Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a 27 February Daily market report

Similar a 27 February Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

27 February Daily market report

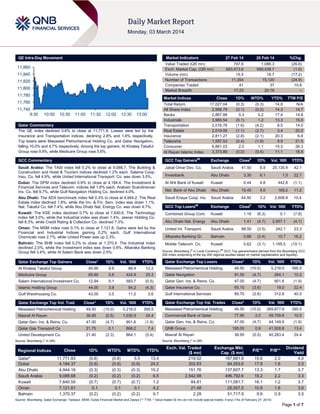

- 1. QE Intra-Day Movement Market Indicators 11,860 11,840 11,820 11,800 11,780 26 Feb 14 %Chg. 797.6 683,473.6 15.5 11,354 41 17:23 1,086.3 690,438.7 18.7 15,120 37 20:16 (26.6) (1.0) (17.2) (24.9) 10.8 – Market Indices 11,760 11,740 9:30 27 Feb 14 Value Traded (QR mn) Exch. Market Cap. (QR mn) Volume (mn) Number of Transactions Companies Traded Market Breadth 10:00 10:30 11:00 11:30 12:00 12:30 13:00 Qatar Commentary The QE index declined 0.6% to close at 11,771.8. Losses were led by the Insurance and Transportation indices, declining 2.8% and 1.6% respectively. Top losers were Mesaieed Petrochemical Holding Co. and Qatar Navigation, falling 10.0% and 4.7% respectively. Among the top gainers, Al Khaleej Takaful Group rose 9.9%, while Medicare Group rose 5.6%. Close Total Return All Share Index Banks Industrials Transportation Real Estate Insurance Telecoms Consumer Al Rayan Islamic Index 1D% WTD% YTD% TTM P/E 17,027.04 2,956.79 2,867.88 3,965.54 2,016.78 2,019.09 2,811.27 1,597.53 6,861.03 3,373.89 (0.3) (0.1) 0.3 (0.1) (1.6) (1.1) (2.8) (0.4) 2.0 (0.0) (0.3) (0.2) 0.2 1.2 (4.2) (2.7) (2.1) (1.9) 1.1 (0.4) 14.8 14.3 17.4 13.3 8.5 3.4 20.3 9.9 15.3 11.1 N/A 14.7 14.8 15.0 14.0 20.0 6.8 21.5 26.3 18.8 GCC Commentary GCC Top Gainers## Exchange Saudi Arabia: The TASI index fell 0.2% to close at 9,088.7. The Building & Construction and Hotel & Tourism indices declined 1.2% each. Salama Coop. Insu. Co. fell 4.9%, while United International Transport. Co. was down 3.5%. Jabal Omar Dev. Co. Saudi Arabia Investbank Abu Dhabi Dubai: The DFM index declined 0.9% to close at 4,184.4. The Investment & Financial Services and Telecom. indices fell 1.8% each. Arabian Scandinavian Ins. Co. fell 9.7%, while Gulf Navigation Holding Co. declined 4.0%. Al Ahli Bank of Kuwait Kuwait Nat. Bank of Abu Dhabi Abu Dhabi Abu Dhabi: The ADX benchmark index fell 0.3% to close at 4,944.2. The Real Estate index declined 1.8%, while the Inv. & Fin. Serv. index was down 1.1%. Nat. Takaful Co. fell 7.4%, while Abu Dhabi Nat. Energy Co. was down 4.7%. Saudi Enaya Coop. Ins. Saudi Arabia 44.50 GCC Top Losers Exchange Kuwait: The KSE index declined 0.7% to close at 7,640.6. The Technology index fell 3.0%, while the Industrial index was down 1.4%. Jeeran Holding Co. fell 8.3%, while Credit Rating & Collection Co. declined 7.3%. Combined Group Cont. Kuwait 1.18 (6.3) 0.1 (7.8) Abu Dhabi Nat. Energy Abu Dhabi 1.41 (4.7) 2,957.1 (4.1) Oman: The MSM index rose 0.1% to close at 7,121.6. Gains were led by the Financial and Industrial Indices gaining 0.2% each. Gulf International Chemicals rose 2.7%, while United Power was up 2.3%. United Int. Transport. Saudi Arabia 88.50 (3.5) 242.1 23.3 Albaraka Banking Gr. Bahrain 0.86 (3.4) 10.7 16.2 Mobile Telecom. Co. Kuwait 0.62 (3.1) 1,165.5 (10.1) Bahrain: The BHB index fell 0.2% to close at 1,370.4. The Industrial index declined 2.0%, while the Investment index was down 0.6%. Albaraka Banking Group fell 3.4%, while Al Salam Bank was down 2.5%. ## Close# 1D% 41.50 8.9 25,135.4 42.1 3.30 6.1 1.5 22.7 0.44 4.8 442.8 (1.1) 15.45 4.0 169.2 11.2 3.2 2,608.9 10.4 # Close Vol. ‘000 1D% Vol. ‘000 YTD% YTD% Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Al Khaleej Takaful Group Close* 1D% Vol. ‘000 YTD% Close* 1D% Vol. ‘000 YTD% 40.95 Qatar Exchange Top Gainers 9.9 88.4 12.2 Mesaieed Petrochemical Holding 49.50 (10.0) 5,218.0 395.5 91.50 (4.7) 264.1 10.2 Qatar Exchange Top Losers Medicare Group 65.80 5.6 424.9 25.3 Qatar Navigation Salam International Investment Co. 12.94 5.1 583.7 (0.5) Qatar Gen. Ins. & Reins. Co. 47.00 (4.7) 901.6 (1.9) Islamic Holding Group 44.00 3.9 94.2 (4.3) Qatar Insurance Co. 65.10 (3.6) 19.0 22.4 Gulf Warehousing Co. 43.00 3.5 11.2 3.6 Gulf International Services 85.70 (2.6) 312.8 40.5 Close* 1D% Val. ‘000 YTD% Mesaieed Petrochemical Holding 49.50 (10.0) 269,877.6 395.5 24.4 Commercial Bank of Qatar 77.90 2.0 49,709.9 10.0 (1.9) Qatar Gen. Ins. & Reins. Co. 47.00 (4.7) 44,149.9 (1.9) 195.00 0.9 41,928.8 13.4 38.95 (0.5) 40,283.4 24.4 Qatar Exchange Top Vol. Trad. Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochemical Holding 49.50 (10.0) 5,218.0 395.5 Masraf Al Rayan 38.95 (0.5) 1,030.9 Qatar Gen. Ins. & Reins. Co. 47.00 (4.7) 901.6 Qatar Gas Transport Co 21.75 0.1 868.2 7.4 United Development Co. 21.40 (2.3) 864.1 (5.4) Qatar* Dubai Abu Dhabi Saudi Arabia Kuwait Oman Bahrain QNB Group Masraf Al Rayan Source: Bloomberg (* in QR) Source: Bloomberg (* in QR) Regional Indices Qatar Exchange Top Val. Trades Close 1D% WTD% MTD% YTD% 11,771.83 4,184.37 4,944.16 9,088.68 7,640.55 7,121.61 1,370.37 (0.6) (0.9) (0.3) (0.2) (0.7) 0.1 (0.2) (0.8) (0.9) (0.3) (0.2) (0.7) 0.1 (0.2) 5.5 (0.9) (0.3) (0.2) (0.7) 0.1 (0.2) 13.4 24.2 15.2 6.5 1.2 4.2 9.7 Exch. Val. Traded ($ mn) 219.02 302.83 151.76 2,542.98 84.81 21.48 2.28 Exchange Mkt. Cap. ($ mn) 187,681.9 84,553.6 137,607.7 496,792.6 111,581.7 25,557.5 51,717.9 P/E** P/B** 15.6 17.9 13.3 18.2 16.1 10.9 9.6 2.0 1.6 1.7 2.2 1.2 1.6 0.9 Dividend Yield 4.0 2.0 3.7 3.3 3.7 3.6 3.5 Source: Bloomberg, Qatar Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) (*As of February 27, 2014) Page 1 of 7

- 2. Qatar Market Commentary The QE index declined 0.6% to close at 11,771.8. The Insurance and Transportation indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Mesaieed Petrochemical Holding Co. and Qatar Navigation were the top losers, falling 10.0% and 4.7% respectively. Among the top gainers, Al Khaleej Takaful Group rose 9.9%, while Medicare Group rose 5.6%. Overall Activity Buy %* Sell %* Net (QR) Qatari 67.92% 72.04% (32,838,647.15) Non-Qatari 32.08% 27.97% 32,838,647.15 Source: Qatar Exchange (* as a % of traded value) Volume of shares traded on Thursday fell by 17.2% to 15.5mn from 18.7mn on Wednesday. However, as compared to the 30day moving average of 12.8mn, volume for the day was 20.3% higher. Mesaieed Petrochemical Holding Co. and Medicare Group were the most active stocks, contributing 33.8% and 6.7% to the total volume respectively. Earnings Earnings Releases Company National Takaful Co. (Watania)* Union Cement Co. (UCC)* Sharjah Cement and Industrial Development Co. (SCIDC)* Equate Petrochemical Co.* The Kuwait Styrene Co. (TKSC)* Muscat National Holding Co. (MNH)* Ubar Hotels & Resorts* A’Sharqiya Investment Holding Co.* Revenue (mn) 4Q2013 % Change YoY Operating Profit (mn) 4Q2013 % Change YoY Net Profit (mn) 4Q2013 % Change YoY AED 37.4 220.4% – – -2.4 NA Abu Dhabi AED 528.1 -12.3% – – 40.8 -16.0% Abu Dhabi AED 624.6 1.6% – – 49.1 102.8% Kuwait USD 0.0 NA – – 1250.0 14.7% Kuwait USD 915.0 37.2% – – 180.0 NA Oman OMR 0.0 NA – – 0.5 NA Oman OMR 6.3 73.4% 1.9 125.7% 1.4 117.9% Oman OMR 0.0 NA – – 0.5 87.2% Market Currency Abu Dhabi Source: Company data, DFM, ADX, MSM (*FY2013 results) News Qatar MCCS net profit rises by 11.4% to QR446.1mn in 2013 – Mannai Corporation Group (MCCS) earned a net profit of QR446.1mn in 2013, up 11.4% from QR400.3mn posted in 2012. Moreover the company’s revenue surged by 17.5% to reach QR5.6bn vs. QR4.8bn in 2012. Mannai said its acquisition in 2012 of a 66% stake in Damas was a defining moment in the company’s history. The company increased its stake in Damas International by an additional 15% by acquiring the remaining shareholding of the founder shareholders, thereby increasing Mannai’s shareholding to 81%. MCCS’s board of directors has recommended a 55% cash dividend to its shareholders, which work out to QR5.50 a share. MCCS’ AGM will be held on March 23, 2014 at the Grand Hyatt Hotel Doha, where the recommendation will be submitted for approval. (QE, GulfTimes.com) Ooredoo gets 5-star rating for excellence – Ooredoo has been awarded five-star recognition by the EFQM (the European Foundation for Quality Management) for its ongoing high performance standards. Ooredoo earned the ―recognized for excellence — 5 Star (R4E-5*)‖ award after a week-long assessment by a team of specially-trained and licensed assessors. The recognition strengthens Ooredoo’s reputation for high operational standards, which has been built over the years, since the company’s first recognition for excellence certification in 2009. Ooredoo is the only telecommunications company in the Middle East to be awarded a five-star accreditation rating for overall organizational excellence based Excellence Model. (Gulf-Times.com) on the EFQM Siemens bags QR920mn Kahramaa expansion deal – Siemens has