Neostem, Inc. ($NBS) - WBB Securities Report

•

1 recomendación•474 vistas

NeoStem, Inc. (AMEX: NBS; Stock Twits: $NBS) is engaged in the development and manufacturing of cell-based therapies in the U.S. Its January 2011 acquisition of Progenitor Cell Therapy, LLC ("PCT") is central to the Company's strategic mission of capturing the paradigm shift to cell therapy.

Recomendados

Más contenido relacionado

Destacado

Destacado (16)

Similar a Neostem, Inc. ($NBS) - WBB Securities Report

Similar a Neostem, Inc. ($NBS) - WBB Securities Report (20)

Más de ProActive Capital Resources Group

Más de ProActive Capital Resources Group (20)

Último

Último (20)

Neostem, Inc. ($NBS) - WBB Securities Report

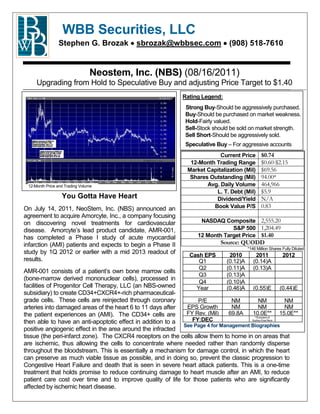

- 1. WBB Securities, LLC Stephen G. Brozak sbrozak@wbbsec.com (908) 518-7610 Neostem, Inc. (NBS) (08/16/2011) Upgrading from Hold to Speculative Buy and adjusting Price Target to $1.40 Rating Legend: Strong Buy-Should be aggressively purchased. Buy-Should be purchased on market weakness. Hold-Fairly valued. Sell-Stock should be sold on market strength. Sell Short-Should be aggressively sold. Speculative Buy – For aggressive accounts Current Price $0.74 12-Month Trading Range $0.60-$2.15 Market Capitalization (Mil) $69.56 Shares Outstanding (Mil) 94.00* 12-Month Price and Trading Volume Avg. Daily Volume 464,966 L. T. Debt (Mil) $5.9 You Gotta Have Heart Dividend/Yield N/A On July 14, 2011, NeoStem, Inc. (NBS) announced an Book Value P/S 0.83 agreement to acquire Amorcyte, Inc., a company focusing on discovering novel treatments for cardiovascular NASDAQ Composite 2,555.20 disease. Amorcyte’s lead product candidate, AMR-001, S&P 500 1,204.49 has completed a Phase I study of acute myocardial 12 Month Target Price $1.40 infarction (AMI) patients and expects to begin a Phase II Source: QUODD *146 Million Shares Fully Diluted study by 1Q 2012 or earlier with a mid 2013 readout of Cash EPS 2010 2011 2012 results. Q1 (0.12)A (0.14)A Q2 (0.11)A (0.13)A AMR-001 consists of a patient’s own bone marrow cells Q3 (0.13)A (bone-marrow derived mononuclear cells), processed in Q4 (0.10)A facilities of Progenitor Cell Therapy, LLC (an NBS-owned Year (0.46)A (0.55)E (0.44)E subsidiary) to create CD34+CXCR4+-rich pharmaceutical- grade cells. These cells are reinjected through coronary P/E NM NM NM arteries into damaged areas of the heart 6 to 11 days after EPS Growth NM NM NM the patient experiences an (AMI). The CD34+ cells are FY Rev. (Mil) 69.8A 10.0E** 15.0E** **Exclusive of then able to have an anti-apoptotic effect in addition to a FY:DEC Suzhou Erye Revs See Page 4 for Management Biographies positive angiogenic effect in the area around the infracted tissue (the peri-infarct zone). The CXCR4 receptors on the cells allow them to home in on areas that are ischemic, thus allowing the cells to concentrate where needed rather than randomly disperse throughout the bloodstream. This is essentially a mechanism for damage control, in which the heart can preserve as much viable tissue as possible, and in doing so, prevent the classic progression to Congestive Heart Failure and death that is seen in severe heart attack patients. This is a one-time treatment that holds promise to reduce continuing damage to heart muscle after an AMI, to reduce patient care cost over time and to improve quality of life for those patients who are significantly affected by ischemic heart disease.

