Top Rated Pune Call Girls Dighi ⟟ 6297143586 ⟟ Call Me For Genuine Sex Servi...

10 August Daily market report

1. Page 1 of 6

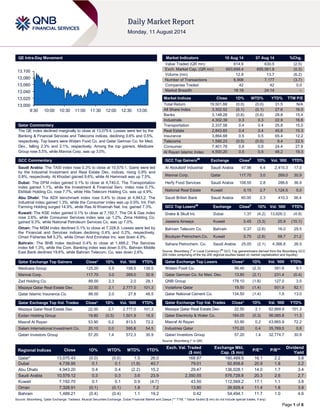

QE Intra-Day Movement

Qatar Commentary

The QE index declined marginally to close at 13,075.4. Losses were led by the

Banking & Financial Services and Telecoms indices, declining 0.6% and 0.5%,

respectively. Top losers were Widam Food Co. and Qatar German Co. for Med.

Dev., falling 2.3% and 2.1%, respectively. Among the top gainers, Medicare

Group rose 5.5%, while Mannai Corp. was up 3.0%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.3% to close at 10,579.1. Gains were led

by the Industrial Investment and Real Estate Dev. indices, rising 0.9% and

0.8%, respectively. Al Khodari gained 9.6%, while Al Hammadi was up 7.5%.

Dubai: The DFM index gained 0.1% to close at 4,740.0. The Transportation

index gained 1.1%, while the Investment & Financial Serv. index rose 0.7%.

Ekttitab Holding Co. rose 7.7%, while Hits Telecom Holding Co. was up 4.9%.

Abu Dhabi: The ADX benchmark index rose 0.4% to close at 4,943.2. The

Industrial index gained 1.3%, while the Consumer index was up 0.9%. Int. Fish

Farming Holding surged 14.9%, while Ras Al Khaimah Nat. Ins. gained 7.3%.

Kuwait: The KSE index gained 0.1% to close at 7,192.7. The Oil & Gas index

rose 2.6%, while Consumer Services index was up 1.2%. Zima Holding Co.

gained 9.3%, while National Petroleum Services Co. was up 7.0%.

Oman: The MSM index declined 0.1% to close at 7,328.9. Losses were led by

the Financial and Services indices declining 0.4% and 0.2%, respectively.

Oman Fisheries fell 5.2%, while Oman And Emirates Inv. was down 4.9%.

Bahrain: The BHB index declined 0.4% to close at 1,488.2. The Services

index fell 1.3%, while the Com. Banking index was down 0.5%. Bahrain Middle

East Bank declined 19.6%, while Bahrain Telecom. Co. was down 2.6%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Medicare Group 125.20 5.5 158.5 138.5

Mannai Corp. 117.70 3.0 269.0 30.9

Zad Holding Co. 89.00 2.3 2.0 28.1

Mazaya Qatar Real Estate Dev. 22.50 2.1 2,777.0 101.3

Qatar Islamic Insurance Co. 86.00 2.0 27.8 48.5

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 22.50 2.1 2,777.0 101.3

Ezdan Holding Group 19.80 (0.5) 1,501.9 16.5

Masraf Al Rayan 53.90 0.2 813.5 72.2

Salam International Investment Co. 20.10 0.0 595.8 54.5

Qatari Investors Group 57.20 1.4 572.3 30.9

Market Indicators 10 Aug 14 07 Aug 14 %Chg.

Value Traded (QR mn) 614.9 630.5 (2.5)

Exch. Market Cap. (QR mn) 693,699.4 695,561.8 (0.3)

Volume (mn) 12.8 13.7 (6.2)

Number of Transactions 6,908 7,177 (3.7)

Companies Traded 42 42 0.0

Market Breadth 18:19 24:14 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,501.88 (0.0) (0.0) 31.5 N/A

All Share Index 3,302.52 (0.1) (0.1) 27.6 16.0

Banks 3,148.28 (0.6) (0.6) 28.8 15.4

Industrials 4,302.39 0.3 0.3 22.9 16.6

Transportation 2,337.58 0.4 0.4 25.8 15.0

Real Estate 2,843.65 0.4 0.4 45.6 15.3

Insurance 3,864.68 0.5 0.5 65.4 12.2

Telecoms 1,590.23 (0.5) (0.5) 9.4 22.5

Consumer 7,401.78 0.8 0.8 24.4 27.8

Al Rayan Islamic Index 4,500.20 0.5 0.5 48.2 19.3

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Al Abdullatif Industrial Saudi Arabia 47.96 4.4 2,415.3 17.0

