Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Similar a 5 June Daily market report

Similar a 5 June Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

5 June Daily market report

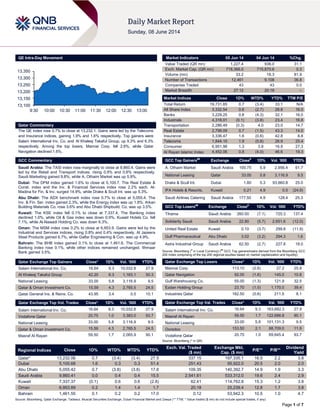

- 1. Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE index rose 0.7% to close at 13,232.1. Gains were led by the Telecoms and Insurance indices, gaining 1.9% and 1.6% respectively. Top gainers were Salam International Inv. Co. and Al Khaleej Takaful Group, up 9.3% and 6.3% respectively. Among the top losers, Mannai Corp. fell 2.6%, while Qatar Navigation declined 1.6%. GCC Commentary Saudi Arabia: The TASI index rose marginally to close at 9,860.4. Gains were led by the Retail and Transport indices, rising 0.9% and 0.6% respectively. Saudi Marketing gained 9.8%, while A. Othaim Market was up 5.9%. Dubai: The DFM index gained 1.6% to close at 5,100.7. The Real Estate & Const. index and the Inv. & Financial Services index rose 2.2% each. Al- Madina for Fin. & Inv. surged 14.9%, while Drake & Scull Int. was up 5.3%. Abu Dhabi: The ADX benchmark index rose 0.7% to close at 5,055.4. The Inv. & Fin. Ser. index gained 2.3%, while the Energy index was up 1.8%. Arkan Building Materials Co. rose 3.6% and Abu Dhabi Shipbuild. Co. was up 3.5%. Kuwait: The KSE index fell 0.1% to close at 7,337.4. The Banking index declined 1.0%, while Oil & Gas index was down 0.9%. Kuwait Hotels Co. fell 7.1%, while Al-Nawadi Holding Co. was down 6.3%. Oman: The MSM index rose 0.2% to close at 6,953.9. Gains were led by the Industrial and Services indices, rising 0.8% and 0.4% respectively. Al Jazeera Steel Products gained 6.7%, while Galfar Engineering & Con. was up 4.9%. Bahrain: The BHB index gained 0.1% to close at 1,461.6. The Commercial Banking index rose 0.1%, while other indices remained unchanged. Ithmaar Bank gained 3.5%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Salam International Inv. Co. 16.64 9.3 10,032.8 27.9 Al Khaleej Takaful Group 42.20 6.3 1,163.1 50.3 National Leasing 33.00 5.8 3,116.9 9.5 Qatar & Oman Investment Co. 15.59 4.3 2,765.5 24.5 Qatar General Ins. & Reins. Co. 43.95 3.4 0.5 10.1 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Salam International Inv. Co. 16.64 9.3 10,032.8 27.9 Vodafone Qatar 20.75 1.0 3,383.0 93.7 National Leasing 33.00 5.8 3,116.9 9.5 Qatar & Oman Investment Co. 15.59 4.3 2,765.5 24.5 Masraf Al Rayan 59.50 1.7 2,065.9 90.1 Market Indicators 05 Jun 14 04 Jun 14 %Chg. Value Traded (QR mn) 1,227.4 936.0 31.1 Exch. Market Cap. (QR mn) 718,366.0 715,870.6 0.3 Volume (mn) 33.2 18.3 81.9 Number of Transactions 12,461 9,108 36.8 Companies Traded 43 43 0.0 Market Breadth 27:12 20:18 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 19,731.85 0.7 (3.4) 33.1 N/A All Share Index 3,332.54 0.6 (2.7) 28.8 16.0 Banks 3,229.25 0.8 (4.3) 32.1 16.0 Industrials 4,318.01 (0.1) (3.8) 23.4 16.8 Transportation 2,286.49 (0.3) 4.0 23.0 14.7 Real Estate 2,799.09 0.7 (1.5) 43.3 14.0 Insurance 3,336.47 1.6 (0.6) 42.8 8.8 Telecoms 1,844.15 1.9 (0.8) 26.9 25.4 Consumer 6,951.98 1.3 3.8 16.9 27.3 Al Rayan Islamic Index 4,452.06 0.8 (4.0) 46.6 19.3 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% A. Othaim Market Saudi Arabia 100.75 5.9 2,956.4 61.7 National Leasing Qatar 33.00 5.8 3,116.9 9.5 Drake & Scull Int. Dubai 1.80 5.3 93,660.8 25.0 IFA Hotels & Resorts. Kuwait 0.21 4.9 0.5 (24.9) Saudi Airlines Catering Saudi Arabia 177.50 4.9 128.4 25.3 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Tihama Saudi Arabia 260.50 (7.1) 725.3 137.4 Solidarity Saudi Saudi Arabia 22.80 (5.7) 2,651.6 (12.0) United Real Estate Kuwait 0.10 (3.7) 299.8 (11.9) Gulf Pharmaceutical Abu Dhabi 3.02 (3.2) 294.3 1.6 Astra Industrial Group Saudi Arabia 62.50 (2.7) 227.8 18.0 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Mannai Corp. 113.10 (2.6) 27.2 25.8 Qatar Navigation 92.00 (1.6) 145.0 10.8 Gulf Warehousing Co. 55.00 (1.3) 121.9 32.5 Ezdan Holding Group 23.70 (1.0) 1,170.0 39.4 Industries Qatar 182.50 (0.6) 211.5 8.1 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Salam International