Target Operating Model Research

•

32 recomendaciones•19,148 vistas

Intense competition and slow growth in mature markets have magnified uncertainty and put pressure on costs, just as regulators are escalating their demands. Research shows that CFOs and other senior finance executives believe that their function can play a key role but the ability to impact these challenges depends on levels of maturity and preparedness, which vary widely across companies and industries, as well by sub-functions. Here are the key findings from our research on how enterprises are driving transformation to achieve business impact.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Similar a Target Operating Model Research

Similar a Target Operating Model Research (20)

Más de Genpact Ltd

Más de Genpact Ltd (20)

Último

Último (20)

Target Operating Model Research

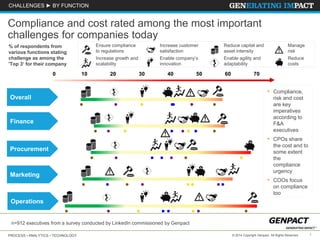

- 1. PROCESS • ANALYTICS • TECHNOLOGY 1© 2014 Copyright Genpact. All Rights Reserved. CHALLENGES ► BY FUNCTION % of respondents from various functions stating challenge as among the 'Top 3‘ for their company Overall Finance Procurement Marketing Operations n=912 executives from a survey conducted by LinkedIn commissioned by Genpact Compliance and cost rated among the most important challenges for companies today Ensure compliance to regulations Increase customer satisfaction Reduce capital and asset intensity Manage risk Increase growth and scalability Enable company’s innovation Enable agility and adaptability Reduce costs 0 10 20 30 40 50 60 70 • Compliance, risk and cost are key imperatives according to F&A executives • CPOs share the cost and to some extent the compliance urgency • COOs focus on compliance too

- 2. PROCESS • ANALYTICS • TECHNOLOGY 2© 2014 Copyright Genpact. All Rights Reserved. CHALLENGES ► BY COMPANY SIZE Ensure compliance to regulations Reduce cost Increase customer satisfaction Manage risk Increase growth and scalability Enable company’s innovation Enable agility and adaptability Reduce capital and asset intensity Overall Overall Overall Overall Overall Overall Overall Overall Large enterprises worry more about compliance and risk while those from smaller enterprises focus on scalability 10,000+ employees 5,001-10,000 employees Importance of the challenge (% of respondents across industries stating that the challenge is among the 'Top 3‘ for their company) 0 10 20 30 40 50 60 70 80 • Gap between smaller and larger companies is limited • Main exception is the growth challenge which is most acute in smaller firms n=912 executives from a survey conducted by LinkedIn commissioned by Genpact

- 3. PROCESS • ANALYTICS • TECHNOLOGY 3© 2014 Copyright Genpact. All Rights Reserved. Overall Overall Overall Overall Overall Overall Overall Overall NA APAC EMEA Ensure compliance to regulations Reduce cost Increase customer satisfaction Manage risk Increase growth and scalability Enable company’s innovation Enable agility and adaptability Reduce capital and asset intensity 0 10 20 30 40 50 60 70 80 • Small variations across regions • Most variance attributable to industries and size of companies present in those areas CHALLENGES ► BY REGIONS Intensity of challenges generally consistent across geographies Importance of the challenge (% of respondents across regions stating that the challenge is among the 'Top 3‘ for their company) n=912 executives from a survey conducted by LinkedIn commissioned by Genpact

- 4. PROCESS • ANALYTICS • TECHNOLOGY 4© 2014 Copyright Genpact. All Rights Reserved. High Tech Capital Markets Healthcare Banking Insurance Life Sciences CPG Manufacturing Overall Overall Overall Overall Overall Overall Overall Overall CHALLENGES ► BY INDUSTRY Ensure compliance to regulations Reduce cost Increase customer satisfaction Manage risk Increase growth and scalability Enable company’s innovation Enable agility and adaptability Reduce capital and asset intensity Financial sector most concerned about compliance and risk management, however results vary across industries DIRECTIONALImportance of the challenge (% of respondents in specific industries stating that the challenge is among the 'Top 3‘ for their company) 0 10 20 30 40 50 60 70 80 • Imperatives vary across industries • High tech most focused on innovation, growth, agility • Life sciences respondents focused on regulation, customer satisfaction, and to some extent cost and innovation n=912 executives from a survey conducted by LinkedIn commissioned by Genpact

