19 June Daily market report

•

0 recomendaciones•1,675 vistas

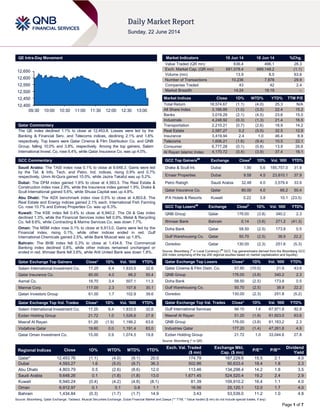

The QE index in Qatar declined 1.1% led by losses in the Banking & Financial Services and Telecom indices. Qatar Cinema & Film Distribution Co. and QNB Group were the top losers falling 10% and 3.8% respectively. Trading activity increased compared to the previous day but remained below the 30-day average. Regional indices were mixed with Saudi Arabia and Oman rising slightly while others fell. The document provides market commentary and data on trading activity in Qatar and other GCC markets.

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a 19 June Daily market report

Similar a 19 June Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

19 June Daily market report

- 1. Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE index declined 1.1% to close at 12,453.8. Losses were led by the Banking & Financial Serv. and Telecoms indices, declining 2.1% and 1.6% respectively. Top losers were Qatar Cinema & Film Distribution Co. and QNB Group, falling 10.0% and 3.8%, respectively. Among the top gainers, Salam International Invest. Co. rose 6.4%, while Qatar Insurance Co. was up 4.0%. GCC Commentary Saudi Arabia: The TASI index rose 0.1% to close at 9,648.3. Gains were led by the Tel. & Info. Tech. and Petro. Ind. indices, rising 0.9% and 0.7% respectively. Umm Al-Qura gained 10.0%, while Jazira Takaful was up 5.2%. Dubai: The DFM index gained 1.6% to close at 4,593.3. The Real Estate & Construction index rose 2.9%, while the Insurance index gained 1.9%. Drake & Scull International gained 5.6%, while Shuaa Capital was up 4.8%. Abu Dhabi: The ADX benchmark index rose 0.5% to close at 4,803.8. The Real Estate and Energy indices gained 2.1% each. International Fish Farming Co. rose 10.7% and Eshraq Properties Co. was up 6.3%. Kuwait: The KSE index fell 0.4% to close at 6,940.2. The Oil & Gas index declined 1.3%, while the Financial Services index fell 0.9%. Metal & Recycling Co. fell 8.6%, while Contracting & Marine Services Co. was down 7.7%. Oman: The MSM index rose 0.1% to close at 6,913.0. Gains were led by the Financial index, rising 0.1%, while other indices ended in red. Gulf International Chemicals gained 2.5%, while Bank Muscat was up 1.8%. Bahrain: The BHB index fell 0.3% to close at 1,434.8. The Commercial Banking index declined 0.8%, while other indices remained unchanged or ended in red. Ithmaar Bank fell 3.6%, while Ahli United Bank was down 1.8%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Salam International Investment Co. 17.25 6.4 1,833.5 32.6 Qatar Insurance Co. 80.00 4.0 66.2 50.4 Aamal Co. 16.70 3.4 507.1 11.3 Mannai Corp. 117.00 2.3 107.8 30.1 Qatari Investors Group 61.00 1.7 102.9 39.6 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Salam International Investment Co. 17.25 6.4 1,833.5 32.6 Ezdan Holding Group 21.72 1.0 1,526.6 27.8 Masraf Al Rayan 51.20 (1.9) 1,199.2 63.6 Vodafone Qatar 19.60 0.0 1,191.4 83.0 Qatar Oman Investment Co. 15.00 0.9 1,074.5 19.8 Market Indicators 19 Jun 14 18 Jun 14 %Chg. Value Traded (QR mn) 636.4 496.1 28.3 Exch. Market Cap. (QR mn) 681,578.4 689,148.2 (1.1) Volume (mn) 13.9 8.5 63.6 Number of Transactions 10,236 7,878 29.9 Companies Traded 43 42 2.4 Market Breadth 14:24 19:19 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,574.67 (1.1) (4.0) 25.3 N/A All Share Index 3,166.89 (1.0) (3.5) 22.4 15.2 Banks 3,019.29 (2.1) (4.5) 23.6 15.0 Industrials 4,248.92 (0.3) (1.3) 21.4 16.5 Transportation 2,210.21 (0.7) (2.6) 18.9 14.2 Real Estate 2,587.27 0.2 (5.5) 32.5 12.9 Insurance 3,419.94 2.4 1.0 46.4 8.9 Telecoms 1,606.21 (1.6) (9.4) 10.5 22.1 Consumer 6,777.28 (0.1) (0.8) 13.9 26.6 Al Rayan Islamic Index 4,170.72 (0.4) (3.9) 37.4 18.1 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Drake & Scull Int. Dubai 1.90 5.6 185,757.0 31.9 Emaar Properties Dubai 9.58 4.5 23,810.1 37.9 Petro Rabigh Saudi Arabia 32.48 4.0 3,579.4 33.9 Qatar Insurance Co. Qatar 80.00 4.0 66.2 50.4 IFA Hotels & Resorts Kuwait 0.22 3.8 10.1 (23.5) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% QNB Group Qatar 176.00 (3.8) 340.2 2.3 Ithmaar Bank Bahrain 0.14 (3.6) 271.2 (41.3) Doha Bank Qatar 58.50 (2.5) 173.8 0.5 Gulf Warehousing Co. Qatar 50.70 (2.5) 38.9 22.2 Ooredoo Qatar 130.00 (2.3) 251.8 (5.3) Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Cinema & Film Distri. Co. 57.60 (10.0) 21.6 43.6 QNB Group 176.00 (3.8) 340.2 2.3 Doha Bank 58.50 (2.5) 173.8 0.5 Gulf Warehousing Co. 50.70 (2.5) 38.9 22.2 Ooredoo 130.00 (2.3) 251.8 (5.2) Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Gulf International