Understanding Discord NSFW Servers A Guide for Responsible Users.pdf

Toll Cross Industry Note: Uranium Update (July 24, 2013)

1.

Industry Research

24 July 2013

TOLL CROSS INDUSTRY NOTES:

Tom Hope, P. Eng

Tom.Hope@tollcross.ca 416.365.1960

URANIUM UPDATE

WHY IS THE SPOT PRICE DROPPING DESPITE THE

POSITIVE JAPAN UPPER HOUSE ELECTION RESULTS?

Current Prices

U3O8

*

Spot/lb

US$

36.50

U3O8

*

Term/lb

US$

57.00

U-T

Delta to

NAV

+6.5%

Recently there has been no shortage of positive news on the

demand side of the uranium industry. This past week Prime

Minister Shinzo -‐nuclear coalition government

308 spot

price has fallen to $36.50, its lowest price since early 2006.

Why are uranium spot prices continuing to fall, despite the

positive news?

Possible factors include unaccounted for selling in the

secondary market, such as if Japan is quietly selling its

contracted long-‐

inventory has grown to approximately 90M lbs. or a 5 year

supply compared with a 75M lbs. or 4.1 year supply prior to

2011. If ultimately 40 out of 50 reactors restart, an inventory

of less than 60 M lbs. would be adequate. But, Japanese utilities

have in place long term supply contracts for approximately 18

M lbs. per year from various sources. They also face financial

pressure to sell extra supplies from their need to buy costly

replacement hydrocarbon fuel.

We believe it is very possible that discrete and unreported

transactions are tak

trading houses. Who could be the lucky discount buyer? China

is an obvious candidate as it needs to grow its inventory to

ENTHUSIASM GROWS FOR EXPLORATION IN CANADA S

ATHABASCA REGION.

Despite the currently depressed uranium spot price, there is

continued faith in the forecasted supply deficit expected to

grow after 2020. Many are looking in the prolific Athabasca

basin for the new supplies needed to fill the projected gap. The

richest mines in the world are located in the northeastern part

of the basin, containing grades of up to 20% U3O8.

Now the focus has turned to the southeast corner, including

the area surrounding Patterson Lake, after Alpha Minerals

(TSXV:AMW) and Fission Uranium (TSXV:FCU) discovered

near surface high grade deposits. Patterson Lake is now

surrounded by claims and multiple companies are conducting

exploration work there.

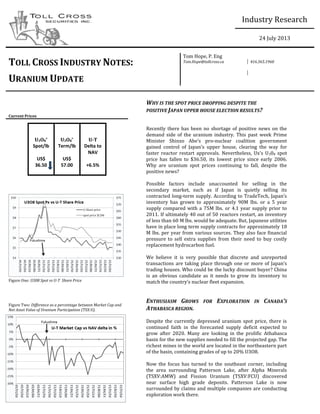

Figure One: U308 Spot vs U-T Share Price

Figure Two: Difference as a percentage between Market Cap and

Net Asset Value of Uranium Participation (TSX:U).

2.

Recently Skyharbour Resources (TSXV:SYH), Athabasca

Nuclear (TSXV:ASC), Lucky Strike Resources (TSXV:LKY) and

Noka Resources (TSXV:NX) signed a $6M joint exploration plan

on their southeastern Athabasca properties. Other properties

are owned by Nexgen Resources (TSXV:NXE), Aldrin Resources

(TSXV:ALN), Forum Minerals (TSXV:FDC) and Lakeland

Resources (TSXV:LK). Both UEX (TSX:UEX) and Cameco

(TSX:CCO) also have property in the area.

When we began publishing our Uranium Update in mid 2005

the spot and term price had risen to $29.50 per lb., from a

mere $10 per lb. in 2002/3. At that time we listed a total of 33

of 26 early exploration companies with the uranium spot at

$36.50 per lb. and a term price of $57 per lb. Obviously the

faithful still believe.

Please see important disclosures on the last page of this

report.

3.

* simple aggregate composite index, base point 1 Jan '13

Uranium Index & Price Performance - Period ending 23 July 2013

Production EquitiesIndex

Company Tick

YTD

Comp

Index 52 wk H 52 wk L

M arket Cap

(C$ M M )

(aggregate)

NAV

($MM)

M C

delta to

NAV

YTD %

Return

52 wk %

Return

Production Composite Index 110.84

Advanced Exploration Composite Index 96.09

Exploration, with a Resource Comp Index 61.72

Early Stage Exploration Comp Index 202.17

Uranium Participation U 5.29$ 5.80$ 4.69$ 562.6$ 528$ 6.49% -1.30 -6.327

Global X Uranium ETF URA-US 18.65$ 25.02$ 15.90$ 144.9$ -5.58 -14.153

U3O8 Spot Price ($US) Ux Sp 36.50$

U3O8 Long Term Price ($US) Ux Trm 57.00$

Production EquitiesIndex

Company Tick L. Px 52 wk H 52 wk L

M arket Cap

(C$ M M )