- 5. PROCESS • ANALYTICS • TECHNOLOGY 5© 2014 Copyright Genpact. All Rights Reserved. Overall RiskMarketing Procurement Operations Finance RiskMarketing Procurement Operations Finance Overall Risk Overall Overall Marketing Procurement OperationsFinance Overall Risk MarketingProcurement Operations Finance Overall Risk Marketing Procurement Operations Finance Overall Risk Marketing Procurement Operations FinanceOverall Risk Marketing Procurement Operations Finance Risk Operations MarketingFinance Procurement CHALLENGES ► BY FUNCTION Ensure compliance to regulations Reduce cost Increase customer satisfaction Manage risk Increase growth and scalability Enable company’s innovation Enable agility and adaptability Reduce capital and asset intensity Significant variation by function: Finance executives most concerned with compliance, risk and cost Importance of the challenge (% of respondents in specific functions across industries stating that the challenge is among the 'Top 3‘ for their company) 0 10 20 30 40 50 60 70 80 DIRECTIONAL n=912 executives from a survey conducted by LinkedIn commissioned by Genpact

- 6. PROCESS • ANALYTICS • TECHNOLOGY 6© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► FUNCTION IMPACT n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact * Impact of a function on company’s challenges is defined as 𝑓 𝑥𝑖 = 𝑗 𝑛 𝑥𝑖𝑗 𝑦𝑗, where 𝑥𝑖𝑗 is the % of respondents who believe that improvement in the function 𝑥𝑖 will have a material impact on the challenge 𝑦𝑗; 𝑦𝑗 is the % of respondents citing the challenge as among the 'Top 3' Function Impact Index* combining stated importance of challenges and stated ability of a function to address them FP&A and MDM seen as important in solving the most pressing challenges among finance functions 140 78 79 93 123 147 MDM R2R FP&A Overall F&A P2P O2C Impact of R2R, P2P and O2C less ubiquitous than FP&A and MDM, which explains the difference between scores

- 7. PROCESS • ANALYTICS • TECHNOLOGY 7© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► FUNCTION IMPACT n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact 31 22 11 32 4248 13 29 17 15 2545 842 47 5487 38 55 29 56 48 4248 42 58 21 43 6358Overall F&A 23 43 37 18 17O2C 50 32 18 22 35R2R 25 53 27 9 22P2P 34 53 20 62 64FP&A 38 40 4949 27MDM Ensurecompliance toregulations Reducecosts Increasecustomer satisfaction Increasegrowth andscalability Managerisk Enablecompany innovation Enableagility andadaptability Reducecapital andassetintensity FP&A and MDM helps solve challenges most, R2R is still critical for compliance, P2P and O2C for cost, O2C for customer satisfaction 10 Magnitude of challenge1 1 % of respondents stating it is one of the top 3 challenges in their company %ofrespondentsstatingfunction canhavematerialimpacton addressingchallenge DIRECTIONAL

- 8. PROCESS • ANALYTICS • TECHNOLOGY 8© 2014 Copyright Genpact. All Rights Reserved. Others1 BFSIOverall Others1 BFSI Overall Others1 BFSI Overall Others1 BFSIOverall Others1 Overall Overall Others1 BFSI BFSI FINANCE AND ACCOUNTING ► MATURITY ► BFSI vs. OTHER INDUSTRIES1 FP&A O2C R2R P2P MDM Overall F&A % of respondents stating that finance function in their organization is either very mature or mature n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact Banking and financial services more mature in FP&A, P2P and MDM, while other industries ahead in O2C and R2R 50 55 60 65 70 75 80 85 90 1 Healthcare, life sciences, consumer goods, high tech and manufacturing BFSI includes banking, capital markets and insurance DIRECTIONAL

- 9. PROCESS • ANALYTICS • TECHNOLOGY 9© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► MATURITY ► BFSI (BANKING, INSURANCE, CAPITAL MARKETS) MDM 33 31 37 P2P 36 32 32 R2R 33 36 32 O2C 48 25 27 FP&A 32 16 32 20 Overall F&A 53 48 Somewhat mature/ImmatureVery mature Mature n=75 finance and accounting executives from banking, capital markets and insurance from a survey conducted by LinkedIn commissioned by Genpact % respondents stating the maturity of the finance functions in their organizations Financial services organizations more mature than other industries with FP&A considered as most mature MDM noticeably least mature F&A process DIRECTIONAL