Inv. Co. 16.64 9.3 163,682.3 27.9 Masraf Al Rayan 59.50 1.7 122,686.8 90.1 National Leasing 33.00 5.8 101,131.3 9.5 Ooredoo 153.50 2.1 88,709.0 11.9 Vodafone Qatar 20.75 1.0 69,645.4 93.7 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 13,232.06 0.7 (3.4) (3.4) 27.5 337.15 197,335.1 16.5 2.2 3.8 Dubai 5,100.68 1.6 0.3 0.3 51.4 251.43 95,922.0 20.5 2.0 2.0 Abu Dhabi 5,055.42 0.7 (3.8) (3.8) 17.8 109.35 140,392.7 14.9 1.9 3.3 Saudi Arabia 9,860.41 0.0 0.4 0.4 15.5 2,541.61 533,312.0 19.6 2.4 2.9 Kuwait 7,337.37 (0.1) 0.6 0.6 (2.8) 62.41 114,762.8 15.3 1.2 3.8 Oman 6,953.89 0.2 1.4 1.4 1.7 20.18 25,239.4 12.8 1.7 3.8 Bahrain 1,461.55 0.1 0.2 0.2 17.0 0.12 53,942.3 10.5 1.0 4.7 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 13,100 13,150 13,200 13,250 13,300 13,350 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE index rose 0.7% to close at 13,232.1. The Telecoms and Insurance indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders. Salam International Inv. Co. and Al Khaleej Takaful Group were the top gainers, rising 9.3% and 6.3% respectively. Among the top losers, Mannai Corp. fell 2.6%, while Qatar Navigation declined 1.6%. Volume of shares traded on Thursday rose by 81.9% to 33.2mn from 18.3mn on Wednesday. Further, as compared to the 30-day moving average of 27.9mn, volume for the day was 19.0% higher. Salam International Investment Co. and Vodafone Qatar were the most active stocks, contributing 30.2% and 10.2% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Aldar Properties S&P UAE LT/ST CCR BB/B BB+/B Stable – Gulf Bank S&P Kuwait LT CR BBB+ BBB+ – Positive – Gulf Bank CI Kuwait FSR BB+ BBB- Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, CCR – Corporate Credit Rating, CR – Credit Rating) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 06/05 US IPSOS Public Affairs RBC Consumer Outlook Index June 51.0 – 50.1 06/05 US Bloomberg Bloomberg Consumer Comfort 1 June 35.1 – 33.3 06/06 US BLS Unemployment Rate May 6.30% 6.40% 6.30% 06/06 US BLS Underemployment Rate May 12.20% – 12.30% 06/07 US Federal Reserve Consumer Credit April $26.847B $15.000B $19.504B 06/05 EU Markit Markit Eurozone Retail PMI May 49.9 – 51.2 06/05 EU Eurostat Retail Sales MoM April 0.40% 0.00% 0.10% 06/05 EU Eurostat Retail Sales YoY April 2.40% 1.20% 1.00% 06/05 EU European Central Bank ECB Announces Interest Rates 5 June 0.15% 0.10% 0.25% 06/05 EU European Central Bank ECB Marginal Lending Facility 5 June 0.40% 0.60% 0.75% 06/05 EU European Central Bank ECB Deposit Facility Rate 5 June -0.10% -0.10% 0.00% 06/05 France Markit Markit France Retail PMI May 50.5 – 50.3 06/06 France Ministry of the Economy Budget Balance YTD April -64.2B – -28.0B 06/06 France Ministry of the Economy Trade Balance April -3933M -5000M -4867M 06/05 Germany Markit Markit Germany Construction PMI May 48.1 – 49.7 06/05 Germany Markit Markit Germany Retail PMI May 52.5 – 53.1 06/06 Germany Deutsche Bundesbank Industrial Production SA MoM April 0.20% 0.40% -0.60% 06/06 Germany BMWi Industrial Production WDA YoY April 1.80% 2.70% 2.90% 06/06 Germany Destatis Trade Balance April 17.4B 15.1B 16.6B 06/06 Germany Destatis Current Account Balance April 18.4B 15.6B 19.7B 06/06 Germany Deutsche Bundesbank Exports SA MoM April 3.00% 1.30% -1.80% 06/06 Germany Deutsche Bundesbank Imports SA MoM April 0.10% 0.80% -1.10% 06/05 UK Bank of England Bank of England Bank Rate 5 June 0.50% 0.50% 0.50% 06/06 UK ONS Trade Balance Non EU GBP/Mn April -£3783 -£3150 -£3418 06/06 UK ONS Trade Balance April -£2543 -£1500 -£1057 06/06 Spain INE Industrial Output NSA YoY April -1.90% – 8.10% 06/06 Spain INE Industrial Output SA YoY April 4.30% 1.20% 0.90% 06/05 Italy Markit Markit Italy Retail PMI May 45.2 – 49.5 06/05 China Markit HSBC China Services PMI May 50.7 – 51.4 06/05 China Markit HSBC China Composite PMI May 50.2 – 49.5 06/06 Japan Ministry of Finance Official Reserve Assets May $1283.9B – $1282.8B 06/06 Japan ESRI Leading Index CI April 106.6 106.1 107.1 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari 56.98% 65.43% (103,713,386.89) Non-Qatari 43.02% 34.57% 103,713,386.89