Mannai Corp. Qatar 117.70 3.0 269.0 30.9

Herfy Food Services Saudi Arabia 108.55 2.8 288.6 36.9

National Real Estate Kuwait 0.15 2.7 1,124.5 5.0

Saudi British Bank Saudi Arabia 60.00 2.3 410.3 36.4

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Drake & Skull Int. Dubai 1.37 (4.2) 13,626.3 (4.9)

Jazeera Airways Kuwait 0.45 (3.3) 25.9 (10.1)

Bahrain Telecom Co. Bahrain 0.37 (2.6) 16.0 29.5

Boubyan Petrochem.Co. Kuwait 0.75 (2.6) 68.7 21.2

Sahara Petrochem. Co. Saudi Arabia 25.05 (2.1) 4,366.8 26.5

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Widam Food Co. 56.40 (2.3) 391.6 9.1

Qatar German Co. for Med. Dev. 13.80 (2.1) 231.4 (0.4)

QNB Group 178.10 (1.8) 127.0 3.5

Vodafone Qatar 19.50 (1.4) 501.9 82.1

Qatar National Cement Co. 134.50 (1.4) 1.5 13.0

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 22.50 2.1 62,668.9 101.3

Qatar Electricity & Water Co. 184.00 (0.3) 56,085.8 11.3

Masraf Al Rayan 53.90 0.2 43,665.9 72.2

Industries Qatar 170.20 0.4 35,769.5 0.8

Qatari Investors Group 57.20 1.4 32,774.7 30.9

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,075.43 (0.0) (0.0) 1.5 26.0 168.87 190,489.9 16.1 2.2 3.8

Dubai 4,739.95 0.1 0.1 (1.9) 40.7 79.01 92,858.6 20.9 1.8 2.2

Abu Dhabi 4,943.20 0.4 0.4 (2.2) 15.2 29.47 136,028.1 14.0 1.7 3.4

Saudi Arabia 10,579.12 0.3 0.3 3.6 23.9 2,350.55 576,728.8 20.3 2.6 2.7

Kuwait 7,192.70 0.1 0.1 0.9 (4.7) 43.50 112,569.2 17.1 1.1 3.8

Oman 7,328.91 (0.1) (0.1) 1.8 7.2 13.90 26,929.4 11.4 1.8 3.8

Bahrain 1,488.21 (0.4) (0.4) 1.1 19.2 0.42 54,494.1 11.7 1.0 4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,000

13,020

13,040

13,060

13,080

13,100

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index declined marginally to close at 13,075.4. The

Banking & Fin. Ser. and Tele. indices led the losses. The index

fell on the back of selling pressure from Qatari shareholders

despite buying support from non-Qatari shareholders.

Widam Food Co. and Qatar German Co. for Med. Dev. were the

top losers, falling 2.3% and 2.1%, respectively. Among the top

gainers, Medicare Group rose 5.5%, while Mannai Corp. was up

3.0%.

Volume of shares traded on Sunday fell by 6.2% to 12.8mn from

13.7mn on Thursday. Further, as compared to the 30-day

moving average of 15.0mn, volume for the day was 14.2% lower.

Mazaya Qatar Real Estate Dev. and Ezdan Holding Group were

the most active stocks, contributing 21.6% and 11.7% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings

Earnings Releases

Company Market Currency

Revenue

(mn)2Q2014

% Change

YoY

Operating Profit

(mn) 2Q2014

% Change

YoY

Net Profit (mn)

2Q2014

% Change

YoY

Gulf Pharmaceutical

Industries (Julphar)

Abu Dhabi AED 368.3 0.6% – – 48.8 -10.4%

Oman Insurance Co. (OIC) Dubai AED 789.3 12.9% -9.2 NA 63.9 29.1%

Drake & Scull International

(DSI)

Dubai AED 1,101.4 -17.8% 24.9 -69.5% 25.9 -41.1%

Agility Logistics (Agility) Dubai KD – – – – 12.9 11.8%

Oman & Emirates

Investment Holding Co. *

Oman OMR – – – – 1.0 4.2%

Al Madina Investment** Oman OMR – – – – -0.7 NA

Ominvest* Oman OMR – – – – 9.4 20.1%

Source: Company data, DFM, ADX, MSM (* 1H2014 results, ** 1Q2015 results)