Services 94.10 1.4 67,971.8 92.8 Masraf Al Rayan 51.20 (1.9) 61,923.0 63.6 QNB Group 176.00 (3.8) 61,183.2 2.3 Industries Qatar 177.20 (1.4) 47,261.8 4.9 Ezdan Holding Group 21.72 1.0 33,044.6 27.8 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,453.76 (1.1) (4.0) (9.1) 20.0 174.79 187,229.6 15.5 2.1 4.0 Dubai 4,593.27 1.6 (5.0) (9.7) 36.3 502.86 90,633.4 18.4 1.8 2.3 Abu Dhabi 4,803.79 0.5 (2.6) (8.6) 12.0 113.46 134,298.4 14.2 1.8 3.5 Saudi Arabia 9,648.26 0.1 (1.8) (1.8) 13.0 1,671.45 524,520.4 19.2 2.4 2.9 Kuwait 6,940.24 (0.4) (4.2) (4.8) (8.1) 81.39 109,910.2 16.4 1.1 4.0 Oman 6,912.97 0.1 0.1 0.8 1.1 16.56 25,120.1 12.0 1.7 4.0 Bahrain 1,434.84 (0.3) (1.7) (1.7) 14.9 3.43 53,539.0 11.2 1.0 4.8 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,400 12,450 12,500 12,550 12,600 12,650 09:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE index declined 1.1% to close at 12,453.8. The Banking & Financial Serv. and Telecoms indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders. Qatar Cinema & Film Distribution Co. and QNB Group were the top losers, falling 10.0% and 3.8% respectively. Among the top gainers, Salam International Investment Co. rose 6.4%, while Qatar Insurance Co. was up 4.0%. Volume of shares traded on Thursday rose by 63.6% to 13.9mn from 8.5mn on Wednesday. However, as compared to the 30- day moving average of 24.8mn, volume for the day was 43.9% lower. Salam International Investment Co. and Ezdan Holding Group were the most active stocks, contributing 13.2% and 11.0% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Islamic Development Bank (IsDB) Fitch Saudi Arabia LT IDR/ST IDR AAA/F1+ AAA/F1+ – Stable – The Saudi British Bank (SABB) CI Saudi Arabia FSR/LT FCR/ST FCR A+/A+/A1 A+/A+/A1 – Stable – AlBaraka Islamic Bank (AIB) CI Bahrain FSR/LT FCR/ST FCR BB/BB/A3 BB/BB/A3 – Stable – United Gulf Bank (UGB) CI Bahrain FSR/LT FCR/ST FCR BBB/BBB/A3 BBB/BBB/A3 – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency) Earnings Releases Company Market Currency Revenue (mn)1Q2014 % Change YoY Operating Profit (mn) 1Q2014 % Change YoY Net Profit (mn) 1Q2014 % Change YoY Al Firdous Holdings* Dubai AED 16.5 25.5% – – 1.7 119.5% Source: Company data, DFM, ADX, MSM, (*FY 2013-14 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 06/19 US Bloomberg Bloomberg Economic Expectations June 48.5 – 42.5 06/19 US Bloomberg Bloomberg Consumer Comfort 15 June 37.1 – 35.5 06/20 EU European Central Bank ECB Current Account SA April 21.5B – 19.6B 06/20 EU European Central Bank Current Account NSA April 18.7B – 21.6B 06/20 EU European Commission Consumer Confidence June -7.4 -6.5 -7.1 06/20 France French Labor Office Wages QoQ 1Q2014 0.60% – 0.60% 06/20 Germany Destatis PPI MoM May -0.20% 0.00% -0.10% 06/20 Germany Destatis PPI YoY May -0.80% -0.70% -0.90% 06/19 UK CBI CBI Trends Total Orders June 11.0 2.0 0.0 06/19 UK CBI CBI Trends Selling Prices June 3.0 5.0 4.0 06/20 UK ONS Public Finances (PSNCR) May 8.5B – -10.8B 06/20 UK ONS Central Government NCR May 12.4B – 1.9B 06/20 UK ONS Public Sector Net Borrowing May 11.5B 12.0B 9.0B 06/20 UK ONS PSNB ex Interventions May 13.3B 8.7B 6.8B 06/20 UK ONS PSNB ex Royal Mail, APF May 13.3B 12.2B 10.9B 06/19 Italy Banca D'Italia Current Account Balance April 2,033M – 1,005M 06/20 Italy ISTAT Industrial Sales MoM April -0.20% – 0.40% 06/20 Italy ISTAT Industrial Sales WDA YoY April 2.20% – 2.60% 06/20 Italy ISTAT Industrial Orders MoM April 3.80% 1.00% 1.40% 06/20 Italy ISTAT Industrial Orders NSA YoY April 6.20% – 2.80% 06/19 Japan METI All Industry Activity Index MoM April -4.30% -4.10% 1.50% 06/19 Japan ESRI Leading Index CI April 106.5 – 106.6 06/19 Japan ESRI Coincident Index April 111.1 – 111.1 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari 54.11% 52.94% 7,440,593.95 Non-Qatari 45.89% 47.06% (7,440,593.95)

- 3. Page 3 of 7 News Qatar Qatar to benefit from robust global LNG demand – QNB Group (QNBK) said that the global demand for liquefied natural gas (LNG) is likely to keep prices high over the next few years. Demand is growing both as a result of a strong Asian economic growth and the switch to cleaner energy, particularly in China. In its weekly analysis, QNB stated that this trend is likely to continue, notwithstanding the so-called US shale gas revolution and the coming into operations of the $400bn Russia-China gas pipeline signed on May 21, 2014. Overall, the future of the LNG market remains bright and is likely to result in high LNG prices for years to come. This will continue to support Qatar’s large current account surpluses, which continues to be the largest LNG exporter, with