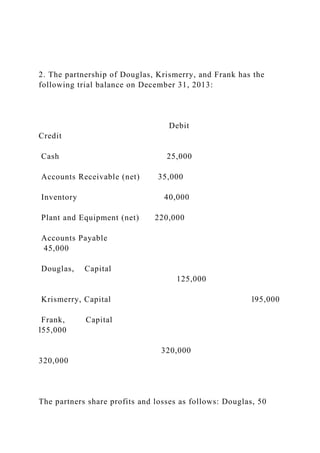

2. The partnership of Douglas, Krismerry, and Frank has the following trial balance on December 31, 2013:

Debit Credit

Cash 25,000

Accounts Receivable (net) 35,000

Inventory 40,000

Plant and Equipment (net) 220,000

Accounts Payable 45,000

Douglas, Capital 125,000

Krismerry, Capital l95,000

Frank, Capital l55,000

320,000 320,000

The partners share profits and losses as follows: Douglas, 50 percent; Krismerry, 30 percent; and Frank, 20 percent. The partners have decided to liquidate their partnership by installments. Cash is distributed to the partners at the end of each month. A summary of the liquidation transactions follows:

January

a. $30,000 is collected on accounts receivable; balance is uncollectible.

b. $25,000 received for the entire inventory.

c. $1,500 liquidation expense paid.

d. $45,000 paid to creditors.

e. $10,000 cash retained in the business at the end of the month.

February

f. $2,000 in liquidation expenses paid.

g. As part payment of his capital, Frank accepted an item of special equipment that he developed, which had a book value of $10,000. The partners agreed that a value of $14,000 should be placed on this item for liquidation purposes.

h. $5,000 cash retained in the business at the end of the month.

March

i. $155,000 received on sale of remaining plant and equipment.

j. $1,000 liquidation expenses paid. No cash retained in the business.

Required:

Prepare a statement of partnership realization and liquidation with supporting schedules of safe payments to partners.

.

2. The partnership of Douglas, Krismerry, and Frank has the foll.docx

1. 2. The partnership of Douglas, Krismerry, and Frank has the

following trial balance on December 31, 2013:

Debit

Credit

Cash 25,000

Accounts Receivable (net) 35,000

Inventory 40,000

Plant and Equipment (net) 220,000

Accounts Payable

45,000

Douglas, Capital

125,000

Krismerry, Capital l95,000

Frank, Capital

l55,000

320,000

320,000

The partners share profits and losses as follows: Douglas, 50

2. percent; Krismerry, 30 percent; and Frank, 20 percent. The

partners have decided to liquidate their partnership by

installments. Cash is distributed to the partners at the end of

each month. A summary of the liquidation transactions follows:

January

a. $30,000 is collected on accounts receivable; balance is

uncollectible.

b. $25,000 received for the entire inventory.

c. $1,500 liquidation expense paid.

d. $45,000 paid to creditors.

e. $10,000 cash retained in the business at the end of the month.

February

f. $2,000 in liquidation expenses paid.

g. As part payment of his capital, Frank accepted an item of

special equipment that he developed, which had a book value of

$10,000. The partners agreed that a value of $14,000 should be

placed on this item for liquidation purposes.

h. $5,000 cash retained in the business at the end of the month.

March

i. $155,000 received on sale of remaining plant and equipment.

j. $1,000 liquidation expenses paid. No cash retained in the

business.

Required:

Prepare a statement of partnership realization and liquidation

with supporting schedules of safe payments to partners.