News

Qatar

IQCD posts weak 2Q2014 results – We expect to lower our

estimates post discussion with management; maintain

Accumulate rating given solid dividend yield and IQCD’s status

as a core long-term holding. With QR2.84bn posted in 1H2014

net income, our QR7.94bn estimate for FY2014 net income

(Bloomberg consensus: QR7.98bn) is clearly at risk. On the plus

side, a significant portion of planned shutdowns are behind us

(3Q2014 planned schedule – LLDPE: 5 days; steel: 86 days

[less than 10% of total production days]) and urea prices have

strengthened sequentially in 3Q2014. Moreover, IQCD stock

continues to provide a solid dividend yield (6.5% at QR11 a

share [in line with 2013] and 5.9% at QR10/share) and we

believe a significant dividend cut remains unlikely; IQCD’s

liquidity position remains solid at QR6.3bn. We recommend

investors Accumulate the stock on dips. Reported 2Q2014 net

profit misses estimates significantly due to prolonged

fertilizer shutdowns and lower-than-expected steel

profitability. IQCD posted 2Q2014 net income of QR1.25bn (-

21% QoQ, -38% YoY) vs. our estimate/Bloomberg consensus

of QR1.77bn/QR1.71bn. Share of results of JVs, which includes

the company’s share of profits from petrochemicals and

fertilizers, came in at QR857mn (-28% QoQ, -45% YoY) and

was also below our expectation significantly. 2Q2014 profitability

was impacted by significant planned/unplanned fertilizer

shutdowns, while steel margins also declined. Group EBITDA

came in at QR1.31bn (-20% QoQ, -37% YoY). Petrochemicals

(incl. fuel additives) performance was modestly lower vs.

our expectations. Revenue of QR1.47bn (+1% QoQ, +29%

YoY) was marginally lower than our model, while net income of

QR627mn (-8% QoQ, -26% YoY) also modestly fell short of our

estimate. PE prices gained QoQ and YoY, while sales volumes

improved sequentially given maintenance-related shutdowns in

1Q2014; in terms of 1H2014 shutdowns, the company’s

ethylene plants lost an average 36 days per plant (all in

1Q2014), LDPE lost 41 days per plant (12 days in 2Q2014) and

LLDPE lost 32 days (14 days in 2Q), following the general

shutdown. LDPE and LLDPE prices increased 11.3% YoY and

7.3% YoY, respectively. In terms of fuel additives, methanol

prices gained 27.7% YoY to $421/MT but came off more than

30% , on average, vs. 1Q2014 according to IQCD; Methanol

and MTBE lost a further 83 days in 2Q2014 (following 27 days in

1Q2014) following routine, planned maintenance. Overall,

2Q2014 utilization rate dropped further to 75.5% vs. 82% in 1Q

(prior historical average range of 95%-110%.) Net margins

dipped to 43% vs. 47% in 1Q2014 given lower fuel additive

(primarily Methanol) pricing and increased opex. Fertilizer

profitability bear the brunt of weak urea realizations and

longer-than-anticipated shutdowns. Revenue of QR1.15bn (-

17% QoQ, -30% YoY) modestly disappointed; urea price

realizations dropped 22.7% to $295/MT vs. $382/MT in 1Q2014

offsetting a marginal sequential increase in sales volume.

However, much higher-than-expected shutdowns, along with

increased opex, hurt profits, sending net margins to 20% in

2Q2014 vs. 37% in 1Q2014. Specifically on shutdowns, IQCD

reported that QAFCO’s ammonia trains 1-4 experienced

unplanned shutdowns. In 2Q2014, the company recorded an

additional 149 days of downtime (vs. 76 days in 1Q2014).

Overall, IQCD faced 225 lost days in 1H2014 vs. a budget of

160 days due to planned and unplanned shutdowns sending its

segment utilization to 88.5% for 1H2014 vs. 97.5% in 1H2013.

Launch and initial ramp-up of the new steel melt shop (1.1

MTPA billet-capacity) aided steel revenue growth but

profitability fell below estimates. For 2Q2014, QASCO

Overall Activity Buy %* Sell %* Net (QR)

Qatari 70.19% 72.53% (14,433,288.55)