- 2. NBS’s product has particular promise given that it is an autologous product, and thus avoids the many negative consequences that plague allogeneic products. AMR-001’s administration is worth highlighting. First, it utilizes the homing potential granted by the CXCR4 receptors, allowing for a larger percentage of cells to remain where they can be effective. Second, AMR-001 is administered via the IRA (Infarct Related Artery), and thus is performed in an identical manner as the original coronary cauterization. This allows for ease of use, consistent deployment of cells and avoids the potential risks arising from intra-cardiac injections of cells. NBS has conducted favorable phase I clinical trials that make AMR-001 an ideal candidate for further trials. The company has a well thought out phase II clinical trial planned that is intended to show clear clinical efficacy in enrolled patients. Heart disease is the leading cause of death in the United States. Over 1 million Americans suffer AMIs each year, with a significant proportion of them having significant cardiac dysfunction. This number is expanded many fold when international markets are considered. Thus we believe AMR-001 has potential to serve a large worldwide population. Given the grim statistics of AMIs in the U.S. and the promise of AMR-001 to provide benefit to these patients, we are raising our rating on NBS to Speculative Buy with a 12-Month Price Target of $1.40 AMR-001 Trials Phase I Study The Phase I study was conducted by the Emory University School of Medicine under Principal Investigator Dr. Arshed Quyummi, M.D., Professor of Medicine and Cardiology. This study performed autologous intracoronary infusions of bone-marrow derived CD34+ cells in patients with significant cardiac dysfunction post-STEMI. Treatment was administered in the golden period of 6 to 9 days after infarct-related artery stent placement. Patients were dosed at four dose levels in this safety and tolerability study. The secondary objective of the study was to assess the effect on cardiac function and cardiac perfusion in the infarcted area. Primary outcome measures for the Phase I study were cardiac function at two time points (3 and 6 months follow-up), compared to baseline measures obtained prior to CD34+ cell product infusion. Secondary outcome measures include perfusion of the infarct region at 6 months follow-up compared to baseline measures obtained prior to CD34+ cell product infusion. The study also established a threshold dose of 10 million cells injected per patient. Inclusion criteria were: Patients age 18 - 75 years Acute ST elevation myocardial infarction meeting ACC/AHA criteria, with symptoms of chest pain within 3 days of admission. Criteria include ST elevation > 1mm in limb leads or 2 mm in two or more precordial leads and increased levels of troponin, CPK MB or both) NYHA heart failure class of I, II or III 2

- 3. Phase II Study The Phase II trial will include 150 patients, 75 of whom will be treated with AMR-001 and 75 will receive a placebo. To be a candidate for this trial, the patient must have had experienced a STEMI, have undergone cardiac stent placement (which is standard of care), and after 96 hours have undergone a cardiac magnetic resonance exam that demonsrates an ejection fraction of less than or equal to 48 percent in addition to abnormal cardiac wall motion. Treated patients will receive a dose greater than 10 million cells, two to four-times the threshold dose established in the Phase I trial. Of note, treatment doses of up to 5 to 10 times that amount are permitted by FDA in this study. The study is expected to be completed in one year and will measure clinically-significant end-points. Six month measurements will include coronary perfusion, preservation of heart muscle function and quality of life. In years one, two and three, patients will be followed for major cardiac events, including heart failure, myocardial infarction and death. AMR-001’s phase II trial will be considered successful if positive end-points of heart function are observed. These will be quantified by maintenance of ejection fraction, improved wall motion, increased myocardial contractility, and improved heart volumes in the treated group versus the control group. This should also be met by improvement in quality of life (QoL) without safety signals. Should all measures trend positively NeoStem hopes to initiate a pivotal study prior to 2 and 3 year MACE read-outs upon which point a Phase II/III study may qualify as a supporting trial for approval. Other NBS Initiatives In addition to AMR-001, NBS operates within three distinct business segments: the U.S. market for adult stem cells, the China market for adult stem cells, and the China market for pharmaceuticals. U.S. Adult Stem Cells In the U.S., NBS provides stem cell collection, processing and storage services through a network of centers primarily in the Southern California and Northeastern U.S. NBS allows healthy individuals to donate their own stem cells to be used therapeutically later in life. The therapeutic applications for which the stem cells would be used are under each collection center’s discretion. NBS does not participate in any clinical decision-making in the U.S. Progenitor Cell Therapy; LLC provides the commercial collection and processing services. On April 27, 2010, NBS announced the launch of a new adult stem cell collection center and research and development laboratory in Cambridge, Massachusetts. The company now has a network of collection centers in the U.S. NBS licensed Very Small Embryonic-Like (VSEL) technology from the University of Louisville to research and develop potential diagnostic and therapeutic products based on very small embryonic- like stem cells, found in bone marrow. The company believes vast therapies could be developed from VSEL technology including those for cardiovascular, neural and ophthalmic diseases. VSEL technology holds the promise as a naturally pluripotent cell and has the potential to move the regenerative adult stem cell space to the next level of therapeutic value. 3

