does india is doing well?

•Descargar como DOCX, PDF•

0 recomendaciones•86 vistas

market analysis report

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a does india is doing well?

Similar a does india is doing well? (20)

Más de National Management Olympiad

Más de National Management Olympiad (20)

Último

Último (20)

does india is doing well?

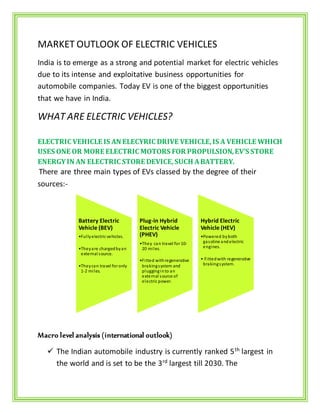

- 1. MARKET OUTLOOK OF ELECTRIC VEHICLES India is to emerge as a strong and potential market for electric vehicles due to its intense and exploitative business opportunities for automobile companies. Today EV is one of the biggest opportunities that we have in India. WHAT ARE ELECTRIC VEHICLES? ELECTRIC VEHICLE IS AN ELECYRIC DRIVE VEHICLE,IS A VEHICLE WHICH USES ONE OR MORE ELECTRIC MOTORS FOR PROPULSION,EV’S STORE ENERGYIN AN ELECTRIC STORE DEVICE,SUCH ABATTERY. There are three main types of EVs classed by the degree of their sources:- Macro level analysis (international outlook) The Indian automobile industry is currently ranked 5th largest in the world and is set to be the 3rd largest till 2030. The Battery Electric Vehicle (BEV) •Fullyelectric vehicles. •Theyare chargedbyan external source. •Theycan travel foronly 1-2 miles. Plug-in Hybrid Electric Vehicle (PHEV) •They can travel for 10- 20 miles. •Fitted withregenerative brakingsystem and plugginginto an external source of electric power. Hybrid Electric Vehicle (HEV) •Powered byboth gasoline andelectric engines. • Fittedwith regenerative brakingsystem.

- 2. requirement of mobility in India is set to change dramatically in the near future to cater to the requirement of population of 130 crores. Considering the government’s initiative working towards improving mobility requirements, has increased the need to prepare for green future Indian mobility and reduce dependence upon fossil fuels. Norway became the third world leader in the EV market industry in 2018 after china and United States. WHY? Commitment to zero emissions. Set up ambitious goals for all new cars to have zero emission. Policy measures such as tax exemptions, toll exemptions and other promoting incentives. Large import duties and car registration taxes. The government target for 30% adoption of the electric vehicles by 2030 will ne majorly driven by the electrification of the two electric-wheeler, and commercial vehicles. Lower rate of adoption 73000 361000 1053000 0 500000 1000000 1500000 NORWAY UNITED STATES CHINA NO. OF EVS REGISTERED

- 3. of electric vehicles in passenger vehicle segment is expected to have a limited impact on achieving the target. EV market is expected to grow at a robust rate of 43.13 % during the forecast period from 2019 to 2030, and installation of charging infrastructure project to grow at a CAGR of 42.38%. BS6 norms becoming more prices competitive with conventionally fueled vehicles, thus accelerating the electric vehicles sales in the country. Production of automobiles increased at a CAGR of around 4% over FY 12-17. Industry accounts for about 7.1% of the country’s Gross Domestic Product (GDP). GOVERNEMENT OF INDIA’S INITIATIVE (VISION 2030) FAME Faster adoption and manufacturing of hybrid and electric vehicles was launched in April 2015 fast track the goals of NMEP 2020 plan. As a part of National Mission Mobility Plan 2020, under which govt. provides incentives to lower purchasing cost of electric vehicles. Focused on 4 areas technology, Demand creation, pilot Projects and charging stations. A budget of Rs 75 crores was allocated which was fully utilized in 205-16 and a budget of Rs 91 crores has been utilized for budget allocation of Rs 122.9 crores. Incentives of about 33 to 66 Lakhs are planned for ach electric bus with typically costs around Rs 1-2 crores

- 4. (imported cars) and around Rs 50-80 Lakhs (domestically manufactured). Under JNURM (Jawaharlal Nehru Urban Renewal Mission) , NEMMP(National electric Mobility Mission Plan) and smart cities plans launched by the government expected to electric buses over the next 5 years. NMEMMP, 2020 (NATIONAL ELECTRIC MOBILITY MISSION PLAN) NEMMP targets 400000 passenger battery electric cars (BEVs) by 2020 avoiding 120 million barrels of oil and 4 million tons of carbon dioxide. Total investment required for this be 20000- 23000 Crore. Permissive legislations to allow usage of electric vehicles. Operational regulations and frame work aimed at setting safety regulations , Emissions regulations , vehicles performance standards , charging standards Policy for facilitating research and development. Incentivizing manufacturing and early adoption of electric policies aimed at encouraging investments and demand creations. MICRO ANALYSIS (STATE ANALYSIS) IN India, focus is on getting the public transport fleet into the electrification journey before focusing on private vehicles. Priority will be given in order to electric buses, 3 wheelers, fleet cars and then private cars.

