespread consumer adoption. As regulators work to determine the legitimacy & role of crypto currencies, a number of bitcoin wallets , debit cards & processors are allowing consumers & US retail consortium MCX launches its CurrentC mobile payment & loyalty scheme in 2015. Backed by merchants including Walmart, Target & Best Buy, payment processing is via a dedicated ACH network operated by FIS to speed settlement & lower transaction costs. QR codes will be used to maximise handset compatibility but MCX hints NFC & beacons may also be supported. Apple Pay has re-energised expectations for NFC payments. Processing is via existing card infrastructure with leading schemes, issuing banks & acquirers supporting. TouchID biometric authentication coupled with simple NFC payment, Apple Watch support & EMVCo standard tokenisation sets the bar for frictionless, secure online & offline mobile payments. Consumers need a compelling use case to adopt a new payment paradigm Transport has been a major enabler of contactless & remote payment uptake as rapid transactions are of immediate value to traveller & operator. 1 of US consumers buy in store after browsing digitally Card Linked Marketing Authentication Technologies Securing Accounts & Transactions Secure Elements, HCE & Tokenisation: Token-xxxx-xxxx-xxxx-xxxx-xxx Merchant Token Service Provider Card Issuer Acquirer Card Network $ a.name 1234-5678-9012-3456 01-12-2016 789 Token Vault EMV cards & early NFC services store encrypted account credentials & payment apps in a physical Secure Element (SE). Host Card Emulation (HCE) uses Tokenisation & executes the application on the host device. Tokenisation replaces real account details with an encrypted token which is held on the device & passed to the merchant. True account details are stored & tokens are generated & matched in a secure, managed vault. Biometric Authentication: Brought to the forefront by Apple Pay, aims to replace PINs with a frictionless yet accurate & reliable user experience. - Fingerprint - Vein scanning - Facial recognition - VoiceRecognition - Retina Scanning - ECG signature Point to Point Encryption (P2PE): Encrypts payment credentials at point of sale so they are never transmitted or stored “in the clear” by merchants. Fraud Detection TheTransactionValueChain Mass Transit Taxi Payment Mobile Money Emerging market mobile money & developed market P2P schemes support in store payments Point of Sale Mobile Wearables Smart watches and glasses with biometric authentication or phone pairing & basic NFC bands for low value payments promise a simple user experience - Swatch - Apple Watch - Samsung Gear/PayPal - Gemalto mini tag - Barclays bPay Payment Card Will continue to account for the majority of non cash transactions in developed markets for the foreseeable future Instore, on-line & mobile experiences merge as consumers “Hybrid” Payments pick & mix how they browse, select and buy e and m-commerce Click & collect & in app payments for physical goods APIs Open APIs are seen by some payment schemes & PSPs as important enablers, maximising the opportunity for developers to integrate payment & deliver seamless purchasing experiences Device/Card Enablement & Management Coupon/Reward Distribution Retailer & Social Media Apps Merchant Acceptance Retail Payment Terminals Mobile Point of sale (MPoS) PoS Systems & Software E & M Commerce PlatformsE & M Commerce PSPs/Gateways Connectivity Technologies BLE BeaconsQR CodeNFC/Contactless Audio/Light SMS IP 192.11.222.3 Mag Stripe Issuing Banks Mobile Network Operators ChallengersRetailers Other ProcessorsCard Schemes Bank Transfer Based Interbank ACH Scheme Operators MCX (US) ZAPP (UK) Mobile Network Carrier Billing Widely used for virtual goods, processing via the phone bill is being tried for retail Mobile Money Can support retail payments with processing & settlement via the operator mobile money network Other Processors Retailer Prepaid/Loyalty Stored Value Bitcoin Processors Loyalty & Proximity Marketing Having implemented multiple initiatives from single ordering & supply chain systems via staff training to JLAB retail tech business incubator, John Lewis believes 66% of its customers are omnichannel Innovative integration with social media channels, use instore tablets & integration of fulfilment systems EMVCo PCI Global Platform Payment Security FIDO Alliance FirstPartnerMarket Insight Proposition Development Product Launch Customer Engagement The Transformation of Retail Payments FirstPartner EVALUATIO N C O PY Secure Elements, Trusted Service Managers & HCE Issuing Platforms Internet & Tech Companies