about one third of global supply. The global LNG market continued to tighten in 2013, with LNG deliveries estimated at 240m tons, which was broadly flat as compared to 2012. At the same time, demand from Asia and Latin America increased, with China, South Korea and Mexico registering the largest increase. In particular, China brought three new re- gasification terminals online as its switch from coal to LNG as a cleaner fuel for electricity production continued. This tightening of the market resulted in an average $1 increase in LNG prices per million British thermal units (mBtu), despite Brent crude oil prices falling $4.5 per barrel and lower LNG demand from Europe. The outlook for the LNG market is likely to continue along similar trends in 2014. On the supply side, three new LNG trains in Algeria, Australia and Papua New Guinea are expected to come on-stream in 2014. This is likely to add about 10m tons to global LNG production, a 4.2% increase. On the demand side, continued growth in Asian demand and the need for Europe to diversify away from Russian pipeline gas may outpace the increased supply, leading to a small increase in LNG prices of about $0.5 per mBtu despite the expected decline in Brent crude oil prices. The ongoing violence in Iraq and Syria could, however, result in higher-than-expected LNG and crude oil prices in the second half of 2014. Over the medium term, global LNG exports are unlikely to meet the growing global demand, leading to higher LNG prices. (Bloomberg) AIECGC: Qatar’s GDP to touch $220.6bn by 2015 – Arab Investment & Export Credit Guarantee Corporation (AIECGC) said that Qatar’s GDP is projected to reach $220.6bn by 2015, after touching $209bn by the end of 2014. In its report, AIECGC stated that Qatar ranks top among Arab countries in terms of per capita income, which would reach $106,700 by 2015. The average annual per capita income of Arab citizens during 2005- 2009 was $5,067, which reached to $8,171 in 2013. The figure would go up to $8,402 by the end of 2014 and is expected to reach $8,591 by 2015. Meanwhile, foreign currency reserves of Arab countries jumped during the period of 2000-2009 from an annual average of $730bn to $1,374bn in 2013. It is expected to rise to $1,482bn by year-end. (Peninsula Qatar) QNB First launches Global Recognition Program in 5 countries – QNB Group (QNBK) will simultaneously launch its “Global Recognition Program” in five countries, to cater to premium customers in Qatar, Oman, Kuwait, UK, and France. QNBK’s General Manager–Group Retail Heba al-Tamimi said that the premium banking service will be launched by QNB First as the first service of its kind offered by a regional bank. She said as the first banking initiative of its type in the MENA region, the Global Recognition Program is a comprehensive suite of premium financial products and services. Importantly, QNB First has taken the next step in extending its service to this affluent customer segment within Qatar and across its expanding network abroad. (Gulf-Times.com) Six top Qatar companies on ‘Forbes Global 2000 list’ – QNB Group (QNBK), Industries Qatar (IQCD), Qatar Insurance (QATI), Woqod (QFLS), Ooredoo (ORDS) and the Qatar Electricity & Water Company (QEWS) are among the top Arab companies that figured in the ‘Forbes Global 2000’ list. In the Banking category, QNBK took the top spot. Qatar registered nine entries out of a total of 101 banks included in the ranking. For the second year, IQCD took the top position in the Industrials category with a market value of $31.3bn. In total, 107 Middle East companies figured in this list. In the Services category, QEWS topped the list, while QATI and Qatar General Insurance are in second and third positions, respectively, in the Insurance category. As many as 31 companies from the region’s insurance sector have been featured in 2014. In the Retail category, Woqod topped the list with revenues of $3.5bn and market value of $4.4bn. ORDS has made the cut among the top Telecom companies from the region. Overall, GCC companies dominated the lineup among the top Arab companies, with the top 10 including four entries from Saudi Arabia, three from the UAE, two from Qatar and one from Kuwait. (Gulf-Times.com) QNB Group to disclose 1H2014 results on July 08, 2014 – QNB Group (QNBK) will disclose the reviewed financial reports for the period ending June 30, 2014 on July 08, 2014. (QE) VFQS’ AGM approves 1.7% cash dividend – Vodafone Qatar’s (VFQS) AGM has approved the board of directors’ proposal for the distribution of 1.7% cash dividend (QR0.17 per share) for the financial year ended March 31, 