- 5. DHI has come up with the scheme to assist all 1Mn+ populated cities to buy Electric Buses with a subsidy support of INR 1.05 billion per city and INR 150 million for charging infrastructure. Karnataka aroused the fort amongst other state to get notifies with EV policies. Karnataka has notified a very comprehension state policy for electric vehicles. The policy sets the mission and intension to take leadership position in the EV business in India. Availability of charging infrastructure is a prerequisite for electric mobility. Government of Karnataka will develop charging infrastructure as a commodity viable business venture that attracts private investment. This is a policy which covers all elements like EV manufacturing, EV charging business and EV sales and lane preferences for EV. BANGALORE EMERGED AS THE ONLY PLAYER IN EV MARKET IN INDIA. 70% 24% 6% INSTALLED CAPACITY BANGALORE DELHI OTHERS

- 6. About 7100 cars on the road since, introduction of the first Electric cars in 2001 by REWA (MAHINDRA) Limited support from the government in the car market. Currently the market largely limited to 2 cities in India. Mahindra’s manufacturing plant is located in Bangalore and new one is being planned at Nasik. Bangalore has the highest number of EVs in India with only just 6200 vehicles among 7200000 total vehicles. MARKET SEGMENTATION ANALYSIS Four segments under EV INDUSTRY:- Public transport- buses, E- Rickshaws (.02%) Two-wheelers (33.63%) Three wheelers (.09%) Four Wheelers (66.26%) Under the 4- wheelers segment – nearly 99000 are Hybrid SUV’S and only about 4000 are EV passengers. 0 10000 20000 30000 40000 50000 60000 70000 80000 90000 100000 2011-2012 2015-2016 2016-2017 2018-2019 97500 20000 22000 25000 350 2000 2000 3000 CARS TWO-WHEELERS

- 7. The sales of electric car have been stagnant at 2000 units per years since the last 2 years. The 2w industry is now slowly coming out of its slump of 2-15 where it has reached a sale of 20000 units from a high of 100000 in 2011. The government subsequently slashed the import duty on batteries from 26 per cent to 4 per cent. Since, 2012 there were no fiscal incentives available for EV’s and sales slumped to 20000 units. Now, with the FAME policy, sales have started to rise but most of the earlier EV wheeler firms have shut shop. EV MARKET ESTIMATION:- 2016-2017 revised classification as per Niti Aayog 2016-2017 Domestic Sales 2026 SIAM Projections (min.) 20126 SIAM Projections (Max.) 2026 SIAM Projections (Median) Passenger vehicles- personal 2132,709 5,170,000 7,370,000 6,270,000 Passenger vehicles- commercial/ fleet 914,018 4,230,000 6,030,000 5,130,000 Commercial vehicles 616,106 1,700,000 3,315,000 2,507,500 Commercial vehicles 98,126 300,000 585,000 442,500

- 8. Three- wheelers 511,658 1,200,000 1,500,000 1,350,000 Two - wheelers 17,589,511 50,600,000 55,600,000 53,100,000 OVERALL VEHICLES 21,862,128 63,200,000 74,400,000 68,800,000 MAJOR MARKET PLAYERS PASENGER VEHICLES OEM’S – 15 AND MANUFACTURING UNITS- 29 COMPANIES- MARUTI SUZUKI, HYUNDAI, TATA MOTORS, FIAT, FORD, HONDA, GENERAL OTORS, MAHINDRA, NISSAN, VOLKWAGEN, TOYOTA, GROUP, RENAULT, PREMIER AUTO, MERCEDES BENZ, BMW. 2 WHEELERS OEM’S – 13 MANUFACTURING UNITS- 22 COMPANIES- Hero Moto corp., Honda motors, Bajaj, TVS, Suzuki, Motorcycles, Yamaha, Mahindra, Royal Enfield, Piaggio vehicles, LML, Harley Davidson triumph, Kawasaki. THREE-WHEELERS OEM’S – 7 MANUFACTURING UITS- 7 Companies- TVS, Bajaj, Piaggio, Atul Auto, Scooters India, Mahindra, Force motors.

