Health FSAs Can Now Allow Carryover

•

0 recomendaciones•219 vistas

Guidance was recently issues that modified the Health FSA Use-or-Lose Rule to allow carryover of FSA funds from one plan year to the next plan year - at an employer's discretion. What does this mean?

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a Health FSAs Can Now Allow Carryover

Similar a Health FSAs Can Now Allow Carryover (20)

Más de Infinisource

Más de Infinisource (20)

Último

Último (20)

Health FSAs Can Now Allow Carryover

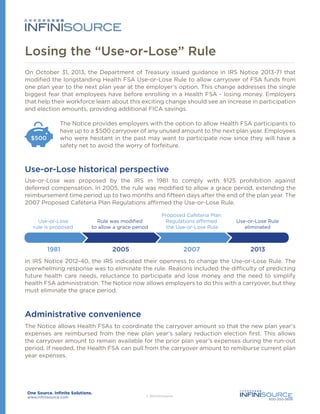

- 1. Losing the “Use-or-Lose” Rule On October 31, 2013, the Department of Treasury issued guidance in IRS Notice 2013-71 that modified the longstanding Health FSA Use-or-Lose Rule to allow carryover of FSA funds from one plan year to the next plan year at the employer’s option. This change addresses the single biggest fear that employees have before enrolling in a Health FSA - losing money. Employers that help their workforce learn about this exciting change should see an increase in participation and election amounts, providing additional FICA savings. $500 The Notice provides employers with the option to allow Health FSA participants to have up to a $500 carryover of any unused amount to the next plan year. Employees who were hesitant in the past may want to participate now since they will have a safety net to avoid the worry of forfeiture. Use-or-Lose historical perspective Use-or-Lose was proposed by the IRS in 1981 to comply with §125 prohibition against deferred compensation. In 2005, the rule was modified to allow a grace period, extending the reimbursement time period up to two months and fifteen days after the end of the plan year. The 2007 Proposed Cafeteria Plan Regulations affirmed the Use-or-Lose Rule. Use-or-Lose rule is proposed Rule was modified to allow a grace period Proposed Cafeteria Plan Regulations affirmed the Use-or-Lose Rule Use-or-Lose Rule eliminated In IRS Notice 2012-40, the IRS indicated their openness to change the Use-or-Lose Rule. The overwhelming response was to eliminate the rule. Reasons included the difficulty of predicting future health care needs, reluctance to participate and lose money and the need to simplify health FSA administration. The Notice now allows employers to do this with a carryover, but they must eliminate the grace period. Administrative convenience The Notice allows Health FSAs to coordinate the carryover amount so that the new plan year’s expenses are reimbursed from the new plan year’s salary reduction election first. This allows the carryover amount to remain available for the prior plan year’s expenses during the run-out period. If needed, the Health FSA can pull from the carryover amount to remiburse current plan year expenses. www.infinisource.com 800-300-3838

- 2. Example: Fred is able to carry over $500 in his Health FSA into the 2014 calendar plan year. His 2014 election is $2,500. On January 4, 2014, he incurs a $2,750 expense. He has a $100 expense that was incurred in 2013, but he does not $500 submit it until January 11, 2014, during the runout period. 2013 2014 The FSA pays $2,500 from the 2014 election, then the remaining $250 from $500 carryover. The $250 balance is available to reimburse the $100 expense incurred in 2013 submitted during the run-out period. Fred now has $150 remaining for 2014. Plan amendment Employers choosing to provide the carryover must amend the plan before the end of plan year from which the carryover will occur. Plan amendments must also include the elimination of any grace period. Participants must be notified of the carryover provision via a revised summary of plan description (SPD) or summary of material modifications (SMM). Plan years starting in 2013 have until the end of the plan year that starts in 2014 to amend plan documents to allow a carryover. Other rules and implications Employer plans may establish a lower maximum limit than $500, but it must be uniformly applied to all eligible participants. The carryover is applicable only to Health FSAs (not to Dependent Care FSAs). A participant’s carryover amount does not count toward $2,500 §125(i) salary reduction contribution limit. The carryover amount can include both employer and employee contributions. The carryover amount is available, even if a participant does not make an election for the next plan year. For example, if $500 remains unused at the end of the plan year, it can be carried over for the next plan year even though the participant does not elect Health FSA coverage in the following year. The participant will start the new plan year with a $500 account balance. In theory, this balance could be carried over for several years even though the participant does not elect Health FSA coverage. Unused amounts above the carryover limits are subject to forfeiture and cannot be cashed out or transferred to other taxable or nontaxable benefits (e.g., HSAs). The carryover is not available if employment terminates except via COBRA (if available). Further guidance is expected on some of the COBRA issues related to the carryover. HSA compatibility also was not addressed in the Notice. We do know that a general purpose Health FSA (including carryover) disqualifies an individual from contributing to an HSA, most likely for the entire plan year. www.infinisource.com 800-300-3838

- 3. In such an event, it appears that the Health FSA might have some design options: • Limited purpose • Post-deductible • Both limited purpose and post-deductible Based on existing regulations, it does not appear that carryover amounts would be included in nondiscrimination testing or justify a midyear election change. It is unclear whether carryover amounts need to be reported on W-2s in box 12 as Code DD. In theory, individuals wanting to contribute to an HSA could simply waive the carryover. Comparison Feature Carryover Grace period Amount available after plan year ends Up to $500 Unlimited Duration of availability after plan year ends Unlimited 2 months, 15 days Use-or-Lose Rule is no longer a major concern Yes No Likely decrease in forfeitures Yes No Likely increase in participation Yes No Likely increase in election amounts Yes No Corresponding increase in savings related to income tax and FICA for participants Yes No Corresponding increase in savings related to FICA for employers Yes No Most employers should be doing the math right now. With carryovers, will the likely moderate decrease in forfeitures be offset by the increase in FICA savings (7.65 percent)? When you do the math, many will agree that the carryover presents an exciting win-win proposition for both employers and employees! www.infinisource.com 800-300-3838