2014. (QE) ORDS to pay interest to GMTN holders soon, launches new feature on Mozaic Go – Ooredoo (ORDS) has announced that its wholly owned subsidiary, Ooredoo International Finance Limited, will pay both the principal and interest payments to its Global Medium Term Note (GMTN) holders on July 31, 2014. Meanwhile, ORDS has announced a new streaming feature on Mozaic Go that will enable its customers to watch popular TV channels live on their personal devices, wherever they are in Qatar. (ADX, Gulf-Times.com) Kahramaa awards QR1.09bn Doha pipelines project to HLG – The Qatar General Electricity & Water Corporation (Kahramaa) has awarded a QR1.09bn contract to Habtoor Leighton Group (HLG) for the construction of pipelines for two sections of Doha’s Mega Reservoir Corridor Main 1 (Packages A & B). HLG, operating as Leighton Contracting (Qatar), is responsible for the supply, installation, testing and commissioning of 120km of iron pipes and fittings. (GulfBase.com) MDPS: Monthly salary averaged QR9,667 in 2013 in Qatar – According to the Ministry of Development Planning & Statistics (MDPS), the monthly average salary in Qatar was QR9,667 in 2013, with the average for men being QR10,075 and QR8,510 for women. Around 1.53mn people were employed, of which 192,584 were women. Those in public administration, defense and social security sectors got the highest pay package (QR24,258). The lowest monthly wages were drawn by household employees (average QR2,548), followed by construction workers (QR4,811). Education sector employees received QR19,708 and their counterparts in the fields of public health and social work were paid QR17,628. Oil & gas sector employees earned an average of QR21,965 a month, which is the second highest. Finance & insurance industry staff stood next with an average of QR20,597. People employed in the transport & communications sector were paid QR20,062 on average. The highest-paid women were in the energy sector, with their average monthly package being QR23,787. Women

- 4. Page 4 of 7 engaged in the domestic sector were the lowest-paid, with an average salary of QR2,589. (Peninsula Qatar) Msheireb Partners with VFQS for Msheireb Downtown Doha – Msheireb Properties and Vodafone Qatar (VFQS) have entered into a partnership that will see Vodafone become the primary provider of mobile services for Msheireb Downtown Doha (MDD), the world's first sustainable downtown regeneration project. As a part of this agreement, Vodafone will build and maintain all the necessary mobile sites on the premises to provide superior network coverage and data speeds to customers using the latest technology such as 4G and beyond. VFQS is also committed to supply any future technology requirements that might emerge as the construction progresses. This is all underpinned by the latest fibre network service offered in Qatar. (Zawya) BRES sells Barwa City share capital to Labregah for QR7.57bn – Barwa Real Estate Company (BRES) has announced that it has completed the sale of its entire share capital in Barwa City Real-Estate Company (Barwa City) to Labregah Real Estate Company, a wholly-owned subsidiary of Qatari Diar Real Estate Investment Company (QDREIC), on 18 June 2014. The purchase consideration was worth QR7.57bn, which will be subject to a customary price adjustment. This transaction has happened after the framework agreement between QDREIC and BRES, which had been previously announced. (QE) International Yellen gives green light for more stock gains – The US Federal Reserve Chief Janet Yellen signaled that rational exuberance is just fine. That, at least, is how some of America's money managers interpreted her comments suggesting that interest rates will remain low through 2016. Her comments reinforced their views that easy money means the US stock market rally has further to run despite already notching a series of record highs this year. That could easily put the S&P 500 benchmark on track to surpass 2,000 for the first time by the end of this year. Such a gain for 2014, after a 30% rise in 2013, would surprise those who worried that stocks might be getting overvalued and were due for a sizable pullback. One reason for increasing confidence is that the market resilience has been strong in the face of various shocks this year. A combination of factors such as an improving economy, rising earnings, and cheap borrowing costs has made that possible. (Reuters) IMF: Eurozone has correct fiscal stance to cut debt, help growth – The International Monetary Fund stated that the Eurozone's fiscal stance strikes the right balance between reducing debt and bolstering demand. In 