Bank Merger & Acquisition Review: 2011 & Q1 2012 | Mercer Capital

Despite an anticipated surge of transactions within the banking industry, bank merger and acquisition activity declined in 2011 compared to the prior year, hindered by a weak economic recovery, mounting regulatory pressures, and, according to some analysts, excessive seller expectations. This article from the professionals of Mercer Capital reviews the M&A landscape for community banks in both 2011 and the 1st quarter of 2012. ----------------------------------- Mercer Capital is one of the nation’s leading financial institutions valuation firms. The firm assists community banks with significant corporate valuation issues. In addition, Mercer Capital has a wealth of transaction experience helping clients with mergers, acquisitions, recapitalizations and other substantial transactions. Core services include: » Financial Institution Valuation » M&A Representation & Consulting » Bank ESOP Valuation » Fairness Opinions » Valuation for Tax Compliance » Loan Portfolio Valuation » Goodwill Impairment Testing » Capital Raising Consulting For more information about Mercer Capital, visit www.mercercapital.com.

Recomendados

Recomendados

Más contenido relacionado

Destacado

Destacado (17)

Más de Mercer Capital

Más de Mercer Capital (20)

Último

Último (20)

Bank Merger & Acquisition Review: 2011 & Q1 2012 | Mercer Capital

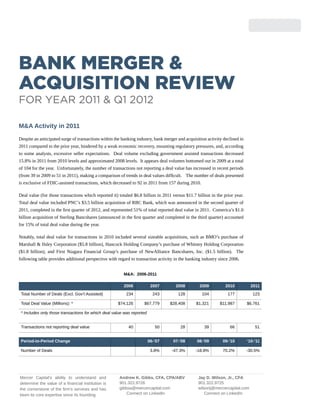

- 1. Bank Merger & Acquisition Review For Year 2011 & Q1 2012 M&A Activity in 2011 Despite an anticipated surge of transactions within the banking industry, bank merger and acquisition activity declined in 2011 compared to the prior year, hindered by a weak economic recovery, mounting regulatory pressures, and, according to some analysts, excessive seller expectations. Deal volume excluding government assisted transactions decreased 15.8% in 2011 from 2010 levels and approximated 2008 levels. It appears deal volumes bottomed out in 2009 at a total of 104 for the year. Unfortunately, the number of transactions not reporting a deal value has increased in recent periods (from 39 in 2009 to 51 in 2011), making a comparison of trends in deal values difficult. The number of deals presented is exclusive of FDIC-assisted transactions, which decreased to 92 in 2011 from 157 during 2010. Deal value (for those transactions which reported it) totaled $6.8 billion in 2011 versus $11.7 billion in the prior year. Total deal value included PNC’s $3.5 billion acquisition of RBC Bank, which was announced in the second quarter of 2011, completed in the first quarter of 2012, and represented 51% of total reported deal value in 2011. Comerica’s $1.0 billion acquisition of Sterling Bancshares (announced in the first quarter and completed in the third quarter) accounted for 15% of total deal value during the year. Notably, total deal value for transactions in 2010 included several sizeable acquisitions, such as BMO’s purchase of Marshall & Ilsley Corporation ($5.8 billion), Hancock Holding Company’s purchase of Whitney Holding Corporation ($1.8 billion), and First Niagara Financial Group’s purchase of NewAlliance Bancshares, Inc. ($1.5 billion). The following table provides additional perspective with regard to transaction activity in the banking industry since 2006. M&A: 2006-2011 2006 2007 2008 2009 2010 2011 Total Number of Deals (Excl. Gov’t Assisted) 234 243 128 104 177 123 Total Deal Value (Millions): * $74,126 $67,779 $28,408 $1,321 $11,987 $6,761 * Includes only those transactions for which deal value was reported Transactions not reporting deal value 40 50 28 39 66 51 Period-to-Period Change 06-’07 07-’08 08-’09 09-’10 ‘10-’11 Number of Deals 3.8% -47.3% -18.8% 70.2% -30.5% Mercer Capital’s ability to understand and Andrew K. Gibbs, CFA, CPA/ABV Jay D. Wilson, Jr., CFA determine the value of a financial institution is 901.322.9726 901.322.9725 the cornerstone of the firm’s services and has gibbsa@mercercapital.com wilsonj@mercercapital.com been its core expertise since its founding. Connect on LinkedIn Connect on LinkedIn