bagged a contract worth QR920mn from the Qatar General Electricity and Water Corp (Kahramaa) that will strengthen Qatar’s power supply system. The contract includes the construction of 9 turnkey substations for the Phase 11 of Kahramaa’s power transmission system expansion project. Under this contract, Siemens will provide gas-insulated switchgears (GIS), with voltages including 220kV, 132kV and 66kV, for the first stage of the Phase 11 expansion. Siemens is scheduled to complete the project within 26 months from the award date. (Gulf-Times.com) New Port Project set for early completion – According to a top official, quick progress is being made in the construction of the New Port Project (NPP) and more than 35% of the work has been completed as of now. The project consists of the new port, a naval base for the Emiri Naval Force and Qatar Economic Zone 3. Situated 24 kilometers south of Doha, the entire cost for the project is estimated at QR27bn. With an area of 26.5 square kilometer, a major part of the project is reclaimed land. (GulfTimes.com) QTA to focus on new infrastructure – Qatar Tourism Authority (QTA) Chairman Issa bin Mohammed Al Mohannadi said that as part of the endeavor to develop a vibrant and sustainable tourism industry, QTA will make huge investments on infrastructure development, including building new hotels and Page 2 of 7

- 3. resorts, public parks and monuments. Under the recently launched National Tourism Sector Strategy 2030, Qatar will make investments of up to QR163.8bn over the next 16 years to transform the energy-rich country into a new tourist hub in the region. Al Mohannadi said investment will be divided into three streams, and one is product development, which means building hotels, resorts, public parks and monuments. (Peninsula Qatar) QE suspends trading in DHBK, MARK, QIMD shares on March 3 – The Qatar Exchange (QE) has suspended trading in the shares of three companies on March 3, 2014 due to their AGMs and EGMs being held on that day. The three companies are: Doha Bank (DHBK), Masraf Al Rayan (MARK) and Qatar Industrial Manufacturing Company (QIMD). (QE) QA launches more UAE flights – Qatar Airways (QA) has launched two new regional routes to Sharjah and Dubai World Central’s Al Maktoum International Airport. The new routes will be operated daily on Airbus A320 aircraft from the airline’s hub in Doha and add to the existing QA network of flights to Dubai and Abu Dhabi, doubling the number of destinations in the UAE from two to four. There will be three flights daily to Sharjah, with two flights per day to DWC. (GulfBase.com) ERES postpones its board meeting to March 6 – Ezdan Holding Group (ERES) has postponed its board meeting. The meeting is scheduled to take place on March 6, 2014 instead of March 3, 2014. (QE) MPHC’s BoD to meet on March 16 – Mesaieed Petrochemical Holding Company’s (MPHC) board of directors will meet on March 16, 2014 to discuss the company’s financial results for the year ended December 31, 2013. (QE) AHCS’ AGM to be held on April 6 – Aamal Company (AHCS) announced that its AGM will be held on April 6, 2014 at Al Areen Hall, Renaissance Hotel, City Center Doha. In case of lack of quorum, the second meeting will be held on April 9, 2014 at the same place. The AGM’s agenda includes discussing the board of directors’ proposal to carry forward the net profits generated for the year 2013 to the year 2014, among others. (QE) International QNB: Ageing population impacts economic performance, fiscal policy – When comparing the growth rates of advanced economies, many commentators often forget that Europe and Japan have a larger percentage of their population above the age of 60. Such aging population has a direct impact on economic performance, fiscal policy and asset allocation. It is also a critical indicator for long-term financial sector developments. According to a recent UN study, between 2010 and 2050 about 1.25bn people will be added to the global population aged 60+, while the number of people under 25 is projected to hold steady at 3bn. This implies that an increasingly smaller share of the population will be working, the so-called support ratio, while older people will depend on public transfers, their children or their own assets to sustain their old-age consumption. The biggest policy