Non-Qatari 29.81% 27.47% 14,433,288.55

3. Page 3 of 6

recorded revenue of QR1.82bn (+38% QoQ, +28% YoY) that

handily beat our estimate. While rebar price declined modestly

to QR2,389/MT vs. QR2,427/MT in 1Q2014, production from the

new EF-5 facility aided revenue. In 1H2014, a significant portion

of EF-5’s billet to date production of 336,000 MT was sold to the

100%-owned Dubai subsidiary Qatar Steel FZE to boost its wire

rod and rolling mill utilization rates; IQCD expects EF-5

production levels to gradually improve over the year. Overall, the

steel segment sold an additional 167,000 MT of billets and

91,000 MT of DRI/HBI in 2Q2014 vs. 1Q2014 to drive

sequential revenue growth. Net income of QR370mn (+3%

QoQ, -17% YoY) implied that net margins deteriorated

sequentially to 20% vs. 27% in 1Q2014 due to increased raw

material costs primarily associated with the EF-5 launch despite

a QoQ decline in iron ore prices. Catalysts: Future capacity

expansions and dividend growth. Access to incremental

feedstock supply could reignite earnings growth in the future. In

the interim, investors should benefit from IQCD’s industry-

leading dividend yield. Moreover, startup of commercial

production from the Al Sejeel Petrochemical project in early

2019 should boost petrochemical production capacity by around

25%; we will incorporate this project into our model as more

details become available. (QNBFS Research, IQCD Press

Release)

WDAM reports QR14.5 net profit in 2Q2014 – Widam Food

Company (WDAM) reported a net profit of QR14.5mn in 2Q2014

as compared to QR19.4mn in 1Q2014 (net profit of QR33.9mn

in 1H2014 compared to QR32.4mn in 1H2013). The Company’s

EPS amounted to QR1.88 in 1H2014 versus QR1.80 in 1H2013.

The company reported impairment on projects of QR4mn in

1H2014 which adversely impacted its bottom-line. WDAM’s

revenue increased 30.8% YoY to QR98.9mn in 2Q2014. For

1H2014, the company’s revenue grew 27.8% YoY to

QR195.4mn. (QE)

ORDS names Uber global Nojoom partner – Ooredoo

(ORDS) has announced Uber, a smartphone application

evolving the way the world moves, as the newest international

partner to join the 150+ Nojoom partner network. Nojoom

members can now earn and redeem Nojoom Points with Uber

rides in over 140 cities across 40 countries. (Peninsula Qatar)

International

Europe’s growth engine stutters as Spain beats Germany –

Germany probably underperformed Spain last quarter for the

first time in more than five years as the Euro area recovery

almost ground to a halt. According to a Bloomberg News survey,

after leading the currency bloc out of its longest-ever recession

last year, Europe’s largest economy contracted in the three

months through June. The downturn in the region’s powerhouse

highlights the fragility of a revival that European Central Bank

(ECB) President Mario Draghi has described as modest and

uneven. The 18-nation Euro area is struggling to boost growth

and inflation (ECCPEMUY) even amid unprecedented ECB

stimulus, with Draghi citing inadequate structural reforms as a

key reason. While the German data is distorted by mild winter

weather that front-loaded output earlier in the year, Bundesbank

President Jens Weidmann has warned that the country must

also adjust or risk losing its role as a growth engine. According

to the median estimate in the Bloomberg survey, German GDP

shrank 0.1% in the three months through June, the first

contraction since 2012. Separate surveys show the economies

of the Euro area and France grew 0.1%. (Bloomberg)

UK record-low interest rate is justified – According to a

Bloomberg survey, Mark Carney’s justification for keeping the

Bank of England’s(BoE) benchmark interest rate at a record low

has the backing of economists. Sixty-seven percent of 33

respondents said there is still enough slack in the economy to

justify holding the key rate at 0.5%, where it has been since

March 2009. The BoE has put spare capacity at about 1% to

1.5% of GDP. As Carney prepares to publish new forecasts in

two days and update investors on his views, the level of slack

remains a pivotal issue. Conflicting signals from wage and

employment data are dividing the Monetary Policy Committee

over how the pick-up in the economy will feed through to

inflation and when rate increases need to start. Eleven of the 21

economists in the Bloomberg survey agree with the BoE’s

assessment that the slack in the economy is within its estimated

range. Nine said it is less than 1%, and one said it was more

than 1.5% of GDP. Carney said last month that while there may

be more labor supply than previously thought, it is also true that

the spare capacity is being used up a bit more rapidly than BoE

had expected. (Bloomberg)

China loosens monetary conditions in test of credit power –

According to Bloomberg LP gauge, China loosened monetary

conditions last quarter at the fastest pace in almost two years,

testing the waning effectiveness of credit in supporting economic

growth. Bloomberg’s new China Monetary Conditions Index – a

weighted average of loan growth, real interest rates and China’s

real effective exchange rate – rose 6.71 points to 82.81 in the

second quarter from the previous three months. That’s the

biggest jump since the July-September period of 2012, with May

and June’s numbers the first back-to-back readings above 80

since January 2012. According to a Bloomberg News survey of

analysts, New Yuan loans in July will be a record high for that

month, suggesting officials are keeping the credit spigot open

even as debt risks mount. While consumer inflation below the

government’s goal allows room for more easing, economic data

will determine how far policy makers go. (Bloomberg)