- 3. Page 3 of 7 News Qatar MCCS completes 49% stake sale in Transfield Mannai – Mannai Corporation’s (MCCS) wholly owned subsidiary, Gulf Laboratories, has completed the sale of its 49% shareholding in Transfield Mannai to Cofely Besix Facility Management Ltd. However, MCCS still holds the remaining 51% stake in Transfield Mannai. Following the completion of the requisite formalities, the company will be renamed as ‘Cofely Besix Mannai Facility Management’. (QE) Mannai HED sees growing potential for heavy transport equipment in Qatar – Mannai Heavy Equipment Division (Mannai HED) sees growing potential for heavy transport equipment in the country, including its DAF trucks line. According to Mannai HED, DAF trucks are among the most reliable and sought-after trucks in the construction, distribution and long-haul sectors. Mannai HED’s partnership with DAF allows it to deliver standard production trucks customized to suit client requests. DAF is a global leader in ‘build to order’ truck deliveries. (Gulf-Times.com) QNBK wins two Euromoney awards – QNB Group (QNBK) has been awarded "The Best Bank in the Middle East" and "The Best Bank in Qatar" Awards by eminent international finance magazine Euromoney. The awards reflect the continuing progress being made by QNBK across the MENA region and the domestic market. This also marks the 11th occasion that QNBK has won this accolade from the international magazine. (Peninsula Qatar) DIG to form JV with Klondike Technologies – Ireland-based thermal management solutions provider, Klondike Technologies has signed a MoU with Dyarco International Group (DIG) to form a joint venture. The move marks an essential part of Klondike’s strategy to establish a permanent footprint in Qatar and the GCC region, by leveraging Dyarco’s over 20 years of experience in the service consultancy industry in Qatar. (Gulf-Times.com) QDREIC, CWG wins London Shell centre project approval – Qatari Diar Real Estate Investment Company (QDREIC) and Canary Wharf Group (CWG) have won approval to redevelop a site in central London next to the River Thames. Under the plan, eight new buildings will be constructed around the Shell Centre on the south bank of the Thames, creating a 1.45mn square feet complex with shops, offices and 877 homes. (Reuters, Bloomberg) QIIK wins Best Islamic Bank 2014 award – Qatar International Islamic Bank (QIIK) has won the “Best Islamic Bank in Qatar 2014” award given by UK-based Capital Finance International (CFI). QIIK stated that CFI considered a number of criteria such as financial stability, profitability, continued growth, asset quality, adherence to Islamic banking standards as well as the steady expansion in QIIK’s customer base. (Bloomberg) QDB named Best Development Bank in Middle East – Qatar Development Bank (QDB) has been named as the “Best Development Bank in the Middle East” at the 2014 Banker Middle East Industry Awards. (Peninsula Qatar) Qatar Solar Energy to be launched today - Qatar Solar Energy Company, which aims to produce solar energy and boast the largest solar energy technology in the Middle East will have its official launch soon. The company is expected to produce and market solar energy at a cheaper rate as compared to conventional electricity. (Peninsula Qatar) International Fed officials put forward financial stability concerns – Two officials of the US Federal Reserve have warned that raising interest rates to fend off troubling signs in the financial market could undercut the Fed's efforts to put the US economy back on a sounder footing. San Francisco Fed President John Williams presented alternative ways to use the monetary policy to shore up the financial system's ability to withstand shocks. These included ‘nominal income targeting’, which is aimed at keeping incomes growing steadily so that families will be in a better position to avoid bankruptcy. Williams said such alternative approaches can boost stability without derailing the Fed from its main goals of low inflation and high employment. Meanwhile, Minneapolis Fed President Narayana Kocherlakota