challenge of declining support ratios is how to pay for old-age consumption. In countries with well-developed pension and social safety nets, governments are increasingly seeing a larger proportion of their expenditures devoted to pension benefits for older people. Since 1990, public pension spending has increased by 1.25% of GDP in advanced economies. Without an increase in the retirement age or a reduction in pension benefits, such trends could jeopardize public finances and lead to unsustainable public debt burdens. Taxing the young to pay for the old also has its limits. As in the case of Greece and Italy, excessive taxation leads the young to emigrate, thus further exacerbating the declining support ratio. An alternative is to facilitate immigration, like in the United States, so as to increase the share of the working population. (QNB Group) Obama's dilemma: boosting domestic initiatives without adding to deficit – President Barack Obama will unveil a budget this week that seeks to boost spending on new initiatives such as road repairs, education programs and tax breaks for the working poor while avoiding an increase in U.S. deficits. Obama has made reducing the gap between the rich and the poor a centerpiece of his agenda for his next three years in office. But he is limited in his ability to offer bold new initiatives because of a budget accord he reached in 2011 with House of Representatives Republicans that puts strict curbs on both domestic and military spending. An agreement reached in December between congressional Republicans and Obama's Democrats allowed a slight easing of curbs on spending in the current 2014 fiscal year, but outlays will be essentially flat in fiscal 2015, which begins October 1. Because of the caps, spending on programs subject to annual review in 2015 will total $1.014tn compared to $1.012tn - an increase of less than twotenths of a percent. Obama's budget and the coming debate in Congress will focus on how to work within those limits. (Reuters) US GDP revised down, but hints of economic thaw emerge – The US government slashed its estimate for fourth-quarter economic growth in the latest sign of a loss of momentum, but some tentative signs emerged that suggested the worst of the slowdown may be over. The Commerce Department said, GDP expanded at a 2.4% annual rate, down sharply from the 3.2% pace it reported last month and the 4.1% logged in the third quarter. The economy has faced a number of headwinds, including a 16-day shutdown of the government in October and an unusually cold winter that has weighed on activity since late December. Growth has also been dampened by the expiration of long-term unemployment benefits, cuts to food stamps and businesses placing fewer orders with manufacturers as they work through a pile of unsold goods in their warehouses. (Reuters) China HSBC manufacturing PMI hits seven-month low in February – China's factory activity shrank again in February as output and new orders fell, a private survey found on Monday, reinforcing concerns of a slowdown in the world's second largest economy. The final Markit/HSBC manufacturing Purchasing Managers' Index (PMI) fell to a seven-month low of 48.5 in February, the third straight monthly decline, from January's 49.5. The figure was in line with the 48.3 reported in the preliminary version of the PMI released on Feb 20. (Reuters) Downward 4Q GDP revision seen after modest Japan capex growth – Japanese companies raised spending on plant and equipment in October-December for a second straight quarter, but rather modestly, suggesting firms were wary of boosting investment in the face of an uncertain economic outlook. Ministry of Finance (MOF) data showed 4.0% YoY rise in capital spending followed a 1.5% increase in the previous quarter, which was the first increase in four quarters. Compared with the previous quarter, however, capital spending excluding software declined 0.3% on a seasonally adjusted basis, down for a second straight quarter. The data suggests Japan's 4Q growth is likely to be revised down slightly from an initial estimate, as this data will be used to calculate revised gross domestic product (GDP) figures due on March 10. (Reuters) Eurozone inflation stabilizes in 'danger zone' – Eurozone inflation stabilized in the European Central Bank's (ECB) "danger zone" in February but did not fall as expected, making it less likely the ECB will loosen monetary policy further at its Page 3 of 7

