EMEA Corporate Occupier Conditions, Winter 2015

•

1 recomendación•603 vistas

The winter 2015 edition of the EMEA Corporate Occupier Conditions sheds light on the current market conditions, rental favourability and the opportunities and challenges for corporate occupiers across EMEA.

Recomendados

Recomendados

Más contenido relacionado

Similar a EMEA Corporate Occupier Conditions, Winter 2015

Similar a EMEA Corporate Occupier Conditions, Winter 2015 (20)

Más de JLL France

Más de JLL France (20)

Último

Último (20)

EMEA Corporate Occupier Conditions, Winter 2015

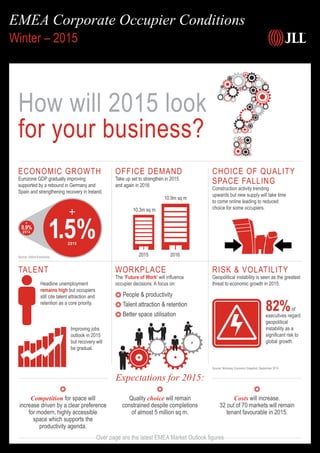

- 1. How will 2015 look for your business? EMEA Corporate Occupier Conditions Winter – 2015 Source: Oxford Economics Economic Growth Eurozone GDP gradually improving supported by a rebound in Germany and Spain and strengthening recovery in Ireland. TALENT Headline unemployment remains high but occupiers still cite talent attraction and retention as a core priority. Improving jobs outlook in 2015 but recovery will be gradual. OFFICE Demand Take up set to strengthen in 2015 and again in 2016 CHOICE OF QUALITY SPACE FALLING Construction activity trending upwards but new supply will take time to come online leading to reduced choice for some occupiers. WORKPLACE The ‘Future of Work’ will influence occupier decisions. A focus on: People productivity Talent attraction retention Better space utilisation RISK VOLATILITY Geopolitical instability is seen as the greatest threat to economic growth in 2015. 82%of executives regard geopolitical instability as a significant risk to global growth. Competition for space will increase driven by a clear preference for modern, highly accessible space which supports the productivity agenda. Quality choice will remain constrained despite completions of almost 5 million sq m. Costs will increase. 32 out of 70 markets will remain tenant favourable in 2015. Expectations for 2015: Over page are the latest EMEA Market Outlook figures Source: Mckinsey Economic Snapshot, September 2014 1.5%0.9% 2014 2015 2015 10.3m sq m 2016 10.9m sq m

- 2. 2014 2015 Prague 14.0% €234 20152014 Athens 19.1% €204 20152014 Budapest 16.9% €240 20152014 Copenhagen 10.5% €235 2014 2015 7.0% Oslo €505 20152014 Stockholm 9.2% €494 2014 2015 15.5% Moscow €871 2014 2015 13.8% Warsaw €288 20152014 Edinburgh €4086.5% 20152014 Madrid €30012.0% 20152014 London West End €1,4502.6% 20152014 Dublin €48415.0% 20152014 Lisbon €21913.3% 20152014 Milan €47014.4% 20152014 Munich €3907.0% 20152014 Brussels €27510.3% 20152014 Amsterdam €34515.8% 20152014 Luxembourg €5044.1% 2014 2015 Istanbul 16.5% €420 20152014 Kiev 22.5% €294 20152014 Paris CBD €7405.2% Landlord favourable market Balanced market Tenant favourable market Vacancy rate (%) Sentiment based view from each market outlining future expectations of prime rental direction (per sq ft) Prime rents (€ per sq m) as of Q3 2014 www.jll.eu COPYRIGHT © JONES LANG LASALLE IP, INC. 2015 This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication. Source: JLL October 2014 This summary of EMEAOccupier Conditions provides a macro level overview of real estate occupancy indicators across 75 key EMEAoffice markets. For a more in-depth view of any particular market please call us and we will be happy to assist. EMEA Occupier Office Property Clock Dublin, London City, London West End, Luxembourg Belfast, Southampton, Stockholm Edinburgh, Glasgow, Western Corridor Cairo, Muscat, Riyadh, Manama Doha, Kuwait City, Zagreb Geneva, Zurich, Warsaw The Hague, Düsseldorf Johannesburg St. Petersburg Amsterdam, Milan, Dubai, Belgrade Lisbon Kiev Madrid Manchester Nottingham, Istanbul, Abu Dhabi Jeddah Gothenburg, Hamburg, Munich, Oslo, Rotterdam Eindhoven, Helsinki, Lyon, Utrecht, Krakow, Moscow Berlin, Frankfurt, Stuttgart Cologne, Tel Aviv Antwerp, Athens, Barcelona, Birmingham, Bristol, Brussels, Cardiff, Copenhagen, Leeds, Malmo, Paris CBD, Rome, Bratislava, Bucharest, Budapest, Prague,Tri-City, Capetown Rental growth acceler- ating Rents bottoming out Rental growth slowing Rents falling Western Europe Central Eastern Europe Middle East Africa Karen Williamson Associate Director EMEA Research +44 (0) 203 147 1197 karen.williamson@eu.jll.com Tom Carroll Director EMEA Research +44 (0)203 147 1207 tom.carroll@eu.jll.com Any questions, please contact: Select EMEA market conditions 11.3% Helsinki €306 €177 2014 2015 12.3% Johannesburg 2014 2015