Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Similar a 7 July Daily market report

Similar a 7 July Daily market report (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

7 July Daily market report

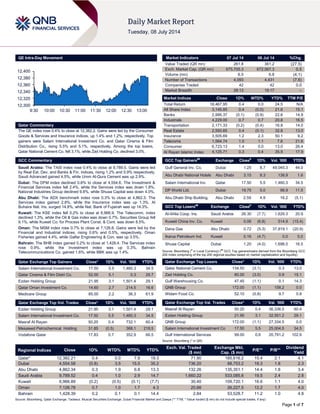

- 1. Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE index rose 0.4% to close at 12,382.2. Gains were led by the Consumer Goods & Services and Insurance indices, up 1.4% and 1.2%, respectively. Top gainers were Salam International Investment Co. and Qatar Cinema & Film Distribution Co., rising 5.5% and 5.1%, respectively. Among the top losers, Qatar National Cement Co. fell 3.1%, while Zad Holding Co. declined 3.0%. GCC Commentary Saudi Arabia: The TASI index rose 0.4% to close at 9,789.5. Gains were led by Real Est. Dev. and Banks & Fin. indices, rising 1.2% and 0.9% respectively. Saudi Advanced gained 4.5%, while Umm Al-Qura Cement was up 2.9%. Dubai: The DFM index declined 0.8% to close at 4,554.6. The Investment & Financial Services index fell 2.4%, while the Services index was down 1.8%. National Industries Group declined 9.8%, while Shuaa Capital was down 4.0%. Abu Dhabi: The ADX benchmark index rose 0.3% to close at 4,862.3. The Services index gained 2.8%, while the Insurance index was up 1.3%. Al Buhaira Nat. Ins. surged 14.8%, while Nat. Bank of Fujairah was up 14.3%. Kuwait: The KSE index fell 0.2% to close at 6,966.9. The Telecomm. index declined 1.3%, while the Oil & Gas index was down 0.7%. Securities Group fell 9.1%, while Kuwait Co. for Process Plant Const. & Cont. was down 8.5%. Oman: The MSM index rose 0.7% to close at 7,126.8. Gains were led by the Financial and Industrial indices, rising 0.6% and 0.5%, respectively. Oman Fisheries gained 4.4%, while Galfar Engineering & Con. was up 3.5%. Bahrain: The BHB index gained 0.2% to close at 1,428.4. The Services index rose 0.9%, while the Investment index was up 0.3%. Bahrain Telecommunications Co. gained 1.6%, while BBK was up 1.4%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Salam International Investment Co. 17.50 5.5 1,460.3 34.5 Qatar Cinema & Film Distri Co. 52.00 5.1 0.3 29.7 Ezdan Holding Group 21.95 3.1 1,501.4 29.1 Qatar Oman Investment Co. 14.60 2.7 214.5 16.6 Medicare Group 85.00 2.2 36.3 61.9 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 21.95 3.1 1,501.4 29.1 Salam International Investment Co. 17.50 5.5 1,460.3 34.5 Masraf Al Rayan 50.20 0.4 732.1 60.4 Mesaieed Petrochemical Holding 31.85 (0.5) 368.1 218.5 Vodafone Qatar 17.83 0.7 352.9 66.5 Market Indicators 07 Jul 14 06 Jul 14 %Chg. Value Traded (QR mn) 261.8 361.2 (27.5) Exch. Market Cap. (QR mn) 675,705.3 672,567.3 0.5 Volume (mn) 6.5 6.8 (4.1) Number of Transactions 4,093 4,431 (7.6) Companies Traded 42 42 0.0 Market Breadth 28:13 19:17 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,467.95 0.4 0.0 24.5 N/A All Share Index 3,145.85 0.4 (0.0) 21.6 15.1 Banks 2,995.37 (0.1) (0.9) 22.6 14.9 Industrials 4,229.00 0.7 0.7 20.8 16.5 Transportation 2,171.33 (0.2) (0.4) 16.8 14.0 Real Estate 2,593.65 0.4 (0.1) 32.8 13.0 Insurance 3,505.69 1.2 2.3 50.1 9.2 Telecoms 1,564.74 1.0 1.1 7.6 21.6 Consumer 6,723.13 1.4 0.0 13.0 26.4 Al Rayan Islamic Index 4,125.71 0.3 0.4 35.9 17.9 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Gulf General Inv. Co. Dubai 1.25 8.7 49,045.3 44.0 Abu Dhabi National Hotels Abu Dhabi 3.15 8.3 138.9 1.6 Salam International Inv. Qatar 17.50 5.5 1,460.3 34.5 DP World Ltd. Dubai 19.75 5.0 98.9 11.5 Abu Dhabi Ship Building. Abu Dhabi 2.59 4.9 16.2 (5.1) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Al-Ahlia Coop. Ins. Saudi Arabia 26.30 (7.7) 1,629.3 20.9 Kuwait China Inv. Co. Kuwait 0.06 (6.8) 514.9 (15.4) Dana Gas Abu Dhabi 0.72 (5.3) 37,819.1 (20.9) Ikarus Petroleum Ind. Kuwait 0.16 (4.7) 0.0 5.0 Shuaa Capital Dubai 1.20 (4.0) 1,698.0 16.5 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar National Cement Co. 134.50 (3.1) 0.3 13.0 Zad Holding Co. 80.00 (3.0) 0.9 15.1 Gulf Warehousing Co. 47.45 (1.1) 0.1 14.3 QNB Group 172.00 (1.1) 158.2 0.0 Widam Food Co. 52.10 (0.8) 9.7 0.8 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Masraf Al Rayan 50.20 0.4 36,336.5 60.4 Ezdan Holding Group 21.95 3.1 32,551.2 29.1 QNB Group 172.00 (1.1) 27,334.5 0.0 Salam International Investment Co 17.50 5.5 25,004.5 34.5 Gulf International Services 99.00 0.6 20,791.2 102.9 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,382.21 0.4 0.0 7.8 19.3 71.90 185,616.2 15.4 2.1 4.1 Dubai 4,554.58 (0.8) 3.5 15.5 35.2 