- 4. monthly meeting next week. European Union statistics office Eurostat estimated on Friday that consumer prices in the 18 countries sharing the Euro rose an annual 0.8% this month. That was the same rate as in January and December, after readings of 0.9% in November and 0.7% in October. Economists polled by Reuters had forecast inflation would slow to 0.7%. Fears the bloc may be at risk of deflation as it struggles to recover from its debt crisis have raised expectations the ECB will use interest rates or other policy tools to give the economy further support. (Reuters) SABIC and K.A.CARE sign R&D deal – Saudi Basic Industries Corporation (SABIC) and the King Abdullah City for Atomic & Renewable Energy (K.A.CARE) have signed a research & development agreement to explore areas of cooperation in joint technology development for creating new intellectual property in Saudi Arabia. Under the agreement, SABIC and K.A.CARE will develop a range of protocols for evaluation and feasibility of renewable energies including, solar, wind, and municipal waste with specific attention given to electricity or steam generation for industrial usage, and energy storage. (GulfBase.com) Regional Saudi tourism investments to hit SR33.5bn by 2020 – According to the experts, the Kingdom of Saudi Arabia will now see a steady growth in its travel and tourism industry with almost SR33.5bn to be invested in the sector until 2020. Data from the World Trade and Tourism Council show travel and tourism investments in Saudi Arabia have grown at a CAGR of 5.8% since 2001 and are estimated to have reached SR20.55bn at year-end 2012. It is expected to increase at an annual rate of 6.7% to reach SR33.5bn of total investments in 2020. (GulfBase.com) Saudi Arabia's Public Investment Fund plans to sell 15% stake in NCB – National Commercial Bank (NCB) Chairman Mansoor Al Maiman said Saudi Arabia's Public Investment Fund is planning to sell its 15% stake in NCB through an IPO. Finance Minister Ibrahim Al-Assaf said the state-run investment fund, which owns 69.3% stake in the Jeddah-based bank, will seek approval for the IPO from the market regulator in 3Q2014. He further added that the fund plans to allocate an additional 10% stake to the Public Pension Agency. The sale process will mark Saudi Arabia's first bank IPO since 2008 and will probably be the region's biggest IPO as NCB has SR377.3bn in assets. The bank reported a profit of SR7.9bn last year. (Bloomberg) STC selects Cisco’s network solutions; signs deal with SAP to optimize network operations – The Saudi Telecom Company (STC) announced that it has chosen Cisco Advanced Solutions to become the first service company in the MENA region to select Cisco’s fundamental convergent system. The system is a part of new networks that are specifically designed to be the basis for a smarter, wider and more adapting internet. It will be connected to the new reinforced generation of the advanced programmable network. The system also facilitates reinforced demand delivery and increases STC network service delivery. Meanwhile, STC has signed an agreement with SAP to implement its solutions for network life-cycle management to improve network operations. SAP’s solutions will offer visibility into STC’s equipment and assets, including multifaceted historical details at every step of the lifecycle, while maintaining the high quality of STC’s IT infrastructure. These solutions reduce and optimize costs related to build and repair, as well as helping increase the productivity of field workers. (GulfBase.com) Mobily signs $280mn credit deal with NSN – Etihad Etisalat Company (Mobily) has signed a $280mn credit deal with NSN to source 3G, 4G networks at the Mobile World Congress. The export credit facilitated by NSN will enable Mobily to accelerate expansion and modernization of its 4G LTE, 3G and 2G networks during 2014–2016. The investment is primarily aimed at improving Mobily’s customer experience and addressing demand for high speed data services. (GulfBase.com) Saudi CMA approves SPIMACO’s capital increase – The Saudi CMA’s board has approved the Saudi Pharmaceutical Industry & Medical Appliances Corporation’s (SPIMACO) request to increase its capital from SR784.375mn to SR1,200mn by issuing 9 bonus shares for every 17 existing shares. This increase will be paid by transferring an amount of SR395.6mn from retained earnings account and SR20mn from the contractual reserve account to the company’s capital. Consequently, the company's outstanding shares will increase from 78,437,500 to 120,000,000 shares. The bonus shares eligibility is limited to those shareholders who are registered at the close of trading on the day of the extraordinary general assembly, which will be determined later. (Tadawul) RCJY signs contracts for SR260mn projects – The Royal Commission for Jubail and Yanbu’s (RCJY) Chairman, Prince Saud bin Abdullah Al-Thunayan, has signed three contracts for the construction and maintenance of a series of educational and engineering projects worth SR260mn in the two industrial cities. The first contract included the construction of four schools (boys and girls) in Jubail Industrial City (JIC) together with the associated facilities such as car parking, water and sanitary networks, air-conditioning and heating, fire-fighting system, TV cable services, CCTV, and sports facilities. Works will run for three years. The second contract will provide engineering services to the industrial and housing areas (phase II) in Yanbu Industrial City (YIC) in addition to other services related to soil control and telecommunications system. The third contract covers operation and maintenance services to public utility facilities in YIC and runs for five years. (GulfBase.com) Saudi Aramco awards contract Metso to supply valve solutions – Saudi Arabian Oil Company (Saudi Aramco) has awarded a large order to Finland’s Metso Oyj for its petroleum refining and petrochemical production complex currently under construction. The order includes a considerable number and wide range of Metso's Neles rotary and globe valves and Jamesbury valves, including control, on-off and safety valves. It also includes Metso's intelligent safety solenoid technology and valve controllers. The expansion of the current facilities is part of Saudi Aramco's plan to diversify its business from crude oil into chemicals, unconventional gas and renewables. (GulfBase.com) IT, telecom share of Saudi’s GDP rises to 2.75% – According to a report released by Saudi Arabian Monetary Agency (SAMA), the share of IT and telecommunications sector to the gross domestic product (GDP) increased to 2.75% while its share to nonoil GDP grew to 7.0% in 2012. Revenues of the telecom firms operating in the Kingdom stood at SR71bn by the end of 2012, at an annual average growth rate of 12% in the last 10 years (2003-2012). Revenues of mobile telecom services represented 78% of the total revenues. Overseas investments of the Saudi telecom companies jumped from SR455mn in 2007 to SR18.7bn by the end of 2012 thus bringing the total revenues of the company’s inland and overseas operations to nearly SR90bn. (GulfBase.com) ADC to sell textile factory in Al-Ahsa Industrial City – AlAhsa Development Company (ADC) announced that, due to the accumulated losses of SR142mn, its board has decided to sell the whole textile factory in Al-Ahsa Industrial City, which has Page 4 of 7

- 5. stopped production since 2007. The factory is built on total area of 43,200 square meters and includes all textile machineries, utilities equipment. (Tadawul) UAE-led group to buy Indian power plants for $1.6bn – A consortium led by Abu Dhabi National Energy Company (TAQA) has agreed to buy two Indian hydroelectric power plants from Jaiprakash Power Ventures in a deal worth about $1.6bn. The group will spend $616mn on equity in the plants, and in addition take over their non-recourse project debt, bringing the total enterprise value to around $1.6bn. State-run TAQA, with 51% stake in the consortium, will control the operations and management of both plants. PSP Investments, one of Canada’s largest institutional investors, will own 39% and an infrastructure fund run by India’s IDFC Alternatives will hold 10%. (Peninsula Qatar) UAE, Japan sign deal to boost crude storage – Japan has signed an agreement to boost the UAE’s crude storage capacity in the Asian nation to 6.29mn barrels, up from the current 4.4mn barrels. The deal will allow the UAE easy access