2013, the Eurozone's overall government deficit fell to the EU limit of 3% of GDP from 6.2% in 2010 – the year when it had to bail out Greece for the first time. The €9.6tn economy is now recovering slowly and Eurozone policymakers are discussing how to balance the reduction of public debts, while at the same time stimulate growth. The IMF noted said the recovery was neither robust nor sufficiently strong, so continued support for demand was vital. The IMF praised the recent steps taken by the European Central Bank to help accelerate dangerously low inflation, but noted more might be needed if those steps fail. Meanwhile, the IMF is considering creating a new way for indebted countries to get large loans and dropping an exception to its lending rules that enabled Greece to obtain a loan in 2010, without having to first restructure its debt. IMF staff proposed that a country’s creditors instead be asked for a relatively short extension of maturities in exchange for IMF support. (Reuters, Bloomberg) Japan inflation seen falling minus tax hike in May; Kuroda says price moves improving sharply – Consumer inflation in Japan is expected to ease slightly in May 2014, excluding a sales tax hike, as gains in gasoline moderated, but prices are believed to accelerate soon as a tight labor market supports consumer spending. Demand for new workers in May is expected to remain at the strongest level in more than seven years, supporting the Bank of Japan's (BoJ) argument that the upward pressure on wages will keep the economy on track. Consumer spending is expected to decline in May, but at a slower pace than the previous month in a sign that shoppers are gradually shaking off an increase in the nationwide sales tax on April 1. May's data could also suggest that consumer prices are still on track to meet the BoJ's 2% inflation target in about a year's time. Meanwhile, the BoJ Governor Haruhiko Kuroda said the bank’s massive monetary stimulus is exerting its intended effects with the economy recovering moderately and price developments improving sharply. He also did not see any change in Japan's consumer price trend after the increase in the sales tax in April. He said the BoJ will examine all risks to the economy and prices, and will not hesitate in adjusting policy if needed to achieve its 2% inflation target. (Reuters) Li Keqiang’s Greece visit signals investment flow from China – Chinese Premier Li Keqiang said confidence in the Greek economy is returning, as China signaled its interest in investing in the Mediterranean country’s airports, railways and energy sector. Li said Greece’s Piraeus Port can become an entry point for Chinese goods in Europe. Li, who is on the second day of a three-day visit to Greece, said that China wants to see a prosperous and stable Europe. When the Greek government issues new bonds, China will continue to be a long- term investor in those bonds. Greek Prime Minister Antonis Samaras said Chinese investors have expressed interest in Athens International Airport and in the recently announced tender for the construction of a new airport at Kasteli, on the island of Crete. The two countries held talks on investments including in the country’s port connection to the rest of Europe, Greek food exports to China and the creation of mutual investment funds. (Bloomberg) Regional Mideast ICT spending to top $96bn in 2014 – The overall Information & Communication Technology (ICT) spending in the Middle East among businesses such as healthcare, banking and finance, transportation and the energy sector is predicted to top $96bn in 2014. The public cloud services market in MENA is expected to grow 21.3% to $620mn in 2014. (GulfBase.com) CCI clears HSBC Oman-DHBK deal – The Competition Commission of India (CCI) has approved the proposed transfer of HSBC Oman's banking business in India to Doha Bank (DHBK). HSBC Oman is part of HSBC Holdings which has interests in banking companies worldwide, including in India. (Bloomberg) SEC signs SR49.4bn interest-free govt loan – The Saudi Electricity Company (SEC) has signed for an interest-free loan of SR49.4bn with the Kingdom’s Ministry of Finance (MoF). The loan will be made available to the company in equal tranches over a five-year period and the terms include a grace period of 10 years before repayments begin. (GulfBase.com) BSF issues SR2bn Sukuk through private placement – Banque Saudi Fransi (BSF) has completed the issuance of its SR2bn capital-boosting Sukuk issue through private placement. This Sukuk will support the bank's capital base in accordance with Basel III requirements in order to assist further growth. The issuance has a tenor of 10 years with the bank having the right

