Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (20)

Similar a Draghinomics Introduces Quantitative Easing to the Eurozone

Similar a Draghinomics Introduces Quantitative Easing to the Eurozone (20)

Más de QNB Group

Más de QNB Group (20)

Último

Último (20)

Draghinomics Introduces Quantitative Easing to the Eurozone

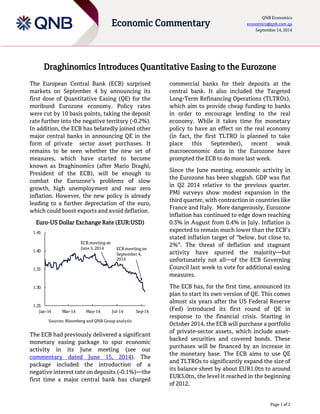

- 1. Page 1 of 2 Economic Commentary QNB Economics economics@qnb.com.qa September 14, 2014 Draghinomics Introduces Quantitative Easing to the Eurozone The European Central Bank (ECB) surprised markets on September 4 by announcing its first dose of Quantitative Easing (QE) for the moribund Eurozone economy. Policy rates were cut by 10 basis points, taking the deposit rate further into the negative territory (-0.2%). In addition, the ECB has belatedly joined other major central banks in announcing QE in the form of private sector asset purchases. It remains to be seen whether the new set of measures, which have started to become known as Draghinomics (after Mario Draghi, President of the ECB), will be enough to combat the Eurozone’s problems of slow growth, high unemployment and near zero inflation. However, the new policy is already leading to a further depreciation of the euro, which could boost exports and avoid deflation. Euro-US Dollar Exchange Rate (EUR:USD) Sources: Bloomberg and QNB Group analysis The ECB had previously delivered a significant monetary easing package to spur economic activity in its June meeting (see our commentary dated June 15, 2014). The package included the introduction of a negative interest rate on deposits (-0.1%)—the first time a major central bank has charged commercial banks for their deposits at the central bank. It also included the Targeted Long-Term Refinancing Operations (TLTROs), which aim to provide cheap funding to banks in order to encourage lending to the real economy. While it takes time for monetary policy to have an effect on the real economy (in fact, the first TLTRO is planned to take place this September), recent weak macroeconomic data in the Eurozone have prompted the ECB to do more last week. Since the June meeting, economic activity in the Eurozone has been sluggish. GDP was flat in Q2 2014 relative to the previous quarter. PMI surveys show modest expansion in the third quarter, with contraction in countries like France and Italy. More dangerously, Eurozone inflation has continued to edge down reaching 0.3% in August from 0.4% in July. Inflation is expected to remain much lower than the ECB’s stated inflation target of “below, but close to, 2%”. The threat of deflation and stagnant activity have spurred the majority—but unfortunately not all—of the ECB Governing Council last week to vote for additional easing measures. The ECB has, for the first time, announced its plan to start its own version of QE. This comes almost six years after the US Federal Reserve (Fed) introduced its first round of QE in response to the financial crisis. Starting in October 2014, the ECB will purchase a portfolio of private-sector assets, which include asset- backed securities and covered bonds. These purchases will be financed by an increase in the monetary base. The ECB aims to use QE and TLTROs to significantly expand the size of its balance sheet by about EUR1.0tn to around EUR3.0tn, the level it reached in the beginning of 2012. 1.251.301.351.401.45Jan-14Mar-14May-14Jul-14Sep-14ECB meetingon June 5, 2014ECB meetingon September 4, 2014

- 2. Page 2 of 2 Economic Commentary QNB Economics economics@qnb.com.qa September 14, 2014 Such large expansion in the balance sheet could have a significant impact on the euro. In contrast with long-term movements in currencies, which are determined by economic fundamentals such as the current account balance and productivity, short-term movements tend to be dominated by interest rate differentials. As investors borrow funds from low-interest rate countries and invest them in high-interest rate one (the so-called carry trade), the resulting portfolio flow causes high-yielding currencies to appreciate. The financial crisis of 2008 has resulted in short-term interest rates falling to near zero in most advanced economies. So carry traders have focused instead on the relative size of the major central banks’ balance sheets as an alternative measure of monetary conditions. For example, the difference in the growth rates of the Fed versus the ECB balance sheet has become an important driver of the EUR:USD exchange rate. If the growth rate in the Fed balance sheet is larger than the ECB’s (as has been the case since the second half of 2012), carry traders interpret this as a tightening in the monetary conditions in the Eurozone relative to the US. As a result, the euro will appreciate against the US dollar, as it did during that time. What does this imply going forward? The Fed is expected to end its asset purchases program in October 2014 and the Fed’s balance sheet is then likely to plateau at around USD4.5tn. Fed vs. ECB Balance Sheet Growth and EUR:USD % Change Sources: ECB, Eurostat, Federal Reserve Board and QNB Group analysis and forecasts Meanwhile, the ECB wants to expand the size of its balance sheet to about EUR3.0tn. If, as in the recent past, the movement in EUR:USD exchange rate is mostly determined by the relative growth of the central banks’ balance sheets, this would result in a depreciation of the EUR:USD to around 1.25 in the coming months. Fundamentals, including the Eurozone’s large current account surplus, are likely to have an impact on the exchange rate as well. Overall, Draghinomics may help the Eurozone to recover and avoid deflation. Its new flagship scheme, a private-sector QE program, may have come later than other major central banks, but better late than never. Contacts Joannes Mongardini Head of Economics Tel. (+974) 4453-4412 Rory Fyfe Senior Economist Tel. (+974) 4453-4643 Ehsan Khoman Economist Tel. (+974) 4453-4423 Hamda Al-Thani Economist Tel. (+974) 4453-4646 Ziad Daoud Economist Tel. (+974) 4453-4642 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group. -80 -60 -40 -20 0 20 40 60 80 -20 -15 -10 -5 0 5 10 15 20 2010 2011 2012 2013 2014 2015 2016 EUR:USD (YoY % Change, LHS) Growth Difference in Fed vs ECB Balance Sheet (%, RHS) Forecast