- 10. PROCESS • ANALYTICS • TECHNOLOGY 10© 2014 Copyright Genpact. All Rights Reserved.© 2014 Copyright Genpact. All Rights Reserved. 30 46 24 FP&A 4528 27 2733 40 25 R2R 3441 44 P2P 4115MDM O2C Overall F&A 29 2447 MatureVery mature Somewhat mature/Immature n=85 finance and accounting executives from CPG, life sciences, manufacturing, high tech and healthcare from a survey conducted by LinkedIn commissioned by Genpact MDM noticeably least mature F&A process % respondents stating the maturity of the finance functions in their organizations Order to cash most mature for consumer goods, life sciences, healthcare, high tech and manufacturing FINANCE AND ACCOUNTING ► MATURITY ► CPG, LIFE SCIENCES, HIGH TECH, HEALTHCARE, MANUFACTURING DIRECTIONAL

- 11. PROCESS • ANALYTICS • TECHNOLOGY 11© 2014 Copyright Genpact. All Rights Reserved. BFSIOthers1 Overall BFSIOthers1 Overall BFSIOthers1 Overall BFSIOthers1 Overall BFSIOthers1 Overall BFSI Others1 Overall FINANCE AND ACCOUNTING ► PREPAREDNESS ► BFSI vs. OTHER INDUSTRIES1 n=157 for finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact FP&A O2C R2R P2P MDM Overall F&A % respondents stating their organization is very prepared or prepared to mature the specific finance function FP&A, MDM and R2R least ready to transform in manufacturing, life sciences, healthcare , CPG and high tech Banking and financial services most prepared to transform the F&A function 1 Healthcare, life sciences, consumer goods, high tech and manufacturing. BFSI includes banking, capital markets and insurance 30 60 70 80 9040 50 DIRECTIONAL

- 12. PROCESS • ANALYTICS • TECHNOLOGY 12© 2014 Copyright Genpact. All Rights Reserved. Overall R2R Overall P2P Overall O2C Overall MDM Overall FP&A Overall Overall F&A FINANCE AND ACCOUNTING ► PREPAREDNESS ► LARGE vs. SMALL COMPANIES n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact (21 from small companies with 5,001-10,000 employees and 136 from large companies with 10,000+ employees) Larger companies most prepared to transform F&A further % respondents stating their organization is very prepared or prepared to mature the specific finance function 10,000+ employees 5,001-10,000 employees 30 60 70 80 9040 50 DIRECTIONAL

- 13. PROCESS • ANALYTICS • TECHNOLOGY 13© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► OVERALL ABILITY TO IMPACT ► BFSI (BANKING, INSURANCE, CAPITAL MARKETS) Somewhat mature or Immature Very mature or mature Somewhat prepared or not prepared Fully prepared or prepared Overall F&A O2C R2R P2P FP&A MDM 58 58 58 5 8 55 45 41 53 61 33 22 61 57 24 32 24 29 26 34 50 31 53 59 52 61 48 50 28 5 8 1 3 66 10 14 66 15 53 44 32 9 13 17 Ensure compliance toregulations Managerisk Increase customer satisfaction Reducecosts Increasegrowth andscalability Maturityof process In BFSI, MDM comparatively less mature; plans seem to be in place to transform further if needed n=72 for F&A executives from capital markets, banking and insurance from a survey conducted by LinkedIn commissioned by Genpact Magnitude of challenge1 1 % of respondents stating it is one of the top 3 challenges in their company %ofrespondentsstatingfunction canhavematerialimpacton addressingchallenge Prepared % of respondents assessing maturity and preparedness DIRECTIONAL