- 5. Page 5 of 7 to call the Sukuk at the end of the fifth year. The Sukuk is priced at 140 basis points over the three-month Saudi interbank offered rate (Saibor). (Tadawul) MMG signs MoU with Saudi FAS – Mohammad Al-Mojil Group (MMG) has signed a MoU with Saudi FAS Holding Company for an entry as a strategic investor. Under the terms of the MoU, contribution by Saudi FAS will be SR327mn, which includes SR227mn as capital injection and SR100mn as a subordinated loan. After restructuring the debt, trade obligations and paid up capital, Saudi FAS will own 40% of the issued shares of MMG and the current shareholders the remaining percentage. (Tadawul) Al Khodari wins SR40.6mn Dammam contract – Abdullah A. M. Al-Khodari Sons Company (Al-Khodari) has won SR40.6mn contract from the Ministry of Municipal & Rural Affairs (Eastern Province Municipality). The contract includes the operation and maintenance of a landfill site at Dammam and neighbor cities for a period of three years. (Tadawul) Firms to build SR3.75bn pipes plant in Kingdom – Four companies from Saudi Arabia, India, Germany and Czech Republic have formed an alliance to build a large plant for manufacturing seamless pipes in Ras Alkhair. The plant is estimated to cost SR3.75bn and will be financially managed by Alinma Investment. The plant is expected to produce 600,000 tons of steel and is set for the beginning of 2015. (GulfBase.com) Eram signs deal to deliver ASME training courses – Eram Group has entered into an agreement with the American Society of Mechanical Engineers (ASME) Training & Development, to deliver ASME’s courses in the Middle East. Under the agreement, Eram will serve as an authorized training provider to deliver ASME’s more than 300 courses to the region. The training courses are specifically developed to boost technical competence and heighten managerial experience for engineers and technical professionals. (GulfBase.com) TRA releases ICT in UAE; Business Survey 2013 report – The Telecommunication Regulatory Authority of the UAE (TRA) released its ‘ICT in UAE; Business Survey – 2013’. A total of 1,502 businesses across the UAE participated in this research, which was limited to businesses with 10 or more employees. The survey spanned multiple services including fixed telephony, mobile telephony, internet, advanced telecommunication services and e-commerce. Across these services, the survey examined the access and the use of ICT by businesses in the UAE. (GulfBase.com) CNTAC: UAE controls 5.5% of global textile market – According to China National Textile & Apparel Council (CNTAC), the UAE controls 5.5% of the global textile market. Gulf countries are emerging as leading textile manufacturing and trading centers globally. By 2016, the UAE is expected to become the world’s leading high-end textile and garment re- export centre. (GulfBase.com) DEL records 20% reduction in flaring – Dolphin Energy (DEL) has recorded a 20% reduction in flaring and at the same time exceeded the Ministry of Environment’s flaring target of 0.3% in gas export. DEL’s General Manager Adel Ahmed Albuainain said that the achievement is among the highlights included in its fifth sustainability report entitled “Powered by Performance,” which showcases the company’s commitment to the economy, environment, and society. Notable achievements in the company’s performance in 2013 include: successfully securing gas without interruption in supply to customers and recording 99.997% plant availability; reaching 1bn barrels of oil equivalent of cumulative gross production; and achieving 23mn man hours without a lost time incident (LTI), in addition to a 12% rise in community investment expenditure in Qatar. (Gulf-Times.com) Compareit4me.com completes $3mn funding round – UAE- based finance comparison site, Compareit4me.com has completed $3mn first round of funding. The investment was led by Mulverhill Associates, a Dubai-based investment & advisory firm focused on the Middle East. (Bloomberg) Former CEO of Arabtec to hold on to stake – The former Chief Executive of Arabtec, who abruptly resigned from the company this week, said that he has no plans to sell his 28.85% stake. In late May, Arabtec said Ismaik had raised his stake to 21.46% from 8.03%, while this week, bourse data showed his stake had risen further to 28.85%. Forbes magazine said that Ismaik, 37, had become the first Jordanian billionaire — and the third-youngest billionaire in the Middle East — because of his holdings of Arabtec shares. (Peninsula Qatar) DEC, StanChart sign MoU – The Dubai