Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (19)

Similar a The theory of the firm

Similar a The theory of the firm (20)

Más de boxonomics

Más de boxonomics (13)

Último

Último (20)

The theory of the firm

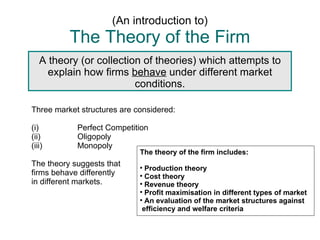

- 1. (An introduction to) The Theory of the Firm A theory (or collection of theories) which attempts to explain how firms behave under different market conditions. Three market structures are considered: (i) Perfect Competition (ii) Oligopoly (iii) Monopoly The theory of the firm includes: The theory suggests that Production theory firms behave differently Cost theory in different markets. Revenue theory Profit maximisation in different types of market An evaluation of the market structures against efficiency and welfare criteria

- 2. Underlying concepts To understand the theory of the firm you must firstly understand some basic concepts underpinning the theory... 1. What is a firm? A firm is a business enterprise which produces, or trades in, goods and/or services. A firm can be privately or state owned (i.e. by individuals or government).

- 3. Concepts continued... 2. Profit Maximisation PROFIT Firms aim to make as much profit Revenue as possible i.e. produce at the Costs level of output at which the gap between revenue and production costs is greatest. 3. Production Factors of Production A firm 'adds value' by combining a range of factors of production PRODUCT into a finished product or service. This process is known as production.

- 4. Concepts continued 4. Productive efficiency The production process incurs costs. Firms will attempt to minimise costs to maximise profit. A firm will be productively efficient is costs are minimised. 100 units 200 units 300 units 400 units Total Cost £500 £900 £1200 £1800 Unit cost What level of output is the most productively efficient?

- 5. Concepts continued 4. Productive efficiency The production process incurs costs. Firms will attempt to minimise costs to maximise profit. A firm will be productively efficient is costs are minimised. 100 units 200 units 300 units 400 units Total Cost £500 £900 £1200 £1800 Unit cost £5 £4.50 £4 £4.50 What level of output is the most productively efficient?

- 6. Concepts continued 5. Revenue maximisation Firms receive revenue for selling their product or service. The amount of revenue is determined by the price charged and the level of sales. 100 units 200 units 300 units 400 units Price £10 £6 £3 £2 Revenue What level of price generates the most revenue?

- 7. Concepts continued 5. Revenue maximisation Firms receive revenue for selling their product or service. The amount of revenue is determined by the price charged and the level of sales. 100 units 200 units 300 units 400 units Price £10 £6 £3 £2 Revenue £1000 £1200 £900 £800 What level of price generates the most revenue?

- 8. Concepts continued 6. Market structure Put these UK markets in order according to the The behaviour of a firm will vary number of firms according to the nature of the operating in them. market it is in. An important factor is the number of firms in Car market the market. Hairdressers Monopoly = 1 firm Banks Nuclear power plants Oligopoly = a few firms Supermarkets Website designers Perfect competition = many firms

- 9. Concepts continued And... 7. Short run 8. Long run Revenue and costs in the short Revenue and costs are not run are influenced by the restricted by factors of factors of production available. production in the long run. 'Short-run' is defined as a 'Long run' is defined as a period period within which at least one over which all the factors of factor of production is fixed. production can change. Consider the This isn't a output achievable 'short run'. The with one factory finish line keeps compared to as moving! many factories as you can build.

- 10. And finally... 9. Welfare and efficiency What is the best market structure? We can judge this by the extent to which they deliver economic welfare and efficiency. Economic efficiency Output per Jobs Max out worker Economic for min in welfare Best use of resources Consumer Producer surplus surplus (utility) (profit)

- 11. Summary Evaluating market structures using efficiency and welfare criteria Imperfect Competition Model of Perfect Model of Monopoly Competition Model of Oligopoly PRODUCTION THEORY Short-run production Long-run production Revenue theory (for theory (the law of theory (returns to each market structure) diminishing returns) scale) Short-run cost theory Long-run cost theory

- 12. Application of the theory Understanding the Theory of the Firm will help you answer questions like these... Why is Tesco's starting a price war? Should the Post Office be privatised? Will making schools more competitive help improve standards? Why are Honda cutting wages? What makes Facebook the market leaders in social networking?