- 4. China Adult Stem Cells NBS’s Chinese adult stem cell efforts include creating a separate China-based stem cell operation, constructing a new research and development laboratory and processing facility in Beijing that will compliment PCT’s CMO operations as well. In addition, NBS is today providing stem cell therapies to a network of hospitals and obtaining stem cell product licenses in regenerative medicine. To develop its regenerative medicine pipeline in China, NBS acquired an exclusive license in Asia from Regenerative Sciences, Inc. for a procedure called Regenexx™. The Regenexx procedure involves extracting mesenchymal stem cells from the bone marrow to potentially treat various musculoskeletal diseases. The company has partnered with Shandong Wendeng Orthopedic Hospital to treat patients with adult stem cell therapies and conduct clinical research in orthopedic applications. NBS has also in-licensed certain technologies from Vincent Giampapa, M.D. for skin rejuvenation therapies based on autologous adult stem cells. The company intends to eventually launch a range of anti-aging and cosmetic applications in China. China Pharmaceuticals In October 2009, NBS completed a merger China Biopharmaceuticals Holdings, Inc., and as a result, acquired a 51 percent stake in Suzhou Erye Pharmaceuticals Company Ltd. Erye is a Chinese pharmaceutical company primarily focused on the manufacturing and distribution of generic antibiotic products throughout China. Valuation Our valuation of NBS is based on a sum of the parts analysis. We believe NBS’s greatest asset is its Amorcyte Phase II clinical technology at $100M. We also believe that the Suzhou Erye Pharmaceuticals assets have a value of $30M at a minimum. Using a three-times sales model for Progenitor Cell Therapy, we add an additional $30M. We use a value of $20M for the NBS (VSEL) technology and finally a $20M price for both cash and remaining assets. Assuming a fully diluted share count of 146 million shares, we arrive at our adjusted 12-month price target of $1.40 per share. Management Biographies Robin L. Smith – Chairman & CEO, M.D., MBA, joined as Chairman of the Advisory Board in September 2005 and, effective June 2, 2006, became the Chief Executive Officer and Chairman of the Board. Dr. Smith received a medical degree from Yale University and a master’s degree in business administration from the Wharton School. From 2000 to 2003, Dr. Smith served as President and Chief Executive Officer of IP2M, a multi-platform media company specializing in healthcare. From 1998 to 2000, she was Executive Vice President and Chief Medical Officer for HealthHelp, Inc., a National Radiology Management company. She currently serves on the Board of Trustees of the NYU Medical Center Board, is a member of the Board of Directors for the New York University Hospital for Joint Diseases, and serves on the Board of Choose Living. Dr. Smith is the President and serves on the Board of Directors of The Stem for Life Foundation. 4

- 5. Larry A. May, Chief Financial Officer since January 2006. Mr. May, joined Neostem in September 2003 to assist with licensing activities. He worked for Amgen from 1983 until 1998 in several positions of increasing responsibility, becoming Vice President/Treasurer in 1997. From 1998 to 2000, Mr. May served as the Senior Vice President, Finance and Chief Financial Officer of Biosource International, Inc. From 2000 to 2003, Mr. May served as the Chief Financial Officer of Saronyx, Inc. From August 2003 to January 2005, Mr. May served as the Chief Financial Officer of NS California. In March 2005, Mr. May was appointed CEO of NS California and in May 2005 he was elected to the Board of Directors of NS California. He received a Bachelor of Science degree in Business Administration & Accounting in 1971 from the University of Missouri. Catherine M. Vaczy, Vice President and General Counsel since April 2005. From 1997 through 2003, Ms. Vaczy held various senior positions at ImClone Systems Incorporated, most recently as its Vice President, Legal and Associate General Counsel. From 1988 through 1996, Ms. Vaczy served as a corporate attorney at the New York City law firm of Ross & Hardies. Ms. Vaczy is Secretary and serves on the Board of Directors of The Stem for Life Foundation. Ms. Vaczy received a Bachelor of Arts degree in 1983 from Boston College and a Juris Doctor from St. John’s University School of Law in 1988. Jason Kolbert, Vice President of Strategic Business Development, MBA was formerly a managing director of National Securities where he founded the firm's biotechnology research effort. He spent the past 16 years on Wall Street as an analyst, both managing biotechnology dedicated investments (buy-side) and covering biotechnology companies (sell-side). Prior to his career on Wall Street he spent several years in the pharmaceutical industry with Schering-Plough in Japan. Mr. Kolbert has an undergraduate degree in Chemistry (New Paltz) and an MBA in Finance (University of New Haven). Ian Zhang, President of NeoStem China and Managing Director since September 2010. He held management and scientific positions in healthcare and biotechnology industries for the past ten years. Since January 2008, he held the position of Head of Corporate Development and Head of Integration for Asia Pacific at the Life Technology Corporation. In those positions, Mr. Zhang was responsible for strategic initiatives in the region to build capabilities and capture growth, identifying key investment markets in China and other regions, and managing acquisition and integration. Before that, he was President and General Manager of Dynal Biotech (Beijing) Ltd, a wholly owned subsidiary of Invitrogen serving the clinical transplant diagnostic market as well as medical research institutions and government agencies. Mr. Zhang holds a Ph. D. in biotechnology from Simon Fraser University and a MBA from the University of Chicago. Andrew L. Pecora, Chief Medical Officer, Progenitor Cell Therapy, M.D., F.A.C.P. since March 1999. He is scheduled to join the Board of Directors for NeoStem pending Board approval. Dr. Pecora currently serves as Vice President of Cancer Services and Chief Innovations Officer of the John Theurer Cancer Center at Hackensack University Medical Center, and Co-Managing Partner of the Northern New Jersey Cancer Center (NNJCC), which is a private physicians practice group affiliated with HUMC. Dr. Pecora currently serves as Chairman of the Board of Directors of Tetralogics, a private venture funded Biotechnology Company developing small molecules for cancer therapy and on the Board of directors of Cancer Genetics, a private venture funded cancer Diagnostics Company. Dr. Pecora is a Professor of Medicine at the University of Medicine and Dentistry of New Jersey. He serves on 5