736.20 88,753.2 18.3 1.8 2.3 Abu Dhabi 4,862.34 0.3 1.9 6.8 13.3 132.26 135,351.1 14.4 1.8 3.4 Saudi Arabia 9,789.52 0.4 1.0 2.9 14.7 1,660.22 533,085.8 19.5 2.4 2.8 Kuwait 6,966.89 (0.2) (0.5) (0.1) (7.7) 30.40 109,720.1 16.6 1.1 4.0 Oman 7,126.78 0.7 1.0 1.7 4.3 20.66 26,227.5 12.2 1.7 4.0 Bahrain 1,428.39 0.2 0.1 0.1 14.4 2.84 53,528.7 11.2 1.0 4.8 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,300 12,320 12,340 12,360 12,380 12,400 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE index rose 0.4% to close at 12,382.2. The Consumer Goods & Services and Insurance indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders. Salam International Investment Co. and Qatar Cinema & Film Distribution Co. were the top gainers, rising 5.5% and 5.1%, respectively. Among the top losers, Qatar National Cement Co. fell 3.1%, while Zad Holding Co. declined 3.0%. Volume of shares traded on Monday fell by 4.1% to 6.5mn from 6.8mn on Sunday. Further, as compared to the 30-day moving average of 21.2mn, volume for the day was 69.3% lower. Ezdan Holding Group and Salam International Investment Co. were the most active stocks, contributing 23.0% and 22.4% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Commercial Bank of Dubai Limited (CBD) CI Dubai LT FCR/ST FCR/SR/FSR A-/A2/2/BBB+ A-/A2/2/BBB+ – Stable – National Bank of Oman's (NBO) CI Oman LT FCR/ST FCR/SR/FSR BBB+/A2/3 BBB+/A2/3/ BBB+ Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency) Earnings Releases Company Market Currency Revenue (mn)1Q2014 % Change YoY Operating Profit (mn) 2Q2014 % Change YoY Net Profit (mn) 2Q2014 % Change YoY Jarir Marketing Co. Saudi Arabia SR – – 133.3 4.7% 135.2 7.1% United Electronic Co. (UEC) Saudi Arabia SR – – 56.1 2.2% 53.8 0.9% Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 07/07 EU Sentix Sentix Investor Confidence July 10.1 7.8 8.5 07/07 Germany Deutsche Bundesbank Industrial Production SA MoM May -1.80% 0.00% -0.30% 07/07 Germany BMWi Industrial Production WDA YoY May 1.30% 3.60% 1.30% 07/07 UK Lloyds Bank Lloyds Employment Confidence June 1.0 – 4.0 07/07 Spain INE Industrial Output NSA YoY May 0.40% – -2.10% 07/07 Spain INE Industrial Output SA YoY May 2.50% 3.70% 4.10% 07/07 Japan Ministry of Finance Official Reserve Assets June $1283.9B – $1283.9B 07/07 Japan ESRI Leading Index CI May 105.7 105.9 106.5 07/07 Japan ESRI Coincident Index May 111.1 111 111.1 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar QNBFS: Mixed outlook for 2Q2014 earnings of Qatari stocks under coverage – QNB Financial Services (QNBFS) expects the 2Q2014 earnings for Qatari stocks under coverage to have a mixed outlook. Despite showing a modest sequential growth in aggregate net income, several companies are expected to experience bottom-line volatility in 2Q2014. On the positive front, Industries Qatar (IQCD), Qatar Electricity & Water (QEWS) and Gulf International Services (GISS) will positively contribute toward the 2Q2014 aggregate bottom-line. However, the seasonal nature of some companies’ businesses, lack of dividend income, lower investment income from debt securities for banks, etc. could restrict the earnings growth of several companies. Looking ahead, QNBFS’ annual estimates remain robust and it expects a 9.2% YoY bottom-line growth in 2014, followed by 11.1% and 11.5% in 2015 and 2016, respectively. In terms of equity performance, post the significant volatility already witnessed in the market, QNBFS expects a more measured rally in the remainder of 2014 – Qatar is already part of the MSCI Emerging Markets Index and is expected to benefit from a similar upgrade by S&P Dow Jones later in 2014. QNBFS is also of the view that foreign institutional (FI) activities will be key to market performance. So far YTD, FI investors have already pumped in $1.87bn as compared to ~$700mn in net equity buying in 2013 (an outflow of roughly $900mn in 2012). QNBFS’ long-term (beyond 2014) positive outlook for the Qatari equity market remains unchanged. QNBFS said that its view is based on robust top-down fundamentals with real GDP expected to be up by an average of 7.7% in 2015-16 (after an estimated growth of 6.8% in 2014), significant infrastructure spending of roughly $30bn earmarked for major projects annually over 2014-16, strong earnings growth with stocks under coverage expected to grow earnings per share (EPS) by low double-digits in 2015 and 2016, and newsflow catalysts Overall Activity Buy %* Sell %* Net (QR) Qatari 55.28% 66.81% (30,158,003.04) Non-Qatari 44.72% 33.19% 30,158,003.04