U3O8 NI

43-101

(lbs. MM) M C/lb$

YTD

Return

52 wk

Return

Cameco Corp. CCO 21.86$ 23.49$ 16.50$ 8,787.7$ 996.10 8.82$ 16.18 1.83

Paladin Energy PDN 1.07$ 1.52$ 0.75$ 782.2$ 500.18 1.56$ -5.46 -14.75

Energy Fuels Inc. EFR 0.18$ 0.24$ 0.13$ 18.7$ 71.00 0.26$ 2.86 28.57

Uranium Energy Corp UEC-US 2.52$ 3.02$ 1.40$ 215.5$ 14.58 14.77$ -3.91 25.51

Energy Resources of Australia Ltd ERA-AU 1.62$ 1.66$ 0.95$ 168.5$ 161.05 1.05$ 27.56 6.93

AdvancedExploration andDevelopment EquitiesIndex

Company Tick L. Px 52 wk H 52 wk L

M arket Cap

(C$ M M )

U3O8 NI

43-101

(lbs. MM) M C/lb$

YTD

Return

52 wk

Return

Denison Mines Corp. DML 1.34$ 1.68$ 1.04$ 499.8$ 131.37 3.80$ 11.38 3.01

Ur-Energy Inc. URE 1.35$ 1.38$ 0.64$ 141.8$ 25.32 5.60$ 66.27 102.94

Uranerz Energy Corp. URZ 1.36$ 1.82$ 0.92$ 106.1$ 18.36 5.78$ 2.92 3.68

UEX Corporation UEX 0.41$ 0.84$ 0.38$ 89.8$ 82.51 1.09$ -28.81 -31.15

Peninsula Energy (AUS$) PEN-AU 0.03$ 0.06$ 0.02$ 91.5$ 103.80 0.88$ -20.51 3.33

Laramide Resources Ltd LAM 0.61$ 1.10$ 0.47$ 45.8$ 61.20 0.75$ -25.61 -21.80

Forsys Metals Corp FSY 0.48$ 0.89$ 0.47$ 41.8$ 112.30 0.37$ -40.00 -43.53

Mega Uranium Ltd. MGA 0.10$ 0.22$ 0.07$ 29.9$ 43.03 0.70$ -12.50 -43.24

Strathmore Minerals Corp. STM 0.25$ 0.34$ 0.14$ 25.5$ 34.27 0.74$ -9.43 -7.69

Bannerman Resources Ltd. BAN 0.05$ 0.14$ 0.05$ 12.7$ 273.78 0.05$ -41.18 -61.54

Macusani Yellowcake Inc YEL 0.06$ 0.18$ 0.06$ 9.6$ 39.40 0.24$ -58.62 -53.85

Strateco Resources Inc RSC 0.07$ 0.33$ 0.04$ 9.6$ 28.70 0.33$ -67.50 -79.03

Khan Resources Inc KRI 0.15$ 0.21$ 0.09$ 8.4$ 66.70 0.13$ 25.00 3.45

Exploration, with a Resource

Company Tick L. Px 52 wk H 52 wk L

M arket Cap

(C$ M M )

U3O8 NI

43-101

(lbs. MM) M C/lb$

YTD

Return

52 wk

Return

Kivalliq Energy Corporation KIV 0.24$ 0.46$ 0.23$ 28.9$ 43.30 0.67$ -27.78 -22.39

Rockgate Capital Corp. RGT 0.17$ 0.67$ 0.14$ 18.0$ 45.25 0.40$ -69.44 -45.00

U3O8 Corp. UWE 0.14$ 0.45$ 0.13$ 13.1$ 47.60 0.28$ -35.56 -57.97

Vena Resources Inc. VEM 0.09$ 0.42$ 0.07$ 10.8$ 18.61 0.58$ -53.49 -75.00

Continental Precious Minerals Inc. CZQ 0.13$ 0.26$ 0.09$ 8.2$ 10.98 0.75$ -33.33 -47.62

Crosshair Exploration & Mining CXX 0.03$ 0.24$ 0.02$ 4.8$ 4.61 1.04$ -71.43 -85.00

Powertech Uranium Corp PWE 0.06$ 0.17$ 0.06$ 3.4$ 22.80 0.15$ -48.00 -43.48

Bayswater Uranium Corporation BYU 0.09$ 0.15$ 0.01$ 2.1$ 28.91 0.07$ 0.00 -15.79

Silver Spruce Resources Inc. SSE 0.01$ 0.07$ 0.01$ 1.4$ 2.22 0.62$ -50.00 -66.67

Deep Yellow Ltd. DYL-AU 0.04$ 0.10$ 0.03$ 1.3$ 119.30 0.01$ -32.79 -19.61

5.

