VIP Independent Call Girls in Bandra West 🌹 9920725232 ( Call Me ) Mumbai Esc...

indian economy before US recession

1. :-Done by Sunil Kumar and Ajeet verma

Indian economy before us recession

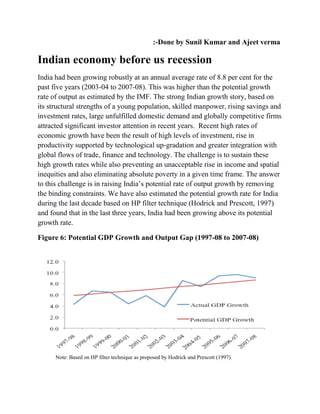

India had been growing robustly at an annual average rate of 8.8 per cent for the

past five years (2003-04 to 2007-08). This was higher than the potential growth

rate of output as estimated by the IMF. The strong Indian growth story, based on

its structural strengths of a young population, skilled manpower, rising savings and

investment rates, large unfulfilled domestic demand and globally competitive firms

attracted significant investor attention in recent years. Recent high rates of

economic growth have been the result of high levels of investment, rise in

productivity supported by technological up-gradation and greater integration with

global flows of trade, finance and technology. The challenge is to sustain these

high growth rates while also preventing an unacceptable rise in income and spatial

inequities and also eliminating absolute poverty in a given time frame. The answer

to this challenge is in raising India’s potential rate of output growth by removing

the binding constraints. We have also estimated the potential growth rate for India

during the last decade based on HP filter technique (Hodrick and Prescott, 1997)

and found that in the last three years, India had been growing above its potential

growth rate.

Figure 6: Potential GDP Growth and Output Gap (1997-08 to 2007-08)

Note: Based on HP filter technique as proposed by Hodrick and Prescott (1997).

2. Fears of over-heating of the economy prompted the Reserve Bank of India (RBI) to

begin monetary tightening as early as September 2004 when the cash-reserve

ratio(CRR) for commercial banks was raised. The sharp increase in global fuel and

food prices in the first quarter of 2008 aggravated inflationary concerns and

resulted in further monetary tightening that saw interest rates being hiked until

August 2008.This was clearly a case of policy running behind the curve and

consequently over-compensating in its attempt to weaken inflationary expectations.

Expectedly, this amount of monetary contraction resulted in a slowing down of the

economy with the GDP growth coming down to 7.8 per cent during April-

September 2008 from 9.3 percent in the same period of 2007.

US RECESSION AND ITS EFFECT ON INDIAN ECONOMY

Since US is one of the major super powers, a recession–mild or deeper will

have eventual global Consequences? The crisis rapidly developed and spread into a

global economic shock, resulting in a number of European bank failures, declines

in various stock indices, and large reductions in the market value of equities and

commodities A slowdown in the US economy was definitely a bad news for India

because Indian companies have major outsourcing deals from the US. India's

exports to the US have also grown substantially over the years. But in spite of all

this India has successfully weathered the great financial crisis of September 2008.

Indian gross domestic product (GDP) has grown around 6% in every quarter of the

most difficult 12 months in recent history. Here are some worth following:

Impact of Recession on Indian Industrial Sector

During Recession industrial growth was also faltering India’s industrial sector has

suffered from the depressed demand condition in its export market as well as from

suppressed domestic demand due to the slow generation of employment domestic

demand due to the slow generation of employment . As per the index of industrial

production (IIP) the overall growth in 2008-09 was 3.2 percent compared to a

growth of 8.7 percent in 2007-08.

Index of Industrial Production Growth

year 2005-06 2006-07 2007-08 2008-09 2009-10

3. Index of

IndustrialProduction(Growth)

8.0% 11.9% 8.7% 3.2% 10.5%

Source: Central Statistical Organization, Government of India

Impact of Recession on Indian Stock Market

The Indian stock exchange hold a place of prominence not only in Asia but also at

the global stage. The Bombay stock Exchange(BSE) is one of the oldest exchanges

across the world, while the National stock Exchange(NSE) is among the best in

terms of sophistication and advancement of technology. The Indian stock market

scene really picked up after the opening up of the economy in the early nineties.