- 3. Page 3 of 7 concerning major project mobilizations. However, QNBFS cautioned that estimates can be impacted by one-off events, greater or lower provisions for banks and investment income/capital gains. (Gulf-Times.com) Qatari mobile subscribers’ growth slows down – Mobile subscribers’ growth rate in Qatar eased down from previous quarter, increasing by 2.8% QoQ in 1Q2014. In 4Q2013, the growth rate was up by 3.5% as compared to 3Q2013. Despite high penetration rate of around 192%, the growth potential continues to be backed by expected economic and population growth. Global Research Institute said in its latest GCC Telecom Sector Quarterly Review report that population growth is seen to exceed average GCC growth due to foreign workforce requirement. Ooredoo (ORDS) recorded an increase of 57,900 subscribers in 1Q2014 as compared to 44,400 in 4Q2013. Vodafone Qatar (VFQS) subscribers increased by 47,000 in 1Q2014, after the company saw a rise of 85,000 in the previous quarter — the largest increase since 2010. The report said that Vodafone increased its market share to 33.8% in 1Q2014. (Peninsula Qatar) Al Wakrah Mall to open in Dec 2014 – Local daily Al Arab has reported that the Ezdan Al Wakrah Mall will open in December 2014, quoting Ali bin Mohamed al-Obaidli, Group CEO, Ezdan Holding. Al-Obaidli said that the mall will feature a number of global brands and be the first of its kind in Al Wakrah, which has been witnessing rapid growth in its population. He added that the mall will cover an area of 75,600 square meters. (Gulf- Times.com) QIMD to disclose results on July 22 – Qatar Industrial Manufacturing Company (QIMD) will disclose its financial reports for the period ending June 30, 2014, on July 22, 2014. (QE) ERES to announce results on July 22 – Ezdan Holding Group (ERES) will disclose its financial reports for the period ending June 30, 2014, on July 22, 2014. (QE) QISI to announce results on July 23 – Qatar Islamic Insurance Company (QISI) will disclose its financial reports for the period ending June 30, 2014, on July 23, 2014. (QE) UDCD to disclose results on July 23 – United Development Company (UDCD) will disclose its financial reports for the period ending June 30, 2014, on July 23, 2014. (QE) International Central banks ending era of clear promises, return to 'artful' policy – The world's major central banks are returning to a more opaque and artful approach to policymaking, ending a crisis-era experiment with explicit promises that they found risked their credibility and did not substitute for action. From Washington to London to Tokyo, the global shift from transparency to flexibility underscores the challenges central bankers face as they test the limits of what monetary policy can achieve. The return to a more traditional policymaking approach and nuanced statements will challenge the communication skills of central bankers, who have been chastened in the last year after some too-specific messages confused and disrupted the financial markets. Complicating things on the world stage, the US Federal Reserve and the Bank of England are looking to telegraph plans and conditions for raising interest rates, while the European Central Bank and the Bank of Japan are heading the other way. A senior G7 central bank official said central banking used to be an art and became less so once, globally, but with what's happened at the Fed and the BoE, it may be back to being an art. (Reuters) BCC: UK economy growing solidly but exports and investment slip – The British Chambers of Commerce's (BCC) survey showed Britain's economy kept growing at a robust rate in the second quarter, but exports and business investment weakened, clouding the prospects for a balanced recovery. BCC’ quarterly survey of nearly 7,000 companies showed most of its key measures for manufacturing and services companies fell in the second quarter of 2014, albeit from the strong levels at the start of 2014. Manufacturers reported the biggest rise in domestic sales since the survey started in 1989, although growth cooled in the services companies that comprise the bulk of the economy. While the survey was broadly positive, it suggested the long-awaited rebalancing of Britain's economy, reviving the part played by manufacturing might not be progressing as quickly as hoped. That may cause concern for Bank of England and government policymakers. (Reuters) German industrial output posts surprise slump in