counseled a measure of tolerance for increasing financial stability risks, painting those risks as an unwanted, but an unavoidable side effect of the low rates the economy will need for years to claw its way back to normal. (Reuters) BofA shrinks its Irish derivatives business amid move to London – The Bank of America Corp (BofA) has shrunk its Irish derivatives business by $169bn over the past two years as part of a plan to move most of its contracts in Dublin to London by the end of 2014. Merrill Lynch International Bank’s derivative contracts in Dublin fell to $368.6bn on December 31, 2013 from $537.3bn at the end of 2011. The move helped cut the Irish- based bank’s total assets by $187bn to $406bn over the two years. According to sources, BofA as well as many other large, international banks, are addressing a dual goal of cost reductions and regulatory pressure to simplify risk. This is part of BofA’s plans to move most of the derivatives on its Irish balance sheet at the end of 2011 to its London operation. (Bloomberg) ECB hurls cash at sluggish Eurozone economy – The European Central Bank (ECB) cut its interest rates to record lows last week as part of its several measures to pump money into the sluggish Eurozone economy, and pledged to do more if needed to fight off deflation risk. For the first time, the ECB will charge banks for parking funds overnight at the central bank in an attempt to force them to lend to small and medium-sized businesses. These measures were also aimed at easing pressure on the strong euro, which is threatening the economic recovery and is creating deflation. Inflation in the Eurozone has been stuck in the so-called ‘danger zone’ below 1% since October 2013, because of weaker commodity and food prices, as well as wage and other adjustments in crisis countries. The central bank stopped short of full-fledged quantitative easing (QE), but ECB President Mario Draghi said more action would come if necessary. (Reuters) German industrial output rises in April with solid growth pace – Industrial output in Germany rose in April 2014 in a sign that Europe’s largest economy is poised to continue growing at a solid pace. The Federal Statistics Office said production adjusted for seasonal swings increased 0.2% from March 2014, when it declined a revised 0.6%. Production rose 1.8% YoY in April when adjusted for working days. Despite that, the Bundesbank stated that growth will slow noticeably after a faster-than-forecast expansion in the first quarter, even as factory orders rebounded in April. While Germany remains Europe’s economic powerhouse, low inflation and a weak recovery in the 18-nation Eurozone weigh down on the recovery outlook. A recent report showed manufacturing rose 0.1%, while consumer-goods output advanced 1.1%, and intermediate goods production increased 0.1%. Construction output retreated 1.2% and energy output increased 2.7%. (Bloomberg)

- 4. Page 4 of 7 Abe orders review of Japanese pension fund assets – Japanese Prime Minister Shinzo Abe ordered an earlier review of the biggest pension fund’s portfolio, amid speculation that the fund is already buying more stocks. Health Minister Norihisa Tamura said he will ask the Government Pension Investment Fund (GPIF) worth 128.6tn yen to work on an overhaul of its investments by September or October. Investors are watching for Japan’s cautious retirement savings managers, led by GPIF, to shift into shares as the Bank of Japan spurs inflation that risks eroding the value of bonds. The Topix index of equities slipped 5.2% this year, adding pressure on Abe to prove his policies can spur a sustained economic recovery. Trust banks, which often trade on behalf of pension investors, are putting their most money on local stocks in five years as foreigners sell, fueling speculation that GPIF is already buying. (Bloomberg) IMF urges China to focus on reforms, target 7% growth in 2015 – The International Monetary Fund (IMF) recommended that China adopt an economic growth target of about 7% for 2015 and urged authorities to avoid further stimulus measures and