Economic Council (DEC) and Standard Chartered Bank (StanChart) have signed a MoU stipulating that StanChart will advise, arrange and facilitate trade & investment flows between the public and private sectors based in Dubai, UAE and the US. (GulfBase.com) DFFS, DREC in deal to prepare for World Expo 2020 – The Dubai Fund for Financial Support (DFFS) has reached a strategic deal with the Dubai Real Estate Corporation (DREC) to develop the fund’s plots to support the economic growth of the Emirate ahead of the World Expo 2020. As per the agreement, the first project will be set up along the Sheikh Zayed Road, which includes the construction of a modern mall center and residential complexes. DREC will develop a number of hotel projects, residential units and hotel apartments. The long-term strategic partnership between the two parties involves other agreements to develop plots of the fund. (GulfBase.com) DSC: Dubai’s economy up 4.6% to AED325.7bn – According to the data from the Dubai Statistics Centre (DSC), Dubai’s economy expanded by 4.6% in 2013, its fastest rate of growth since 2007, driven by a solid performance spanning across manufacturing to hospitality. The economy grew to AED325.7bn in 2013, up from AED 311bn in 2012. (GulfBase.com) Deutsche Post to boost Mideast investments – Germany- based Deutsche Post’s DHL Express parcel delivery subsidiary is planning to invest AED100mn to expand its ground operations in Dubai, along with additional investments at the Dubai International Airport (DIA), in Abu Dhabi, in Saudi Arabia and in Cairo, for a total sum of about $341mn. (Bloomberg) Abraaj close to acquire CMC; plans stake acquisition in CIRA – Abraaj Group is about to complete a take-over of the healthcare company, Cairo Medical Center (CMC). Earlier, Creed Healthcare, a company owned by one of its funds had agreed to buy 41.98% of CMC for a purchase consideration of 75 Egyptian pounds per share valuing the business at AED104mn. The offer is conditional to 51% of the total outstanding shares being tendered, out of which Abraaj has already obtained irrevocable sale undertakings from the shareholders owning 50.09% of CMC. Additionally, Abraaj is also planning to submit a tender offer to acquire a stake in an education group, Cairo Investment and Real Estate Development (CIRA). Both the target entities are listed on Egyptian Stock Exchange. (GulfBase.com) Dana Gas gets approval for AED29.55mn capital increase – Dana Gas has received the approval from the competent authorities for the capital increase of AED29.55mn. The capital increase is arising out of the conversion of voluntary conversion

- 6. Page 6 of 7 notices received between May 1 and May 15, 2014 amounting to $6.03mn of convertible Sukuk. (ADX) DED to observe investment projects – Abu Dhabi’s Department of Economic Development (DED) has signed a joint cooperation agreement with industrial arm Senaat, in addition to 60 government institutions and semi-governmental bodies of departments, agencies and organizations, with the aim of cooperation and coordination between the two parties on the Abu Dhabi Projects Program (ADPP). ADPP aims at highlighting the size of domestic and foreign investment in each sector separately, as well as supporting decision makers to the analysis of development in every sector, in addition to the identification of all existing delayed and postponed projects and facilitate the access of investors to the investment data in the appropriate sector. (GulfBase.com) Etihad Airways denies talks with Malaysian Airlines over equity stake – Abu Dhabi's Etihad Airways said that it is not in talks with Malaysian Airlines for an equity investment, dismissing media reports. (Reuters) Al Madina appoints CEO – Al Madina for Finance & Investment Company has appointed Mohammed Saud Sulaiman Al Abdullah as Chief Executive Officer (CEO) effective from June 17, 2014. (DFM) Fitch affirms Kuwait at 'AA'; outlook stable – Fitch Ratings has affirmed Kuwait's Long-term foreign and local currency Issuer Default Ratings (IDR) at 'AA'. The Outlooks are Stable. The Country Ceiling has been affirmed at 'AA+' and the Short- term foreign currency IDR at 'F1+'. (Reuters) IHP approves KISR’s proposal to become UNESCO regional center – International Hydrological Programme (IHP) has approved a proposal by Kuwait Institute for Scientific Research's (KISR) to affiliate its hydrology department with UNESCO. The IHP is the only intergovernmental programme of the UN system devoted to water research, water resources management, education and capacity building. (Bloomberg) ACWA Power Barka’s BoD approves OMR3mn cash