May – Germany's industrial output fell 1.8% in the month of May, its biggest drop in more than two years, as holiday days ate into working hours, construction slumped and geopolitics weighed, casting a shadow on its role as Eurozone motor. The drop was a surprise and sent the Euro weaker - the consensus forecast in a Reuters poll was for industrial output to be unchanged. The economy ministry also slightly downwardly revised April data to - 0.3% from a previous -0.2%. The disappointing data added to mounting signs of a weaker second quarter in Europe's largest economy, after it enjoyed a quarterly growth of 0.8% in the first three months of 2014, its fastest growth rate in three years. The figures also fanned expectations that the European Central Bank (ECB) may have to further loosen monetary policy in coming months in the face of disinflationary pressures and subdued growth. (Reuters) Greek central banker warns political risks could threaten recovery – Greece's newly-appointed central bank chief said that the political uncertainty around a presidential election scheduled for 2015 is the main risk to the debt-laden country's economic recovery. Yannis Stournaras, the former finance minister, reiterated that he expected a moderate growth of about 0.5% of GDP this year, but in his first comments on politics since taking over as central bank governor last month said there were still downside risks to the economic outlook. Stournaras added that the main risks are due to political uncertainty, related to the election of a new president in early 2015. He stated that other challenges included a slowdown in the global economy and geopolitical risks in Russia & Ukraine, which could hurt exports. Bailed out twice by the European Union and International Monetary Fund, Greece relies on loans from its foreign creditors to stay afloat, in exchange for austerity measures that have pushed unemployment to record levels and deepened a six-year recession. (Reuters) Japan’s current-account surplus beats economist estimates; Exporters cannot rely on weaker yen – Japan posted a fourth straight current-account surplus in May, as income from overseas investments outweighed a trade deficit. The excess in the widest measure of trade was 522.8bn Yen. This compared with the median forecast of 417.5bn yen in a Bloomberg News survey of 28 economists. Imports fell for the first time in 19 months, as consumers cut spending after a sales- tax increase in April, while exports remained sluggish, highlighting how manufacturers cannot rely on the Yen’s slide against the dollar for support. Prime Minister Shinzo Abe’s task is to steer the world’s third-largest economy through the aftermath of the levy increase. Meanwhile, according to economists led by Mary Amiti of the Federal Reserve Bank of New York, Japanese exporters looking to boost shipments after

- 4. Page 4 of 7 the first monthly decline in more than a year cannot rely on a weaker Yen for support. While depreciation typically favors exporters, a decline in the Yen would boost the cost of the fuel imports needed by Japanese companies to manufacture products. (Bloomberg) Li Keqiang: China second-quarter growth better, more policy steps ahead – Premier Li Keqiang said China's economic growth quickened in the second quarter from the previous three months, but felt that modest government support measures will still be needed. Speaking at a news conference with German Chancellor Angela Merkel, who is visiting Beijing, Li said the Chinese economy still faces downward pressure and that the government will increase its usage of targeted measures to boost growth. His cautiously optimistic remarks may boost market confidence ahead of China's second-quarter economic report due on July 16. Analysts polled by Reuters expect China's growth for the April-June period to have steadied at 7.4%. In order to lift China's flagging economic growth, which hit an 18-month low of 7.4% in the first quarter of 2014, authorities have cut taxes, ordered regional governments to speed up spending and reduced the amount of cash that some banks have to hold as reserves. Use of these so-called "targeted measures" are meant to help areas of the economy with real business needs, and is a departure from the past when China would cut rates or reserve requirements for all banks and ramp up spending across the country. (Reuters) Regional GPCA: GCC fertilizer industry growth twice the global average – The Gulf Petrochemicals & Chemicals