to Asian markets, while giving Japan priority access to reserves in case of emergencies. In return for providing free storage space, Japan gets a priority claim on the stockpiles in case of emergency. According to Japan External Trade Organisation, the trade volume between the two countries rose to AED194.5bn ($52.9bn) in 2012, up by 6%. (GulfBase.com) IDB lists $1bn sukuk in Dubai – The Islamic Development Bank (IDB) has announced the listing of its $1bn sukuk on Nasdaq Dubai. The listing is the result of joint efforts between the Ministry of Finance, Supreme Committee of the Islamic Economy Initiative, Nasdaq Dubai and the IDB. The listing falls in line with the IDB’s Medium Term Note Programme, which recently increased from $6.5bn to reach $10bn. (GulfBase.com) NCC’s BoD proposes 25% cash dividend – National Cement Company’s (NCC) board of directors has proposed the distribution of 25% cash dividend to its shareholders. (DFM) Etisalat, Huawei sign deal on 40Gbps GPON technology – Emirates Telecommunication Corporation (Etisalat), and Huawei signed a new agreement that will see the two companies working together to run a trial of their ultra-fast 40Gbps Gigabit Passive Optic Network (GPON) Technology across Etisalat’s footprint over the coming four years. The GPON project can provide the speed and bandwidth required for seamless services including voice over IP, high-speed internet, and IPTV. (GulfBase.com) Agthia to raise production in Al Ain Water – Emirates FoodStuff & Mineral Water Company (Agthia) will increase the production of its bottled water facility (Al Ain Water) and open a new baked goods facility in 2Q2014. The new facility will increase capacity by 60% to 52mn cases of bottled water a year from 32mn cases. Total investment in the expansion amounts to around AED90mn. (GulfBase.com) Adaviation to invest AED25mn in training center – Ahmed Al Khouri, an adviser at Abu Dhabi Aviation Company (Adaviation), announced that the company is investing up to AED25mn in a new flight simulator training center in Abu Dhabi. The company is floating a tender to build the center near the Etihad offices in Abu Dhabi by mid-2015, which will hold the region’s first helicopter simulator. The center will be used to train Adaviation’s own pilots as well as those from the UAE army and police force. (GulfBase.com) Royal Jet’s new operational base to be completed in 4Q2015 – Abu Dhabi-based Royal Jet has announced that the planning and development of its integrated base at Al Bateen Executive Airport is well underway with first phase completion targeted for 4Q2015. The land allocated by Abu Dhabi Airports will be home to Royal Jet’s hangar. Royal Jet will build a 4,500 square metre hangar in addition to a 5,000 square metre facility as a part of its first phase. Royal Jet is the international luxury flight services company, which is jointly owned by Abu Dhabi Aviation and the Presidential Flight Authority the royal flight service. (GulfBase.com) Mubadala, Trafigura acquire iron ore port in Brazil for $971mn – Mubadala Development Company and Trafigura Group have completed the acquisition of a controlling stake in a Brazilian iron ore port terminal from MMX Mineração e Metálicos for $971mn. The deal involved Mubadala and Trafigura (through its Impala subsidiary) paying $400mn for the shares in Porto Sudeste, a major iron-ore port terminal located in Itaguai, Rio de Janeiro state. The two parties will also assume approximately 1.3bn reais (AED2.03bn) of Porto Sudeste’s debt. MMX retains a 35% interest in the port as part of the agreement. Porto Sudeste is designed to handle 50mn tons of iron ore per year, with future expansion to 100mn tons per year. Construction work on the port began in July 2010, with commercial operations expected to begin in 3Q2014. (GulfBase.com) ADNTC’s BoD proposes 16% cash dividend – Abu Dhabi National Takaful Company’s (ADNTC) board has proposed the distribution of 16% cash dividend to its shareholders. (ADX) UCC’s BoD recommends 7% cash dividend – Union Cement Company’s (UCC) board of directors has recommended the distribution of 7% cash dividend to its shareholders for the year ended December 31, 2013. (ADX) OCC to obtain $39mn loan for cement project – The Oman Cement Company (OCC) has decided to obtain a loan to finance the setting up