dividend – ACWA Power Barka’s board of directors has approved the distribution of 20% cash dividend amounting to OMR3mn for the period January 1 – April 30, 2014. (MSM) Al Batinah Power’s BoD approves 1.5% interim cash dividend – Al Batinah Power Company’s board of directors has approved the distribution of 1.5% interim cash dividend (1.5 baiza per share) for the period ended December 31, 2013. (MSM) Al Suwadi Power’s BoD approves 1.5% interim cash dividend – Al Suwadi Power Company’s board of directors has approved the distribution of 1.5% interim cash dividend (1.5 baiza per share) for the period ended December 31, 2013. (MSM) $6bn Duqm refinery development to kick off soon – The process of pre-qualifying international companies for the multibillion dollar engineering, procurement & construction (EPC) package of the Duqm Refinery project in Oman is expected to be kicked off in 3Q2014. Duqm Refinery and Petrochemical Industries Company, a JV of Oman Oil Company (50%) and International Petroleum Investment Company (50%), a wholly owned commercial entity of the government of Abu Dhabi, is jointly developing the refinery project with an investment of around $6bn. Plans for an associated petrochemical complex in the second phase could add a further $9bn to the total project cost. (GulfBase.com) Orpic invites bid for $3.6bn LPP EPC – Oman Oil Refineries and Petroleum Industries Company (Orpic) has launched the process of prequalifying contractors for the construction phase of its $3.6bn Liwa Plastics Project (LPP). The company has issued ‘Request for Information’ engineering contractors inviting them to affirm their interest in bidding for the multibillion dollar engineering, procurement and construction (EPC) package of the huge petrochemicals project. The LPP is proposed to be established adjacent to the ongoing Sohar Refinery Improvement Project (SRIP) under way at the industrial port of Sohar. (Bloomberg) Investcorp issues bonds – Investcorp has issued 125mn Swiss Franc of 4.75% bonds due 2019. The bonds are listed on the SIX Swiss Exchange and they are guaranteed by Investcorp’s parent Investcorp Bank. (Bahrain Bourse) Fitch affirms Bahrain at 'BBB'; outlook stable – Fitch Ratings has affirmed Bahrain's Long-term foreign currency Issuer Default Rating (IDR) at 'BBB' and local currency IDR at 'BBB+'. The Outlooks are Stable. The issue ratings on Bahrain's senior unsecured foreign and local currency bonds have also been affirmed at 'BBB' and 'BBB+', respectively. Fitch has simultaneously affirmed Bahrain's Country Ceiling at 'BBB+' and Short-term foreign currency IDR at 'F3'. (Bloomberg) Gulf Air launches additional flights to LIA and IAA – Gulf Air has launched additional flights additional flights to Istanbul Ataturk Airport (IAA) and Larnaca International Airport (LIA) to reach seven weekly flights to both cities. The flights will be operated by an Airbus A320-ER aircraft in a two-class configuration, featuring 14 Falcon Gold Class seats and 96 Economy Class seats. (Bloomberg) Bahrain plans major solar power plant – Bahrainis planning to set up a key solar and wind hybrid plant which will be linked to the country's power-distribution grid by the first quarter of 2015. The 5 megawatt experimental station is expected to be built on a land covering 120,000 square meter south of Al Dur Power and Water Plant Company. It is part of Bahrain's efforts to develop renewable energy sources. (Bloomberg)

- 7. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jul-10 Jul-11 Jul-12 Jul-13 QE Index S&P Pan Arab S&P GCC 0.1% (1.1%) (0.4%) (0.3%) 0.1% 0.5% 1.6% (1.6%) (0.8%) 0.0% 0.8% 1.6% 2.4% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,314.85 (0.4) 3.0 9.1 DJ Industrial 16,947.08 0.2 1.0 2.2 Silver/Ounce 20.88 0.3 6.0 7.2 S&P 500 1,962.87 0.2 1.4 6.2 Crude Oil (Brent)/Barrel (FM Future) 114.81 (0.2) 1.2 3.6 NASDAQ 100 4,368.04 0.2 1.3 4.6 Natural Gas (Henry Hub)/MMBtu 4.51 (2.9) (3.3) 3.9 STOXX 600 348.09 (0.0) 0.3 6.0 LPG Propane (Arab Gulf)/Ton 108.75 0.2 4.9 (13.9) DAX 9,987.24 (0.2) 0.8 4.6 LPG Butane (Arab Gulf)/Ton 125.75 (0.2) 5.3 (7.9) FTSE 100 6,825.20 0.3 0.7 1.1 Euro 1.36 (0.1) 0.4 (1.0) CAC 40 4,541.34 (0.5) (0.0) 5.7 Yen 102.07 0.1 0.0 (3.1) Nikkei 15,349.42 (0.1) 1.7 (5.8) GBP 1.70 (0.2) 0.3 2.8 MSCI EM 1,043.86 (0.6) (0.5) 4.1 CHF 1.12 (0.1) 0.6 (0.2) SHANGHAI SE Composite 2,026.67 0.1 (2.1) (4.2) AUD 0.94 (0.1) (0.1) 5.3 HANG SENG 23,194.06 0.1 (0.5) (0.5) USD Index 80.37 0.1 (0.3) 0.4 BSE SENSEX 25,105.51 (0.4) (0.5) 18.6 RUB 34.47 0.3 0.2 4.9 Bovespa 54,638.19 (1.0) (0.3) 6.1 BRL 0.45 0.1 (0.3) 5.9 RTS 1,358.73 (0.9) (1.2) (5.8) 179.0 150.5 136.6