concentrate on curtailing financial risks instead. The IMF said Beijing must keep its word on implementing reforms that will correct imbalances, including a moderately undervalued Chinese yuan. Specifically, the fund said conditions are right for China to take the next step in freeing its interest rates market, challenging the view that the country is not yet ready for such a move. IMF's First Deputy Managing Director David Lipton said the bigger threat to China is its persistent reliance on debt and investment in areas such as real estate to power its economy. Lipton said unless China's economy is at risk of missing its growth target of about 7.5% this year by a substantial margin, more stimulus is unwarranted. (Reuters) WB sees China’s 7.5% growth on track, urges reform – The World Bank (WB) said China is likely to meet its economic growth target of 7.5% this year, but it must persevere with its fiscal and financial sector reforms to deal with the root cause of its debt problems. The development bank said that the prospect of growth falling below the Chinese government target is likely to trigger accommodative fiscal and monetary policies. These measures should help the authorities to reach an indicative growth target of around 7.5% in 2014, but is likely add to current imbalances and vulnerabilities. The government unveiled a series of targeted measures after the economy got off to a weak start this year, with official manufacturing and service sector surveys in May already showing an improvement. WB expects the Chinese economy to grow 7.6% this year on policy support and a recovery of global demand, while it noted growth could slow to 7.5% in 2015. (Reuters) Regional IMF urges GCC economies to diversify for stronger growth – The IMF Deputy Managing Director Min Zhu said that GCC countries have grown strongly and seen huge improvements in their human development indicators (HDI), but they remain susceptible to fluctuations in oil markets. They need greater economic diversification to boost productivity, living standards, create jobs, and reduce fiscal and external risks associated with the heavy reliance on oil revenues. The prevailing growth model in the GCC region has achieved a rapid improvement in HDI, but has also resulted in a decline in relative economic performance. He said that the main features of this growth model are: the reliance on oil as the main source of revenues, the dependence of the private sector on expatriate labor, and the concentration of economic activity in the low skilled non-tradable sector. The IMF mentioned that the UAE’s airports and seaport infrastructure development, Saudi Arabia’s economic cities, Qatar’s commercial airline, Bahrain’s aluminum industry, and SMEs in Kuwait and Oman as the success stories of diversification. (Peninsula Qatar) KFH Research: GCC healthcare spend to reach $80bn by 2015 – According to a report by KFH Research, health expenditure per capita grew at an annualized rate of 7.9% for the GCC region during 2001-2011. However, the GCC’s overall healthcare expenditure as percentage of GDP remains low at 3.8%, much below the world average of 10%. Country-wise, the total healthcare expenditure as a percentage of GDP in Saudi Arabia and Bahrain is at 3.7%, relatively better than other GCC countries. This is followed by the UAE (3.3%), Kuwait (2.7%), Oman (2.3%) and Qatar (1.9%). According to market consensus, the healthcare expenditure among GCC countries is set to reach almost $80bn in 2015 with public expenditure contributing approximately 64%. (Bloomberg) OAPEC announces new oil & gas discoveries – The Organization of Arab Petroleum Exporting Countries (OAPEC) announced that 34 new oil discoveries and 10 natural gas discoveries have been made in 2013. OAPEC’s monthly report said that the most prominent discovery was in Algeria’s southern region of Hassi Messaoud. Around 1.3bn barrels of oil was discovered in the region, while an estimated 71bn cubic meters of natural gas was found at Qatar’s Al-Shimal field in 2013. OAPEC embarked on several key projects in 2013, noting that