Association (GPCA) said that the fertilizer industry in the GCC region is growing twice as fast as the global industry average, led by the increased investments from petrochemical producers. According to GPCA estimates, GCC’s fertilizer production capacity reached 42.7mn tons in 2013, reflecting a 4% increase from the previous year, while the global fertilizer industry grew by just 1.7% over the same period. The capacity growth was achieved with several multi-million dollar projects in Saudi Arabia, Qatar and the UAE coming on stream. Chairman of the GPCA’s Fertiliser Committee and Qatar Fertiliser Company’s (QAFCO) CEO, Khalifa al-Sowaidi said that GCC producers exported 20mn tons of fertilizer products to more than 80 countries worldwide in 2013. The GCC industry accounted for approximately one- quarter of global urea trade and represented 12% of the global ammonia trade volume in 2013. With double-digit capacity growth over the last five years, the GCC industry has demonstrated its potential to be a major global player. (Gulf- Times.com) Saudi gas development plans hit hurdle as Shell shelves project – Royal Dutch Shell is ending investments in a gas development project in Saudi Arabia, complicating the top oil exporter's efforts to exploit its huge gas reserves. Shell did not give a reason for the decision to shelve the joint venture in the Kidan area of the Empty Quarter, the sea of sand dunes that cover south-east Saudi Arabia. At least three foreign firms - Italy's ENI, Spain's Repsol and France's Total - have already abandoned the search for commercially viable gas deposits in that part of Saudi Arabia. The search for gas has been a priority for Saudi Arabia as it struggles to keep pace with rapidly rising domestic demand. But the emergence of the shale gas industry has opened up more lucrative opportunities for energy companies elsewhere. (Reuters) Moody's affirms MQ2 assessment of Jadwa Asset Management – Moody's Investors Service has affirmed the MQ2 Investment Manager Quality (MQ) assessment of Jadwa Asset Management, a division of Saudi Arabian investment bank Jadwa Investment. The firm has managed to continue growing its assets under management (AUM) in 1H2014, deliver fund performance above their relative benchmarks and achieve a solid financial performance despite the number of recent organizational changes. (GulfBase.com) Saudi invites bids for $16.5bn Makkah metro project – Saudi Arabia has invited bids for the $16.5bn Makkah Metro project, which involves construction of 88 train stations, including 22 underground depots, which will be fully operational in 2020. A total of 10 consortiums are competing for the first phase of the project involving civil works. The contract will be signed in early October 2014. The project would be launched in mid-2015 and would be operated on a trial basis in 2017 before it is fully commissioned at the start of 2020. (GulfBase.com) Maaden announces opening of nominations for Bod membership – Saudi Arabian Mining Company (Maaden) has made an announcement to its shareholders about the opening of nomination for board of directors’ membership for the coming term, which will start from October 25, 2014 for a three-year period. Interested applicants of Maadens shareholders, who are qualified and possess shares in Maaden with nominal value not less than SR10,000 (equal 1000 shares), should apply for nomination to the company’s nominations and remuneration committee. (Tadawul) Riyad Bank reports SR1.14bn net profit in 2Q2014 – Riyad Bank reported a net profit of SR1.14bn in 2Q2014 as compared to SR968mn in 2Q2013, with profit surging 17.36% on a YoY basis due to higher operating income. The bank’s net profit for 1H2014 stood at SR2.22bn as compared to SR1.92bn for 1H2013, up by 15.48%. EPS as of June 30, 2014 amounted to SR0.74 as against SR0.64 a year earlier. The bank’s total assets stood at SR214bn at the end of June 2014 as against SR191.6bn a year ago. Loans & advances stood at SR140.77bn, while customer deposits stood at SR160.1bn. (Tadawul) BSF reports SR884mn net profit in 2Q2014 – Banque Saudi Fransi (BSF) reported a net profit of SR884mn in 2Q2014 as compared to SR763mn in 2Q2013, with profit surging 15.86% on a YoY basis. The bank’s net profit for 1H2014 stood at 1.74bn as compared to SR1.45bn for 1H2013, up by 20.33%. EPS as of June 30, 2014 amounted to SR1.44 as against SR1.2 a year earlier. The bank’s total assets stood at SR184.3bn at the end of June 2014 as against SR165.8bn