Toll CrossSecuritiesInc.

Toronto St. Suite 200

Toronto, Ontario M5C 2V6

telephone: (416) 365-1960

facsimile: (416) 365-1962

email: toronto@tollcross.ca

website: www.tollcross.ca

Institutional Sales

Rodger Gray rodger.gray@tollcross.ca

James Massie james.massie@tollcross.ca

Ed Pennock ed.pennock@tollcross.ca

Institutional Trading

Russ Minor russ.minor@tollcross.ca

Tom George tom.george@tollcross.ca

PrivateClient Group

Rodger Gray andrew.beach@tollcross.ca

Andrew Beach rodger.gray@tollcross.ca

EquitiesResearch

Eleanor Barker International Oil & Gas eleanor.barker@tollcross.ca

Deniz Tura-Matten Energy Analyst deniz.tura-matten@tollcross.ca

Jacques Kavafian Airlines & Aerospace jacques.kavafian@tollcross.ca

Don DeMarco Mining &Minerals don.demarco@tollcross.ca

Investment Banking

Marc Bouchard Communications/Tech marc.bouchard@tollcross.ca

Tom Hope Communications/Tech tom.hope@tollcross.ca

Randall Blom Investment Banking Analyst randall.blom@tollcross.ca

6.

IMPORTANT DISCLOSURES

Analyst'sCertification

All of the views expressed in this report accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securities or issuers. No part

of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the

responsible analyst(s) in this report. The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may

be incomplete.

TCSI compensates its research analysts from a variety of sources. The research department is a cost centre and is funded by the business activities of TCSI including,

institutional equity sales and trading, retail sales, and corporate and investment banking. Since the revenues from these businesses vary the funds for research

compensation vary. No one business line has greater influence than any other for research analyst compensation.

Dissemination of Research

TCSI endeavours to make all reasonable efforts to provide research simultaneously to all eligible clients. TCSI equity research is distributed electronically via email

and is posted on our proprietary websites to ensure eligible clients receive coverage initiations and ratings changes, targets and opinions in a timely manner. Additional

distribution may be done by the sales personnel via email, fax or regular mail. Clients may also receive our research via a third party. Toll Cross Securities Inc. research

dissemination policies and procedures may be found on our website, www.tollcross.ca, in the Research Distribution Policy section.

Company SpecificDisclosures: 1, 2, 3, 4, 5, 6,& 7

SeeCompany Specific DisclosureKey below for explanations.

Company SpecificDisclosureKey

TCSI uses the following Company Specific Disclosure Key. Please refer to the Company SpecificDisclosuressection above for specific disclosures applicable to the

issuer(s) discussed in this report.

1 On the last day of the month preceding the date of this report TCSI and its affiliates held an aggregate of less than 5% of the outstanding shares (of any class of equity

securities) of companies discussed or listed in this report.

2 The research analyst(s) and/or associates (or their household members) who prepared this research report directly or beneficially own common stock of CCO.

3 TCSI has not managed or co-managed an initial public offering of equity or equity-related securities for any company discussed or listed in the past 12 months, the

closing date of which was at least 40 calendar days prior to the issuance of this report.

4 TCSI has not managed or co-managed a secondary offering of equity or equity-related securities for any company discussed or listed in the past 12 months, the

closing date of which was at least 10 calendar days prior to the issuance of this report.

5 TCSI has not provided services to any company discussed or listed for remuneration other than normal course investment advisory or trade execution services during

the preceding 12 months.

6 TCSI has not received compensation for investment banking services from any company discussed or listed during the preceding 12 months.

7 No employee of TCSI is an officer or direct of any company discussed or listed (or servesin an advisory capacity to theissuer).

Other Disclosures

For Canadian Residents this report

and its dissemination in Canada. Canadian clients wishing to effect transactions in any security discussed should do so through a qualified salesperson of TCS. For US

Residents tion in the United States.

This report is intended for distribution in the United States only to certain institutional investors. US clients wishing to effect transactions in any security discussed

should do so through a qualified salesperson of TCS USA.

Every province in Canada, State in the U.S., and most countries throughout the world have their own laws regulating the types of securities and other investment

products which may be offered to their residents, as well as the process for doing so. As a result, some of the securities discussed in this report may not be available

to every interested investor. Accordingly, this report is provided for informational purposes only, and does not constitute an offer or solicitation to buy or sell

securities discussed herein in any jurisdiction where such would be prohibited. Neither TCS nor its affiliates accepts any liability whatsoever for any loss arising from

any use of this report or its contents.