Due to this, there was a collapse in stock Price. As a result, the sensex fell from its

closing peak of 20873 on January 2008 to nearly 8000 in October- November

2008.

year 2008-09 2009-10 2010-11 May 2010

BSE sensex 9708.5 17527.5 17558.7 16944.6

4. From the Table shows that in the last trading day of 2008-09 the BSE sensex was

9708.5. It was increased in 2009-10 was 17527.8 , in 2010-11 it was 17558.7 and

in May 2010 was 16944.6.

Source: SEBI Bulletin June 2010 Vol 8 Number 06

Impact of Recession on Foreign Institution Investment

The Most immediate effect of the crisis on India has been an outflow of foreign

institutional investment from the equity market. Foreign Institutional Investment

which need to retrench assets in order to cover losses in their home countries and

were seeking havens of safety in an uncertain environment, have become major

sellers in Indian markets As FIIs pull out their money from the stock market the

large likely to be the export and small and marginal enterprises that contribute

significantly to employment generation. In 2007-08, net foreign Institutional

Investment (FIIs) inflows into India amounted to $16040 million. But in April-

November 2008 it was negative to $8857 million.

Net Investment Of FIIS At Monthly Exchange Rate ( In Us $ Million)

year 1999-

00

2000-

01

2001-02 2002-03 2003-

04

2004-05 2005-06 2006-07 2007-

08

2008-09

amount 2339 2160 1846 562 9949 10272 9332 6707 16040 -8857

5. Impact of Recession on Foreign Direct Investment

FDI inflow experienced a declining trend in the first three quarters of 2008-09, but

has shown improvement in the fourth quarter. The sectors which received major

part of this FDI flow are the manufacturing sector (21.1%) followed by financial

services (19.4%) and the construction sector (9.9%). The revival in capital flows

witnessed during the first quarter of 2009-10 gathered momentum during the

second quarter of 2009-10.

6. Impact of Recession on Foreign Exchange Market

The foreign exchange market came under pressure because of reversal of capital flows as part of the

global decelerating process. Foreign exchange reserve were depleting. It was $ 309.7 billion in 2007-08

and came down to $252.0 billion in 2008-09 which shows the direct impact of the financial crisis on

India’s foreign exchange reserve.

Foreign Exchange Reserve (In US $ Billion)

year 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

ForeignExchangeReserve 151.6 199.2 309.7 252.0 279.1 297.3

Impact of recession on India’s Foreign Trade in Us $ Million

year Exports

(%growth)

Imports

(%growth)

Balance of trade

2005-06

2006-07

2007-08

2008-09

2009-10

103091(23.4)

126414(24.5)

162904(29.0)

185295(13.3)

178751(-3.5)

149166(33.8)

185765(24.5)

251439(35.5)

303696(20.7)

288373(-5.0)

-46075

-59321

-88535

-118401

-109622

7. 2010-11 105064(29.5) 161051(19.0) -55987

Source: DGCI&S, India

Above table shows that in 2007-08, India export and import were $162904 million

and $251439 million respectively and balance of payment was $ -88535 million .

And in 2008-09 export and import were $185295 million and $303696 million

respectively. The Balance of payment was $ -118401 million. The growth rate of

export and import also declined to 13.3 percent and 20.7 percent from 29.0 and

35.5 percent respectively during that period. In 2009-10 the export growth rate was

-3.5 percent and import growth rate was -5.0 percent. The balance of payment was

$ -109622. This shown that India’s exports are adversely affected by the slowdown

in global markets. This is already evident in certain industries like garments

industries where there have been significant job losses with the onset of the crisis.

The depreciation of rupee could not positively affect the export bill of India.

Impact of Recession on Indian Employment

Employment is worst affected during any fiscal crisis, so is true with the current

global meltdown. This recession has adversely affected the service industry of

India mainly the BPO, KPO, IT companies etc. According to a sample survey by

the commerce ministry, 109,513 people lost their jobs between August 2008 and

8. October 2008 in export related companies in several sector primarily textile,

leather engineering, gems and jewellery, handicraft and food processing.

Impact of Recession on India’s GDP Growth Rate

The Impact of the crisis was significantly different for the Indian economy as

opposed to the western developed nations. After a long spell of growth, the Indian

economy was experiencing a down turn.