a year ago. Loans & advances stood at SR117.4bn, while customer deposits stood at SR134.4bn. (Tadawul) Tadawul deposits Herfy’s bonus shares – The Saudi Stock Exchange (Tadawul) announced that Herfy Food Services Company’s (Herfy) bonus shares have been deposited into the investor’s portfolios. Earlier, Herfy’s EGM had approved an increase in the bank's capital via bonus shares. The fluctuation limit of the company's shares on July 7, 2014 will be based on a stock price of SR105.22. (Tadawul) IDB’s infrastructure fund seeks to build regional links – The Islamic Development Bank’s (IDB) new infrastructure fund aims to help Gulf-based companies expand in Asia and Africa, developing stronger economic ties among these regions. The fund could jump-start sluggish levels of trade across these markets, helping the IDB in its efforts to reach a target of 20% of intra-member trade by 2015 from about 17% now. IDB is keen to grow trade among its 56 member countries and fill a void left by other multilateral and private-sector financial institutions that have been slow to support such regional strategies. (Reuters)

- 5. Page 5 of 7 IFC to invest up to $100mn in ACWA Power for renewable energy schemes – The World Bank’s unit, International Finance Corp (IFC), will invest up to $100mn in Saudi-based water and power project developer, ACWA Power, to boost its funding for renewable energy schemes. The investment will focus on expanding the amount of power generated in the MENA region through green methods, as energy demand in the region increases rapidly. The IFC is joining Sanabil al-Saudia and the Public Pension Agency in taking an equity stake in ACWA. (Reuters) UAE to mull rule changes after reviewing June market turmoil – The Securities & Commodities Authority said that the UAE may amend rules governing bank lending against shares after reviewing June’s stock price swings in Dubai and Abu Dhabi. Representatives of the Securities & Commodities Authority, the central bank and the country’s two main stock exchanges met in Abu Dhabi to consider the volatility, and will make changes to lending regulations if necessary. The parties also agreed to set up a joint permanent committee to monitor trades and ensure the absence of any suspicion of manipulation of securities’ price. (Bloomberg) ENOC secures permission to operate fuel stations in Saudi Arabia – Emirates National Oil Company (ENOC) has won the right to operate additional fuel stations in Saudi Arabia, along highways and roads amid the Kingdom’s ambitious infrastructure upgrade plans. (GulfBase.com) Mashreq becomes first UAE bank to secure IIA accreditation – Mashreq Bank’s internal audit function has been assessed to be in conformance with The Institute of Internal Auditors’s (IIA) international standards for the professional practice of internal auditing. The IIA, USA concluded an External Quality Assessment of the internal audit activities at Mashreq Bank. Upon conclusion of the assessment, IIA Executives advised that Mashreq was the first bank in the UAE to achieve conformance with the standards. (GulfBase.com) Emirates NBD becomes global leader in arranging USD Sukuk – Emirates NBD Investment Bank is ranked as the leading arranger of USD Sukuk globally. According to league tables published by Bloomberg, from January 2014 to June 2014, Emirates NBD Investment Bank arranged 10 USD Sukuk issuances aggregating to $5.4bn, which is the highest number of USD Sukuk issuances led by any arranger during this period. (GulfBase.com) DSI wins AED103mn contracts for constructing wastewater treatment plants in India – Drake & Scull International’s (DSI) German subsidiary, Passavant Energy & Environment, has won two contracts worth AED103mn for the construction and operation of two wastewater treatment plants in India. The new contracts are for the Amritsar Sewerage Project in Punjab. The scope of work includes design & construction, including installing, testing, commissioning and five-year operation of two sewage treatment plants each with a capacity of 95mn liters per day (MLD) based on the activated sludge treatment process in North and South Zones of Amritsar, Punjab. (DFM) Damac Properties receives Green Building Certification – Damac Properties has become the first company to receive a Green Building Certification from the Department of Planning & Development, Trakhees. Trakhees, the department for Planning & Development, a Dubai-based local regulatory authority and the first to undertake