Regional

Korea, GCC to diversify economic ties to boost growth –

The Head of the Middle East and Africa Team, Korea Institute

for International Economic Policy has called for diversification of

economic cooperation between South Korea and the GCC

countries. The GCC countries are Korea’s major trading

partners in the Middle East (Mideast). Exports from Korea to the

GCC reached $17.8bn in 2013, accounting for 3.2% of the

country’s exports. Major export products include automobiles,

steel products, machinery, and electronics. Korea’s imports from

the GCC were valued at $105.8bn in 2013, making up a fifth of

all imports. The reason for this wide trade imbalance is that

Korea imports large amounts of oil & gas from the GCC; indeed,

the GCC supplied 71.2% of Korea’s crude oil imports and 52.4%

of its natural gas imports in 2013. (GulfBase.com)

NCB: Saudi Arabia expands ethylene output capacity –

According to a report released by NCB’s Economics Department

Research Team, Saudi Arabia is maintaining its leading position

as the region’s largest petrochemical producer with an annual

86.4mn tons of capacity. The majority of capacity additions

within the GCC region during the 2007-2012 period took place in

Saudi Arabia, which accounted for 64% of the region’s capacity

additions. With 17.5mn tons per year, Saudi Arabia is the largest

ethylene producer in the region, representing 72% of the

regional ethylene capacity, up by 7.7mn tons per year as

compared to five years ago. This expansion in ethylene

production capacity has resulted in Saudi Arabia becoming the

third-largest producer worldwide, constituting 11% of global

ethylene capacity. (GulfBase.com)

Maaden submits capital increase request to Saudi CMA –

Saudi Arabian Mining Company (Maaden) has submitted a

4. Page 4 of 6

capital increase request to the Saudi Capital Market Authority

(CMA). The announcement is in reference with its previous

announcement about the board’s recommendation on increasing

capital through a rights issue. (Tadawul)

Saudi PetroRabigh restarts units after Saturday shutdown –

Saudi Arabia’s PetroRabigh is gradually resuming production

after a technical failure at one of its units forced a shutdown of

some operations on Saturday. The unit, which handles air

supply for control systems, has now restarted and other units

are gradually coming back online, with normal operations

expected to resume by this Friday. The disruption will cause

PetroRabigh’s 3Q2014 profit to fall by nearly SR30mn.

(Bloomberg)

Tiger Properties launches Al Manara Tower – UAE-based

Tiger Properties has launched Al Manara Tower in Jumeirah

Village Circle at a cost of over AED200mn. The construction

work on Al Manara Tower has already reached 20% and once

finished, the premium lifestyle development will be home to 300

residential units comprising studio and one & two-bedroom

apartments. The project is expected to be completed in 24

months. (GulfBase.com)

AGT: UAE lighting industry to grow by 15% in 2015 – Al

Yousuf GreenTech (AGT) is planning to launch more energy-

efficient lighting products in the UAE. AGT’s General Manager

Mohamed Al Rashed said that the UAE lighting industry is now

worth AED1bn and is estimated to grow by 15% in 2015.

Energy-efficient lighting products make about 20% of that, but

will grow at a much higher annual growth rate of 300% in 2015,

due to new regulations on use of conventional lighting. This

enables the Dubai government to build a sustainable and eco-

friendly emirate. (GulfBase.com)

Dubai Customs processes 4.5mn transactions in 1H2014 –

According to Dubai Customs, it processed 4.5mn transactions in

1H2014 as compared to 4.1mn in 1H2013. Dubai Customs has

seen a leap of 10% in the transactions processed in 1H2014,

reflecting the UAE’s strong economy, growing business and

investment appeal. (GulfBase.com)

Emicool secures $245mn financing for expansion – Dubai-

based Emirates District Cooling (Emicool) has signed a

AEDh900mn 12-year facility with Dubai Islamic Bank (DIB), to

refinance its existing debt and also fund the company’s

expansion plans. Emicool – a venture between Dubai

Investments and Union Properties – offers cooling services in

some areas of the emirate and has an installed capacity of

330,000 tons of refrigerant. (Reuters)

Mobily signs agreement with Al-Yasra – Etihad Etisalat

Company (Mobily) has signed an agreement to add Al-Yasra

Group to its exclusive list of Neqaty program partners. The

agreement allows Mobily’s subscribers to collect and also

redeem Neqaty points at global brand outlets of Al-Yasra in

Saudi Arabia. This agreement further strengthens the Neqaty

program’s position as the leading rewards program in Saudi

Arabia’s telecom industry, a program which not just allows

subscribers to earn points for their usage for Mobily services but

also collect points at select partner stores. (GulfBase.com)

