Calculating Consignment Stock Value

•

2 recomendaciones•673 vistas

This document contains examples and questions related to consignment accounting. It includes calculations for: 1) Determining the value of consignment stock based on the total cost of goods, goods received and sold by the consignee. 2) Calculating total commission payable to a consignee based on fixed and variable commission rates applied to sales, costs, and profits. 3) Additional questions include calculating stock reserve amounts, profit on consignment, and total commission payable using given sales amounts, invoice prices, and costs. The document provides the questions, calculations, and answers to help understand accounting for consignment arrangements.

Recomendados

Más contenido relacionado

Similar a Calculating Consignment Stock Value

Similar a Calculating Consignment Stock Value (20)

Más de VXplain

Más de VXplain (20)

Calculating Consignment Stock Value

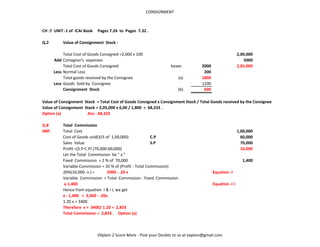

- 1. CONSIGNMENT CH :7 UNIT -1 of ICAI Book Pages 7.24 to Pages 7.32 . Q.2 Value of Consignment Stock : Total Cost of Goods Consigned =2,000 x 100 2,00,000 Add Consignor's expenses 5000 Total Cost of Goods Consigned boxes 2000 2,05,000 Less Normal Loss 200 Total goods received by the Consignee (a) 1800 Less Goods Sold by Consignee 1200 Consignment Stock (b) 600 Value of Consignment Stock = Total Cost of Goods Consigned x Consignment Stock / Total Goods received by the Consignee Value of Consignment Stock = 2,05,000 x 6,00 / 1,800 = 68,333 . Option (a) Ans : 68,333 Q.8 Total Commission IMP. Total Cost 1,00,000 Cost of Goods sold(3/5 of 1,00,000) C.P 60,000 Sales Value S.P 70,000 Profit =(S.P-C.P) (70,000-60,000) 10,000 Let the Total Commission be " x " Fixed Commission = 2 % of 70,000 1,400 Variable Commission = 20 % of (Profit - Total Commission) 20%(10,000- x ) = 2000 - .20 x Equation -I Variable Commission = Total Commission - Fixed Commission. x-1,400 Equation -I I Hence from equation I & I I, we get x - 1,400 = 2,000 - .20x 1.20 x = 3400 Therefore x = 3400/ 1.20 = 2,833 Total Commission = 2,833 . Option (a) VXplain 2 Score More - Post your Doubts to us at vxplain@gmail.com

- 2. CONSIGNMENT Q.12 Value of Consignment Stock : Total Cost of Consignor = (4,000 x 200) + (2,000) 82,000 Add Non-Recurring expenses of the Consignee (i.e Non- Selling ) 2,000 Total Cost 84,000 Value of Consignment Stock : Total Cost x Consignment Stock / Total Goods sent on Consignment 84,000 x 100 / 400 (Option- d ) 21,000 Q.15 Value of Consignment Stock : Invoice Cost Price Price Total Cost of Consignor = (500 x 500) + (4,000) (at Invoice Price ) 2,54,000 Total Cost of Consignor = (500 x 400) + (4,000) (at Cost Price ) 2,04,000 Add Non-Recurring expenses of the Consignee (i.e Non-Selling ) 1,000 1,000 Total Cost 2,55,000 2,05,000 Value of Consignment Stock :(at Invoice Price) Total Cost(at I.P) x Consignment Stock / Total Goods sent on Consignment 2,55,000 x 100 / 500 (Option- d ) 51,000 Additional Other question that can also be asked and answered from the same example : Value of Consignment Stock :(at Cost Price) Total Cost(at Cost) x Consignment Stock / Total Goods sent on Consignment 2,05,000 x 100 / 500 41,000 Amount of Stock Reserve 1) Value of Consignment Stock(at I.P)- Value of Consignment Stock at C.P 51,000- 41,000 10,000 VXplain 2 Score More - Post your Doubts to us at vxplain@gmail.com

- 3. CONSIGNMENT OR 2) (Total Invoice Price - Total Cost) x Consignment Stock / Total Goods received by the Consignee 2,50,000-2,00,000) x 100 / 5000 10,000 Q.24 Total Commission Invoice Price on Goods Sold (2,00,000 x 4) / 5 1,60,000 Commission upto Invoice Price @2% = 1,60,000 x 2 % 3200 Commission in excess of Invoice Price @ 10 % = (1,76,000 - 1,60,000) x 10% 1600 Total Commission 4,800 Option (a) 4,800 Q.32 Total Commission payable "B" Invoice Value of Goods Sent =(12,500 /10%) 1,25,000 75% of Invoice Value (75% of 1,25,000 ) 93,750 Total Sales 1,00,000 Excess of Sales over Invoice Price (1,00,000-93750) 6,250 Normal Commission 10% on sales = 10% of 1,00,000 10000 Additional Commission 25% on surplus above Invoice Price(i.e 25% of 6250) 1562.5 Total Commission (option -a) 11,562.50 Q.44 Profit on Consignment To Goods sent on Consignment a/c. 2,00,000 By Consignee (Sales) 2,10,000 To Cash/Bank(Consignor Exp,) 5,000 By Consignment Stock 40,000 To Consignee (Exps./Comm.) (2,000+3,000+2,000) 7,000 To Gen. P&L a/c (Profit on Consignment) 38,000 (2,54,000-2,00,00-5,000-7,000) 2,54,000 2,54,000 VXplain 2 Score More - Post your Doubts to us at vxplain@gmail.com

- 4. CONSIGNMENT Other Important MCQ's Q . Nos. 11 ,17, 21 , 28 ,29 ,33, 37, 38, 43, 47, 48, 49,62, 63 , 66 Question Set II -----------Match the Column . VXplain 2 Score More - Post your Doubts to us at vxplain@gmail.com