Econ 210 Term Project - Winter 2016

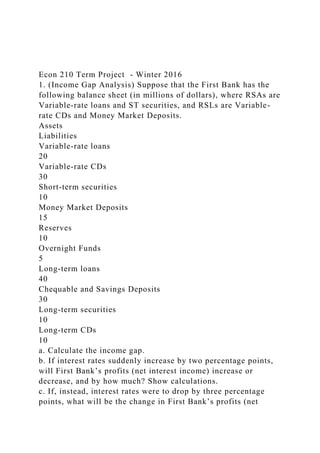

1. (Income Gap Analysis) Suppose that the First Bank has the following balance sheet (in millions of dollars), where RSAs are Variable-rate loans and ST securities, and RSLs are Variable-rate CDs and Money Market Deposits.

Assets

Liabilities

Variable-rate loans

20

Variable-rate CDs

30

Short-term securities

10

Money Market Deposits

15

Reserves

10

Overnight Funds

5

Long-term loans

40

Chequable and Savings Deposits

30

Long-term securities

10

Long-term CDs

10

a. Calculate the income gap.

b. If interest rates suddenly increase by two percentage points, will First Bank’s profits (net interest income) increase or decrease, and by how much? Show calculations.

c. If, instead, interest rates were to drop by three percentage points, what will be the change in First Bank’s profits (net interest income)? Show calculations.

d. Repeat parts b and c to calculate the changes in interest rate margin in each case.

e. Suppose the bank decides to convert $25mln of its variable CDs to long-term CDs. How would an increase of interest rates by 2% affect on the interest margin and income in this case? Would this increase or decrease interest rate risk? Explain! Show calculations.

Assets

Liabilities

2. The average duration of the assets and the liabilities are 1.16 and 2.77, respectively, for XYZ Company. Assuming they cannot do anything to the average duration of the liabilities, how (calculate the new value for average duration of assets) can they alter the average duration assets to ensure that any fluctuation of interest rates does not affect the value of net worth as a percentage of assets? Show all calculations.

3. (Duration Gap Analysis) XYZ Bank has total asset value of $200 million, and total liability value of $180 million. The average duration of assets is 2.5, and the average duration of liabilities is 1.1.

a. What is the duration gap for XYZ bank?

b. What is the change in the market value of net worth as a percentage of assets if interest rates fall from 6% to 5%? Show calculations.

c. Would you get the same results if you were to calculate the change in the market value of the assets (%ΔPA) and liabilities (%Pll.)? Show calculations.4. (Open Market Operations) One of the ways the Bank of Canada exercises control over the monetary base is through its purchases and sales of government securities in the open market, called open market operations.

a) How will a Bank of Canada sale of $100 of government bonds to the nonblank public affect the monetary base and reserves if the nonblank public pays for the bonds with cheques? Fill in the following T-accounts in arriving at your answer. Clearly mention what asset and/or liability item will be affected, the direction of the change ((+) or (-)) and the dollar amount of the change.

Nonbank Public

Assets

LiabilitiesBanking System

Assets

LiabilitiesThe Bank of Canada

Assets

LiabilitiesChange in monetary base = --------------$ Change in reserves = - ...

Econ 210 Term Project - Winter 20161. (Income Gap Analysis) S.docx

1. Econ 210 Term Project - Winter 2016

1. (Income Gap Analysis) Suppose that the First Bank has the

following balance sheet (in millions of dollars), where RSAs are

Variable-rate loans and ST securities, and RSLs are Variable-

rate CDs and Money Market Deposits.

Assets

Liabilities

Variable-rate loans

20

Variable-rate CDs

30

Short-term securities

10

Money Market Deposits

15

Reserves

10

Overnight Funds

5

Long-term loans

40

Chequable and Savings Deposits

30

Long-term securities

10

Long-term CDs

10

a. Calculate the income gap.

b. If interest rates suddenly increase by two percentage points,

will First Bank’s profits (net interest income) increase or

decrease, and by how much? Show calculations.

c. If, instead, interest rates were to drop by three percentage

points, what will be the change in First Bank’s profits (net

2. interest income)? Show calculations.

d. Repeat parts b and c to calculate the changes in interest rate

margin in each case.

e. Suppose the bank decides to convert $25mln of its variable

CDs to long-term CDs. How would an increase of interest rates

by 2% affect on the interest margin and income in this case?

Would this increase or decrease interest rate risk? Explain!

Show calculations.

Assets

Liabilities

2. The average duration of the assets and the liabilities are 1.16

and 2.77, respectively, for XYZ Company. Assuming they

cannot do anything to the average duration of the liabilities,

how (calculate the new value for average duration of assets) can

they alter the average duration assets to ensure that any

fluctuation of interest rates does not affect the value of net

3. worth as a percentage of assets? Show all calculations.

3. (Duration Gap Analysis) XYZ Bank has total asset value of

$200 million, and total liability value of $180 million. The

average duration of assets is 2.5, and the average duration of

liabilities is 1.1.

a. What is the duration gap for XYZ bank?

b. What is the change in the market value of net worth as a

percentage of assets if interest rates fall from 6% to 5%? Show

calculations.

c. Would you get the same results if you were to calculate the

change in the market value of the assets (%ΔPA) and liabilities

(%Pll.)? Show calculations.4. (Open Market Operations) One of

the ways the Bank of Canada exercises control over the

monetary base is through its purchases and sales of government

securities in the open market, called open market operations.

a) How will a Bank of Canada sale of $100 of government

bonds to the nonblank public affect the monetary base and

reserves if the nonblank public pays for the bonds with

cheques? Fill in the following T-accounts in arriving at your

answer. Clearly mention what asset and/or liability item will be

affected, the direction of the change ((+) or (-)) and the dollar

amount of the change.

Nonbank Public

Assets

LiabilitiesBanking System

Assets

LiabilitiesThe Bank of Canada

Assets

LiabilitiesChange in monetary base = --------------$

Change in reserves = --------------$

b) How will a Bank of Canada sale of $100 of government

bonds to banks affect the monetary base and reserves? Fill in

the following T-accounts in arriving at your answer. Clearly

4. mention what asset and/or liability item will be affected, the

direction of the change ((+) or (-)) and the dollar amount of the

change. Follow the instructions provided in part a).Banking

System

Assets

LiabilitiesThe Bank of Canada

Assets

LiabilitiesChange in monetary base = --------------$ Change

in reserves = --------------$

c) How will a Bank of Canada sale of $100 of government

bonds to the nonbank public affect the monetary base and

reserves if the nonbank public pays for the bonds with

currency? Fill in the following T-accounts in arriving at your

answer. Follow the instructions provided in part a).

Nonbank Public

Assets

LiabilitiesThe Bank of Canada

Assets

LiabilitiesChange in monetary base = --------------$

Change in reserves = -------------

5.Spillover Effects of US Credit Crunch

The blame of the recent financial turmoil goes to the

phenomenon of “securitization”. Explain how this phenomenon

would create such a pandemic across the world.

(Hint: Refer to class discussion, watch the video posted under

content, do your diligent research (there are lots of documents

on this topic. Try to connect together the lack of financial

regulation to the eventual collapse of the system. For example,

try to explain how subprime lending could have happened, how

lenders packaged those assets (mortgages) with other assets and

sold to others, how banks’ assets lost value, what was the role

of low capital/asset ratio, how governments bailed big banks

out, why? Etc.)). Also incorporate mortgage backed securities,

collateralized debt obligations, credit default swaps, etc.

5. This is an essay question. There is no length requirement but

your discussion must be coherent enough to cover the main

concepts and facts we discussed in class.

6