UAE's Dana Gas says tribunal gives favorable ruling on Iran

deal – UAE-based energy firm Dana Gas said an international

tribunal had issued a favorable ruling in the dispute over a

natural gas supply contract between its affiliate Crescent

Petroleum and Iran. Dana said that the tribunal issued a ruling

that a 25-year contract for National Iranian Oil Company (NIOC)

to supply gas to Crescent was valid and binding on both parties,

and that NIOC has been obligated to deliver gas since

December 2005. NIOC and Crescent signed the 25-year

contract in 2001, with the price linked to oil. But deliveries were

delayed as oil prices rose and some officials and politicians in

Iran called for a revision in the gas pricing formula. According to

sources, supplies would not begin in the near-term, since

subsidiary agreements needed to be reached and infrastructure

work completed. Sources said that the contract provides for the

UAE to import some 600mn cubic feet per day of Iranian gas,

though the actual amount will depend on many factors and may

only become clear in the coming months.(Reuters)

$20bn Kuwait Metro to have 61 stations – The $20bn planned

Kuwait Metro Project will have 61 stations on three railway lines

covering all areas and governorates of the country. The work on

the project is expected to start in 2017, and will be implemented

on a public-private partnership basis. (GulfBase.com)

KIPCO rejects $3.2bn offer for OSN – Kuwait Projects

Company (KIPCO) announced that it rejected a $3.2bn offer

from a US private equity firm for a majority stake in pay-

television company OSN. KIPCO owns 60.5% of OSN, while

Saudi Arabia-based Mawarid Group holds the remainder. The

offer comprised $2.4bn in cash and a further $800mn subject to

certain conditions. (Bloomberg)

DNO Oman plans exploratory wells in Block 36 – Norwegian

oil & gas company, DNO International is planning to drill two

exploratory wells in Block 36 onshore Oman. Block 36 is a

roughly 18,000 square kilometer frontier exploration block

located in the prolific Rub Al Khali basin. According to DNO, two

of the three exploration wells drilled previously on the block have

pointed to the presence of source rock found in a majority of the

oil & gas fields discovered elsewhere around the Arabian

Peninsula. All three exploration wells had hydrocarbon shows.

(GulfBase.com)

Oman’s MoTC awards project management contract to Hill

International – Oman’s Ministry of Transport and

Communications (MoTC) has awarded a contract to Hill

International to provide project management services in

connection with the construction of Sections 1 and 2 of the

Bidbid Sur Road. The three-year contract has an estimated

value of approximately OMR1.5mn. The OMR432mn project

includes nine interchanges, two underpasses, two overpasses,

associated retaining wall structures and approximately 171

reinforced concrete culverts. (GulfBase.com)

NCSI: Salalah Port and SPQ cargo volumes surge –

According to a vessel movement report by National Centre for

Statistics and Information (NCSI), vessel activities at Port Sultan

Qaboos (SPQ) and Salalah Port witnessed growth in terms of

unloaded and loaded (export) cargo in 1H2014 as compared to

the same period in 2013. The total volume of cargo handled in

both ports increased by 2.5% and 34.9%, respectively, as

compared to the same period in 2013. The total volume of

unloaded cargo and loaded export cargo at Port Sultan Qaboos

during the January 2014-June 2014 period reached 2.81mn

tons, as compared to 2.75mn tons handled over the same

period in 2013. The increase is attributed to the growth of total

unloaded cargo over the same period by 0.5%, totaling 2.27mn

tons by the end of June 2014, as compared to 2.26mn tons by

the end of June 2013. Loaded cargo exports from SPQ totaled

540,000 tons in 1H2014 as compared to 496,000 tons in

1H2013, representing a growth of 8.8%. (GulfBase.com)

BMI Bank reports loss of BHD3.1mn for 1H2014 – BMI Bank

reported a loss after provisions of BHD3.1mn for 1H2014 as

compared to a net profit of BHD540,000 in 1H2013. Total assets

at the end of 1H2014 stood at BHD760mn as against

BHD730mn a year earlier. Total loans & advances stood at the

5. Page 5 of 6

same level of BHD370mn at the end of 1H2014 as compared to

the figure recorded in 1H2013. Customer deposits grew from

BHD530mn at the end of 2013 to BHD550mn at the end of the

2Q204 at an annualized growth rate of 9.5%. (GulfBase.com)

KHCB 2Q2014 net profit up 166.9% YoY – Khaleeji

Commercial Bank (KHCB) recorded a net profit of BHD1.2mn

reflecting an increase of 166.9% as compared to BHD0.45mn in

2Q2013, an increase of BHD0.865 from 1Q2014. The bank’s

financial position remains strong with a liquid asset ratio of 27.2

% and a capital adequacy ratio of 24.2 %. (GulfBase.com)

Investcorp completes sale of SourceMedia – Investcorp has

completed the sale of SourceMedia to Observer Capital. The

sale of SourceMedia follows an active year for Investcorp’s

corporate investment group, which deployed $609mn across five

acquisitions in the fiscal year ending June 30, 2014.