local certification, bestowed the honor on the NAIA at Suburbia Jebel Ali hotel apartments, which will open later in 2014. The project demonstrated its compliance to environment, health & safety (EHS) sustainability criteria for the built environment, and became the first project to be certified green under the scheme. NAIA at Suburbia Jebel Ali is a two- tower luxury furnished serviced apartment development adjacent to the Jebel Ali Port. (GulfBase.com) Jebeli Ali Port wins best seaport – Middle East award – DP World’s flagship Jebel Ali Port has been voted the “Best Seaport – Middle East” for the 20th consecutive year. The award was given at the Asian Freight and Supply Chain Awards. It is decided by decision makers in the industry. (GulfBase.com) Dubai Cranes unveils new crane storage & assembly facility at DIP – Dubai Investments’ (DIC) subsidiary, Dubai Cranes & Technical Services, has announced the opening of the first-of- its-kind crane storage and assembly facility in the region, which will significantly reduce the delivery time for standard cranes across the GCC & MENA region and lead to massive savings in cost & time for clients and partners. With the new facility within the Dubai Investments Park (DIP), Dubai Cranes can now deliver standard cranes for projects across GCC and MENA within four weeks as compared to the average turnaround period of 16 weeks. The new facility will stock over 50 standard overhead crane kits from the Street ZX and LX product range offering various lifting capacities and will be able to accommodate crane spans of up to 20 meters. Apart from storage, the facility offers fabrication services for crane beams, gantries and other structural crane parts as well as spare parts for both the company’s cranes as well as for competitor crane companies. (DFM) DMCC considers new agricultural contracts, delays launch of spot gold contract – The Dubai Multi Commodities Center (DMCC) CEO, Gautam Sashittal, said that DMCC will delay the launch of a spot gold contract to 3Q2014 to ensure that the technical aspects run smoothly. The contract will cover 1 kg (32 troy ounces) of 0.995 purity gold. Further, Dubai is looking into the possible launch of contracts in several agricultural commodities in the near future, including the possibility of one for black pepper. (Reuters) SMT bags contract to supply aluminum rod system for Dubai Cable Company – US-based Southwire Company has awarded an order to Germany-based Siemens Metals Technologies (SMT) to supply an aluminum rod system for Dubai Cable Company. SMT will be responsible for engineering, manufacturing and commissioning equipment for a rolling mill manufactured by Southwire in Abu Dhabi. (Bloomberg) ADIA sells shares worth 4.21bn Indian Rupees in India- based Kotak Mahindra Bank – Abu Dhabi Investment Authority (ADIA) has sold 4.21bn Indian Rupees worth of shares in India's Kotak Mahindra Bank in stock market deals on July 7, 2014. ADIA sold about 4.8mn shares at 874.55 Indian Rupees a piece, according to data from the Bombay Stock Exchange (BSE). (Reuters) CBK gets approval to raise up to KD120mn via bonds – Commercial Bank of Kuwait (CBK) has received regulatory approval to issue up to KD120mn of bonds, as it prepares to convert into an Islamic bank. The bonds will comply with Basel- III rules, which are being phased in around the world over the next several years. CBK is not the first to convert into an Islamic bank, with Boubyan and Al Ahli having done so previously, but this is becoming more attractive as the industry's growth continues to outpace that of their conventional peers. (Reuters) DGCA: KIA travelers and flights up in June 2014 – According to Directorate General of Civil Aviation (DGCA), the number of travelers and flights at Kuwait International Airport (KIA) increased by 7% and 2% respectively in June 2014 as