Saudi Arabia had begun its Karan Gas Project, which produces 4.2mn cubic meters of gas per day. (GulfBase.com) S&P affirms ratings on Saudi Arabia; outlook positive – Standard & Poor's has affirmed its long and short-term foreign and local currency sovereign credit ratings on the Kingdom of Saudi Arabia at AA-/A-1+. The outlook remains positive. (Bloomberg) Tadawul announces suspension, delisting of SEC Sukuk 2 – The Saudi Stock Exchange (Tadawul) announced the suspension of the Saudi Electricity Company’s (SEC) Sukuk 2 on June 5, 2014 based on the CMA approval of SEC’s request to purchase the SEC Sukuk 2 issue. Accordingly, the Sukuk will be delisted from Tadawul on July 6, 2014. (Tadawul) SAIB completes issuing SR2bn Sukuk – The Saudi Investment Bank (SAIB) has completed the issuance of a SR2bn Sukuk through a private placement inside the Kingdom on June 5, 2014. This Islamic bond will support the bank's capital base in accordance with Basel III requirements in order to assist the bank’s further growth. The issuance has a tenor of 10 years with the bank having the right to call the Sukuk at the end of the fifth year. The instrument was priced at 145 basis points over the six-month Saudi interbank offered rate (SIBOR). (Tadawul) Almarai signs two deals with PDC – Almarai Company has signed two agreements with the Ports Development Company (PDC) in Rabigh. The first one consists of a renewable long- term bulk-berth use agreement that will provide Almarai a right to use a designated berth according to its needs. Almarai will invest in erecting discharge equipment including crane and its related support equipments. The second agreement consists of a renewable long-term industrial land-lease agreement of a 35,000-square meter industrial plot located within the King Abdullah Port Processing and Services Zone. From November 2014, Almarai will erect grain silos on this plot to store and transport bulk cargos of grains. (Tadawul) GO Telecom signs IRU agreement with STC – Etihad Atheeb Telecommunication Company (GO Telecom) has signed an Indefeasible Rights of Use (IRU) agreement with the Saudi Telecommunication Company (STC). Under the agreement

- 5. Page 5 of 7 terms, STC has granted IRU to GO Telecom for 15 years of 30,000 ports on its fiber network as an initial phase. The agreement gives GO Telecom the right to acquire up to 100,000 ports. GO Telecom will use these ports to serve its residential and small business clients with broadband internet services and fixed voice services. (Tadawul) Alhokair signs SR1bn loan deal – Fawaz Abdulaziz Alhokair & Company (Alhokair) has signed SR1bn Islamic loan maturing in March 2021 to help repay loans and fund expansion. The loan is repayable by semi-annual installments starting 18 months from June 4, 2014. Samba Financial Group’s investment banking arm arranged the loan, while Gulf International Bank, National Commercial Bank, Arab Bank, Saudi Hollandi Bank and the National Bank of Kuwait are participating lenders. (GulfBase.com) First IPP project launched in Rabigh – The first Independent Power Producer (IPP) project for producing electrical power in Saudi Arabia has been launched with a total investment of around SR10bn in Rabigh City. The project has a generation capacity of 1,204 megawatts (MW). (GulfBase.com) Jeddah Economic selects Kone to provide elevators for Kingdom Tower – Jeddah Economic Company has selected Kone as the vertical transportation provider to deliver the world’s fastest and highest double-decker elevators to the Kingdom Tower. The Kingdom Tower is expected to rise to a height of more than 1km upon completion in 2018. Featuring Kone’s people flow solutions, the building will have the world’s fastest double deck elevators with travel speed of over 10 m/s as well as the world’s highest elevator rise at 660 meters. (GulfBase.com) Al-Zayedi launches SR70mn cement products plant – Al- Zayedi Group for Development & Investment (Al-Zayedi) has launched SR70mn Al-Zayedi plant for cement products in Makkah. The plant has a capacity of manufacturing 100,000 blocks and 5,000 interlock