(GulfBase.com)

Al Baraka Bank posts 3.8% rise in 2Q2014 net profit –

Bahrain-based Al Baraka Banking Group posted a 3.8%

increase in 2Q2014 net income. The bank, which has operations

in the Middle East, Asia and Africa, made a net attributable profit

of $43.8mn in 2Q2014 as compared to $42.2mn in 2Q2013.

Total assets stood at $22.1bn in 1H2014, up from $19.5bn a

year earlier. (Reuters)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

0.3%

(0.0%)

0.1%

(0.4%)

(0.1%)

0.4%

0.1%

(0.6%)

(0.4%)

(0.2%)

0.0%

0.2%

0.4%

0.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,310.95 0.0 0.0 8.7 DJ Industrial 16,553.93 0.0 0.0 (0.1)

Silver/Ounce 19.89 0.0 0.0 2.2 S&P 500 1,931.59 0.0 0.0 4.5

Crude Oil (Brent)/Barrel (FM

Future)

105.02 0.0 0.0 (5.2) NASDAQ 100 4,370.90 0.0 0.0 4.7

Natural Gas (Henry

Hub)/MMBtu

3.91 0.0 0.0 (9.9) STOXX 600 324.91 0.0 0.0 (1.0)

LPG Propane (Arab Gulf)/Ton 102.50 0.0 0.0 (18.8) DAX 9,009.32 0.0 0.0 (5.7)

LPG Butane (Arab Gulf)/Ton 118.63 0.0 0.0 (13.1) FTSE 100 6,567.36 0.0 0.0 (2.7)

Euro 1.34 0.0 0.0 (2.4) CAC 40 4,147.81 0.0 0.0 (3.4)

Yen 102.04 0.0 0.0 (3.1) Nikkei 14,778.37 0.0 0.0 (9.3)

GBP 1.68 0.0 0.0 1.3 MSCI EM 1,045.51 0.0 0.0 4.3

CHF 1.10 0.0 0.0 (1.4) SHANGHAI SE Composite 2,194.43 0.0 0.0 3.7

AUD 0.93 0.0 0.0 4.0 HANG SENG 24,331.41 0.0 0.0 4.4

USD Index 81.39 0.0 0.0 1.7 BSE SENSEX 25,329.14 0.0 0.0 19.6

RUB 36.18 0.0 0.0 10.1 Bovespa 55,572.93 0.0 0.0 7.9

BRL 0.44 0.0 0.0 3.5 RTS 1,170.60 0.0 0.0 (18.9)

187.9

161.3

145.4

![Page 2 of 6

Qatar Market Commentary

The QE index declined marginally to close at 13,075.4. The

Banking & Fin. Ser. and Tele. indices led the losses. The index

fell on the back of selling pressure from Qatari shareholders

despite buying support from non-Qatari shareholders.

Widam Food Co. and Qatar German Co. for Med. Dev. were the

top losers, falling 2.3% and 2.1%, respectively. Among the top

gainers, Medicare Group rose 5.5%, while Mannai Corp. was up

3.0%.

Volume of shares traded on Sunday fell by 6.2% to 12.8mn from

13.7mn on Thursday. Further, as compared to the 30-day

moving average of 15.0mn, volume for the day was 14.2% lower.

Mazaya Qatar Real Estate Dev. and Ezdan Holding Group were

the most active stocks, contributing 21.6% and 11.7% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings

Earnings Releases

Company Market Currency

Revenue

(mn)2Q2014

% Change

YoY

Operating Profit

(mn) 2Q2014

% Change

YoY

Net Profit (mn)

2Q2014

% Change

YoY

Gulf Pharmaceutical

Industries (Julphar)

Abu Dhabi AED 368.3 0.6% – – 48.8 -10.4%

Oman Insurance Co. (OIC) Dubai AED 789.3 12.9% -9.2 NA 63.9 29.1%

Drake & Scull International

(DSI)