- 14. PROCESS • ANALYTICS • TECHNOLOGY 14© 2014 Copyright Genpact. All Rights Reserved. 45 50 55 60 65 70 75 80 85 45 50 55 60 65 70 75 80 85 %ofcompaniesstatedasverypreparedor preparedtomatureinspecifiedfunctions MDM FP&A P2P R2R O2C FINANCE AND ACCOUNTING ► OVERALL ABILITY TO IMPACT ► BFSI (BANKING, INSURANCE, CAPITAL MARKETS) Size of the bubble indicates the impact of the sub-function on the company’s challenges as a % of overall finance impact MDM comparatively less mature; plans seem to be in place to transform further if needed % of companies stated as very mature or mature in the specified functions Reduce cost Manage risk Increase growth and scalability Reduce Costs Increase Customer Satisfaction Ensure compliance to regulation Reduce Costs Increase Customer Satisfaction Ensure compliance to regulation Manage risk Ensure compliance to risk Increase growth and scalability Ensure compliance to regulations Reduce costs Increase customer satisfaction Size of the circle indicates importance of challenge and size of the slice indicates impact of improving the function on the challenge n= 72 finance and accounting executives from commercial and retail banking, insurance and capital markets from a survey conducted by LinkedIn commissioned by Genpact DIRECTIONAL

- 15. PROCESS • ANALYTICS • TECHNOLOGY 15© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► OVERALL ABILITY TO IMPACT Very mature or mature Somewhat mature or immature Fully prepared or prepared Somewhat prepared or not prepared Maturityof process Preparedto mature 56 48 48 42 42 58 21 43 6458Overall F&A 23 43 37 18 17O2C 50 32 18 22 35R2R 25 53 27 9 22P2P 34 53 20 62 64FP&A 38 40 4949 27 MDM Ensure compliance toregulations Reducecosts Increasecustomer satisfaction Increasegrowth andscalability Managerisk MDM is important and has comparatively lower maturity and preparedness to evolve n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact Magnitude of challenge1 % of respondents assessing maturity and preparedness 1 % of respondents stating it is one of the top 3 challenges in their company %ofrespondentsstatingfunction canhavematerialimpacton addressingchallenge DIRECTIONAL

- 16. PROCESS • ANALYTICS • TECHNOLOGY 16© 2014 Copyright Genpact. All Rights Reserved. 45 50 55 60 65 70 75 80 85 45 50 55 60 65 70 75 80 85 MDM %ofcompaniesstatedasverypreparedor preparedtomatureinspecifiedfunctions FP&A P2P R2R O2C Size of the bubble indicates the impact of the sub-function on the company’s challenges as a% of overall finance impact MDM is important but least mature yet many aren’t ready to evolve it further in life sciences, healthcare, manufacturing, CPG and high-tech % of companies stated as very mature or mature in the specified functions Reduce cost Ensure compliance to regulation Increase growth and scalability Reduce Costs Ensure compliance to regulation Enable agility and adaptation Ensure compliance to regulation Reduce costs Increase growth and scalability Increase growth and scalability Reduce costs Reduce cost Increase customer satisfaction Ensure compliance to regulation Completeness the slice indicates impact of improving the function on the challenge n= 85 finance and accounting executives from healthcare, life sciences, consumer goods, high tech and manufacturing from a survey conducted by LinkedIn commissioned by Genpact FINANCE AND ACCOUNTING ► MATURITY ► CPG, LIFE SCIENCES, HIGH TECH, HEALTHCARE, MANUFACTURING DIRECTIONAL

- 17. PROCESS • ANALYTICS • TECHNOLOGY 17© 2014 Copyright Genpact. All Rights Reserved.© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► OPERATING MODEL INITIATIVES ► BFSI (BANKING, INSURANCE, CAPITAL MARKETS) n= 72 finance and accounting executives from commercial and retail banking, insurance and capital markets from a survey conducted by LinkedIn commissioned by Genpact 25R2R 21P2P 21 39 5835Overall F&A Business process re-engineering Radically improved use of technology 42 25 39 • Technology quite important in FP&A and MDM • More BFSI executives see advanced organizational structures as helpful for MDM 25 60MDM 46 118 128 17O2C 21 40 64 33FP&A 4640 127 82 68 Impact Index* Advanced organizational structures most frequently applicable among operating model initiatives % of respondents stating the initiative can have a material impact on the function * Function Impact Index combining stated importance of challenges and stated ability of a function to address them BPO or SSC or hybrid1 DIRECTIONAL 1 BPO – Business Process Outsourcing, SSC – Shared Services Center