blocks daily. Large contracts totaling SR20mn were signed, including projects in Makkah and development of the paving of the Jeddah Islamic Port. The projects being undertaken by the company include development of the Al-Aziziyah Road, Al-Awali streets, Jeddah Corniche and entrances of Asfan and Shamiah. (GulfBase.com) UBF launches Mobile Wallet - The UAE Banks Federation (UBF) has begun the implementation of its Mobile Wallet project. The project is a comprehensive digital payment solution and has been developed by a special committee of nine-member banks under the Chairmanship of Tirad Al Mahmoud, CEO of Abu Dhabi Islamic Bank. The project is expected to be implemented over next year in phases. The Mobile Wallet is a financial component of the Smart Government initiative, which has identified over 90 services provided by government departments requiring digital payment in the UAE. (GulfBase.com) REN21: UAE third in CSP capacity – According to REN21, the UAE has been ranked third among the world’s nations in both 2013 concentrated solar power (CSP) technology investment and total CSP capacity. The 100 megawatt Masdar’s Shams I CSP plant in Abu Dhabi is one reason why CSP’s growth in emerging markets almost tripled during 2013. (GulfBase.com) IDS, HP extends technology partnership – UAE-based Injazat Data Systems (IDS) and US-based Hewlett-Packard Company (HP) have extended their collaboration to strengthen enterprise and public cloud offering, specifically targeted at Government and enterprise clients in the Middle East region. Injazat is a joint venture between HP and Mubadala, is already an HP-certified Software Partner, and will work closely with HP Middle East to develop the new breed of cloud services specifically designed and packaged for the region. (GulfBase.com) Emaar Malls to hold investor meetings from June 8 – Emaar Malls Group will hold meetings with fixed income investors in Asia, Europe and Middle East from June 8, 2014 ahead of a potential benchmark-sized sukuk issue. Dubai Islamic Bank, Emirates NBD, Mashreq, Morgan Stanley, First Gulf Bank, National Bank of Abu Dhabi, Noor Bank and Standard Chartered will be arranging the meetings on Emaar’s behalf. (DFM) MEED: Dubai real estate projects market tops $123bn – According to MEED Projects, 744 individual real-estate developments are currently planned or underway in Dubai with a combined budget value of $123bn. The combined value of the top 10 biggest projects planned or underway in Dubai is $50.5bn. The biggest individual project currently planned in the Emirate is $17.7bn Lagoons project being developed jointly by Dubai Holding and Emaar Properties as part of the $32bn Mohammed Bin Rashid City megaproject. (GulfBase.com) NBC appoints Noor Bank as distributor – National Bonds (NBC) has appointed Noor Bank as a distribution agent to extend the availability of the savings program. As part of the agreement, NBC will also join Noor Bank's direct debit scheme (DDS) platform recently facilitated by the UAE Central Bank. This will allow Noor Bank to register any NBC customer with the DDS without the necessity of him or her maintaining an account with Noor Bank. (Bloomberg) Abu Dhabi Airport April passenger traffic rises 22.5% – Abu Dhabi International Airport said that the passenger traffic in April 2014 rose by 22.5% to 1.62mn passengers as compared to 1.51mn passengers in April 2013. Aircraft movements rose 16.4% to 12,420 as compared to 10,673 in April 2013. Cargo activity handling rose to 60,059 tons, a 17% increase from April 2013. (Bloomberg) S&P affirms ratings on Oman; outlook stable – Standard & Poor's (S&P) Ratings Services has affirmed its 'A/A-1' long and short-term foreign and local currency sovereign credit ratings on the Sultanate of Oman. The outlook is stable. (Bloomberg) Al Batinah to invest OMR928,500 in IPOs – Al Batinah Development & Investment Holding Company’s BoD has approved to invest OMR928,500 in the IPOs of Al-Batinah Power Company and Al-Suwadi Power Company. (MSM) Topaz energy, Viking ink life-raft servicing contract – Renaissance Services’ subsidiary Topaz Energy & Marine and Viking Life-Saving Equipment have signed a multi-million dollar, 10-year life-raft servicing agreement. Under the terms of the contract, Viking will upgrade all of Topaz's current life-rafts and manage the ongoing servicing and certification of Topaz's life- raft fleet. (GulfBase.com) GPIC production rate surges to new record – Gulf Petrochemical Industries Company (GPIC) has achieved the highest production rate in its history during 1Q2014. A total of 460,029 metric tons of methanol, ammonia and urea were produced during the period without any lost time accidents. (GulfBase.com) 29 projects ready at SEZAD – Special Economic Zone Authority Duqm’s (SEZAD) Chairman, Yahya bin Said Al Jabri, said that 29 projects have been completed at a total cost of more than OMR1.7bn at SEZAD. These projects include a commercial terminal, the drydock, Duqm port, power plant, water desalination plant, electricity distribution network, water distribution network, main road, sanitary drainage plant, Crowne

- 6. Page 6 of 7 Plaza Hotel, City Hotel, the hospital expansion and employees' camp. (GulfBase.com) Al Rafd Fund provides OMR14mn loan – Oman’s Minister of Commerce & Industry (MCI) and Chairman of Al Rafd Fund, Dr. Ali bin Masud Al Sunaidi, said that the Al Rafd Fund has financed more than 500 projects to the tune of over OMR14mn. These projects are managed by full-time entrepreneurs. (GulfBase.com) NCSI: Oman's budget surplus at OMR615.4mn in 1Q2014 – According to a report by National Centre for Statistics and Information (NCSI), Oman's budget surplus stood lower at OMR615.4mn in 1Q2014, down from OMR931mn 1Q2013. Net oil revenue declined by 4.7% to OMR2,586.8mn from OMR2,714.1mn, mainly due to a fall in international oil prices, according to the information from National Centre for Statistics and Information. Although oil production edged up by 1.1% to 113.09mn barrels in 1Q2014, average price of Oman crude fell by 2.2% to $105.73 per barrel from $108.07 per barrel. As a result, the country's total revenue in fell 1Q2014 substantially by 7% to OMR3,214.3mn from OMR3,456.7mn, while total expenditure was up by 2.9% to OMR2,598.9mn from OMR2.525.7mn. The Sultanate of Oman, which based its 2014 budget on a projected oil price of $85 per barrel, expects expenditure of OMR13.5bn and a deficit of OMR1.8bn in 2014. (GulfBase.com) Al Salam and BMI Bank in Meethaq partnership – Al Salam Bank Bahrain (ASBB) and BMI Bank jointly signed a MoU with Meethaq, the pioneer of Islamic banking in Oman from Bank Muscat. As part of the MoU, the banks have collectively agreed to pool their expertise and resources to work together across a range of Islamic banking activities. These include Islamic syndications, particularly those issued in Oman, treasury transactions, liquidity management products and Islamic trade finance transactions. (Bloomberg)

- 7. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg (*Market closed on June 06, 2014) Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC 0.0% 0.7% (0.1%) 0.1% 0.2% 0.7% 1.6% (0.8%) 0.0% 0.8% 1.6% 2.4% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,253.25 (0.0) 0.3 3.9 DJ Industrial 16,924.28 0.5 1.2 2.1 Silver/Ounce 19.03 (0.1) 1.1 (2.2) S&P 500 1,949.44 0.5 1.3 5.5 Crude Oil (Brent)/Barrel (FM Future) 108.61 (0.2) (0.7) (2.0) NASDAQ 100 4,321.40 0.6 1.9 3.5 Natural Gas (Henry Hub)/MMBtu 4.65 0.2 3.6 7.0 STOXX 600 347.30 0.7 0.9 5.8 LPG Propane (Arab Gulf)/Ton* 101.00 0.0 (3.2) (20.0) DAX 9,987.19 0.4 0.4 4.6 LPG Butane (Arab Gulf)/Ton 117.00 (0.4) (2.5) (14.3) FTSE 100 6,858.21 0.7 0.2 1.6 Euro 1.36 (0.1) 0.1 (0.7) CAC 40 4,581.12 0.7 1.4 6.6 Yen 102.48 0.1 0.7 (2.7) Nikkei 15,077.24 (0.0) 3.0 (7.5) GBP 1.68 (0.1) 0.3 1.5 MSCI EM 1,044.93 1.0 1.7 4.2 CHF 1.12 (0.2) 0.2 (0.1) SHANGHAI SE Composite 2,029.96 (0.5) (0.5) (4.1) AUD 0.93 (0.1) 0.2 4.7 HANG SENG 22,951.00 (0.7) (0.6) (1.5) USD Index 80.41 0.0 0.0 0.5 BSE SENSEX 25,396.46 1.5 4.9 20.0 RUB 34.41 (0.8) (1.4) 4.7 Bovespa 53,128.66 3.0 3.7 3.1 BRL 0.44 0.7 (0.3) 5.1 RTS 1,359.10 1.9 4.9 (5.8) 190.1 155.7 141.6