of a new cement mill at its existing plant at an estimated expenditure of $39mn. Further, the company has decided to appoint two new portfolio managers to handle part of its investments. (MSM) Omani Banks’ non-performing loan ratio to total loan portfolio declines – Central Bank of Oman’s (CBO) Executive President, Hamoud bin Sanjour al-Zedjali, said that the ratio of non-performing loan (NPL) to total loan portfolio of the commercial banks in Oman has continued to decline through 2013, reaching 2.1% at the end of September 2013, compared to 2.2% at the end of December 2012. The surplus in Oman's balance of trade was OMR6,268.3mn in 9M2013. However, excluding oil and gas exports, there is a deficit of OMR4,573.4mn. (GulfBase.com) BASREC’s BoD recommends 40% cash dividend – Bahrain Ship Repairing & Engineering Company’s (BASREC) board of directors has recommended the distribution of 40% cash dividends from the paid-up capital (i.e. 40 fils per share) to its shareholders registered on the date of the AGM and EGM. (Bahrain Bourse) Alba appoints new Chairman – Aluminium Bahrain (Alba) has appointed Shaikh Daij bin Salman bin Daij Al Khalifa as the new Chairman of the company. (GulfBase.com) GBCorp reports net profit of $14.835mn – Global Banking Corporation (GBCorp) has reported a net profit of $14.835mn in 2013 as compared to a net loss of $17mn in 2012. Net profit after provisions for 4Q2013 stood at $12.3mn compared to a net loss of $10.3mn for the same period in 2012. The total operating income in 2013 rose to $30.6mn. (GulfBase.com) Bahrain financial sector grows on GCC demand – According to the Economic Development Board (EDB) and Central Bank of Page 5 of 7

- 6. Bahrain (CBB), growing demand for more sophisticated financial products and services helped drive growth in Bahrain's financial sector during 2013 and the trend is expected to continue in 2014. Bahrain attracted a number of businesses, with the number of registered financial services firms swelling to 415 by the end of the year, making it one of the largest financial centres in the region. Among the businesses that established in Bahrain in 2013 were Cigna, Julius Baer and Takaud. (GulfBase.com) RNSS’ BoD proposes 10% cash dividend – Renaissance Services’ (RNSS) board of directors has proposed the distribution of 10% cash dividend (10 Baisa per share) to its shareholders. (MSM) GIS’ BoD recommends 15% cash dividend – Gulf Investment Services Holding Company’s (GIS) board has recommended the distribution of 15% cash dividend (15 Baisa per share) for the year 2013. (MSM) Page 6 of 7

- 7. Rebased Performance Daily Index Performance 180.0 170.0 160.0 150.0 140.0 130.0 120.0 110.0 100.0 90.0 80.0 0.1% 0.0% (0.3%) (0.2%) (0.2%) (0.6%) (0.9%) May-13 S&P Pan Arab Dec-13 S&P GCC Source: Bloomberg ( Asset/Currency Performance Gold/Ounce Silver/Ounce Crude Oil (Brent)/Barrel (FM Future) Natural Gas (Henry Hub)/MMBtu North American Spot LPG Propane Price North American Spot LPG Normal Butane Price Euro Source: Bloomberg (* As of February 27, 2014) Close ($) 1D% WTD% YTD% 1,326.44 0.0 0.0 10.0 21.23 0.0 0.0 9.0 109.07 0.0 0.0 (1.6) 4.70 0.0 0.0 8.1 112.25 0.0 0.0 (11.1) 129.37 0.0 0.0 (5.2) Global Indices Performance Close 1D% WTD% YTD% 16,321.71 0.0 0.0 (1.5) S&P 500 1,859.45 0.0 0.0 0.6 NASDAQ 100 4,308.12 0.0 0.0 3.1 338.02 0.0 0.0 3.0 DAX 9,692.08 0.0 0.0 1.5 FTSE 100 6,809.70 0.0 0.0 0.9 DJ Industrial STOXX 600 1.38 0.0 0.0 0.4 101.80 0.0 0.0 (3.3) GBP 1.67 0.0 0.0 1.1 MSCI EM CHF 1.14 0.0 0.0 1.4 SHANGHAI SE Composite AUD 0.89 0.0 0.0 0.1 USD Index 79.69 0.0 0.0 (0.4) RUB 35.86 0.0 0.0 9.1 BRL 0.43 0.0 0.0 0.9 Yen Dubai Oct-12 Abu Dhabi QE Index Mar-12 (0.9%) Oman Aug-11 (0.7%) Qatar * (1.2%) Jan-11 (0.3%) (0.6%) Bahrain 131.5 Kuwait 144.3 Saudi Arabia Jun-10 0.3% 169.2 Source: Bloomberg CAC 40 Nikkei 4,408.08 0.0 0.0 2.6 14,841.07 0.0 0.0 (8.9) 966.42 0.0 0.0 (3.6) 2,056.30 0.0 0.0 (2.8) HANG SENG 22,836.96 0.0 0.0 (2.0) BSE SENSEX 21,120.12 0.0 0.0 (0.2) Bovespa 47,094.40 0.0 0.0 (8.6) 1,267.27 0.0 0.0 (12.2) RTS Source: Bloomberg Contacts Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui Head of Research Head of Trading Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (―QNBFS‖) a wholly-owned subsidiary of Qatar National Bank (―QNB‖). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7