YEAR GDP(2004-05 PRICE) GROWTH IN %

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

3254216

3566011

3898958

4162509

4493743

4879232

9.5

9.6

9.3

6.8

8.0

8.6

Source: Central Statistical Organization, Government of India

Trends in GDP (Growth Rate In %)

The Table shows that in 2006-07 the GDP growth rate was 9.6% which became

9.3% in 2007-08 and due to the impact of recent global financial crisis and global

recession, the growth rate of Indian economy became declining. In 2008-09 it

reduced to 6.8%. The International Monetary fund has also projected the growth

9. prospects for Indian economy to 5.1% in next year. And the RBI annual policy

statement 2009 presented on July 28, 2009 projected GDP growth at 6% for 2009-

10. The declining trends has affected adversely the industrial activity, especially in

the manufacturing, infrastructure and in service sector mainly in the construction,

transport and communication, trade, hotels etc.

Causes of the Slowdown in 2008-09

Impact of Monetary Tightening

Price stability, strongly anchoring inflationary expectations, promoting growth and

maintaining financial stability are the avowed objectives of Indian monetary

policy. The tolerance limit for the purposes of monetary policy for inflation in

India is considered to be at about 5 per cent. Inflation in India has been at moderate

levels as compared to other emerging economies but during 2003-04 the wholesale

price index (WPI) inflation crossed the 6 per cent mark

Figure 9: WPI Inflation and CPI (Industrial Workers) Inflation Rates

source: Office of Economic Advisor, Ministry of Commerce & Industry, Government of India.

In response to the rise in inflation, the RBI, with its hawkish stance on inflation,

and faced with an overheating economy, started monetary policy tightening as

early as September 2004 when the CRR was raised from 4.5 to 5 per cent in two

steps. As the inflationary situation worsened in the subsequent period the

10. tightening got harder as shown in Fig. With headline inflation crossing double

digits first time in the second week of June 2008 and reaching 11 per cent

primarily due to the abnormal hike in global fuel, food and commodity prices, the

RBI continued with further monetary tightening. The last set of measures to cool

the economy were announced at the end of August 2008. The RBI, ostensibly in

response to global oil prices crossing $147 per barrel and domestic year-on-year

inflation reaching 12.9 per cent raised the CRR by 25 basis points to 9 per cent. As

several critics pointed out, the tight monetary policy stance was provoked

principally to compensate for the fiscal expansion that originated with the 2008-09

budget. But the RBI perhaps overlooked that price trends, as reflected in the

month-on-month changes had begun to head southwards since end of September

2008. The economy had already slowed down before the onset of the global crisis

on account of the measures taken since the latter half of 2004.

Figure 10: Monetary Policy Changes, March 2004- March 2009

Source: Reserve Bank of India.

The effects of monetary policy are subject to long lags and the full impact of the

progressive tightening that continued until August 2008 is still to fully work itself

out. However, the concretionary impulses generated by the tightening undertaken

until August 2008 are now being countered by the expansionary impact of

monetary policy relaxation that started in the latter half of October 2008.

11. Industrial Sector Weakness

The recent downturn started since May 2007 and by December 2008 has already

run for 20 months was preceded by the longest upward industrial cycle during

which the IIP growth rate improved almost continuously for 64 months.

Underlying the beginning of the slowdown is the hardening of interest rates since

March 2007 in the wake of the tightening monetary policy. The second quarter

year-on-year IIP growth in the current year (Q2 2008-09) has dropped to 4.7 per

cent from 5.3 per cent in the first quarter. In Q3 2008-09, the growth rate had

turned to just 0.4 per cent. In January 2009 the growth rate turned negative at -0.5

per cent. The downturn is turning severe and would be prolonged due to the global

crisis.

Figure : 12 Month Moving Average of IIP (1982-2008)

Source: Central Statistical Organization.

Investment Weakness

The major drivers of India’s high growth rate in the last five years have been

investment and private consumption. As can be seen from Fig. the rate of growth

in gross fixed investment more than doubled from about 7 per cent during 2001-03

to about 16 per cent during 2003-07. Growth in private final consumption also rose

from about 5 per cent during 2001-05 to about 8 per cent during 2005-07. Private

consumption growth has slowed down since Q3 2007-08, and the growth in fixed

investment has continuously fallen since Q2 2007-08 with some pick-up just in Q2

12. 2008-09. Government final consumption expenditure which normally is subject to

wide swings has shown some reasonable growth in recent quarters and

substantially so in Q3 2008-09.