- 2. As in 2010, the majority of acquisitions involved sellers with assets less than $500 million. As shown below, for deals for which pricing multiples and deal value were available (a total of 72 transactions), 56 transactions, or more than 75%, involved targets with assets less than $500 million. Asset target Size Median Median Median Median Median Median Price/ Tang. No. of % of Price/ Price/ Price/ Asset Size LTM Prem/Core Trans. Trans. Book TBV Assets EPS Deposits Assets < $500 Million $127,202 25.32 101.00 103.74 10.51 0.01 56 77.8% Assets $500 Million to $2 Billion $714,973 23.32 121.34 121.34 11.27 3.65 12 16.7% Assets $2 Billion to $10 Billion $2,616,014 NM 134.53 149.26 13.08 6.03 3 4.2% Assets > $10 Billion $27,375,539 NM 87.46 97.29 12.60 -0.54 1 1.4% Twenty-one of the 72 transactions for which pricing information was available were all-cash transactions, 35 deals involved some mixture of cash and other consideration (generally common stock), and 10 transactions involved common stock as currency. The remaining deals were unclassified or not reported. Regional economic viability again affected transaction volume during the year. Deal volume was highest in the Midwest and West regions1, which reported 24 and 19, respectively, of the 72 total transactions with pricing multiples. The Atlantic Coast and Northeast regions followed with 11 deals each in 2011. Seven transactions occurred in the Southeast region. For comparison, FDIC-assisted transactions, which totaled 92 in 2011 compared to 157 in 2010, continued to be concentrated in states with severely depressed real estate markets, such as Florida and Georgia (both in the Southeast region), which had 13 and 23 bank failures, respectively, during 2011. Illinois and Colorado followed with 9 and 5 failures, respectively, and all remaining states reported less than 5 failures each during the year. REGION Median Median Median Median Median Median Tang. No. of Price/LTM Price/ % of Trans. Asset Size Price/Book Price/TBV Prem/Core Trans. EPS Assets Deposits Atlantic Coast $247,009 16.39 77.69 81.25 6.92 -1.03 11 15.3% Midwest $72,594 19.21 114.07 118.76 11.32 2.64 24 33.3% Northeast $283,277 35.42 137.26 142.91 15.01 6.41 11 15.3% Southeast $116,160 14.55 63.72 63.72 3.07 -2.01 7 9.7% West $186,970 33.64 91.79 91.79 10.61 -0.95 19 26.4% 1 The regions include the following states: ◉◉ Atlantic Coast – Delaware, Florida, Maryland, North Carolina, South Carolina, Virginia, West Virginia, Washington, D.C. ◉◉ Midwest – Iowa, Illinois, Indiana, Kansas, Michigan, Minnesota, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Texas, Wisconsin ◉◉ Northeast – Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Vermont ◉◉ Southeast – Alabama, Arkansas, Georgia, Kentucky, Louisiana, Missouri, Mississippi, Tennessee ◉◉ West – Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington, Wyoming © 2012 Mercer Capital 2 www.mercercapital.com

- 3. First Quarter 2012 Activity Through March of 2012, a total of 16 bank failures were reported with eight attributable to the Southeast region. Florida and Tennessee each reported two failures, while Georgia reported four, and Illinois reported three failures. For comparison, through March of 2012, transaction volume was higher with 56 total deals reported (compared to 47 in the first quarter of 2011). Total reported deal value through the first quarter of 2012 was also higher at $3.0 billion (compared to $1.5 billion in the first quarter of 2011) and included Mitsubishi UFJ Financial Group’s $1.5 billion acquisition of Pacific Capital Bancorp as well as Prosperity Bancshares’ $529 million acquisition of American State Financial Corp. Deal volume in the first quarter of 2012 was weakest in the Northeast, where four transactions occurred, while deal volume was higher in the Midwest and Southeast, which reported 25 and 13 transactions, respectively. Some analysts have attributed the heightened transaction activity in the first quarter of 2012 to the improved economy BANK WATCH and an increased confidence among buyers, and, in particular, confidence with regard to loan portfolio assessment. Transaction activity going forward is expected to remain concentrated among smaller institutions in light of revenue Mercer Capital’s and regulatory challenges. However, uncertainty concerning regulatory changes and the resulting burdens placed on complimentary institutions (smaller ones in particular), coupled with market volatility and the heated political climate, still looms, monthly newsletter threatening any impending, potential surge of transaction activity. for bankers and those serving the Furthermore, capital raising remains difficult, and lackluster market activity caused many institutions to look to private banking industry equity firms as a source of capital in 2011. Preferred stock issuances were successful for several firms during the year, and some analysts expect more buyers to utilize such issuances to finance acquisitions when consolidation activity resumes. Focusing on bank activity in five U.S. regions: Atlantic Coast, Midwest, Northeast, Southeast, and West About Mercer Capital The Financial Institutions Group of Mercer Capital provides a broad range of specialized advisory services to the financial services View Archives industry. Mercer Capital assists financial institutions with significant corporate valuation, transactions, and other strategic decisions. Mercer Capital is one of the nation’s leading financial institutions valuation firms. In addition, the firm has a wealth of transaction experience helping clients with mergers, acquisitions, recapitalizations and other substantial transactions. Core services include: » Financial Institution Valuation » M&A Representation & Consulting » Bank ESOP Valuation » Fairness Opinions » Valuation for Tax Compliance » Loan Portfolio Valuation » Goodwill Impairment Testing » Capital Raising Consulting Contact Us Andrew K. Gibbs, CFA, CPA/ABV Jay D. Wilson, Jr., CFA Leader, Financial Institutions Group Vice President HEADQUARTERS 901.322.9726 901.322.9725 5100 Poplar Avenue, Suite 2600 gibbsa@mercercapital.com wilsonj@mercercapital.com Memphis, Tennessee 38137 Connect on LinkedIn Connect on LinkedIn 901.685.2120 (p) 901.685.2199 (f) www.mercercapital.com © 2012 Mercer Capital 3 www.mercercapital.com