- 9. COMMERCIAL VEHICLES OEM’S – 12 MANUFACTURING UNITS- 34 COMPANIES- Tata motors, Ashok Leyland, Force Motors, Hindustan Motors, Isuzu Motors, Mahindra, AMW motors Piaggio Vehicles, SML Isuzu ltd., Eicher, Volvo man force. TRACTORS OEM’S – 17 MANUFACTURING UNITS- 20 COAMPANIES- Mahindra, Escorts, Tafe, John Deere and SAS motors, Trishul Tractors etc. Mahindra Electric is the first major EV manufacturer In India. The first and pioneer in the electric vehicle in India. The company is selling around 180-200 units month across India. Recently, launched a new EV model, e-Verito and expecting sales 350-400 per month. It has dedicated research and development centers in Bangalore where over 200 engineers are working on e- vehicle technology and refinements. Since, 2010 Mahindra electric has 7000+ customers under EV segment and has completed over 50 million miles of electric driving in India. Partnered with corporate fleet form- Lithium and provides Electric corporate fleet services in Bangalore. Partnered with NTPC to launch charging stations in Noida and Delhi.

- 10. The company is boosting capacity at it Bangalore facility to make battery packs from 500 per month to 800 -1000 per month in the next two-three months. They are planning to increase their capacity that can help them to sell over 5000 units per month over all the categories of vehicles. They are connected through 33 dealers across 9 states with 60% dealers in Bangalore, Mumbai and Delhi. Charging stations with 80 locations across 10 cities with 86% located in Delhi, Kolkata, Bangalore and Pune. Service of free charge as of now and will charge around 99-60 per charge in future. TATA MOTORS RECENTLY ENTERED THE MARKET IN PASSENGER VEHICLES AND ELECTRIC BUSES. Tata Motors has recently entered the EV market in passenger vehicles and electric buses. It plans to deliver 25 Hybrid buses to MMRDA in Mumbai. Expected demand from state transport Unions alone to be around 400000 electric buses in the long run. It has already launched electric buses in Himachal Pradesh. It has launched EV passenger vehicles by winning the tender of 10000 vehicles. Tata motors will launch many electric vehicles in India and it has already showed an electric variant of the Tiago and has been testing Nano Electric quite extensively.

- 11. Tata Motors is setting 400 charging stations in Delhi alone and has plans for more cities. EV CHARGING INDUSTRY AND INFRASTRUCTUR 15 firms currently supplying EV chargers in India. Only 3 firms in 4W, AC chargers so far in India and 10-12 firms in small 2w AC chargers supply along with their vehicles and a few OEM’s for EV chargers. These are Power electronics and battery charger manufacturers who have diversified into EV chargers. Firms like ABB India, Delta designs and products and are studying the technical /specifications, business models and potential for their products looking for the 4wheelers cars, E chargers. Most of the Indian firms are also looking at charging investments and getting theory designs and products at place. BATTERY MARKET IN INDIA It accounts for40% of the market in volume terms currently ruled by lead acid batteries in India.

- 12. Lithium battery requirements are imported and now we see some lithium battery packaging happening in India since last year. Currently there are 2500 market players in making batteries in the lead acid market and there could be close to another 10000 old small and unorganized players in the battery market. Enhanced Maintenance Free (EMF) batteries account for 67% of the market, VRLA are now gaining prominence is 31% of the market. Low maintenance batteries accounts for 2% of batteries. The market is dominated by 2 key players – Exide Industries and Amar Raja Industries. 0% 10% 20% 30% 40% 50% 60% 70% OTHERS TELECOM UPS AUTOMOTIVE SPLIT BY SEGMENT (BASE: 80.5 Mn UNITS)

- 13. INDIA IS AN IMMATURE MARKET FOR LITHIUM ION OR OTHER ADVANCED BATTERIES IN THE MARKET. Lithium ion batteries are starting out in the country and is currently almost non-existent, last year most of the batteries were imported from china South Korea , Vietnam, Singapore and Japan predominantly. Activities increased in lithium ion batteries packaging in India. India may reach a capacity of 1GWH of battery packaging by 2018. Current lithium ion packaging capacity in India is 500 MWh. BUSINESS OPPORTUNITIES IN THE INDIAN MARKET Opportunities in the Indian Market:- World’s third largest car market by 2026 is now starting its EV journey – India could learn from the world largest EV market. 16% 12% 10% 62% 0% 10% 20% 30% 40% 50% 60% 70% SMALL MEDIUM LARGE VERY LARGE VOLUME SPLIT BY CAEGORY (BASE: 80.5 Mn UNITS)

- 14. Firms could lead Indian industry by helping in EV regulations and standards to being a technology provider foe a smart mobility program. EV business throws up multiple new businesses /technology challenges such as EV charging, smart charging batteries, cloud based mobility etc. which could be key areas where technology could be introduced. CHALLENGES Policies are still in the making and due to multiple stakeholders; it may take a while before a clear horizon for EV emerges. Existing strong domestic auto industry and ecosystem could pose a challenge in terms of entry barriers. Local partnership will be vital for Norwegian companies to enter the Indian market. Indian EV market will face initial hiccups and will require some time to stabilize. “Value for money” association is vital to succeed in any business in India – same appliances for EV business a well.