Figure 13: Composition of Demand Growth, 2001-02 to 2008-09 Q3 (Per cent)

source: Central Statistical Organization.

Fiscal Measures Deficit

There has been a steady improvement in central and state finances since 2001-02

when the fiscal and revenue deficits of the combined central and state governments

reached a peak of 9.9 per cent and 7.0 percent of GDP respectively.

Figure 14: Fiscal Indicators of the Combined Centre and States

13. Source: Reserve Bank of India.

There was some deterioration in the central government finances in 2005-06 but

these improved in 2006-07. The fiscal consolidation by the states has also been

quite significant in recent years. The central government budget for the current

year 2008-09 targeted a further improvement in the fiscal situation. However,

several leading experts and economists have conclusively pointed out the gross

underestimation of fiscal deficit in that budget. The Interim Budget, released in

February 2009, has now revealed a huge rise in fiscal deficit of the central

government to 6 per cent of GDP in 2008-09 from 2.7 percent in 2007-08.

Global Integration

Indian economy has become much more integrated with the world economy now

than the pre-reform period. Liberalization in industry, investment, foreign trade,

financial sector and capital flows that was undertaken after the balance of payment

crisis in early 1990s led to India becoming well integrated with the world

economy. With the increased linkage with the world economy, India cannot

remain immune to the global crisis. India began to feel the impact of the crisis in

January 2008 when the BSE sensex collapsed after crossing the peak of 20800 in

early January 2008. Basically there are three channels through which India is

affected by the global crisis:

Depreciating of currency

The rupee has been depreciating since January 2008 as a direct result of the huge

reverse flow of capital out of India. From an average Rs. 40.36 per US dollar in

March 2008 it fell to an average of Rs. 49.00 in November 2008, depreciation of

about 18 per cent and further to nearly Rs 52 at the beginning of March 2009. This

is a decline of 22 per cent over the same month in 2008. Depreciation is good for

Indian exports but it will have adverse effects on corporates who borrowed abroad

and will raise the cost of external debt servicing.

Policy Response to the Economic

Monetary Policy Measures

14. Before the spread of the global crisis, rising inflation was one major downside risk

for the Indian economy. But the fall of prices of oil and other commodities and

overall fall in demand as a result of recession in major developed countries has

pushed down the rate of inflation in India. Inflation measured by the wholesale

price index (WPI) had peaked at 12.9 per cent in early August 2008 and has been

coming down since then. WPI inflation dropped to 4.4 per cent by 31st January

2009 and just 2.4 percent as on 28th February 2009. Monetary policy shifted gear

and became expansionary from October after the scale of the US financial sector

meltdown and its likely adverse effects on the Indian economy became evident.

The policy focus has shifted from containing inflation to promoting growth.

Falling inflation, a positive by product of global crisis, enabled the central bank to

loosen monetary policy more aggressively. As indicated earlier, the RBI lowered

the cash reserve ratio (CRR) requirements of banks from 9 per cent to 5 percent,

statutory reserve ratio (SLR) requirements from 25 percent to 24 percent and the

repo rate (the rate at which it lends to banks overnight), from 9 percent to 5 percent

and reverse repo rate (the rate at which RBI borrows from banks) from 6 percent to

3.5 per cent. RBI has opened a refinance facility to Small Industrial Development

Bank of India (SIDBI), National Housing Bank (NHB).

Fiscal Stimulus

governments across the world have announced various fiscal stimulus packages to

counter the crisis. The Indian government’s fiscal package is small in magnitude

constituting around 1.3 percent of GDP for 2008-09. This seems to be quite small

as compared to most of the countries. But as has been reiterated earlier there is less

fiscal headroom in India which is already running a high public debt.

Why did India suffer so little in the Great Recession that laid

low the biggest economies of the West?

It may be true with rest of the world but India had some higher immunity to resist

the global meltdown which started in USA in 2007. This financial crisis impacted

various economies across the world; including USA, UK, Japan, China, France and

India. During this turmoil the countries had varying impacts; countries like China

and India had a lesser share of the worldwide despair. There are many reasons

which it has led the world to believe that India survived the global problem.