- 6. the Board of Directors for the American Society for Blood and Marrow Transplantation. In addition, he has also served on the Board of Directors for the International Society of Hematotherapy and Graft Engineering, now the International Society for Cellular Therapy; the Accreditation Committee of the Affiliated Physicians Network; and as an Inspector for the Foundation for Accreditation of Hematopoietic Cell Therapy. Dr. Pecora received his medical degree from the University of Medicine and Dentistry of New Jersey, graduating with honors. He went on to complete his medical education in internal medicine at New York Hospital and in hematology and oncology at Memorial Sloan-Kettering Cancer Center, both in New York City. He is board certified in internal medicine, hematology, and oncology. Robert A. Preti, President and Chief Scientific Officer, Progenitor Cell Therapy, Ph.D. since March 1999. Dr. Preti is PCT's Co-Founder, President, and Chief Scientific Officer, and a member of the Company's Board of Managers. Previous positions held by Dr. Preti include Scientific and Laboratory Director of Hackensack University Medical Center's stem cell processing and research laboratory and Scientific Director of the Clinical Services Division at the New York Blood Center. Dr. Preti is a founding member of the International Society for Cellular Therapies, formerly the International Society for Hematotherapy and Graft Engineering, served on its Executive Committee and Board of Directors for 10 years, and serves on the Editorial Board for the society’s journal, Cytotherapy. He currently serves in his fourth term as Director for the AABB. Dr. Preti received his Doctor of Philosophy degree from New York University, graduating with distinction. 6

- 7. Distribution of Ratings and Disclosure of Banking Relationships: The following table shows WBB’s ratings distribution expressed as a percentage of all securities rated as of the end of the most recent calendar quarter, as well as the percentage of subject companies within each rating category for whom WBB has provided investment banking services within the previous 12 months. Percentage of Percentage of Covered Securities Banking Clients Buy 68.4% 11.5% Hold 10.5% 0% Sell 21.1% 0% The research analyst who is primarily responsible for the research contained in this research report and whose name is listed on this report: (1) attest that all of the views expressed in this research report accurately reflect that of the research analysts' personal views about any and all of the securities and issuers that are the subject of this research report; and (2) attest that no part of the research analysts' compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the research analysts in this research report. All WBB Securities, LLC ("WBB") employees, including research associates, receive compensation that is based in part upon the overall performance of the firm, including revenues generated by WBB's investment banking department, but not directly related to those revenues. Although information herein has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. Opinions and estimates may be changed or withdrawn without notice. This report is not intended as an offer or solicitation, or as the basis for any contract, for the purchase or sale of any security, loan or other instrument. We or our affiliates or persons associated with us or such affiliates (“Associated Persons”) do not now, but may in the future: maintain a long or short position in securities, loans or other instruments referred to herein or in other securities, loans or instruments of issuers named herein, or in related derivatives; purchase or sell, make a market in, or buy or sell on a principle basis, or engage in other transactions involving such securities, loans or instruments of such issuers; and/or provide investment banking, credit, or other services to any issuers named herein. The authors of this report and the officers of WBB do not now, but may in the future own options, rights or warrants to purchase any of the securities of the issuer whose securities are recommended, unless the extent of ownership is nominal. The past performance of securities, loans or other instruments does not guarantee or predict future performance. This report may not be reproduced or circulated without our written authority. 7