Dubai AED 1,101.4 -17.8% 24.9 -69.5% 25.9 -41.1%

Agility Logistics (Agility) Dubai KD – – – – 12.9 11.8%

Oman & Emirates

Investment Holding Co. *

Oman OMR – – – – 1.0 4.2%

Al Madina Investment** Oman OMR – – – – -0.7 NA

Ominvest* Oman OMR – – – – 9.4 20.1%

Source: Company data, DFM, ADX, MSM (* 1H2014 results, ** 1Q2015 results)

News

Qatar

IQCD posts weak 2Q2014 results – We expect to lower our

estimates post discussion with management; maintain

Accumulate rating given solid dividend yield and IQCD’s status

as a core long-term holding. With QR2.84bn posted in 1H2014

net income, our QR7.94bn estimate for FY2014 net income

(Bloomberg consensus: QR7.98bn) is clearly at risk. On the plus

side, a significant portion of planned shutdowns are behind us

(3Q2014 planned schedule – LLDPE: 5 days; steel: 86 days

[less than 10% of total production days]) and urea prices have

strengthened sequentially in 3Q2014. Moreover, IQCD stock

continues to provide a solid dividend yield (6.5% at QR11 a

share [in line with 2013] and 5.9% at QR10/share) and we

believe a significant dividend cut remains unlikely; IQCD’s

liquidity position remains solid at QR6.3bn. We recommend

investors Accumulate the stock on dips. Reported 2Q2014 net

profit misses estimates significantly due to prolonged

fertilizer shutdowns and lower-than-expected steel

profitability. IQCD posted 2Q2014 net income of QR1.25bn (-

21% QoQ, -38% YoY) vs. our estimate/Bloomberg consensus

of QR1.77bn/QR1.71bn. Share of results of JVs, which includes

the company’s share of profits from petrochemicals and

fertilizers, came in at QR857mn (-28% QoQ, -45% YoY) and

was also below our expectation significantly. 2Q2014 profitability

was impacted by significant planned/unplanned fertilizer

shutdowns, while steel margins also declined. Group EBITDA

came in at QR1.31bn (-20% QoQ, -37% YoY). Petrochemicals

(incl. fuel additives) performance was modestly lower vs.

our expectations. Revenue of QR1.47bn (+1% QoQ, +29%

YoY) was marginally lower than our model, while net income of

QR627mn (-8% QoQ, -26% YoY) also modestly fell short of our

estimate. PE prices gained QoQ and YoY, while sales volumes

improved sequentially given maintenance-related shutdowns in

1Q2014; in terms of 1H2014 shutdowns, the company’s

ethylene plants lost an average 36 days per plant (all in

1Q2014), LDPE lost 41 days per plant (12 days in 2Q2014) and

LLDPE lost 32 days (14 days in 2Q), following the general

shutdown. LDPE and LLDPE prices increased 11.3% YoY and

7.3% YoY, respectively. In terms of fuel additives, methanol

prices gained 27.7% YoY to $421/MT but came off more than

30% , on average, vs. 1Q2014 according to IQCD; Methanol

and MTBE lost a further 83 days in 2Q2014 (following 27 days in

1Q2014) following routine, planned maintenance. Overall,

2Q2014 utilization rate dropped further to 75.5% vs. 82% in 1Q

(prior historical average range of 95%-110%.) Net margins

dipped to 43% vs. 47% in 1Q2014 given lower fuel additive

(primarily Methanol) pricing and increased opex. Fertilizer

profitability bear the brunt of weak urea realizations and

longer-than-anticipated shutdowns. Revenue of QR1.15bn (-

17% QoQ, -30% YoY) modestly disappointed; urea price

realizations dropped 22.7% to $295/MT vs. $382/MT in 1Q2014

offsetting a marginal sequential increase in sales volume.

However, much higher-than-expected shutdowns, along with

increased opex, hurt profits, sending net margins to 20% in

2Q2014 vs. 37% in 1Q2014. Specifically on shutdowns, IQCD

reported that QAFCO’s ammonia trains 1-4 experienced

unplanned shutdowns. In 2Q2014, the company recorded an

additional 149 days of downtime (vs. 76 days in 1Q2014).

Overall, IQCD faced 225 lost days in 1H2014 vs. a budget of

160 days due to planned and unplanned shutdowns sending its

segment utilization to 88.5% for 1H2014 vs. 97.5% in 1H2013.

Launch and initial ramp-up of the new steel melt shop (1.1

MTPA billet-capacity) aided steel revenue growth but

profitability fell below estimates. For 2Q2014, QASCO

Overall Activity Buy %* Sell %* Net (QR)

Qatari 70.19% 72.53% (14,433,288.55)

Non-Qatari 29.81% 27.47% 14,433,288.55](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)