Mixin Classes in Odoo 17 How to Extend Models Using Mixin Classes

Analysis ofAccounting.pptx

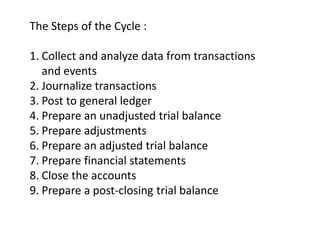

1. The Steps of the Cycle :

1. Collect and analyze data from transactions

and events

2. Journalize transactions

3. Post to general ledger

4. Prepare an unadjusted trial balance

5. Prepare adjustments

6. Prepare an adjusted trial balance

7. Prepare financial statements

8. Close the accounts

9. Prepare a post-closing trial balance

4. • General Ledger - is a labor saving device for the preparation of financial

statements and for establishing multiple income and cost entries

• Accounts Receivable - when computerized, can get your bills out the same

day you’ve performed a service. An accounts receivable module prepares

invoices and customer accounts, adds credit charges where appropriate,

handles incoming payments, flags your attention to customers that are

delinquent, and produces dunning notices.

• Accounts Payable - when computerized, will provide for purchase order

control, invoice processing, payment selection and handling, check writing

and control, cash-requirements, forecasting, and Form 1099 preparation

• Inventory Control - this module has multiple functions, including tracking

inventory for both costing and tax purposes, controlling purchasing (and

the overall level of expenditure) and minimizing the investment in

inventory (and subsequent loss of cash flow)

5. • Point of Sale - module captures all sales information at (or in place of) the cash

register, including salesperson, date, customer, credit information, items, and quantity

sold. It can produce sales slips or sales invoices, plus it reports on items, customer, and

salesperson activity.

• Purchasing and Receiving - module can represent an invaluable addition. It can

generate purchase orders and track their fulfillment. You can find out which vendors

are delivering on time and saving you the expense of having to follow up on partial

and incomplete orders.

6. Computerized processing systems

Accounting software: Once the initial journal entry is prepared, the data are merely being

manipulated to produce the ledger, trial balance, and financial statements.

How much does it cost:

Many companies produce accounting software. These packages range from the

simple to the complex. Some basic products for a small business may be purchased

for under $100. In large organizations, millions may be spent hiring consultants to

install large enterprise-wide packages. Recently, some software companies have

even offered accounting systems maintained on their own network, with the

customers utilizing the internet to enter data and produce their reports.

7. What do they look like: As you might expect, the look, feel, and function of software-based

packages varies significantly. Each company's product must be studied to understand its

unique attributes. But, in general, accounting software packages:

1. Attempt to simplify and automate data entry (e.g., a point-of-sale terminal may actually

become a data entry device so that sales are automatically "booked" into the

accounting system as they occur).

2. Frequently divide the accounting process into modules related to functional areas such

as sales/collection, purchasing/payment, and others.

3. Attempt to be "user-friendly" by providing data entry blanks that are easily understood

in relation to the underlying transactions.

4. Attempt to minimize key-stokes by using "pick lists," automatic call-up functions, and

auto-complete type technology.

5. Are built on data-base logic, allowing transaction data to be sorted and processed based

on any query structure (e.g., produce an income statement for July, provide a listing of

sales to Customer Smith, etc.)

6. Provide up-to-date data that may be accessed by key business decision makers.

7. Are capable of producing numerous specialized reports in addition to the key financial

statements.

8. Overview of Accounting Information

System

1. The Information Environment

2. Organizational Structure and Accounting

Information System

3. The Role of Accountants in Accounting

Information System

4. Task Performance and eLMS

T h e Information Environment

Organizational Structure and Accounting Information

S

y

s

t

e

m

T h e Role of Accountants in Accounting Information

System

T a s k Performance and eLMS

9. THE INFORMATION ENVIRONMENT

Operations

Personnel

Provide day-to-day

operations information

Directly responsible for day-

to-day operations

Middle

Management

Accountable for short-term

planning and coordination of

activities

Top Management

Responsible

for longer-

term

planning and

setting

organization

al objectives

Operat

ions

Management

Day-to-Day Operations Information

Stakeholders

Customers

Suppliers

BM190

8

10. Three (3) Fundamental Information Objectives

• Support the firm’s day-to-day operations.

• Support management decision-making.

• Support the stewardship function of management.

THE INFORMATION ENVIRONMENT

BM190

8

www.slidescarnival.com/help-use-presentation-

template

13. THE INFORMATION ENVIRONMENT

Sources of

Data

Data

Collection

Data

Processing

Information

Generation

External

End Users

Internal

End Users

Internal

Sources of

Data

Database

Management

The Information

System

BM190

8

Feedback

The Business

Organization

The

General

Model of

Accounting

Information

System

(AIESx)ternal

15. Part two:

The Flow of Information here is vertical since it flows from lower-level employees

(the average office employees) to high-level employees (top executives).

V

H

V

V

H

17. THE ROLE OF ACCOUNTANTS IN

ACCOUNTING INFORMATION

SYSTEM

Accountants as System Designers

Accountants as Systems Auditors

BM190

8

https://www.clipartmax.com/png/small/103-1036793_cartoon-businessman-thinking-thinking-business-man-png.png

18. TASK PERFORMANCE

Why is it structured that way?

Are those functional areas enough to meet

all the business requirements?

BM190

8

https://www.clipartmax.com/png/small/103-1036793_cartoon-businessman-thinking-thinking-business-man-png.png

Notas del editor

Assets

Assets in accounting are resources that a company owns and uses to generate income and future economic benefits. They can be classified as operating or nonoperating, tangible or intangible, and current or noncurrent.

Liabilities

Liabilities are amounts owed to other persons or entities as a result of a past event and involve a future settlement using cash, goods, or services. Customers and vendors can be sources of liabilities for operations. Paying taxes, fees, permits, and salaries are liabilities once they become due but aren’t yet paid. Businesses use their assets to pay liabilities.

Owner’s Equity

Owner’s equity is the residual interest or amount that assets exceed liabilities. It also represents the amount of paid-in capital and retained earnings as a result of doing business for profit