15. Indian banks and financial institutions had almost entirely avoided buying the

mortgage-backed securities and credit default swaps that turned toxic and felled

western Financial institutions. India's merchandise exports were indeed hit by the

Great Recession but Service exports did not fall - computer software and BPO

exports held up well. Financiers reversed Flows into India, but long-term investors

in plant and factories completed their ongoing projects. Monetary policy was

accommodating in 2008. The RBI lowered interest rates and expanded Credit. The

government cut excise duties to stoke demand. All these factors cushioned the

shock to the economy.

Table 1: The Institute of International Finance (IIF) Projections for Growth (2008-

10).

World economy 2% growth in 2008 and predicted to

shrink to 0.4% in 2009

USA (World's Largest Economy) 1.3% growth in 2009

Japan (World's Second Largest

Economy)

0% growth predicted in 2010

China 6.5% growth rate in 2009

India 5% growth rate in 2009

Current economy (2013-2014)

According to the Economic Survey 2013-14, tabled in Parliament on July 9, 2014,

by Mr Arun Jaitley, Union Minister for Finance, Government of India, the gross

domestic product (GDP) is expected to grow at 5.4-5.9 per cent in FY15. The

Survey reports that the services sector constituted a 57 per cent share in GDP at

factor cost (at current prices) in FY 14.

The main highlights of the survey are:

Gross domestic product (GDP) is expected to grow at 5.4–5.9 per cent in FY15.

India has the second fastest growing services sector with compound annual growth rate (CAGR)

of 9 per cent.

16. Services constituted a 57 per cent share in GDP at factor cost (at current prices) in FY 14, an

increase of 6 per cent points over FY01.

Foreign exchange reserves grew to US$ 304.2 billion by March 2014 from US$ 292 billion at the

end of March 2013.

Annual average exchange rate of the rupee went up from Rs 47.92 (US$ 0.8) per US dollar in

2011–12 to Rs 54.41 (US$ 0.91) per US dollar in 2012–13 and further to Rs 60.5 (US$ 1.01) per

US dollar in 2013–14.

Revenue receipts in 2013–14 were Rs 1,015,279 crore (US$ 169.85 billion), 8.9 per cent of the

GDP. The gross tax revenue in 2013–14 was estimated at Rs 1,133,832 crore (US$ 189.68 billion),

10 per cent of the GDP.

Fiscal deficit for 2013–14 has been contained at Rs 508,149 crore (US$ 85.01 billion)

(provisional) – 4.5 per cent of the GDP (4.9 per cent in 2012–13).

Indirect tax collection for 2013–14 stood at Rs 496,231 crore (US$ 83.02 billion) as compared to

Rs 473,792 crore (US$ 79.26 billion) in 2012-13.

Direct tax collection for 2013–14 was Rs 633,473 crore (US$ 105.98 billion)

CONCLUSION

India has been hit by the global meltdown, it is clearly due to India’s rapid and

growing integration into the global economy. The strategy to counter these effects

of the global crisis on the Indian economy. The first such departure should be a

return to Food first doctrine, not only to ensure food security of the large

population but also due to the fact the food production will be more profitable

given the current signs of a shrinking market for export oriented commercial crops.

The other important initiatives that needs to be adopted is the building of

institution based on the principle of cooperation that will provide an alternative

frame work of livelihood generation in the rural economy as opposed to the

dominant logic of markets under capitalism.Institutions like cooperative markets

and credit cooperative can go a long way in addressing the lack of economically

viable producer prices primary sector. Such an alternative for economic activities

in the primary sector. To sum up we can say that the global financial recession

which started off as a a sub-prime crisis of USA has brought all nations including

India into its fold. The GDP growth rate which was around none percent over the

last four year has slowed since the last quarter of 2008 owing to deceleration in

employment export, import tax GDP ratio reduction in capital inflows and

significant outflows due to economic slowdown. The demand for bank credit is

also slackening despite comfortable liquidity in the system. Once calm and

17. confidence are restore in the global markets, economic activity in India will

recover sharply. Yet there will be a period of painful adjustment which is

inevitable.