- 18. PROCESS • ANALYTICS • TECHNOLOGY 18© 2014 Copyright Genpact. All Rights Reserved. At least one third of the companies have not initiated the transformation of their operating model Not Considered Planned after 12 months Planned in next 12 months Currently in Progress SSC,BPO or hybrid1 15 13 15 58 BPR 28 5 13 54 Tech 23 7 11 59 16 9 11 64 32 8 10 50 15 15 67 15 13 11 62 15 10 15 60 18 5 13 64 13 5 11 72 18 8 11 16 63 19 8 57 18 10 7 65 24 14 14 48 21 12 13 54 O2C R2R P2P FP&A MDM FINANCE AND ACCOUNTING ► OPERATING MODEL INITIATIVES ► PROGRESS n=157 for finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact % of respondents; Width of the column indicates the % of respondents stating that the operating model initiative will have a material impact on the function. DIRECTIONAL 1 BPO – Business Process Outsourcing, SSC – Shared Services Center

- 19. PROCESS • ANALYTICS • TECHNOLOGY 19© 2014 Copyright Genpact. All Rights Reserved.© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► OPERATING MODEL INITIATIVES ► MATURE vs. IMMATURE Overall F&A P2P O2C R2R FP&A MDM Business process re-engineering Radically improved use of technology Many believe advanced organizational models can have impact; more so for mature F&A functions 634038 494138 603326 302318 493028 352727 512926 392527 453742 314343 523043 483451 • Organizations with mature F&A functions are more likely to believe advanced organizational structures can have a material impact on all sub-functions • Technology and BPR perception is instead not dependent on maturity of process Mature Not mature n=157 finance and accounting executives; Mature=119, Not mature=38 from a survey conducted by LinkedIn commissioned by Genpact % of respondents stating the initiative can have a material impact on the function BPO or SSC or hybrid1 DIRECTIONAL 1 BPO – Business Process Outsourcing, SSC – Shared Services Center

- 20. PROCESS • ANALYTICS • TECHNOLOGY 20© 2014 Copyright Genpact. All Rights Reserved.© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► PREPAREDNESS ► BY MATURITY Already mature functions also more prepared to evolve %respondentsstatingthepreparednessoftheir organizationtomatureafinancefunction Mature 32 68 43 57 36 64 44 56 43 57 46 54Overall F&A 88 R2R 69 31 P2P 73 27 O2C 72 28 MDM 77 23 FP&A 77 23 12 Somewhat prepared/Not prepared Prepared Not mature Respondents rating their company’s functions as n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact Mature=119, Not mature=38 DIRECTIONAL

- 21. PROCESS • ANALYTICS • TECHNOLOGY 21© 2014 Copyright Genpact. All Rights Reserved. FINANCE AND ACCOUNTING ► OPERATING MODEL IMPACT n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact BFSI BFSI Overall Overall Overall Others1 Others1 Others1 BFSI Technology BPR Organizational models (SSC, BPO or hybrid) • Advanced organizational models seen as more frequently deployable but having less standalone impact • Impact in financial services consistently seen as higher than in other industries Improved use of technology, when applicable, is seen as providing largest monetary impact - especially in BFSI 1Healthcare, life sciences, consumer goods, high tech and manufacturing 60 360120 180 240 300 Companies with 10,000+ employees Annual $ impact is the weighted average of the total estimated positive business impact of all operating model initiatives in million US$ per annum including reduction of cost, capital required, improvement of cash and revenue growth BFSI includes banking, capital markets and insurance DIRECTIONAL

- 22. PROCESS • ANALYTICS • TECHNOLOGY 22© 2014 Copyright Genpact. All Rights Reserved. BPR SSC, BPO, Hybrid $ 158m $ 82m $ 83m Tech $ 110m SSC, BPO, Hybrid $ 178m BPR $ 295m TechBPRTech SSC, BPO, Hybrid1 $ 268m $ 155m $ 103m FINANCE AND ACCOUNTING ► OPERATING MODEL IMPACT ► BY MATURITY Annual $ impact is the impact of operating model initiatives in US$ per annum including reduction of cost, capital required, improvement of cash and revenue growth Mature organizations expect more impact than less mature ones from technology and BPR • Advanced organizational models seen as more frequently deployable but having less standalone impact • Impact in mature organizations consistently higher than in the rest OVERALL MATURE IMMATURE n=157 finance and accounting executives from a survey conducted by LinkedIn commissioned by Genpact; Mature=119, Not mature=38 Average $ impact, bar width proportional to percent of respondents stating that the initiative will have a material impact Average $ impact DIRECTIONAL 1 BPO – Business Process Outsourcing, SSC – Shared Services Center