- 6. Page 6 of 7 compared to June 2013. The airport received a total number of 934,000 passengers in June 2014. The DGCA added that there were 7,588 flights, including 7,048 commercial flights. The airport’s air shipping increased by 11% in June 2014 as compared to June 2013. The total weights of shipments reached 16.6mn kilograms in June 2014. (Bloomberg) Warba arranges $155mn loan for leading UAE-based oil firm – Kuwait-based Warba Bank announced that they have successfully arranged a $155mn syndicated financing facility for a leading UAE-based Oil Services Company incorporated in 2006. Warba Bank participated with a stake of $25mn in this transaction along with Noor Bank and Qatar Islamic Bank (QIBK). The Obligor oilfield services company serves the entire MENA region. The company offers a complete range of oilfield services and has appropriate infrastructure to cater to multinational oil & gas exploration and drilling companies (MNOCs). (AmeInfo.com) Bank Sohar wins three CPI Financial awards – Bank Sohar has won three awards from the Banker Middle East Product Awards 2014 organized by CPI Financial. Bank Sohar was recognized as the bank with the ‘Best Customer Service — Retail Banking’ ‘Best Cash Management’ and ‘Best Corporate Card’. (GulfBase.com) CBO: Omani crude exports to China reached 180.8mn barrels in 2013 – According to a report released by the Central Bank of Oman (CBO), China has remained the dominant importer of Omani crude for over ten consecutive years, lifting as much as 60% of the Sultanate’s total crude oil exports in 2013. The bilateral trade has surged to an unprecedented $23bn in value in 2013. Volumes jumped from 77.6mn barrels in 2009 (representing 31% of its total exports) to 180.8mn barrels of Omani crude, amounting to 59.4% of the Sultanate’s total crude exports of 304.2mn barrels, in 2013. Japan stood at second place lifting 29.3mn barrels of Omani crude in 2013, down from 38.2mn barrels in 2012. Taiwan, with 27.4mn barrels, was the next most significant importer, with Thailand (17.1mn barrels) and Singapore (13.5mn barrels) being placed fourth and fifth respectively. Exports to India climbed to 13.2mn barrels, up from 5.2mn barrels in 2012. (GulfBase.com) NCSI: Tourism arrivals show steady growth in Oman – According to the figures released by the National Center for Statistics and Information (NCSI), visitors staying at Oman’s four and five-star hotels grew by 23.8% in the first four months of 2014, as compared to the year-ago period. Occupancy rates at the four and five-star hotels reached 71.6% in April from 66.9% a year earlier. Hotels’ revenue was up 10.5% in April, with overall revenue reaching OMR65.9mn, as compared to OMR59.7mn a year ago. Meanwhile, the passenger traffic at the Muscat International Airport was up 8% to 3.6mn passengers in the first five months of 2014, as compared to 3.4mn a year earlier. (GulfBase.com) Investcorp appoints four new Corporate Investment Advisory Directors – Bahrain-based Investcorp has appointed four new Corporate Investment Advisory Directors in Europe. The firm has appointed Brendan Harris, Joan Julia Dinares, Guy Leymarie and Philip Walters. Investcorp’s Advisory Directors in Europe provide senior external counsel to Investcorp, helping to assess potential investment opportunities and supporting portfolio company management, and consists of distinguished corporate executives who are highly successful in their respective fields. (Bahrain Bourse) Bahrain sends RFP ahead of potential Eurobond issue – Bahrain has send out request for proposals (RFP) to banks ahead of a potential Eurobond issuance. The sovereign plans to issue the note through its central bank. Earlier, in July 2013, Bahrain was last in the market when it issued a $1.5bn 6.125% 10-year note. The timing of the deal will be September at the earliest. (Reuters)

- 7. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg (* Market closed on July 07 2014) Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 QE Index S&P Pan Arab S&P GCC 0.4% 0.4% (0.2%) 0.2% 0.7% 0.3% (0.8%) (1.2%) (0.8%) (0.4%) 0.0% 0.4% 0.8% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,319.94 (0.0) (0.0) 9.5 DJ Industrial 17,024.21 (0.3) (0.3) 2.7 Silver/Ounce 21.05 (0.6) (0.6) 8.1 S&P 500 1,977.65 (0.4) (0.4) 7.0 Crude Oil (Brent)/Barrel (FM Future) 110.24 (0.4) (0.4) (0.5) NASDAQ 100 4,451.53 (0.8) (0.8) 6.6 Natural Gas (Henry Hub)/MMBtu 4.25 (0.9) (0.9) (2.1) STOXX 600 344.80 (0.9) (0.9) 5.0 LPG Propane (Arab Gulf)/Ton* 103.88 0.0 0.0 (17.9) DAX 9,906.07 (1.0) (1.0) 3.7 LPG Butane (Arab Gulf)/Ton 123.75 (0.2) (0.2) (8.8) FTSE 100 6,823.51 (0.6) (0.6) 1.1 Euro 1.36 0.1 0.1 (1.0) CAC 40 4,405.76 (1.4) (1.4) 2.6 Yen 101.86 (0.2) (0.2) (3.3) Nikkei 15,379.44 (0.4) (0.4) (5.6) GBP 1.71 (0.2) (0.2) 3.4 MSCI EM 1,064.33 0.2 0.2 6.1 CHF 1.12 0.1 0.1 (0.1) SHANGHAI SE Composite 2,059.93 0.0 0.0 (2.6) AUD 0.94 0.1 0.1 5.1 HANG SENG 23,540.92 (0.0) (0.0) 1.0 USD Index 80.22 (0.1) (0.1) 0.2 BSE SENSEX 26,100.08 0.5 0.5 23.3 RUB 34.43 (0.1) (0.1) 4.8 Bovespa 53,801.83 (0.5) (0.5) 4.5 BRL 0.45 (0.4) (0.4) 6.4 RTS 1,385.24 1.8 1.8 (4.0) 177.9 151.7 137.5